i) Royalty income

- Royalty income for resident individuals is taxed in two stages;

- First a withholding tax of 5% of the gross royalty income is imposed

- Then gross royalty less allowable expenses is added to other incomes of a taxpayer and taxed, and a relief of withholding tax earlier deducted is set off against tax computed.

ii) Loan from an employer

- Up to 11 June 1998, low interest benefit was taxed on the employee at the difference between the interest rate charged and prescribed commissioner‘s rate.

- With effect from 12 June 1998, loans at a rate below the 91 Day Treasury bill rate, (below market interest rate) will attract a fringe benefit tax payable by the employer at the corporate tax rate of 30%.

Wilfykil answered the question on February 13, 2019 at 08:39

-

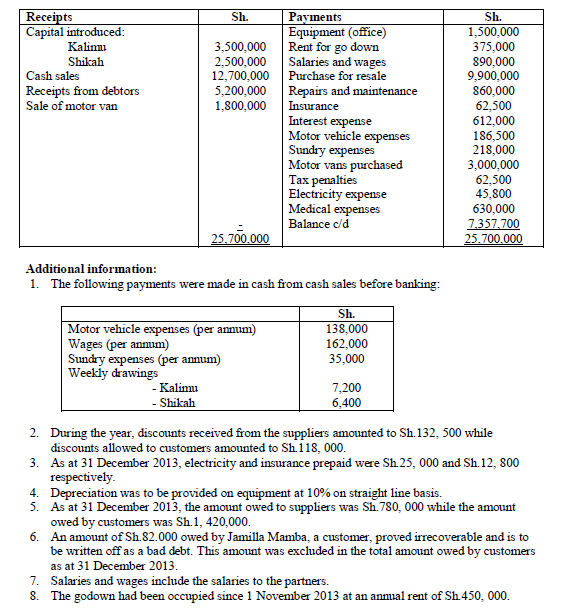

Kalimu and Shikah commenced trading in partnership as Kashi Enterprises on 1 January 2013. They share profits and losses in the ratio of 2:1 for...

(Solved)

Kalimu and Shikah commenced trading in partnership as Kashi Enterprises on 1 January 2013. They share profits and losses in the ratio of 2:1 for Kalimu and Shikah respectively. The partners were to receive monthly salaries of Sh.18, 000 and Sh.22,000 for Kalimu and Shikah respectively. The partnership did not maintain a complete set of accounting records.

The following summary of the bank statements for the year ended 31 December 2013 has been presented to you.

Required:

(i) Adjusted partnership profit or loss for the year ended 31 December 2013.

(ii) Distribution schedule of the profit or loss calculated in (i) above.

Date posted:

February 13, 2019

.

Answers (1)

-

Explain four reasons why a country might prefer a multiple tax system over a single tax system

(Solved)

Explain four reasons why a country might prefer a multiple tax system over a single tax system

Date posted:

February 13, 2019

.

Answers (1)

-

Identify four ways in which an individual or firm could engage in ?tax avoidance

(Solved)

Identify four ways in which an individual or firm could engage in ―tax avoidance

Date posted:

February 13, 2019

.

Answers (1)

-

Argue six cases against indirect taxes imposed in your country

(Solved)

Argue six cases against indirect taxes imposed in your country

Date posted:

February 13, 2019

.

Answers (1)

-

Outline four sources of revenue for a county or local authority

(Solved)

Outline four sources of revenue for a county or local authority

Date posted:

February 13, 2019

.

Answers (1)

-

Discuss four factors that influence tax shifting in an economy

(Solved)

Discuss four factors that influence tax shifting in an economy

Date posted:

February 13, 2019

.

Answers (1)

-

Explain the term "set-off tax" as used in taxation

(Solved)

Explain the term "set-off tax" as used in taxation

Date posted:

February 13, 2019

.

Answers (1)

-

Distinguish between a "single tax system" and a "multiple tax system".

(Solved)

Distinguish between a "single tax system" and a "multiple tax system".

Date posted:

February 13, 2019

.

Answers (1)

-

Suggest four ways on how tax policy can be used to promote the growth of small and medium enterprises (SMEs) in your country

(Solved)

Suggest four ways on how tax policy can be used to promote the growth of small and medium enterprises (SMEs) in your country

Date posted:

February 13, 2019

.

Answers (1)