-

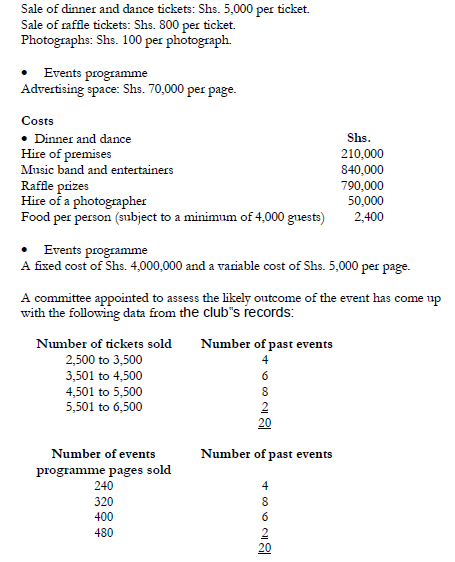

Mwito Club is a charitable organization based in Nairobi. For the last 20 years, the

club has held an annual dinner and dance event with the...

(Solved)

Mwito Club is a charitable organization based in Nairobi. For the last 20 years, the

club has held an annual dinner and dance event with the primary aim of raising

funds to help the less fortune members of the society.

This year, there is concern that an economic recession may adversely affect the

success of the event with a fall in the number of guests attending and sale of

advertising space in the published events programme.

A study of past experience, current prices and quotations shows that the following

costs and revenues will apply for the event:

Revenue

Dinner and dance

Required:

(i) The expected profit from the event. (Assume one raffle ticket and one

photograph per attendant).

(ii) Describe how cost-volume-profit (C-V-P) analysis can be applied in

absorption costing.

Date posted:

May 7, 2021

.

Answers (1)

-

Angels of Mercy Mission Hospital operates on charity basis. The hospital?s board

of directors has recently complained about the increasing size of the cost budget insisting...

(Solved)

Angels of Mercy Mission Hospital operates on charity basis. The hospital‟s board

of directors has recently complained about the increasing size of the cost budget insisting that

the management should cut down on costs.

The major concern of the board is the cost of maintaining patients at the intensive care unit

(ICU).

The following information is available on the operations of the hospital:

1. The average cost of maintaining a patient at the ICU per week is Shs. 200,000 compared

to Shs. 100,000 per week incurred in maintaining a patient at the high dependency unit

(HDU) and Shs. 50,000 per week of maintaining a patient at the general ward (GW).

2. Past information on patients indicates that:

(i) 50% of the patients in ICU at the beginning of the week will remain in ICU

at the end of the week and 50% will be transferred to HDU by the end of the

week.

(ii) 10% of the patients in HDU at the beginning of the week will be transferred

to ICU, 50% will remain in HDU, and 40% will be transferred to GW.

(iii) 85% of the patients in the GW at the beginning of the week will remain in

GW at the end of the week, 10% will be transferred to HDU and 5% to ICU.

3. The board of directors believe that the criteria for maintaining patients in the ICU is too

strict and should be relaxed so that only 40% of the patients in ICU at the beginning of

the week remain there at the end of the week while 60% are transferred to HDU.

4. The staff at the hospital insist that if the proposed criterion is adopted:

(i) 20% of patients in HDU at the beginning of the week will be transferred to

ICU, 50% will remain in HDU while only 30% will be transferred to GW.

(ii) No changes will be expected in the GW.

5. Past hospital records indicate that the hospital serves an average of 4,000 patients

weekly.

Required:

(a) The steady state weekly costs under the current policy.

(b) The steady state weekly costs under the proposed policy.

(c) Advise the board on the best policy.

(d) State the assumptions of the quantitative technique used in solving problems (a) and

(b) above.

Date posted:

May 7, 2021

.

Answers (1)

-

Pwani Marine Ltd., a boat construction company, has developed a new type

of speed boat called “Speed Surf.”

The following information has been availed to you:

1. Boat...

(Solved)

Pwani Marine Ltd., a boat construction company, has developed a new type

of speed boat called “Speed Surf.”

The following information has been availed to you:

1. Boat construction is a continuous assembling process carried out at

the company‟s yard.

2. Boat assembling is labour intensive involving the use of two classes of

labour namely:

Skilled labour at a standard rate of Shs. 1,250 per hour.

Semi-skilled labour at a standard rate of Shs. 950 per hour.

3. Experience on boat construction from other models indicates that the use of

skilled labour is associated with an 80% learning curve effect whereas use of

semi-skilled labour is associated with a 90% learning curve effect.

4. Labour usage for the first speed boat assembled was as follows:

Skilled labour – 952 hours.

Semi-skilled labour – 650 hours.

5. In October 2005, the sixth and the seventh speed boats were assembled

from start to finish. During the month, the following labour usage and costs

were recorded:

Skilled labour – 680 hours at a total cost of Shs. 800,400.

Semi-skilled labour – 1,256 hours at a total cost of Shs. 1,281,200.

The management of Pwani Marine Ltd. is concerned about the cost variances and

would like to learn more on the composition of the variances.

Required:

(i) Calculate the standard labour cost of the month of October 2005.

(ii) Reconcile the standard cost with the actual cost for the month of October

2005 showing the labour rate and labour efficiency variances.

(iii) Express the labour efficiency variance in terms of labour mix and labour

output variances. (Value the labour mix variances using standard rates).

Date posted:

May 7, 2021

.

Answers (1)

-

Explain the applications of the learning curve.

(Solved)

Explain the applications of the learning curve.

Date posted:

May 7, 2021

.

Answers (1)

-

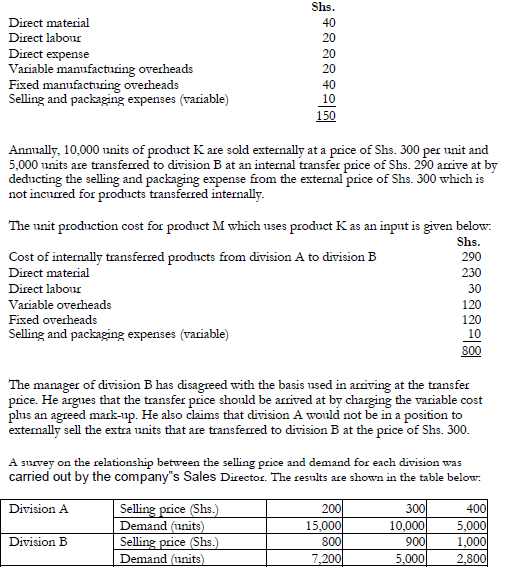

Kutwa Ltd. is a manufacturing company with two divisions; A and B. Division A

manufactures a single standard product K, some of which is sold externally...

(Solved)

Kutwa Ltd. is a manufacturing company with two divisions; A and B. Division A

manufactures a single standard product K, some of which is sold externally and the

remainder used as an input in division B in the manufacture of product M.

The unit production costs of product K are given below:

The manager of division B suggests that based on the above results, a transfer price of Shs.

120 would offer division A a reasonable contribution towards its fixed cost and earn

division B a reasonable profit. This would lead to an increase in the output and overall

profitability of the company.

Required:

( a) Calculate the effect of the existing transfer pricing system on the company‟s profits.

( b) Calculate the effect of adopting the transfer price of Shs. 120 on the company‟s

profits.

Date posted:

May 7, 2021

.

Answers (1)

-

Nairobi Manufacturers Ltd. produces component X on machine Y at a rate of 4,000

units per month. Machine Z uses component X at the rate of...

(Solved)

Nairobi Manufacturers Ltd. produces component X on machine Y at a rate of 4,000

units per month. Machine Z uses component X at the rate of 1,000 units per month,

the remainder being put into stock. It costs Shs. 2,000 to set up machine Y while the

stock holding cost is estimated at Shs. 2.50 per unit per annum plus a 20% opportunity

cost of capital per annum. Each component costs Shs. 25 to produce.

Required:

(i) Compute the optimal batch size that should be produced using machine Y.

(ii) Assume that the actual set-up cost of machine Y is Shs. 1,000 instead of

Shs. 2,000. Calculate the cost of prediction error.

Date posted:

May 7, 2021

.

Answers (1)

-

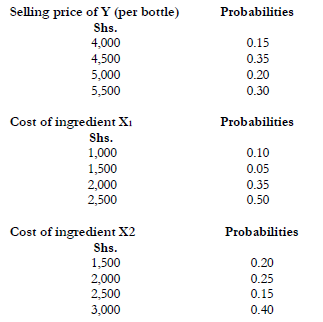

Manukato Ltd. produces a designer perfume called “Hint of Elegance.”

Production of the perfume involves the use of two ingredients, X1 and X2

represented by the production...

(Solved)

Manukato Ltd. produces a designer perfume called “Hint of Elegance.”

Production of the perfume involves the use of two ingredients, X1 and X2

represented by the production function given below:

Required:

(i) Calculate the daily expected profit of the company.

(ii) Simulate the company‟s profit for 10 days using the following

random numbers:

58, 71, 96, 30, 24, 18, 46, 23, 34, 27, 85, 13, 99, 24, 44, 49,

18, 09, 79, 49, 74, 16, 32, 23, 02, 56, 88, 87, 59, 41, 06

Date posted:

May 7, 2021

.

Answers (1)

-

Shadow prices may be used in the setting of transfer prices between divisions in a

company, where the intermediate products being transferred are in short supply.

Required:

Explain...

(Solved)

Shadow prices may be used in the setting of transfer prices between divisions in a

company, where the intermediate products being transferred are in short supply.

Required:

Explain why the transfer prices thus calculated are more likely to be favoured by the

management of the divisions supplying the intermediate products rather than the

management of the divisions receiving the intermediate products.

Date posted:

May 7, 2021

.

Answers (1)

-

Transfer pricing of products between processes in a manufacturing company can be done at:

1. Cost or

2. Sales value at the point of transfer.

Required:

Discuss how each...

(Solved)

Transfer pricing of products between processes in a manufacturing company can be done at:

1. Cost or

2. Sales value at the point of transfer.

Required:

Discuss how each of the above methods could be used effectively in the operations

of a responsibility accounting system.

Date posted:

May 7, 2021

.

Answers (1)

-

State four objectives of a transfer pricing system.

(Solved)

State four objectives of a transfer pricing system.

Date posted:

May 7, 2021

.

Answers (1)

-

State the limitations of the use of fame theory in decision making.

(Solved)

State the limitations of the use of fame theory in decision making.

Date posted:

May 7, 2021

.

Answers (1)

-

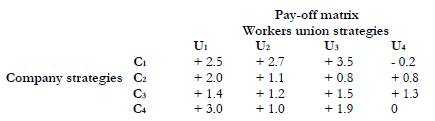

Topcom Kenya International Limited (TKIL) is a telecommunications company

situated in Nakuru. Recently, the company was faced with a workers strike which

necessitated a renegotiation of the...

(Solved)

Topcom Kenya International Limited (TKIL) is a telecommunications company

situated in Nakuru. Recently, the company was faced with a workers strike which

necessitated a renegotiation of the workers‟ salaries through their union.

The management with the help of a consultant, has prepared the pay-off matrix

shown below:

A positive sign represents a wage increase while a negative sign represents a wage decrease.

Required:

(i) Advise the management on the best strategies.

(ii) The value of the game

Date posted:

May 7, 2021

.

Answers (1)

-

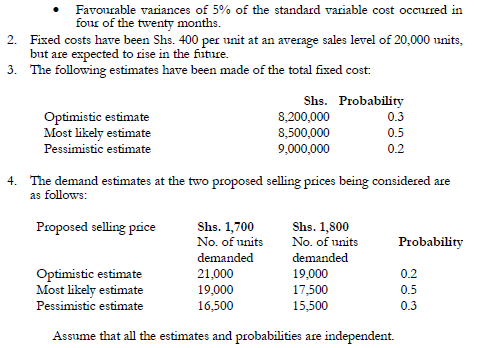

Makazi Ltd. manufactures a hedge-trimming tool which has been selling at Shs.

1,600 per unit for a number of years. The selling price is to be...

(Solved)

Makazi Ltd. manufactures a hedge-trimming tool which has been selling at Shs.

1,600 per unit for a number of years. The selling price is to be reviewed and the

following information is available on costs and the likely demand:

1. The standard variable cost of manufacturing the tool is Shs. 1,000 per unit and

an analysis of the cost variances in the past 20 months shows the following

pattern which the production manager expects to continue in the future.

Adverse variances of 10% of the standard variables cost occurred in ten

of the twenty months.

Nil variances occurred in six of the twenty months.

Required:

(i) Based on the information given above, advise the management of Makazi Ltd.

on whether they should change the selling price. Indicate the price you would

recommend.

(ii) The expected profit at the price you have recommended in (i) above and the

resulting margin of safety expressed as a percentage of expected sales

(iii) Comment on the method of analysis you have used to deal with the

probabilities given in the question.

(iv) Explain briefly how the use of a computer program would improve your

analysis.

Date posted:

May 7, 2021

.

Answers (1)

-

Equi -solutions Ltd. was formed ten years ago to provide business equipment solutions tolocal business. It has separate divisions for research, marketing, product design, technologyand...

(Solved)

Equi -solutions Ltd. was formed ten years ago to provide business equipment solutions to

local business. It has separate divisions for research, marketing, product design, technology

and communication services, and now manufactures and supplies a wide range of business

equipment. To date the company has evaluated its performance using monthly financial

reports that analyze profitability by type of equipment. The managing director of Equi solutions

Ltd. has recently returned from a course in which it has been suggested that the

“Balanced Scorecard” could be a useful way of measuring performance.

Required:

a) Explain the “Balanced Scorecard” and how it could be used by Equi-solutions Ltd. to

measure its performance.

b) The managing director of Equi-solutions Ltd. also overheard someone mention how the

performance of their company had improved after they introduced “Bench marking.”

Required:

Explain “Bench-marking” and how it could be used to improve the performance of

Equi -solutions Ltd.

Date posted:

May 7, 2021

.

Answers (1)

-

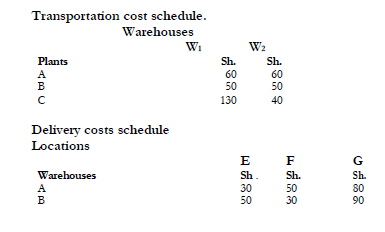

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may...

(Solved)

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may be distributed through any combination of the two

company warehouses W1 and W2.

2. The available monthly production capabilities for the new products are:

1000 units at plant A

2000 units at plant B

1000 units at plant C

3. Three major concentration points of customer demand are at locations E, F

and G which are estimated to have a monthly demand of:

900 units at E

800 units at F

900 units at G

4. The unit production costs amount to Sh.30, Sh.40, Sh.10 at A, B and C

respectively.

5. The unit handling costs at the warehouses amount to Sh.20 and Sh.30 at W1

and W2.

6. The unit transportation costs from plant to warehouse and unit delivery cost

from warehouse to customers are as shown below:

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Date posted:

May 7, 2021

.

Answers (1)

-

Explain the following terms as applied in competitive situations:

i) Degeneracy

ii) Pure strategy

iii) Mixed strategy

iv) Dominance rule

(Solved)

Explain the following terms as applied in competitive situations:

i) Degeneracy

ii) Pure strategy

iii) Mixed strategy

iv) Dominance rule

Date posted:

May 7, 2021

.

Answers (1)

-

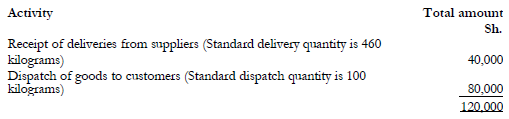

Industrial Chemical Ltd. (ICL) produces chemical Y. the standard ingredients of 1 kilogram

of Y are:

0.65 kilograms of ingredient F @ Sh. 40 per Kg

0.30 kilograms...

(Solved)

Industrial Chemical Ltd. (ICL) produces chemical Y. the standard ingredients of 1 kilogram

of Y are:

0.65 kilograms of ingredient F @ Sh. 40 per Kg

0.30 kilograms of ingredient D @ Sh. 60 per Kg.

0.20 kilograms of ingredient N @ Sh. 25 per Kg.

The following additional information is provided:

1. Production of 4,000 kilograms of chemical Y was budgeted for October 2004.

2. The production of chemical Y is entirely automated and production costs attributed to

its production comprise only direct materials and overheads.

3. ICL‟s production process works on a just-in-time (JIT) inventory system and

no ingredients or inventories of chemical Y are held.

4. Overheads budgeted for the production of Y in the month of October 2004 were as

follows:

5. In October 2004, 4,200 kilograms of Y were produced and the cost details were as

follows:

Materials used

2,840 kilograms of F, 1,210 kilograms of D and 860 kilograms of N at a total cost of

Sh. 203,800.

Actual overhead costs

12 supply deliveries at a cost of Sh.48,000 and 38 customer dispatches at a cost of

Sh. 78,000 were made.

6. ICL‟s budget committee met recently to discuss the preparation of the cost

control report for October 2004 and the following discussion took place:

Chief accountant: “the overheads do not vary directly worth output and

are therefore by definition „fixed‟. They should be analyzed and reported

accordingly”.

Management accountant: “the overheads do not vary with output, but they

are certainly not fixed. They should be analyzed and reported on an activity based

basis.”

Required:

Having regard to this discussion,

a) Prepare a variance analysis of the production costs of Y in October 2004. (Separate the

material cost variance into price, mixture and yield components and the overhead cost

variance into expenditure, capacity and efficiency components using consumption of

ingredient F as the overhead absorption base).

b) Prepare a variance analysis of the overhead production costs on Y in October 2004 on

an activity based basis.

Date posted:

May 7, 2021

.

Answers (1)

-

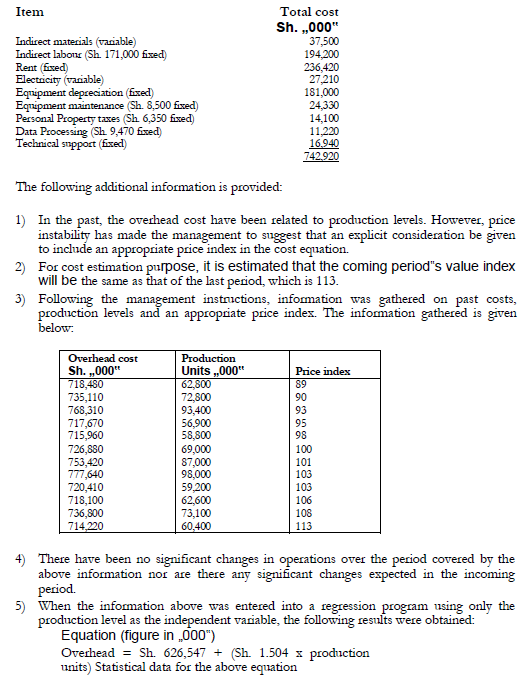

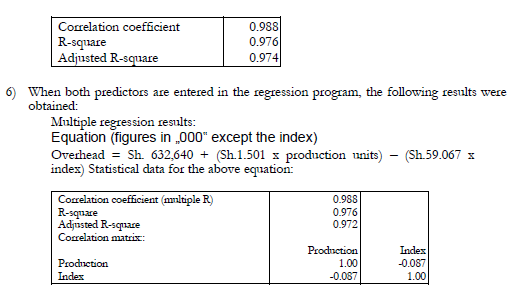

Maisha Meta Products Ltd. has prepared a schedule of estimated overhead costs for the

coming year. The schedule was prepared on the assumption that production would...

(Solved)

Maisha Meta Products Ltd. has prepared a schedule of estimated overhead costs for the

coming year. The schedule was prepared on the assumption that production would amount

to 800,000 units. Costs have been classified as either fixed or variable according to the

judgement of the financial controller. The following overhead cost items and their

classification as either fixed or variable form the basis for the overhead cost schedule:

Required:

a) Determine the cost estimation equation using the account analysis method

b) Use the high-low method to estimate the cost of 800,000 units of production expected

in the coming period.

c) Using the simple linear regression, estimate the cost of 800,000 units of production.

d) Use the multiple regression results to prepare an estimated cost for the 800,000 units in

the incoming period.

e) Comment on which of the methods is more appropriate under the above circumstances.

Date posted:

May 6, 2021

.

Answers (1)

-

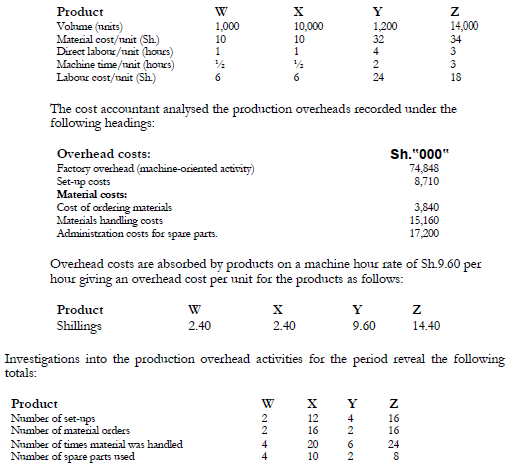

The Marima Manufacturing Company produces four products; W, X, Y and Z using

the same plant and processes.

The following information relates to the company:

Required:

(i) Unit costs...

(Solved)

The Marima Manufacturing Company produces four products; W, X, Y and Z using

the same plant and processes.

The following information relates to the company:

Required:

(i) Unit costs per product using activity-based costing tracing costs to production units by

means of cost drivers.

(ii) Comment briefly on the differences disclosed between overheads traced by the present

system and those traced by activity based costing.

Date posted:

May 6, 2021

.

Answers (1)

-

The current thinking in Management Accounting contends that Activity-Based

Costing (ABC) provides better information concerning products costs and decision

making than traditional management accounting techniques.

However, whereas ABC...

(Solved)

The current thinking in Management Accounting contends that Activity-Based

Costing (ABC) provides better information concerning products costs and decision

making than traditional management accounting techniques.

However, whereas ABC may give a different impression of product costs, it is not

necessarily a good idea and it may be advisable to continue improving traditional

cost accounting techniques before moving to ABC.

Required:

(i) Explain cost behaviour issues underlying the use of ABC.

(ii) Explain why ABC might, be more suitable for modern manufacturing

environment than traditional cost accounting techniques?

(iii) Comment on the reported claim that ABC gives better information as a

guide to decision making than the traditional product costing techniques.

Date posted:

May 6, 2021

.

Answers (1)