Get premium membership

Get premium membership and access questions with answers, video lessons as well as revision papers.

- At the beginning of year 1, a company grants 20 senior executives 1.000 share options, each based on two conditions. First, the executive has to...(Solved)

At the beginning of year 1, a company grants 20 senior executives 1.000 share options, each based on two conditions. First, the executive has to remain with the entity until the end of year 3. Second, the share options may not be exercised unless the share price has increased from Sh.100 at the beginning of year 1 to above Sh,130 at the end of year 3. If the share price is above Sh. 130 at the end of year 3. the share options may be exercised at any time during the next five years.

The entity applies a binomial option-pricing model, which takes into account the possibility that the share price will exceed Sh.130 at the end of year 3 (in this case the share options become exercisable) and the possibility that the share price will not exceed Sh.130 at the end of year 3 (and then the options will be forfeited). The company estimates the fair values of the share options with this market condition to be Sh.48 per option.

At the end of year 1, the company estimates the turnover of senior executives at 2%. In the second year, one executive leaves the company but the turnover estimate remains the same. During the third year, two executives leave the company.

Required:

The remuneration expense for each year in which an expense needs to be recorded indicating which account will be credited when the remuneration expense is recorded.

(Your answer should be in conformity with the requirements of 1FRS 2 - Share Based Payment).

Date posted: February 14, 2019.

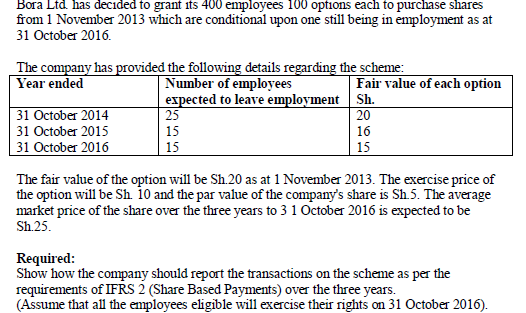

- Bora Ltd. has decided to grant its 400 employees 100 options each to purchase shares from 1 November 2013 which are conditional upon one still...(Solved)

Date posted: February 14, 2019.

- With reference to IFRS 2 'Share Based Payments', outline three types of share based payment transactions.(Solved)

With reference to IFRS 2 'Share Based Payments', outline three types of share based payment transactions.

Date posted: February 14, 2019.

- Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000,...(Solved)

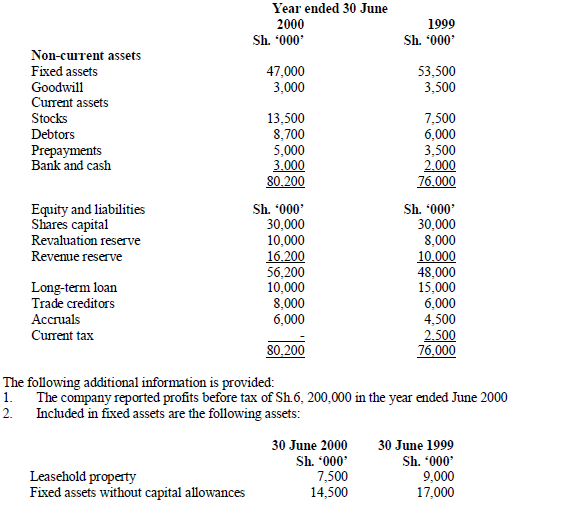

Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000, the company changed to deferred tax method and the new policy was to be applied retroactively to the accounts of the years ended 30 June 1999 and 2000.

The following are the balance sheets of the company for the two years ended 30 June 1999 and 2000 before incorporating tax expense for the year 2000

No acquisition or disposal of fixed assets took place in the year ended 30 June 2000

3. Written down value of fixed assets were Sh.22, 500,000 and Sh.18, 000,000 as at 30 June 1999 and 2000 respectively

4. Stocks as at 30 June 2000 are net of a general provision for price fluctuation of 10% of the cost. The provision is not allowed for tax purposes.

5. Accruals include leave passage provision of Sh.2, 500,000 as at 30 June 1999 and Sh.1, 800,000 as at June 2000

6. Prepayments for the year 2000 include Sh.2, 000,000 allowed as a deduction on computation of current tax.

7. Assets subjects to wear and tear allowance were first revalued in 1999 and revaluation repeated in 2000. No adjustments were made to the tax base of the assets following the revaluations.

8. Foreign exchange loss balances amounted to Sh.3, 600,000 and Sh.2, 800,000 on 30 June 1999 and 2000 respectively.

9. Donations in the year 2000 were Sh.5, 000,000.

10 Tax rates in 1999 and 2000 were 40% and 50% respectively.

Current tax for a year is paid on 15 September of the following financial year.

Required:

a) Current tax for the year ended 30 June 2000

b) Using the method recommended by the revised IAS 12, calculate deferred tax expense or income for the years 1999 and 2000

c) The current tax account, deferred tax account and revaluation account for the years 1999 and 2000

No acquisition or disposal of fixed assets took place in the year ended 30 June 2000

3. Written down value of fixed assets were Sh.22, 500,000 and Sh.18, 000,000 as at 30 June 1999 and 2000 respectively

4. Stocks as at 30 June 2000 are net of a general provision for price fluctuation of 10% of the cost. The provision is not allowed for tax purposes.

5. Accruals include leave passage provision of Sh.2, 500,000 as at 30 June 1999 and Sh.1, 800,000 as at June 2000

6. Prepayments for the year 2000 include Sh.2, 000,000 allowed as a deduction on computation of current tax.

7. Assets subjects to wear and tear allowance were first revalued in 1999 and revaluation repeated in 2000. No adjustments were made to the tax base of the assets following the revaluations.

8. Foreign exchange loss balances amounted to Sh.3, 600,000 and Sh.2, 800,000 on 30 June 1999 and 2000 respectively.

9. Donations in the year 2000 were Sh.5, 000,000.

10 Tax rates in 1999 and 2000 were 40% and 50% respectively.

Current tax for a year is paid on 15 September of the following financial year.

Required:

a) Current tax for the year ended 30 June 2000

b) Using the method recommended by the revised IAS 12, calculate deferred tax expense or income for the years 1999 and 2000

c) The current tax account, deferred tax account and revaluation account for the years 1999 and 2000

Date posted: February 14, 2019.

- The original IAS 12 did not refer explicitly to fair value adjustments made on a business combination and did not require an enterprise to recognize...(Solved)

The original IAS 12 did not refer explicitly to fair value adjustments made on a business combination and did not require an enterprise to recognize a deferred tax liability in respect of asset revaluations. The revised IAS 12 “income taxes” now requires deferred tax adjustments for these items and classifies them as temporary differences.

Required:

Explain the reasons why IAS 12 (revised) requires companies to provide for deferred taxation on revaluations of assets and fair value adjustments on a business combination irrespective of the tax effect in the current accounting period.

Date posted: February 14, 2019.

- Sumias Sugar Company Limited is in the process of finalizing its financial statements for the year ended 31 March 2003.

Its loss before taxation for the...(Solved)

Sumias Sugar Company Limited is in the process of finalizing its financial statements for the year ended 31 March 2003.

Its loss before taxation for the year is Sh.110 million. Included in this figure is a capital gain on the sale of some land: the capital gain was Sh.20 million. In arrival at loss figure, non-allowable expenses (for taxation purposes) of Sh.10 million had been incurred and a non-allowable depreciation charge of Sh.120 million had also been made. The equivalent tax-allowable capital allowances (wear and tear deductions and farm works deductions) figure was Sh.50 million.

The performance of the company depends very much on how much cheap sugar is imported tax free from COMESA region. However, the directors have an assurance from the Treasury that suitable action will be taken. Based on this assurance you have projected that profit in the year to 31 March 2004 will be Sh.150 million; there will be a non-allowable expenses of Sh.20 million in the year to 31 March 2004, and it is envisaged that a non-taxable capital gain will be made ofSh.10 million (you have included these in the projected profit of Sh.150 million). The capital allowances figure will be Sh.80 million and the depreciation charge will be Sh.130 million.

At 31 March 2002, there was a deferred tax liability due to accelerated capital allowances of Sh.500 million and a deferred tax asset on a tax loss brought forward of Sh.20 million. The rate of corporation tax throughout the period should be taken to be 30%. Tax losses can be carried backwards in Kenya, but can be carried forward indefinitely.

Required:

(a). Compare the tax liability for the year ended 31 March 2003 and the estimated liability for the year ending 31 March 2004.

(b). Show the part of the income statement from 'profit (loss) before tax' to 'profit (loss) after tax' and showing the tax charge or credit in its separate components and as a sub-total, for both years.

Date posted: February 14, 2019.

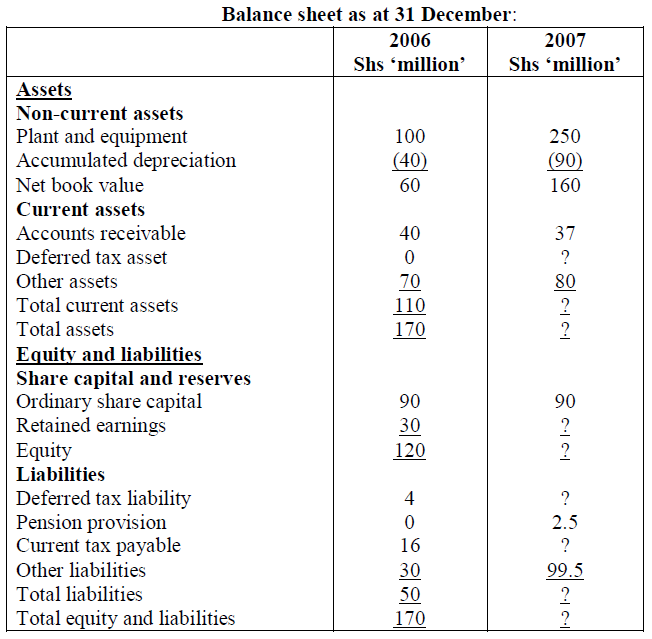

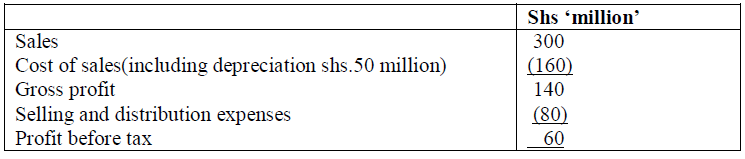

- The following incomplete balance sheet relate to Concorde Ltd for the years ended 31 December 2007:(Solved)

The following incomplete balance sheet relate to Concorde Ltd for the years ended 31 December 2007:

Additional information:

1. The company reported an accounting profit before tax of sh.60 million for the year ended 31 December 2007. This profit was arrived at as shown below:

Additional information:

1. The company reported an accounting profit before tax of sh.60 million for the year ended 31 December 2007. This profit was arrived at as shown below:

2. The company declared a dividend of sh.10 million for the year ended 31 December 2007.

3. Depreciation on plant and equipment is provided at the rate of 20% on straight-line basis. Plant and equipment qualify for capital allowances at the rate of 25% of cost on straight –line basis.

4. Accumulated tax depreciation as at 31 December 2006 was sh.50 million. On 1 February 2007, the company purchased additional costing sh.150 million. The company’s policy is to charge a full year’s depreciation in the year of purchase and none in the year of disposal.

5. Included in selling and distribution expenses is sh.5 million representing an expense which was disallowed by the tax authorities.

6. The company charged the income statement with sh.14 million representing pension costs for the year ended 31 December 2007. Sh.11.5 million of this amount was allowed for tax purposes.

7. The company made a general provision for bad debts of sh.3 million for the year ended 31 December 2007. There were no bad debts written off during the year.

8. On 31 July 2007, the company made a tax payment of sh.15 million.

9. Corporation rate of tax is 30%.

10. The company separately accounts for deductible and taxable temporary differences.

Required:

i) Determine the charge in the income statement for current tax and deferred tax expenses.

ii) Prepare the income statement showing the retained profit balance.

iii) Prepare the complete balance sheet.

2. The company declared a dividend of sh.10 million for the year ended 31 December 2007.

3. Depreciation on plant and equipment is provided at the rate of 20% on straight-line basis. Plant and equipment qualify for capital allowances at the rate of 25% of cost on straight –line basis.

4. Accumulated tax depreciation as at 31 December 2006 was sh.50 million. On 1 February 2007, the company purchased additional costing sh.150 million. The company’s policy is to charge a full year’s depreciation in the year of purchase and none in the year of disposal.

5. Included in selling and distribution expenses is sh.5 million representing an expense which was disallowed by the tax authorities.

6. The company charged the income statement with sh.14 million representing pension costs for the year ended 31 December 2007. Sh.11.5 million of this amount was allowed for tax purposes.

7. The company made a general provision for bad debts of sh.3 million for the year ended 31 December 2007. There were no bad debts written off during the year.

8. On 31 July 2007, the company made a tax payment of sh.15 million.

9. Corporation rate of tax is 30%.

10. The company separately accounts for deductible and taxable temporary differences.

Required:

i) Determine the charge in the income statement for current tax and deferred tax expenses.

ii) Prepare the income statement showing the retained profit balance.

iii) Prepare the complete balance sheet.

Date posted: February 14, 2019.

- Define the following terms as used in IAS 12-Income Taxes:

i) Deferred tax liabilities

ii) Deferred tax assets.

iii) Temporary differences.(Solved)

Define the following terms as used in IAS 12-Income Taxes:

i) Deferred tax liabilities

ii) Deferred tax assets.

iii) Temporary differences.

Date posted: February 14, 2019.

- Explain to a non-accountant the difference between the “income statement view” and the “balance sheet view” of deferred tax.

(Solved)

Explain to a non-accountant the difference between the “income statement view” and the “balance sheet view” of deferred tax.

Date posted: February 14, 2019.

- Maji Limited had a deferred tax liability of Sh. 105 million as at 1 June 2010. During the year ended 31 May 2011, the...(Solved)

Maji Limited had a deferred tax liability of Sh. 105 million as at 1 June 2010. During the year ended 31 May 2011, the company had the following items with regard to estimating deferred tax:

1. The carrying amount of property, plant and equipment as at 31 May 2011 was Sh.980 million. This included some buildings which were revalued upwards by Sh 50 million at 31 May 2010 which had a remaining useful life of 10 years at that date. The company's accounting policy is to treat revaluation surpluses as realized on disposal of the revalued assets. The tax base of property, plant and equipment as at 31 May 2011 was Sh 640 million.

2. Deferred development expenditure amounted to Sh.45 million at year end (Sh.40 million as at 31 May 2010). Sh.10 million of additional development expenditure was incurred during the year and the remaining difference between 2010 and 2011 figures relates to development expenditure amortized for products that have started being commercially produced. All development expenditure is allowed for tax purposes.

3. Included in current assets is an amount of Sh.40 million due in respect of some patent royalties on one of the company's older products which is now being produced by other companies. Patent royalties are taxed only when received.

4. The company’s tax rate proposals.

Required:

i) The deferred tax balance as at 31 May 2011 and the relevant journal entry.

ii) The directors of Maji Limited have proposed that deferred tax should be discounted and also provided on the share of post-acquisition profits in its subsidiary and associate companies.

Comment on these proposals.

Date posted: February 14, 2019.

- Lami Limited had a deferred tax liability as at I May 2011 of Sh.100 million. For the purposes of preparing financial statements for the year...(Solved)

Lami Limited had a deferred tax liability as at I May 2011 of Sh.100 million. For the purposes of preparing financial statements for the year ended 30 April 2012, the following additional information is available:

1. Property, plant and equipment has a carrying amount of Sh.1,200 million and a tax base of Sh.1,000 million. Some land and buildings were revalued upwards by Sh.50 million during the year ended 30 April 2012.

2. Intangible assets consisting of trade licences being amortized over five years had a carrying amount of Sh 60 million. This was allowed for tax purposes in full two years ago.

3. The company has available for sale financial assets with a carrying amount of Sh.20 million and financial assets at fair value through profit and loss of Sh. 10 million. Both financial assets reported losses in fair value of Sh.2 million each as at 30 April 2012.

4. Inventory is shown at the lower of cost and net realisable value. The cost is Sh.800 million while the net realizable value is Sh.780 million.

5. Receivables had a carrying amount of Sh.500,million after making an allowance for doubtful debt of Sh.20 million and an exchange gain of Sh.40 million (unrealized). Both the allowance and exchange gain arc not allowed for tax purposes.

6. Trade and other payable are stated at Sh. 900 million after making provision for discount of Sh. 10 million.

7. Assume a tax rate of 30%.

Required

i) Compute the relevant temporary differences.

ii) Show the journal entry to record changes in the deferred tax liability

Date posted: February 14, 2019.

- Justify the provision of deferred tax using temporary differences in the financial statements of a reporting entity.(Solved)

Justify the provision of deferred tax using temporary differences in the financial statements of a reporting entity.

Date posted: February 14, 2019.

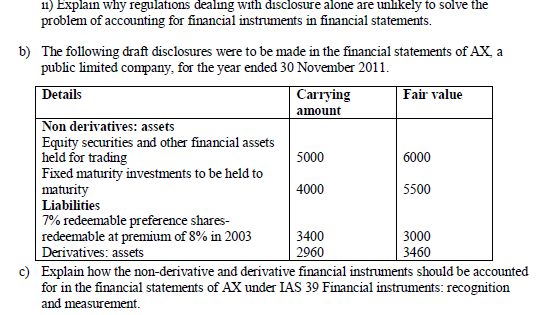

- Standard setters have been struggling for several years with the practical issues of the disclosure, recognition, and measurement of financial statements. The dynamic nature of...(Solved)

Standard setters have been struggling for several years with the practical issues of the disclosure, recognition, and measurement of financial statements. The dynamic nature of international markets has resulted in the widespread use of a variety of financial instruments, and present accounting rules struggle to deal effectively with the impact and risks of such instruments.

Required

a) i) Discuss the concerns about the accounting practices used for financial instruments which led to demands for an accounting standard.

Date posted: February 14, 2019.

- IAS 32 'Financial Instruments: Disclosure and Presentation' states that the purpose of the disclosures required by this standard is to provide information that will enhance...(Solved)

IAS 32 'Financial Instruments: Disclosure and Presentation' states that the purpose of the disclosures required by this standard is to provide information that will enhance understanding of the significance of on-balance-sheet and off-balance-sheet financial instruments to an enterprise’s financial position, performance and cash flow and assist in assessing the amounts, timing and certainty of future cash flows associated with those instruments. State and briefly describe three types of financial risks described in the standard, in relation to transactions in financial instruments.

Date posted: February 14, 2019.

- With reference to IAS 39(Financial Instruments: Recognition and Measurement), explain how financial instruments are initially recognized and subsequently measured in the books of a reporting...(Solved)

With reference to IAS 39(Financial Instruments: Recognition and Measurement), explain how financial instruments are initially recognized and subsequently measured in the books of a reporting entity.

Date posted: February 14, 2019.

- Redline Limited invested in 10% loan stock on 1 November 2007 given a par value of Sh. 20 million. The issuer of the loan stock...(Solved)

Red line Limited invested in 10% loan stock on 1 November 2007 given a par value of Sh. 20 million. The issuer of the loan stock was Borrow Limited. The loan stock was for five years and is to be settled on 31 October 2012. The loan stock was quoted but Red line Limited was to hold it to maturity. The effective interest rate on 1 November 2007 was 12% and this had not changed over the three years to 31 October 2010.

On 31 October 2010, Borrow Limited, after paying the annual interest, went into financial difficulties and Red line Limited estimated that interest would be received over the remaining two years but only half of the loan stock would be received on maturity. The loan stock was therefore impaired.

Required:

Explain how the loan stock in Borrow Limited will be reported in the financial statements for the year ended 31 October 2010.

Date posted: February 14, 2019.

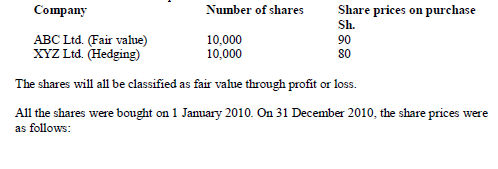

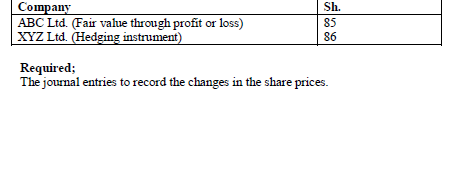

- Biz Ltd. invested in the shares of ABC Ltd. and XYZ Ltd. where the two were designated as a hedge based on cash.

The investments were...(Solved)

Biz Ltd. invested in the shares of ABC Ltd. and XYZ Ltd. where the two were designated as a hedge based on cash.

The investments were made up as follows:

Date posted: February 14, 2019.

- Explain the three main types of hedge as provided in IAS 39 (Financial Instruments: Recognition and Measurement) and their accounting treatment.(Solved)

Explain the three main types of hedge as provided in IAS 39 (Financial Instruments: Recognition and Measurement) and their accounting treatment.

Date posted: February 14, 2019.

- With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

(Solved)

With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

Date posted: February 14, 2019.

- The distinction between a provision and a contingent liability is irrelevant. Discuss.(Solved)

The distinction between a provision and a contingent liability is irrelevant. Discuss.

Date posted: February 14, 2019.

- Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will...(Solved)

Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will have on accounting for financial assets.

Date posted: February 14, 2019.

- (a) IAS 16: property, plant and equipment gives certain criteria to be satisfied before an item of property, plant and equipment should be recognized as...(Solved)

(a) IAS 16: property, plant and equipment gives certain criteria to be satisfied before an item of property, plant and equipment should be recognized as an asset. State these criteria and state the value at which the asset should be measured initially. Give six examples of directly attributable costs that could be included in the value and four examples of cost that should not be included in the value.

(b) Chumuki Supermarket Limited is a quoted company which runs 22 Supermarket stores throughout Kenya. 12 of these stores are situated in and around Nairobi and all 12 are supplied by Chumuki’s central go down situated in the industrial area of Nairobi. Pricing, marketing and human resources policies are decided centrally by Chumuki. All stores are managed in the same way and management run the business on a store-by-store profit basis.

Recently, the Githurai store has seriously under performed against its budget for the year ending 31 December 2000. Rising insecurity in the area together with difficulties in obtaining access to the store have seriously adversely affected its financial performance. The Githurai store together with the Kahawa store were purchased from Ruiru Superstores on 1 January 1998 for Sh.25 million and Sh.25 million and Sh.15 million respectively plus goodwill of Sh.8 million for both stores. The stores are being depreciated on the straightline method to nil residual value over 20 years the goodwill is being amortized to nil on the straight line basis over the same period. The Githurai store could be sold for Sh.15 million net. Its value in use is Sh.20 million. Management have performed a “bottom-up” test in relation to the goodwill and the purchase prices of the stores and are satisfied that a 'top-down' test is not needed.

Required:

State in detail how the impairment loss should be recognized for the Githurai cash-generating unit in the financial Statements for the year ending 31 December 2000: neither depreciation nor amortization has yet been charged for this period. State also the carrying value of the Githurai cash-generating unit after the impairment loss has been recognized. Ignore deferred tax.

Date posted: February 14, 2019.

- Identify and explain five indicators which show that an impairment loss to a fixed asset may have occurred.(Solved)

Identify and explain five indicators which show that an impairment loss to a fixed asset may have occurred.

Date posted: February 14, 2019.

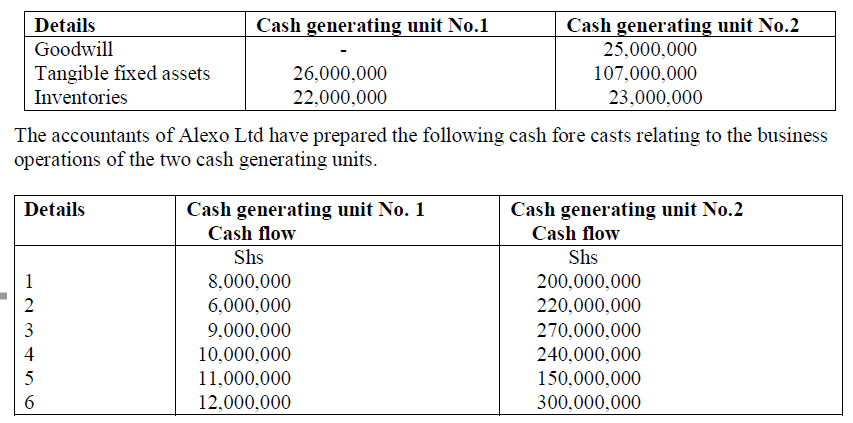

- The following information is provided relating to the carrying amount of the assets comprising the cash generating units of Alexo Ltd as at 30 September...(Solved)

The following information is provided relating to the carrying amount of the assets comprising the cash generating units of Alexo Ltd as at 30 September 2009:

Date posted: February 14, 2019.

- Briefly explain any three factors that may indicate that a financial asset is impaired.(Solved)

Briefly explain any three factors that may indicate that a financial asset is impaired.

Date posted: February 14, 2019.

- International Financial Reporting Standard (IFRS) 6 (Exploration for and Evaluation of Mineral Resources) provides guidance on how tangible and intangible assets used to explore the...(Solved)

International Financial Reporting Standard (IFRS) 6 (Exploration for and Evaluation of Mineral Resources) provides guidance on how tangible and intangible assets used to explore the existence of mineral resources can be accounted for and presented.

Required

Briefly explain four factors that indicate that such assets have been impaired.

Date posted: February 14, 2019.

- Explain how an impairment loss is measured according to IAS 36 (Impairment of Assets).(Solved)

Explain how an impairment loss is measured according to IAS 36 (Impairment of Assets).

Date posted: February 14, 2019.

- On 1 January 2006, Matopeni Primary School acquired a bus at a cost of Sh.6.000.000 to enable students from a nearby village commute to school...(Solved)

On 1 January 2006, Matopeni Primary School acquired a bus at a cost of Sh.6.000.000 to enable students from a nearby village commute to school free of charge. The school estimated that the bus had a useful life of 10 years. Or 31 December 2010, the bus sustained damage in a road accident requiring Sh. 1,200.000 to be restored to a usable condition. The restoration did not affect the useful life of the asset. The cost of a new bus to deliver a similar service was Sh.7, 500,000 as at 31 December 2010.

Required:

Evaluate the impairment loss attributable to the bus using the requirements of IPSAS 21 (Impairment of Non-Cash Generating Assets). Use the restoration cost approach.

Date posted: February 14, 2019.

- With reference to IPSAS 21 (Impairment of Non-Cash Generating Assets), explain the following terms:

i) Government business enterprise

ii) Carrying amount

iii) Recoverable service amount(Solved)

With reference to IPSAS 21 (Impairment of Non-Cash Generating Assets), explain the following terms:

i) Government business enterprise

ii) Carrying amount

iii) Recoverable service amount

Date posted: February 14, 2019.

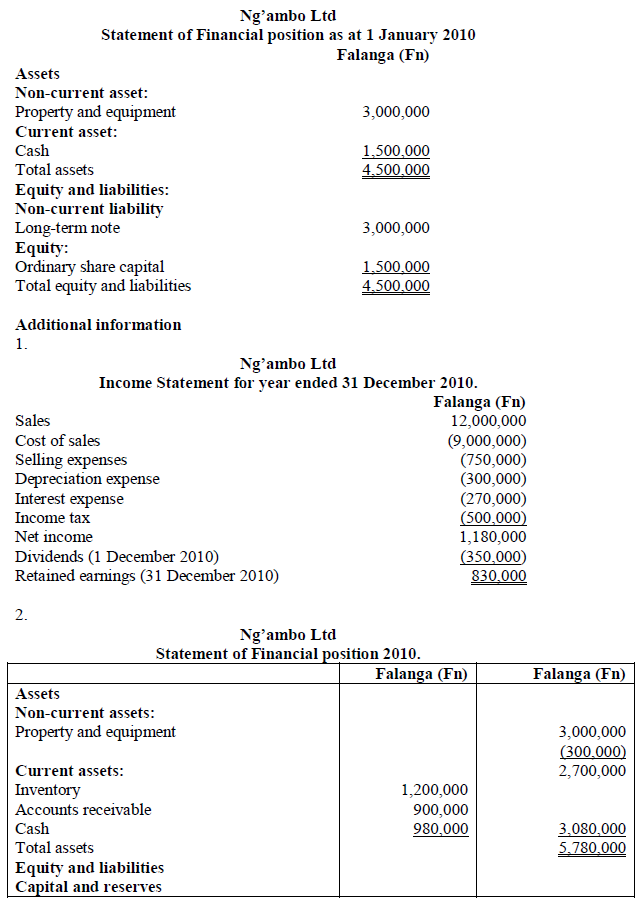

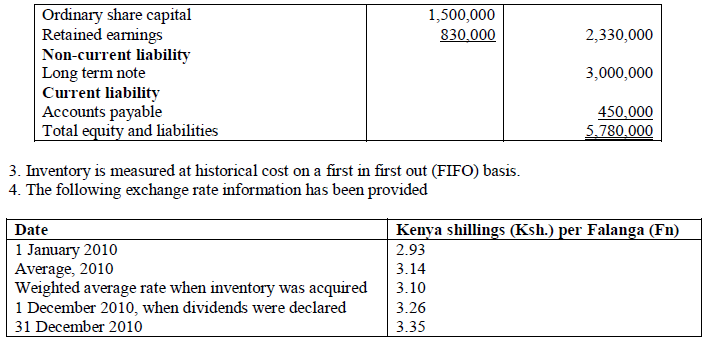

- a) In the context of International Accounting Standard (IAS) 21 (The Effects of Changes in Foreign Exchange Rates), explain two factors that should be considered...(Solved)

a) In the context of International Accounting Standard (IAS) 21 (The Effects of Changes in Foreign Exchange Rates), explain two factors that should be considered in determining an entity's functional currency.

b) Ufanisi Ltd. is a Kenyan-based company that uses the Kenya Shilling (Ksh) as its presentation currency. On 1 January 2010, the company established a wholly owned

subsidiary, Ng'ambo Ltd., in a foreign country known as Ugenini, In addition to Ufanisi Ltd. making an equity investment in the subsidiary, a long term note payable to an Ugenini bank was negotiated to purchase property and equipment. The currency used in Ugenini is known as the Falanga (Fn). The subsidiary began operations with the following statement of financial position as at 1 January 2010:

Required:

Translate the following financial statements of Ng'ambo Ltd. using the temporal method:

i) Income statement for the year ended 31 December 2010.

ii) Statement of financial position as at 31 December 2010.

Required:

Translate the following financial statements of Ng'ambo Ltd. using the temporal method:

i) Income statement for the year ended 31 December 2010.

ii) Statement of financial position as at 31 December 2010.

Date posted: February 13, 2019.