-Fixed Manufacturing Costs are not divorced from production. They are very significant

especially in the modern automated industry. Thus, they should be included in the cost of

production and consequently in stock valuation.

- Where production is constant but sales fluctuate (which is what happens in real business life),

the net profit does not fluctuate as significantly as in marginal costing.

- Where stock building or piling is necessary part of operations, (for example, in timber

seasoning) inclusion of fixed costs in stock valuation is necessary and desirable for statements

to show a true and fair view. Otherwise, a series of fictitious losses will be shown in earlier

periods, only to be offset eventually by excessive profits when the goods are sold.

- Calculating the total costs of producing a good makes a firm to set a selling price that is NOT

below total cost. Calculating marginal cost and contribution may make a firm to set prices

that are below total cost while still producing some contribution.

- Matching concepts advocates for absorption costing: Costs and revenues must be matched in

the period when revenue arises, and not when costs are incurred. SSAP (Stocks and Work in

Progress) advocates for the matching concept and recommends that stock valuations must

include production overheads incurred in the normal course of business even if not time

related.

marto answered the question on February 26, 2019 at 09:41

-

Factors to consider in make -or - buy decisions

(Solved)

Factors to consider in make -or - buy decisions

Date posted:

February 26, 2019

.

Answers (1)

-

What is the role of cost accounting in decision making

(Solved)

What is the role of cost accounting in decision making.

Date posted:

February 26, 2019

.

Answers (1)

-

Factors influencing cost estimation method used by a manufacturing company

(Solved)

Factors influencing cost estimation method used by a manufacturing company

Date posted:

February 26, 2019

.

Answers (1)

-

What are the features of process costing.

(Solved)

What are the features of process costing.

Date posted:

February 26, 2019

.

Answers (1)

-

Give the functions of budgets.

(Solved)

Give the functions of budgets.

Date posted:

February 26, 2019

.

Answers (1)

-

List the ways to improve cash management.

(Solved)

List the ways to improve cash management.

Date posted:

February 26, 2019

.

Answers (1)

-

What are the causes of difference in cost and financial accounts

(Solved)

What are the causes of difference in cost and financial accounts

Date posted:

February 26, 2019

.

Answers (1)

-

Give the causes of stock discrepancies.

(Solved)

Give the causes of stock discrepancies.

Date posted:

February 26, 2019

.

Answers (1)

-

Give the factors considered in selecting overhead absorption rate

(Solved)

Give the factors considered in selecting overhead absorption rate

Date posted:

February 26, 2019

.

Answers (1)

-

Give the disadvantages of overstocking:

(Solved)

Give the disadvantages of overstocking:

Date posted:

February 26, 2019

.

Answers (1)

-

Distinguish between the following Incremental costs and Marginal costs,cost centres and object centres,job costing system and process costing system,relevant cost and relevant range,

(Solved)

Distinguish between the following Incremental costs and Marginal costs,cost centres and object centres,job costing system and process costing system,relevant cost and relevant range,

Date posted:

February 26, 2019

.

Answers (1)

-

Give the assumptions of break-even analysis.

(Solved)

Give the assumptions of break-even analysis.

Date posted:

February 26, 2019

.

Answers (1)

-

Give the classification of costs.

(Solved)

Give the classification of costs.

Date posted:

February 26, 2019

.

Answers (1)

-

Give the assumption of the economic order quantity (EOQ) model.

(Solved)

Give the assumption of the economic order quantity (EOQ) model.

Date posted:

February 26, 2019

.

Answers (1)

-

Explain the term target costing.

(Solved)

Explain the term target costing.

Date posted:

February 26, 2019

.

Answers (1)

-

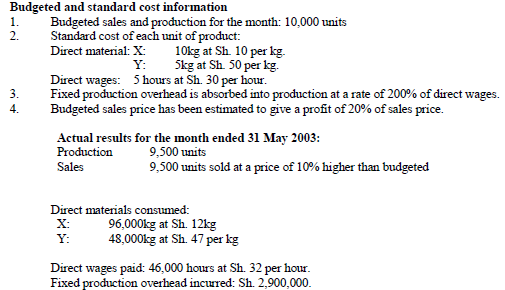

BS Limited manufactures a single standard product and operates a system of standard costing using a

fixed budget. As the company's assistant cost accountant, you are...

(Solved)

BS Limited manufactures a single standard product and operates a system of standard costing using a

fixed budget. As the company's assistant cost accountant, you are responsible for preparing the

monthly operating statements. Details from the budget, the standard product costs and actual results

for the month ended 31 May 2003 are given below:

Required:

The operating statement for the month of May, 2004 showing:

(a) The budgeted profit.

(b) Variances for direct materials, direct wages, overheads and sales.

(c) The actual profit.

Date posted:

February 26, 2019

.

Answers (1)

-

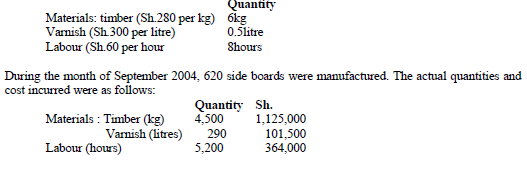

Ufundi Furniture Ltd. Manufactures a wide range of home furniture. Recently the company added

to its range a side board. The standard cost specification for each...

(Solved)

Ufundi Furniture Ltd. Manufactures a wide range of home furniture. Recently the company added

to its range a side board. The standard cost specification for each side board is given below:

The abnormal idle hours were 400 and the hours worked were recorded as 4,800 hours.

Required:

i) Material price variances (for both materials).

ii) Material usage variance (for both materials)

iii) Labour rate of pay variance.

iv) Labour efficiency variance.

v) Idle time variance.

(c) Suggest possible causes of the material variances.

Date posted:

February 26, 2019

.

Answers (1)

-

State the advantages of using standard costs in the manufacturing industry.

(Solved)

State the advantages of using standard costs in the manufacturing industry.

Date posted:

February 26, 2019

.

Answers (1)

-

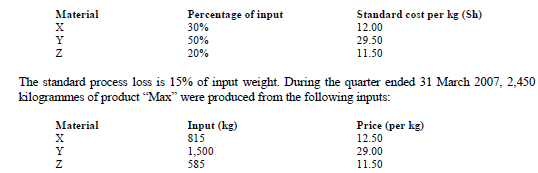

The standard mix of a product branded Max is as follows:

(Solved)

The standard mix of a product branded Max is as follows:

Required:

i) Material price variance.

ii) Material mix variance.

iii) Material yield variance.

Date posted:

February 26, 2019

.

Answers (1)

-

Highlight four disadvantages of standards costing.

(Solved)

Highlight four disadvantages of standards costing.

Date posted:

February 26, 2019

.

Answers (1)