A taxpayers is required to pay taxes on the incomes as per the assessment either self-assessment or originating from the commissioner.

However where a taxpayer feels that the income as per an assessment arising from the commissioner- is too high, they have a right under the income tax Act to object to such an assessment.

A taxpayer shall not be allowed to appeal against his or her own assessment. The only remedy against self-assessment will be a relief of error or mistakes.

An objection raised by the tax payer is referred to as a notice of objection. For such a notice to be treated as valid it must be:

a) Made in writing

b) Must state ground of objection i.e. the reasons why the objection is launched

c) Must be made with in 60days from the date of service of the notice of assessment i.e. plus 10 more days' i.e. days of service.

The 10 days of service are taken to be the maximum time that mail will have been delivered to any address in Kenya or abroad

These are objections made after statutory period have expired. Such a notice shall be accepted by the commissioner provided that the taxpayer can demonstrate that he was prevented from objecting in time due to reasons such as:-

a) Sickness

b) Absence from Kenya

c) Any other reasonable cause e.g. letter being posted to the wrong address.

On receipt of a rated valid notice objection the commissioner has the following objection:-

- He can amend the assessment in accordance with the objection i.e. the commissioner may agree with the taxpayer objection.

- He can amend the assessment in light of objection with some adjustment with both parties agreeing.

- He can amend the assessment in light of taxpayer's objection with adjustment of the taxpayer not agreeing with the adjustments i.e. A non-agreement amended adjustment is issued.

- The commissioner may refuse to amend the assessment and issue a notice to the taxpayer which confirms the disputed assessment.

Note: For 3 and 4 above, taxpayer should be notified of his rights to appeal to the local committee against commissioner's decision.

- The commissioner can take no action where the taxpayer decides to withdraw from the notice of objection.

A taxpayer is aggrieved in the manner in which a notice of the objection against an assessment has been dealt with by the commissioner the tax payer has a further recourse to appeal to the appellate bodies" i.e. Bodies established under the income

Tax Act through any other courts in Kenya.

Wilfykil answered the question on February 25, 2019 at 10:29

-

Explain five types of notices of assessment

(Solved)

Explain five types of notices of assessment

Date posted:

February 25, 2019

.

Answers (1)

-

What are the contents of a notice of assessment?

(Solved)

What are the contents of a notice of assessment?

Date posted:

February 25, 2019

.

Answers (1)

-

Write brief notes on back duty.

(Solved)

Write brief notes on back duty.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain the meaning of tax evasion

(Solved)

Explain the meaning of tax evasion

Date posted:

February 25, 2019

.

Answers (1)

-

It may be advantageous for a trader whose turnover is below the legislated turnover limits under the sixth schedule to the V AT Act to...

(Solved)

It may be advantageous for a trader whose turnover is below the legislated turnover limits under the sixth schedule to the V AT Act to register for VAT voluntarily. Under what circumstances could this be beneficial?

Date posted:

February 25, 2019

.

Answers (1)

-

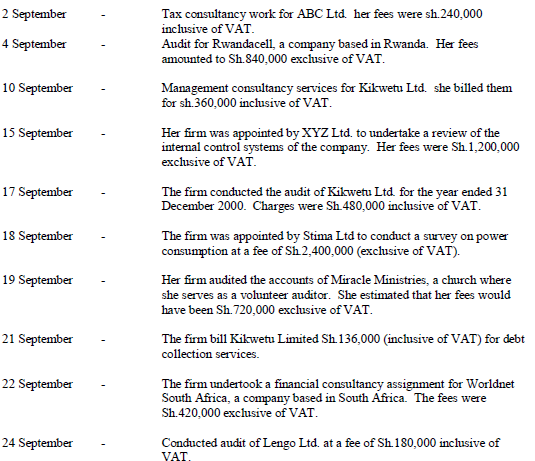

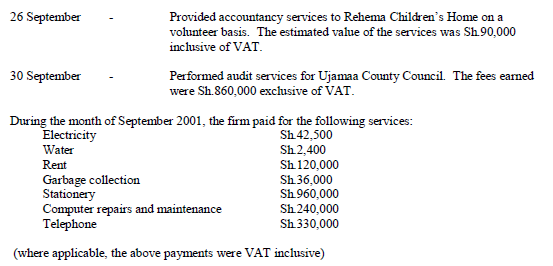

Mrs. Carol Wasike is a practicing accountant working under the style and name of Wasike and Associates. Her firm is registered for Value Added Tax...

(Solved)

Mrs. Carol Wasike is a practicing accountant working under the style and name of Wasike and Associates. Her firm is registered for Value Added Tax (VAT). During the month of September 2001, she undertook and completed the following assignments:

Required:

(a) Prepare a VAT Account for Wasike and Associates for the month of September 2001.

(b) The VAT you have computed in (a) above, was paid on 22 October 2001 since 20 October was on a Saturday. The VAT return was also submitted on the same day. How much additional tax would be payable, if any?

(c) Kikwetu Limited was the subject of a creditors voluntary winding up and the appropriate resolution was passed on 1 April 2002. By that time the company paid Wasike and Associates only Sh.240,000 for services rendered. Assuming that all the conditions for the refund of bad debt relief are met, calculate the amount of VAT bad debt relief.

Date posted:

February 25, 2019

.

Answers (1)

-

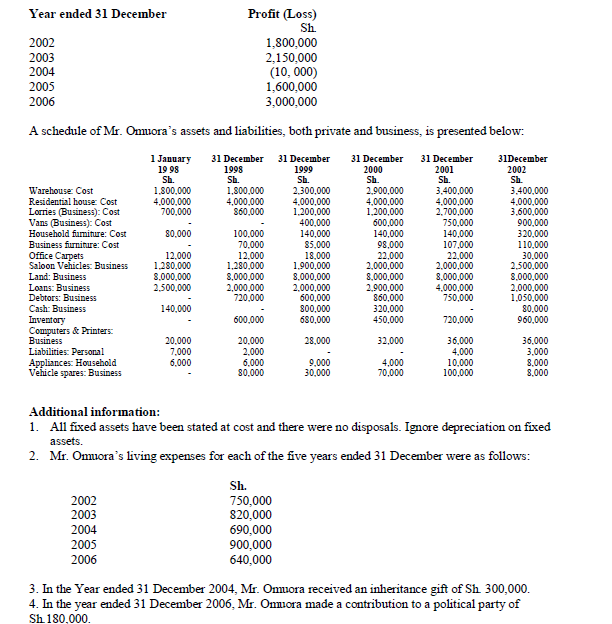

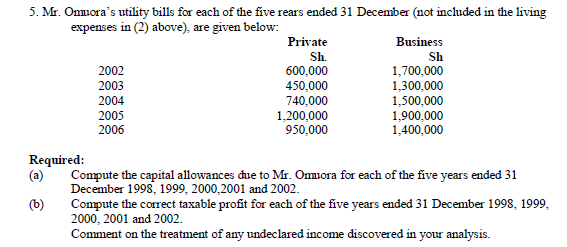

Mr. Joseph Omuora commenced a soft drinks distribution business on 1 January 1998. He has not been maintaining proper books of account and the Commissioner...

(Solved)

Mr. Joseph Omuora commenced a soft drinks distribution business on 1 January 1998. He has not been maintaining proper books of account and the Commissioner of Income Tax has raised doubts about the accuracy of the annual tax returns submitted by him.

You have been appointed to estimate the correct amounts of taxable incomes for the years ended 31 December 1998, 1999, 2000, 2001 for comparison with those disclosed in the annual returns. These returns had disclosed the following profits or losses:

Date posted:

February 25, 2019

.

Answers (1)

-

Mediner Ltd. deals in a variety of goods in the month of September 2004, the Company accountant recorded the following transactions (exclusive of VAT):

(Solved)

Mediner Ltd. deals in a variety of goods in the month of September 2004, the Company accountant recorded the following transactions (exclusive of VAT):

The accountant believes that the allocative method is the best in restricting the input VAT deductible against output VAT. The accountant is also of the opinion that on average, twenty percent of the standard rate purchases were sold as standard rate sales.

Required:

Compute the input VAT deductible against output VAT using the allocative method.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain how section 19 (1) of the VAT Act, on recovery of “tax due and payable from a person who owes money to the tax...

(Solved)

Explain how section 19 (1) of the VAT Act, on recovery of “tax due and payable from a person who owes money to the tax payer” may be enforced by the commissioner.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain the requirements of an application for refund of VAT paid in respect of Bad debts.

(Solved)

Explain the requirements of an application for refund of VAT paid in respect of Bad debts.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain briefly the meaning of “goods subject to customs control” under the Customs and Excise Act (Cap. 472)

(Solved)

Explain briefly the meaning of “goods subject to customs control” under the Customs and Excise Act (Cap. 472)

Date posted:

February 25, 2019

.

Answers (1)

-

Name four incentives given by the government to encourage the growth of capital market in Kenya

(Solved)

Name four incentives given by the government to encourage the growth of capital market in Kenya

Date posted:

February 25, 2019

.

Answers (1)

-

Explain the term “thin capitalization.”

(Solved)

Explain the term “thin capitalization.”

Date posted:

February 25, 2019

.

Answers (1)

-

List four circumstances under which duty paid on imports is refundable

(Solved)

List four circumstances under which duty paid on imports is refundable

Date posted:

February 25, 2019

.

Answers (1)

-

Under what circumstances are imported goods considered to have been dumped in your country.

(Solved)

Under what circumstances are imported goods considered to have been dumped in your country.

Date posted:

February 25, 2019

.

Answers (1)

-

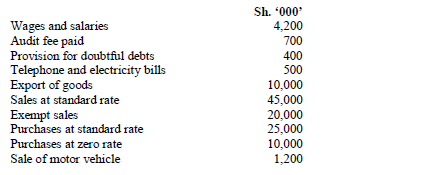

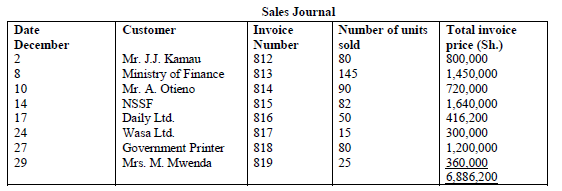

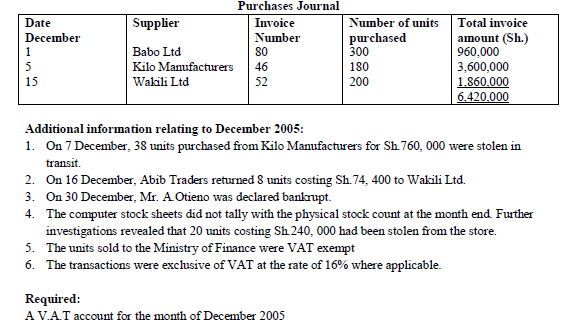

The following details were extracted from the books of Abib Traders. VAT No.A11146789P for the month of December 2005.

(Solved)

The following details were extracted from the books of Abib Traders. VAT No.A11146789P for the month of December 2005.

Date posted:

February 25, 2019

.

Answers (1)

-

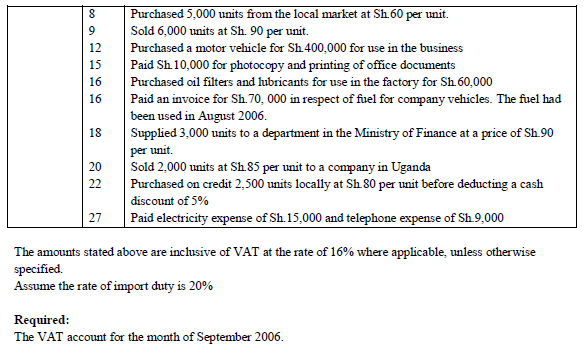

Zawadi Ltd is a Nakuru based company dealing in a variety of VAT designated goods. The following transactions were recorded for the month of September...

(Solved)

Zawadi Ltd is a Nakuru based company dealing in a variety of VAT designated goods. The following transactions were recorded for the month of September 2006:

Date posted:

February 25, 2019

.

Answers (1)

-

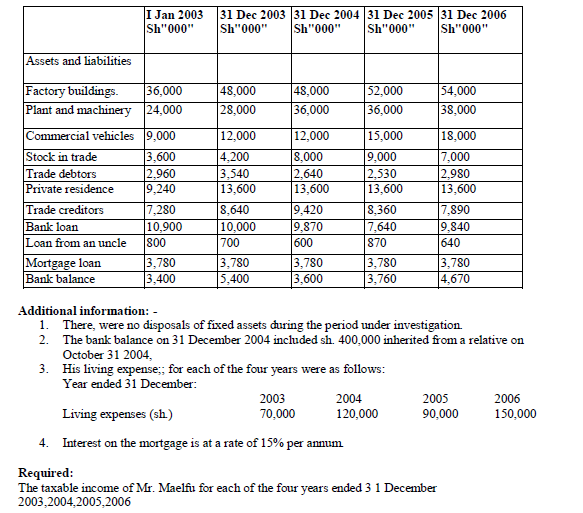

Mr. Dickson Maelfu is a-businessman with interests in the manufacturing sector. He is facing a back duty investigation by the revenue authority which suspects that...

(Solved)

Mr. Dickson Maelfu is a-businessman with interests in the manufacturing sector. He is facing a back duty investigation by the revenue authority which suspects that he has been under - declaring income four years from year 2003 to year 2006.

You are the head of the team from the revenue authority conducting this investigation. Maelfu has submitted to you records of his private and business assets and liabilities from 1 January 2003 to 31 December 2006 as shown below.

Date posted:

February 25, 2019

.

Answers (1)

-

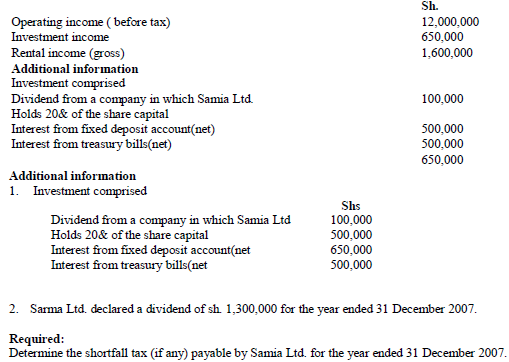

Samia Ltd. reported the following income during the year ended 31 December 2007:

(Solved)

Samia Ltd. reported the following income during the year ended 31 December 2007:

Date posted:

February 25, 2019

.

Answers (1)

-

Briefly explain two conditions under which bad debt relief on VAT might be provided

(Solved)

Briefly explain two conditions under which bad debt relief on VAT might be provided

Date posted:

February 25, 2019

.

Answers (1)