-

Omondi and Maina trade as partners in a brick manufacturing firm sharing profits and losses in the ration of 3:2 after charging their annual salaries...

(Solved)

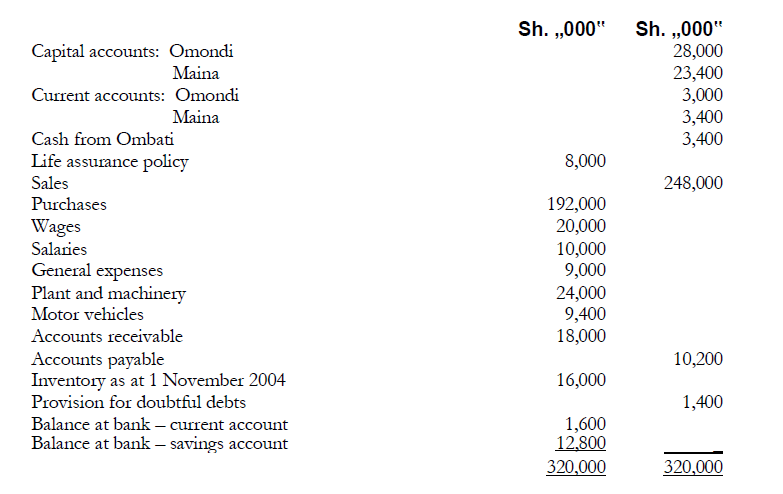

Omondi and Maina trade as partners in a brick manufacturing firm sharing profits and losses in the ration of 3:2 after charging their annual salaries of Shs. 2,500,000 each.

The trial balance extracted from their records as at 31 October 2005 were as follows:

Additional Information:

1. On 1 March 2005, the partners agreed to admit Ombati into the partnership on the

following terms:

- Ombati to pay sh.3,400,000 as his capital contribution.

- Ombati to be entitled to a salary of Sh.2,000,00 per annum and a share of 10% of the

profits.

Omondi and Maina were to continue sharing profits in their old ratios, but guaranteed that

Ombati‟s share of profits after salaries would not fall below Sh.1,200,000 per year.

Goodwill was agreed at Sh.2,100,000 but was not to be retained in the books.

2. The life assurance policy was surrendered on 1 December 2004 for Sh.9,500,000 and the

proceeds paid directly to Omondi and Maina in their profit sharing ratio. The necessary

entries in the current accounts were not made to account for this transaction.

3. The details of the savings bank account were as follows:

4. The actual balance on the bank savings account as at 31 October 2005 amounted to

Sh.400,000. The difference was due to drawings by Omondi Sh.3,400,000. Maina

Sh.3,000,000, Ombati Sh.1,200,000 and tax amounting to Sh.4,800,000 paid on behalf of the

partners (Omondi Sh.2,400,000, Maina Sh.2,000,000 and Ombati Sh.400,000).

5. Inventory as at 31 October 2005 was valued at Sh.19,000,000.

Depreciation is to be provided on plant and machinery at 10% per annum and on motor

vehicles at 20% per annum.

6. Provision for doubtful debts should be maintained at 5% of the balance in the debtors

ledger.

Required:

a) Trading, profit and loss and appropriation accounts for the year ended 31 October 2005.

b) Partners' current accounts.

c) Partners' capital accounts.

Date posted:

November 19, 2018

.

Answers (1)

-

Araka Ltd., a company dealing in retail products, extracted from the following trial balance as at 30 September 2005

(Solved)

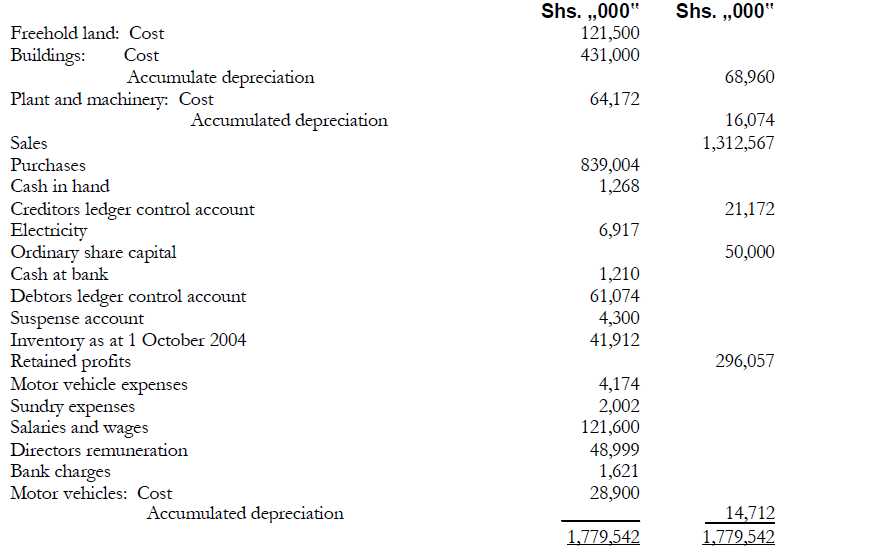

Araka Ltd., a company dealing in retail products, extracted from the following trial balance as at 30 September 2005:

Additional information:

1. Provision for doubtful debts should be made at 2% of the debtors ledger balances after

writing of bad debts amounting to Shs. 1,370,000.

2. The suspense account was analysed as follows:

3. The motor vehicle sold during the year had been purchased on 1 February 2002 for

Sh.6,500,000.

4. Bank statement as at 30 September 2005 showed bank charges of Sh.533,000. This had not

been recorded in the cash book.

5. The debtors ledger control account did not agree with the list of balances in personal

accounts. You ascertain that some invoices for October 2005 had been posted in the

personal accounts as at September 2005. The list of balances was overstated by

Sh.4,300,000.

6. Estimated corporation tax for the year ended 30 September 2005 was Sh.131,700,000.

7. The value of inventory as at 30 September 2005 was amounted to Sh.62,047,000.

8. The directors proposed to pay ordinary dividend of 10%.

9. The following petty cash expenditure had not been recorded:

Shs. „000‟

Motor vehicle expenses 412

Sundry expenses 91

Casual workers wages 36

10. Depreciation is provided at the following

rates: Buildings- 2% per annum on cost

Plant and machinery – 20% per annum on reducing balance

basis. Motor vehicle – 25% per annum on cost

Full year‟s depreciation is provided in the year of purchase and none in the year of disposal.

Required:

a) Trading profit and loss account for the year ended 30 September 2005.

b) Balance sheet as at 30 September 2005

Date posted:

November 19, 2018

.

Answers (1)

-

Identify with reasons, one party who may be interested in each of the following ratios:

(i) Current ratio

(ii) Net profit margin

(iii) Stock turnover

(Solved)

Identify with reasons, one party who may be interested in each of the following ratios:

(i) Current ratio

(ii) Net profit margin

(iii) Stock turnover

Date posted:

November 19, 2018

.

Answers (1)

-

Explain the importance of ratio analysis to a business enterprise

(Solved)

Explain the importance of ratio analysis to a business enterprise.

Date posted:

November 19, 2018

.

Answers (1)

-

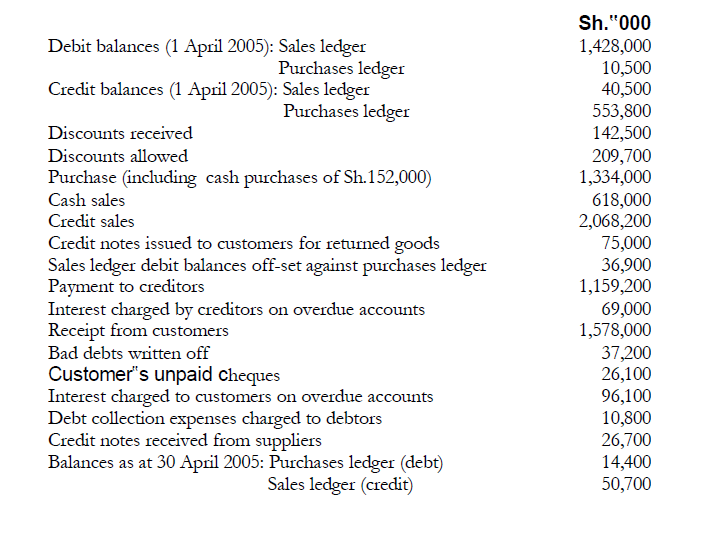

The following balances were extracted from the books of Katee Ltd. for the month of April 2005

(Solved)

The following balances were extracted from the books of Katee Ltd. for the month of April 2005:

(i) Sales ledger control account for the month ended 30 April 2005.

(ii) Purchases ledger control account for the month ended 30 April 2005.

Date posted:

November 19, 2018

.

Answers (1)

-

Explain the advantages of maintaining control accounts

(Solved)

Explain the advantages of maintaining control accounts.

Date posted:

November 19, 2018

.

Answers (1)

-

Faida Commercial Bank Ltd. offered 200,000 ordinary shares for sale to the public at a par value

of Sh.25 each on 1 April 2004, payable as...

(Solved)

Faida Commercial Bank Ltd. offered 200,000 ordinary shares for sale to the public at a par value

of Sh.25 each on 1 April 2004, payable as follows:

- On application, Sh.5 due on 15 April 2004

- On allotment, Sh.5 due on 30 April 2004

- On first call, Sh.7.50 due three months after allotment

- On second and final call, Sh.7.50 due three months after the first call.

Additional information:

1. The company received applications for 530,000 shares on the due dates. Applications for

30,000 shares were rejected and the application money refunded. The rest of the applicants

were allotted shares on a prorate basis.

2. One month after allotment, one shareholder of 2,000 shares remitted Sh.25,000 as calls in

advance. The rest of the calls were received on the due dates except for money due on

second and final call for Sh.8,000 shares which was paid three months late.

3. The surplus application monies were treated as calls in advance.

4. The company‟s articles of association provided for charging of interest on calls in arrears at

10% per annum.

Required:

Ledger accounts to record the above transactions.

Date posted:

November 19, 2018

.

Answers (1)

-

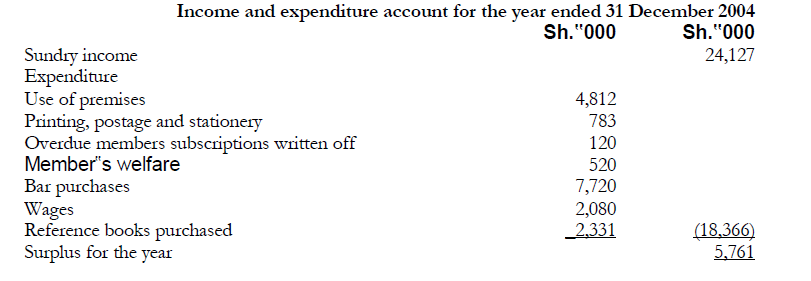

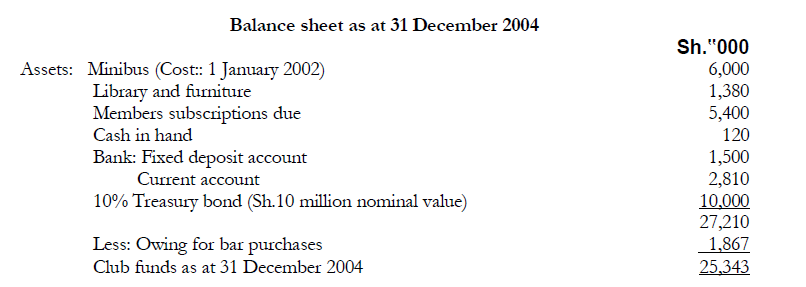

The following draft accounts have been prepared by the treasurer of Wasomaji Members Club

(Solved)

The following draft accounts have been prepared by the treasurer of Wasomaji Members Club:

Additional information:

1. The treasurer had little accounting knowledge and some figures appearing in the draft

accounts were incorrect.

2. The club‟s policy on outstanding subscriptions was to write off amounts

outstanding for a period exceeding five years. As at 1 January 2004, subscriptions

outstanding from members were Sh.3,120,000

3. The club‟s premises were purchased on 1 October 2004 for Sh.4 million.

This amount was posted to the use of premises account in the draft accounts.

4. The treasury bond was purchased for Sh.9.3 million on 1 January 2000 by utilizing

donations earmarked for a member‟s welfare fund. Up to 31 December

2003, the income received from this investment had been distributed to members. The

income for the year ended 31 December 2004 was included under sundry income as

resolved at the annual general meeting held on 10 April 2004.

5. The club runs a bar for the benefit of members. This bar sells stock at a mark-up of

30%. The income from bar sales amounting to Sh.9,927,000 was included under sundry

income. There was no opening stock as at 1 January 2004 and the club owed suppliers

Sh.1,625,000 as at 1 January 2004. Bar closing stock as at 31 December 2004 was not

ascertained.

6. The balance of the fixed deposit account as at 1 January 2004 amounted to Sh.1,500,000

reflected in the balance sheet as at 31 December 2004. No account was taken of interest

amounting to Sh.100,000 which had been credited to the fixed deposit during the year.

7. As at 1 January 2004, cash in hand was Sh.100,000 and the bank current account was

overdrawn by Sh.893,000.

8. The reference books purchased during the year are to be capitalized as part of the

library. Library and furniture are to be revalued to Sh.5,000,000

9. Depreciation is to be provided based on the cost of the assets as follows:

Club premises - 2% per annum

Minibus - 20% per annum

Required:

(a) Income and expenditure account for the year ended 31 December 2004.

(b) Balance sheet as at 31 December 2004.

Date posted:

November 19, 2018

.

Answers (1)

-

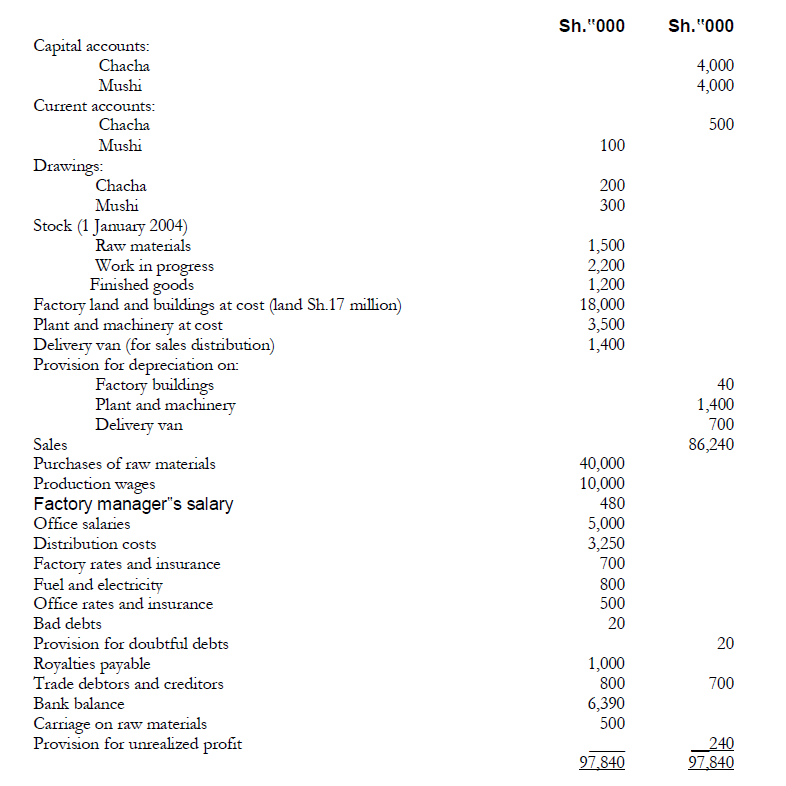

Chacha and Mushi are in partnership sharing profits and losses equally. They manufacture shoes whose brand name is "DAWO". Their trial balance as at 31...

(Solved)

Chacha and Mushi are in partnership sharing profits and losses equally. They manufacture shoes whose brand name is "DAWO". Their trial balance as at 31 December 2004 was as follows:

Additional information:

1. Stock at 31 December 2004 was valued as follows:

Sh. "000"

Raw materials 2,000

Work in progress 4,200

Finished goods 1,000

2. Insurance prepaid (31 December 2004)

Sh. "000"

Factory 200

Office 35

Rates owing (31 December 2004)

Sh."000"

Factory 500

Office 25

3. Depreciation is provided at the following rates:

Factory buildings – 2% per annum on cost

Delivery van – 25% per annum on cost

Plant and machinery – 20% per annum on cost

4. Provision for doubtful debts is to be maintained at 5% of the debtor‟s balance

at the end of the year.

5. Manufactured goods are transferred to the warehouse at cost plus 25% of factory profit

6. The partnership agreement has the following provisions:

(i) A commission of 10% to Mushi based on factory profit while Chacha is

entitled to a commission of 10% based on net profit from trading.

(ii) Partners are allowed interest on their fixed capitals at a rate of 10% per

annum.

(iii) Chacha had guaranteed Mushi a total income from the partnership of

not less than Sh.15,000,000 per annum.

Required:

(a) Manufacturing, trading and profit and loss and appropriation accounts for the year ended 31

December 2004.

(b) Balance sheet as at 31 December 2004.

Date posted:

November 19, 2018

.

Answers (1)

-

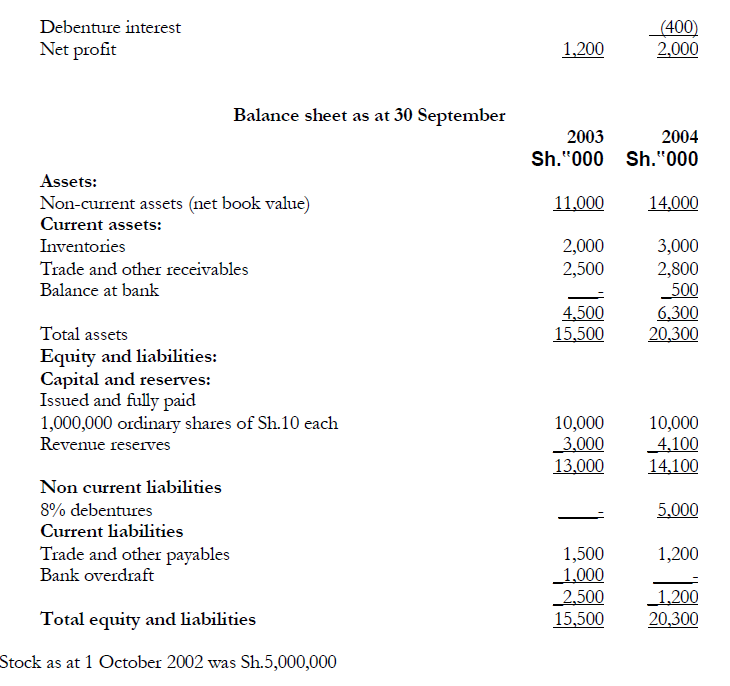

The summarized financial statements of Baraka Enterprises Ltd. are as follows

(Solved)

The summarized financial statements of Baraka Enterprises Ltd. are as follows:

Required:

(i) For each year, calculate the following:

(a) Gross profit margin

(b) Inventory turnover

(c) Return on equity

(d) Return on assets

(e) Acid test ratio

(f) Current ratio

(g) Financial leverage

(ii)Comment on the liquidity position of the company giving possible reasons for the change.

Date posted:

November 19, 2018

.

Answers (1)

-

Explain the meaning of prudence concept showing how this is applied in stock valuation

(Solved)

Explain the meaning of prudence concept showing how this is applied in stock valuation.

Date posted:

November 19, 2018

.

Answers (1)

-

The trial balance of Plastics Ltd as at 31 October 2004 is as follows

(Solved)

The trial balance of Plastics Ltd as at 31 October 2004 is as follows:

Additional information:

1. A building whose net book value is currently Sh.5 million is to be revalued to Sh.9 million

2. A final ordinary dividend of Sh.2 million is proposed.

3. The balance on the corporation tax for the current year is estimated at Sh.3 million.

Required:

(i) Income statement for the year ended 31 October 2004.

(ii) Balance sheet as at 31 October 2004.

Date posted:

November 19, 2018

.

Answers (1)

-

Distinguish reserves from share capital

(Solved)

Distinguish reserves from share capital.

Date posted:

November 19, 2018

.

Answers (1)

-

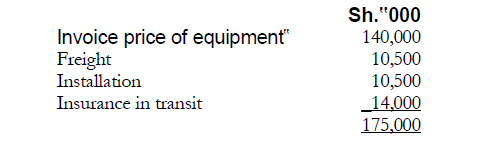

An extract from the balance sheet of Kimwa Construction Ltd as at 30 June 2003 showed the

following summary of property, plant and equipment

(Solved)

An extract from the balance sheet of Kimwa Construction Ltd as at 30 June 2003 showed the following summary of property, plant and equipment:

The following transactions took place during the year ended 30 June 2004:

1. The company incurred the following costs in acquiring new equipment

2. Property, plant and equipment disposed of during the year were as follows:

In addition, a new truck was acquired by trading in an old truck at an agreed value of

Sh.10.5 million and making an additional cash payment of Sh.15 million. The old truck

had cost Sh.15 million in July 2000.

3. The directors recommended a reclassification of some items of equipment to furniture.

These items had cost Sh.15 million and had accumulated depreciation of Sh.3 million.

4. The company‟s policy is to charge depreciation on a straight line basis at the following

rates:

Equipment 20% per annum

Furniture 12 ½ % per annum

Motor vehicles 30 % per annum

5. A full year‟s depreciation was charged in the year of acquisition but none in the year of disposal.

Required:

(a) Explain two other methods of charging depreciation that Kimwa construction Ltd could

have used.

(b) A property, plant and equipment disposal account for the year ended 30 June 2004.

(c) A property, plant and equipment movement Schedule for the year ended 30 June 2004

Date posted:

November 19, 2018

.

Answers (1)

-

On 31 October 2004, the cashbook of Mwea Enterprises Ltd. Showed a debit balance of Sh.1,710,000. This did not agree with the balance shown in...

(Solved)

On 31 October 2004, the cashbook of Mwea Enterprises Ltd. Showed a debit balance of Sh.1,710,000. This did not agree with the balance shown in the bank statement.

Upon investigation, the accountant discovered the following errors:

1. A cheque paid to Kindaruma for Sh.306,000 had been entered in the cashbook as

Sh.387,000

2. Cash paid into the bank by a customer for Sh.90,000 had been entered in the

cashbook as Sh.81,000

3. A transfer of Sh.1,110,000 to Central Savings Bank had not been posted to the cash

book.

4. A receipt of Sh.9,000 shown in the bank statement had not been posted in the

cashbook.

5. Cheques drawn amounting to Sh.36,000 had not been paid into the bank.

6. The cash book balance had been incorrectly brought down at 1 November 2003 as

a debit balance of Sh.1,080,000 instead of a debit balance of Sh.990,000

7. Bank charges of Sh.18,000 do not appear in the cash book.

8. A receipt of Sh.810,000 paid into the bank on 31 October 2004 appeared in the

bank statement on 1 November 2004.

9. A standing order of Sh.27,000 had not been recorded in the cash book.

10. A cheque for Sh.45,000 previously received and paid into the bank had been

returned by the customer‟s bank marked “account closed”.

11. The bank received a direct debit of Sh.90,000 from an anonymous customer.

12. Cheques banked had been totaled at Sh.135,000 instead of Sh.153,000.

13. A cheque drawn in favour of Nyaga for Sh.120,000 had been entered on the debit

side of the cashbook.

Required;

(i) Adjusted cash book as at 31 October 2004.

(ii) A bank reconciliation statement as at 31 October 2004.

Date posted:

November 19, 2018

.

Answers (1)

-

The bank statement and cashbook balances should agree, but sometimes these balances may not agree:

Required:

Discuss this statement and explain why it is important to prepare...

(Solved)

The bank statement and cashbook balances should agree, but sometimes these balances may not agree:

Required:

Discuss this statement and explain why it is important to prepare a bank reconciliation statement.

Date posted:

November 19, 2018

.

Answers (1)

-

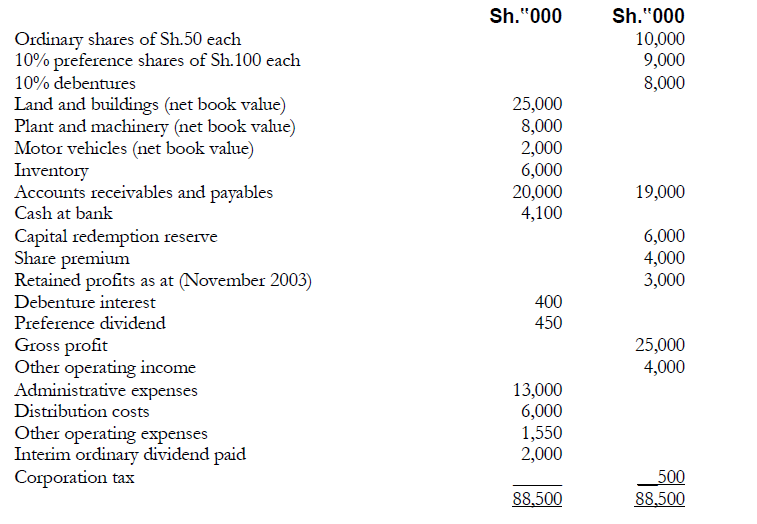

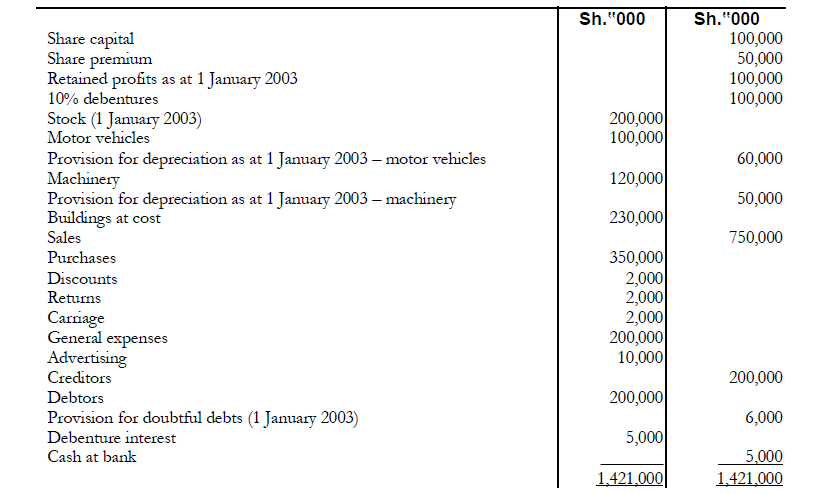

The book keeper of Bidii Ltd. prepared the following trial balance as at 31 December 2003:

(Solved)

The book keeper of Bidii Ltd. prepared the following trial balance as at 31 December 2003:

Additional information:

1. In an effort to simplify the accounting process, the book keeper posted both discounts

received and discounts allowed to the discounts account. He has also posted both

returns inwards and returns outwards to the returns accounts, and both carriage inwards

and carriage outwards to the carriage account. Discounts received, returns outwards and

carriage outwards were as follows:

Sh.

Discounts received 1,000,000

Returns outwards 1,000,000

Carriage outwards 1,000,000

2. The following items are already included in general expenses:

- Rates for the 12 months to 31 March 2004, Sh.4,000,000

- Insurance for the 12 months to 31 December 2003 amounted to Sh.2,000,000.

Half of this amount relates to the managing director‟s private expenses.

3. Accountancy fees of Sh.1,000,000 should be provided for

4. A debtor for Sh.20,000,000 has been declared bankrupt. The provision for doubtful

debts is to be made at 5% of the debtors.

5. Dividends of Sh.10,000,000 have been proposed by the board of directors.

6. Stock as at 31 December 2003 is valued at Sh.180,000,000

7. Depreciation of Sh.20,000,000 is to be provided on the motor vehicles and

Sh.10,000,000 on the machinery. The buildings are to be revalued upwards by

Sh.30,000,000

Required:

(a) Trading and profit and loss and appropriation accounts for the year ended 31 December

2003.

(b) Balance sheet as at 31 December 2003

Date posted:

November 17, 2018

.

Answers (1)

-

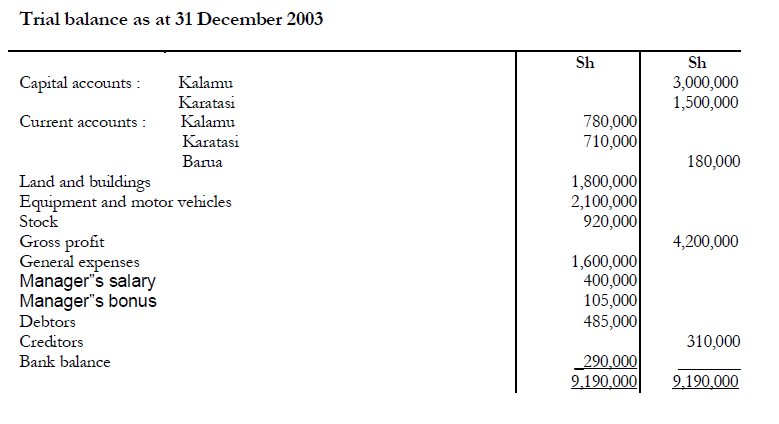

Kalamu and Karatasi have been trading in partnership for several years, sharing profits and

losses equally after allowing interest on their capitals at the rate of...

(Solved)

Kalamu and Karatasi have been trading in partnership for several years, sharing profits and

losses equally after allowing interest on their capitals at the rate of 8% per annum. On 1

September 2003, the manager of their business, Barua, was admitted as a partner and was to

share one fifth of the profits after interest on capital Kalamu and Karatasi were to share the

balance of the profits equally but guaranteed that Barua‟s share would not fall below

Sh.600,000 per annum.

Barua was not required to introduce any capital at the date of admission but agreed to retain

Sh.150,000 of his profit share at the end of each financial year to be credited to his capital

account until the balance reached Sh.750,000. Until that time, no interest was to be allowed on

his capital.

Goodwill was agreed at Sh.1,500,000 at 1 September 2003, but was not to be maintained in the

accounts. Land and buildings were professionally valued at Sh.2,840,000 on the same date while

the book value of equipment and motor vehicles was to be reduced to Sh.1,500,000 as at that

date.

Barua was previously entitled to a bonus of 5% of the gross profit. This bonus was payable half yearly.

The manager's bonus and the manager's salary were to cease when he became a partner.

The trial balance below was extracted as at 31 December 2003. No adjustments had yet been

made in respect of Barua's admission and the amount he introduced as his

contribution for goodwill had been posted to his current account. The drawings of all the

partners had been charged to their current accounts.

Additional information:

1. It is assumed that gross profit and general expenses accrued evenly throughout the year

except that Sh.100,000 of the general expenses relate to a bad debt that arose in the period

after Barua‟s admission. The balance of the general expenses accrued evenly.

2. Depreciation is to be charged on equipment and motor vehicles at the rate of 20% per

annum on the book value. No depreciation is to be charged on land and buildings.

Required:

(a) Profit and loss account for the year ended 31 December 2003

(b) Partner‟s capital accounts as at 31 December 2003.

(c) Partner‟s current accounts as at 31 December 2003.

Date posted:

November 17, 2018

.

Answers (1)

-

The trial balance of Amanda Ltd as at 30 April 2004 did not balance. On investigation, the

following errors were discovered:

1. A loan of Sh.2,000,000 from...

(Solved)

The trial balance of Amanda Ltd as at 30 April 2004 did not balance. On investigation, the

following errors were discovered:

1. A loan of Sh.2,000,000 from one of the directors has been correctly entered in the

cashbook but posted to the wrong side of the loan account.

2. The purchase of a motor vehicle on credit fro Sh.2,860,000 had been recorded by

debiting the supplier‟s account and crediting the motor expenses account.

3. A cheque for Sh.80,000 from Ogola, a customer to whom goods are regularly

supplied on credit, was correctly entered in the cashbook but was posted to the

credit of bad debts recovered account in the mistaken belief that it was a receipt

from Agola, a customer whose debt had been written off three years earlier.

4. In reconciling the company‟s cash book with the bank statement, it was found

that bank charges of Sh.38,000 had not been entered in the company‟s records.

5. The totals of the cash discount columns in the cashbook for the month of April

2004 had not been posted to the respective discount accounts.

The figures were:

Sh.

Discounts allowed 184,000

Discounts received 397,000

6. The company had purchased some plant on 1 March 2003 for Sh.1,600,000. The

payment was correctly entered in the cashbook but was debited to the plant repairs account. Depreciation on such plant is provided for at the rate of 20% per annum on cost.

Required:

(i) Journal entries with narrations to correct the above errors.

(ii) Suspense accounts showing the original difference

Date posted:

November 17, 2018

.

Answers (1)

-

Briefly explain the following types of errors:

(i) Error of commission

(ii) Error of principle

(iii) Complete reversal of entries

(iv) Compensating errors

(Solved)

Briefly explain the following types of errors:

(i) Error of commission

(ii) Error of principle

(iii) Complete reversal of entries

(iv) Compensating errors

Date posted:

November 17, 2018

.

Answers (1)