-

Assume that the risk free rate of return is 8%, the market expected rate of return is 12%. The standard deviation of the market return...

(Solved)

Assume that the risk free rate of return is 8%, the market expected rate of return is 12%. The standard deviation of the market return is 2% while the covariance of return for security A and the market is 2%.

What is the required rate of return on Security A?

Date posted:

April 13, 2021

.

Answers (1)

-

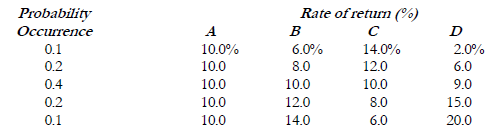

Four assets have the following distribution of returns.a. Compute the expected return and standard deviation of each asset.b. Compute the covariance of asseti. A and...

(Solved)

Four assets have the following distribution of returns.

Required.

a. Compute the expected return and standard deviation of each asset.

b. Compute the covariance of asset

i. A and B

ii. B and C

iii. B and D

c. Compute the correlation coefficient of the combination of assets in b above.

Date posted:

April 13, 2021

.

Answers (1)

-

A piece of equipment requiring the investment of 2.2 million is being considered by Charo Foods Ltd. The equipment has a ten-year useful life and...

(Solved)

A piece of equipment requiring the investment of 2.2 million is being considered by Charo Foods Ltd. The equipment has a ten-year useful life and an expected salvage value of Sh 200,000. The company uses the straight-line method of depreciation for analyzing investment decisions and faces a tax rate of 40%. For simplicity assume that the depreciation method is acceptable for tax purposes.

A pessimistic forecast projects cash earnings before depreciation and taxes at Sh 400,000 per year compared with an optimistic estimate of Sh 500,000 per year. The probability associated with the pessimistic estimate is 0.4 and 0.6 for the optimistic forecast. The company has a policy of using a hurdle rate of 10% for replacement investments, 12% (its cost of capital) for revenue expansion investments into existing product lines and 15% projects involving new areas or new product lines.

REQUIRED:

(a) Compute the expected annual cash flows associated with the proposed equipment investments.

(b) Would you recommend acceptance of this project if it involved expansion of sales for an existing product?

(c) Would it be acceptable if it was for the replacement of equipment with a book value of Sh 200,000 at the end of the tenth year but which could be sold at that time for only Sh 40,000?

(d) Discounted cash flow methods were developed for idealized settings of complete and perfect capital, factor and commodity markets. Explain what complications arise when an attempt is made to apply these methods in real life markets that are neither complete nor perfect.

Date posted:

April 13, 2021

.

Answers (1)

-

The Mentala Plastics Company has been dumping in the local council waste collection

centre some 30,000 Kg. of unusable chemicals each year. In addition to being...

(Solved)

The Mentala Plastics Company has been dumping in the local council waste collection

centre some 30,000 Kg. of unusable chemicals each year. In addition to being an

eyesore, the residents of a nearby estate have started complaining of bad odour

emanating from the dump and suspect that the company is to blame.

The company has received information that these chemicals can be recycled at relatively little

cost. The equipment to do it is however rather expensive and, in addition, the chemicals

recovered are of a relatively poor quality. Investigations have shown that these chemicals can

be sold to another firm at an average price of Sh.35 per Kg. The direct cost of recycling has

been calculated at Sh.15 per Kg. but this is before depreciation and taxes.

The equipment for this process has an expected life of 10 years and a current cost of Sh.2 million. At the

end of the ten years, it will be virtually worthless.

For financial analysis, the company uses the straight line method of depreciation and an average tax rate of

40%. It has a required rate of return of 15%.

REQUIRED:

i. Compute the project's net present value (N.P.V).

ii. Compute the payback period and the accounting rate of return.

iii. Compute the internal rate of return (IRR).

iv. Should this project be undertaken? Explain.

Are there any other important matters that the company should consider in evaluating this project?

Date posted:

April 13, 2021

.

Answers (1)

-

The Zeda Company Ltd. is considering a substantial investment in a new production process. From a

variety of sources, the total cost of the project has...

(Solved)

The Zeda Company Ltd. is considering a substantial investment in a new production process. From a

variety of sources, the total cost of the project has been estimated at Sh.20 million. However, if the

investment were to be increased to Sh.30 million, the productive capacity of the plant could be substantially

increased. Due to the nature of the process, it would be exorbitantly expensive to increase capacity once the

equipment is installed.

Once of the problems facing the company is that there is a considerable degree of uncertainty regarding

demand for the product. After some research which has been conducted jointly by the marketing and

finance departments, some data has been produced. These are shown below:

REQUIRED:

(a) Prepare a statement which clearly indicates the financial implications of each of the two alternative

investment scenarios.

(b) Comment on other matters which the management should take into account before reaching

the final decision.

PVIFA: 10% 5 years = 3.79

PVIFA: 10% 10 years = 6.14

PVIFA: 10% 10 years = 0.62

Date posted:

April 13, 2021

.

Answers (1)

-

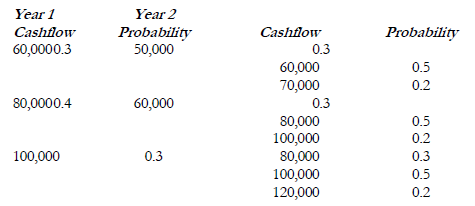

A project has the following cash flows

The projects initial cash outlay is Sh 100,000 with a cost of capital of 12%.

Required:

Determine:

(a) The projects expected monetary...

(Solved)

A project has the following cash flows

The projects initial cash outlay is Sh 100,000 with a cost of capital of 12%.

Required:

Determine:

(a) The projects expected monetary value (EMV)

(b) The projects NPV

Date posted:

April 13, 2021

.

Answers (1)

-

Assume a project costs Sh 30,000 and yields the following uncertain cashflows:

Compute the NPV of the project

(Solved)

Assume a project costs Sh 30,000 and yields the following uncertain cash flows:

Year Cash flow

1 12,000

2 14,000

3 10,000

4 6,000

Assume also that the certainty equivalent coefficients have been estimated as follows:

α0 = 1.00

α1 = 0.90

α2 = 0.70

α3 = 0.50

α4 = 0.30

The risk-free discount rate is given as 10%

Required

Compute the NPV of the project

Date posted:

April 13, 2021

.

Answers (1)

-

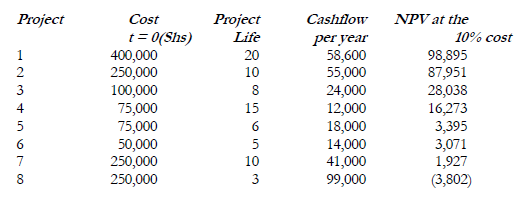

Management is faced with eight projects to invest in. The capital expenditures during the year has been rationed to Sh 500,000 and the projects have...

(Solved)

Management is faced with eight projects to invest in. The capital expenditures during the year has been rationed to Sh 500,000 and the projects have equal risk and therefore should be discounted at the firm's cost of capital of 10%.

Required:

Determine the optimal investment sets.

Date posted:

April 13, 2021

.

Answers (1)

-

A company is considering two mutually exclusive projects requiring an initial cash outlay of Sh 10,000 each and with a useful life of 5 years....

(Solved)

A company is considering two mutually exclusive projects requiring an initial cash outlay of Sh 10,000 each and with a useful life of 5 years. The company required rate of return is 10% and the appropriate corporate tax rate is 50%. The projects will be depreciated on a straight line basis. The before depreciation and taxes cash flows expected to be generated by the projects are as follows.

Required:

Calculate for each project

i. The payback period

ii. The average rate of return

iii. The net present value

iv. Profitability index

v. The internal rate of return

Which project should be accepted? Why?

Date posted:

April 13, 2021

.

Answers (1)

-

Two neighbouring countries have chosen to organize their electricity supply industries in different ways. In

country A, electricity supplies are provided by a nationalized industry. On...

(Solved)

Two neighbouring countries have chosen to organize their electricity supply industries in different ways. In

country A, electricity supplies are provided by a nationalized industry. On the other hand in country B

electricity supplies are provided by a number of private sector companies.

Required:

(a) Explain how the objectives of the nationalized industry in country A might differ from those of the private sector companies in country B.

(b) Briefly discuss whether investment planning and appraisal techniques are likely to differ in the nationalized industry and private sector companies.

Date posted:

April 13, 2021

.

Answers (1)

-

List and explain the 14 principles of management

(Solved)

List and explain the 14 principles of management

Date posted:

March 5, 2019

.

Answers (1)

-

Identify the various methods of issuing new ordinary shares to shareholders.

(Solved)

Identify the various methods of issuing new ordinary shares to shareholders.

Date posted:

February 12, 2019

.

Answers (1)

-

Why does ordinary share capital have a high cost relative to debt capital?

(Solved)

Why does ordinary share capital have a high cost relative to debt capital?

Date posted:

February 12, 2019

.

Answers (1)

-

What practical problems are faced by finance managers in capital budgeting decisions.

(Solved)

What practical problems are faced by finance managers in capital budgeting decisions.

Date posted:

February 12, 2019

.

Answers (1)

-

What are the features of a sound appraisal technique?

(Solved)

What are the features of a sound appraisal technique?

Date posted:

February 12, 2019

.

Answers (1)

-

What are the advantages of having a farmers' bank compared with an ordinary

commercial bank in the provision of services to farmers

(Solved)

What are the advantages of having a farmers' bank compared with an ordinary

commercial bank in the provision of services to farmers

Date posted:

February 12, 2019

.

Answers (1)

-

Why do different sources of finance have different costs?

(Solved)

Why do different sources of finance have different costs?

Date posted:

February 12, 2019

.

Answers (1)

-

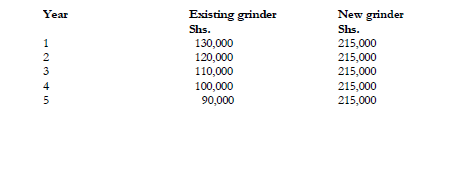

The Kitale Maize Mills is contemplating the purchase of a new high-speed grinder to replace an

existing one. The existing grinder was purchased two years ago...

(Solved)

The Kitale Maize Mills is contemplating the purchase of a new high-speed grinder to replace an

existing one. The existing grinder was purchased two years ago at an installed cost of Sh.300,000.

The grinder was estimated to have an economic life of 5 years but a critical analysis of its

performance now shows it is usable for the next five years with no resale value.

The new grinder would cost Sh.525,000 and require Sh.25,000 in installation costs. It has a five

year usable life. The existing grinder can currently be sold for Sh.350,000 without incurring any

removal costs. To support the increased business resulting from purchase of the new grinder,

accounts receivable would increase by Sh.200,000, inventories by Sh.150,000 and trade creditors

by Sh.290,000. At the end of 5 years the new grinder would be sold to net Sh.145,000 after

removal costs and before taxes. The company provides for 40% taxes on ordinary income. The

estimated profit before depreciation and taxes over the five years for both machines are given as

follows:

The company uses straight line method of depreciation for both machines.

Required:

a) Calculate the initial investment associated with the replacement of the existing grinder

with the new one. Show your full workings.

b) Determine the incremental operating cash flows associated with the proposed grinder

replacement.

c) Calculate the terminal cash flow expected from the proposed grinder replacement.

Date posted:

February 12, 2019

.

Answers (1)

-

The valuation of ordinary shares is more complicated than the valuation of bonds and

preference shares. Explain the factors that complicate the valuation of ordinary shares.

(Solved)

The valuation of ordinary shares is more complicated than the valuation of bonds and

preference shares. Explain the factors that complicate the valuation of ordinary shares.

Date posted:

February 12, 2019

.

Answers (1)

-

Within a Financial Management context, discuss the problems that might exist in the

relationships (sometimes referred to as agency relationships) between:

1. Shareholders and managers, and

2. Shareholders...

(Solved)

Within a Financial Management context, discuss the problems that might exist in the

relationships (sometimes referred to as agency relationships) between:

1. Shareholders and managers, and

2. Shareholders and creditors.

Date posted:

February 12, 2019

.

Answers (1)