1. Cost Classification by Functionbusiness has to perform a number of functions e.g. manufacture, administration, selling, distribution and research. On this basis costs are classified into the following;

a) Manufacturing /production / factory cost This are costs related to the manufacturing process e.g. material cost, labour, cost and factory cost such as rent, depreciation of machinery, power and lighting etc.

b) Administrative costs include all expenditure incurred in formulating policies, directing the organizations and controlling the operation of an undertaking such as audit fee, office rent, salaries etc.

c) Selling cost are costs of seeking to create and stimulate demand and to serve orders e.g. advertising, salaries and commission of salesmen etc.

d) Distribution expenses are cost incurred to avail the product to the final consumer. E.g. packing cost, carriage outward, warehousing cost etc.

e) Research and development cost this is the cost of searching new and improved products and methods. E.g. wages and salaries of research staff, payment to outside research organizations etc.

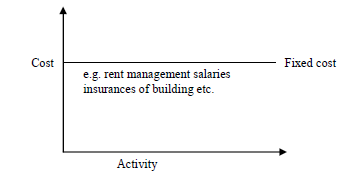

2. Cost Classification by Behaviora) Fixed cost – This is a cost which does not vary with activities or output. It remains constant within the relevant range as shown in Figure. A relevant range is range within which relationship between cost and activity hold.

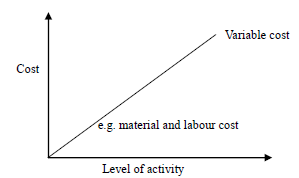

b) Variable cost is costs that vary in direct proportion to the volume of output. When volume of output increases variable cost also increases and vice versa as indicated in Figure

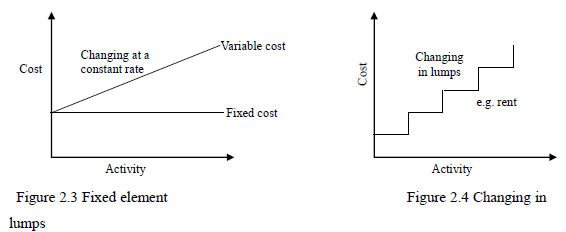

c) Semi variance cost These are costs that are partially fixed and partially variable. A semi-variable cost has often a fixed element below which it will not fall at any level of output. The variable element is a semi-variable cost changes either at a constant rate or in lumps. E.g. electricity bill which has a fixed element in it below which it cannot follow and a variable element that changes based on the power consumptions as shown in Figures

3. Cost Classification in Relation to the Product

3. Cost Classification in Relation to the Producta) Product cost is costs necessary for production and can not be incurred in case there is no production. They include; cost of direct materials, direct labour and some of the factory overhead. They are called production costs because they are included in the course of production.

b) Period costs are costs which are not necessary for production and they are written as expenses in the period in which they are incurred. They are incurred for a time period and are charged to the income statement for the period e.g. rent salary of company executives, travel expenses etc.

4. Cost Classification By Type or NatureCosts are also classified according to the purpose for which the cost is incurred e.g. material cost, labour cost and overheads. These three types of costs have already been discussed above under the heading of 'Elements of Cost'

5. Classification according to identifiability with the producta) Direct costs are costs which are incurred for and may be conveniently identified with a particular cost unit process or department such as direct labour, direct materials etc.

b) Indirect costs are costs which can not be conveniently identified with a particularly cost unit process or department. They are general cost incurred for the benefit of a number of cost unit or cost centres such as salary paid to a factory foreman.

6. Classification according to controllabilitya) Controllable costs are costs that may be directly regulated by a given level of managerial influence. E.g. variable costs are generally controllable by department heads.

b) Uncontrollable costs are costs that cannot be influenced by the action of a specified member of the enterprise e.g. fixed cost like rent are generally uncontrollable.

7. Special cost for managerial decision makinga) Relevant costs are costs which changes from one decision to the next and as such relevant cost will be affected by the decision being made under different alternatives. In decision making management will be concerned with those costs that differ from one decision to another.

b) Sunk or irrelevant cost These are cost which have been already been incurred in the past and cannot be changed. They are relevant in decision making.

c) Incremental cost / differential costs This is an increase or decrease in cost as a result of an alternative course of an action.

d) Marginal or variable cost It is the cost of producing an extra unit of a commodity.

e) Replacement cost This market value of replacing an existing asset.

f) Opportunity cost It is the sacrifice involved in accepting the alternative under consideration.

8. Classification according to timea) Historical costs are costs ascertained after they have been incurred. They are the actual costs which are only available after completion of the manufacturing process.

b) Predetermined costs They are future costs that are ascertained in advance of production on the bases of all specified factors affecting cost.

Wilfykil answered the question on

April 15, 2019 at 09:04