Strategic planning is the process of setting or changing the long-term objectives or strategic

target of a organization. These would include such maters as the selection of products and

markets, the required level of company profitability, the purchases and disposal of subsidiary

companies or major fixed asset. And so on. A notable characteristic of strategic planning is

as follows;

a. It will generally be formulated in writing, and only after much discussion by

committee (the board).

b. It will be (or should be) circulated to all interested parties within the organization and

perhaps even to the press.

c. It will trigger the production not of direct action but of a series of lesser plan for sales.

Production, marketing, and so on.

Operational planning work out what specific tasks needs to be carried out in order

to achieve the strategic plan. For example a strategy may be to increase sales by 5% per

annum for at least five years, and an operational plans to achieve this would be

sales reps? weekly sales target. (Note: we use the word „strategic? and

„operational? in the sense implied in the well-known work of Robert Anthony).

Notable characteristic of operational planning are the speed of response to changing

conditions and the use and understanding of non-financial information such as data about

customer orders or raw material input.

ii)

1. Unrealistic operational plan will force staff to try hard with too few resources.

Mistakes and failure are almost inevitable. This means poor quality products; costs

include lost sales arranging for returns, and time wasted dealing with complaints and

rectification work. Over ambitions plan may also mean that more stocks are produced

than an organization could realistically expected to sell (meaning the costs of written offs,

opportunity costs of wasted production resources and unnecessary stock holding

cost are incurred.

2. Inconsistent strategic planning and operational planning goals may mean that

additional cost are incurred. For example, an operational plan may require additional

inspection point in a production process so as to ensure that quality products are

delivered to customers. The resulting extra costs will be at odds with the strategic

planning goal of minimum costs.

3. Poor communication between the senior management who set strategic goals and lower

level operational management could mean that operational manager are unaware

of the strategic planning goal of sustaining competitive advantage at minimum cost

through speedy delivery of quality products to customers. Some operational managers

may therefore choose to focus on quality of products while others attempts to

produce as many product as possible as quickly as they can; still others will simply

keep their heads down and do as little as possible. This will lead to lack of coordination;

there will be bottlenecks in some operational areas, needing expensive

extra resource in the short term, and wasteful idle time in other areas.

4. Inadequate performance measurement will mean that the organization has little idea of

which area is performing well and which need attention. If quality of products and speed

of delivery are the main source of competitive advantage a business needs to know how

good it is these thing. For example, if an organization measures only conventional

accounting results it will know how much stock it has and how much it has spent on

„carried out?. It will not know the opportunity cost of cancelled sales though not

having stock available when need or not being able to deliver it on time.

Equally, the quantity of products need to be measured in terms not only of sales

achieved, but also in terms of customers complaints and deed back; again the costs is

the opportunity cost of cost sales.

Otherwise, repairs and maintenance cost of machinery would vary with the level of

activity but machines would still need a certain level of maintenance even if they were

not being used,(the company might, one the other hand, be considering selling the

machinery, accounts of which may not have been taken). The estimate of direct

attribute fixed costs may be subjective judgments, such as deciding which supervisor

salaried would be avoidable if the service were contracted out. The variable costs may

be based on past data that does not take account of potential reduction or increases in

productivity due to factors such as untrained staff or new machines.

Finally, the costs of buying in may also be high subjective. Accounts may not have

been taken of costs such as increases or decreases in tie spent delivering the

components (from abroad perhaps) or complaints or costs resulting from badly made

component. It is therefore obvious that the behavior of costs associated withy a

decision must be fully understood and their relevance to that decision ascertained

before the decision is finally made.

Kavungya answered the question on May 10, 2021 at 05:59

-

Decision-making situations under short-term conditions require consideration of;

i. The cost classifications which the management accountant should use or ignore,

and

ii. Factors which may affect the behavior...

(Solved)

Decision-making situations under short-term conditions require consideration of;

i. The cost classifications which the management accountant should use or ignore,

and

ii. Factors which may affect the behavior of costs and hence the accuracy of the

cost analysis and the relevance of the decision making.

Required

In the context of the above statement, discuss whether a company should make

quantities of a component used in a manufacture of a product or buy in the component

from an outside supplier or out source.

Date posted:

May 10, 2021

.

Answers (1)

-

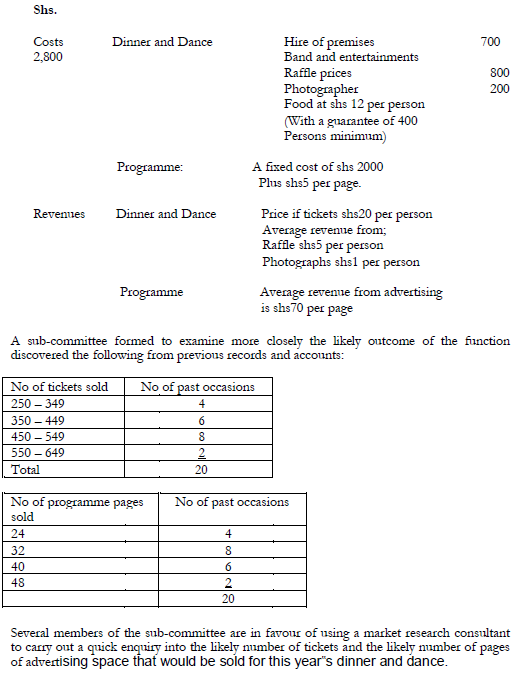

Kenya Charity Organization has been holding annual dinner and dance for the last 100 years

with the primary intention of raising funds.

This year, there is a...

(Solved)

Kenya Charity Organization has been holding annual dinner and dance for the last 100 years

with the primary intention of raising funds.

This year, there is a concern that an economic recession may adversely affect both the

number of persons attending the function and advertising space that will be sold in the

programme published for thee occasion.

Based on past experience and current prices and quotations, it is expected that the following

costs and revenues will apply for the function:

Required:

(a) Calculate the expected value of the profit to be earned from the dinner and dance this year.

(b) Recommend, with relevant supporting financial and cost date, whether or not the

Kenya Charity should spend Shs 500 on the market research enquiry and indicate the

possible benefits the enquiry could provide.

Date posted:

May 10, 2021

.

Answers (1)

-

It has been established that the reasons for the variances for the period ended 31

December 2002 are as follows;

i.80% of the extra material used is...

(Solved)

It has been established that the reasons for the variances for the period ended 31

December 2002 are as follows;

i.80% of the extra material used is due to purchasing from the cheaper

source. The balance off extra material usage is due to the amended

processing method, which was introduced.

ii.60% of the extra hours used is due to the amended processing method, the

balance of extra hours id due to the change to a cheaper material source.

Required

i. Prepare a schedule of costs for the four alternative strategies, which incorporate

different combinations of existing and amended material sources and conversion

process methods and hence determine the profit maximizing strategy.

ii. Prepare a report which discusses ways in which the alternative decision making

focus in each off sections (a) and (b) of the question has contributed to a change in

decision making strategy by the company.

Date posted:

May 10, 2021

.

Answers (1)

-

Tumbo Limited makes and sells executive towels to which the following standard

information relates:

i. Raw material is purchased at Shs 5.00 per square metre on a...

(Solved)

Tumbo Limited makes and sells executive towels to which the following standard

information relates:

i. Raw material is purchased at Shs 5.00 per square metre on a just-in- time basis. The

purchasing manager has the responsibility for the servicing of raw material.

ii. The executive towel is made in a conversion process in which the variable conversion

cost per product unit of output is estimated at Shs 12.50 (a half hour at Shs 25.00 per

hour). The conversion process manager is deemed responsible for material usage and

conversion process efficiency and expenditure variances.

The actual events for the period ending 31 December 2002, which may be considered as a

representative

of future periods, are as follows:

i. 27,000 square metres of raw material purchased at Shs 4.50 per square metre is used to

produce 8,000 units of the executive towels. The purchasing manager has made the

decision to0 buy from a cheaper source.

ii. 4800 hours of conversion process time at a variable cost of Kshs 20.00 per hour is

used to a achieve the output of Shs 8, 000 units of the executive towels. A charge in

the processing method was implemented at the start of the period.

Production capacity is available in order to produce in excess of 5,000 units of the executive

towels if the demand dictates.

Required:

i. Calculate standard cost variances for material usage and price and for

conversion process efficiency and expenditure for the period ended 31 December 2002.

ii. Suggest, giving your reasons, whether decisions should be based on:

1. The variances over which each manager has control or

2. The effect of each material cost variance and conversion cost variance

Date posted:

May 10, 2021

.

Answers (1)

-

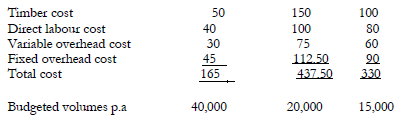

Chemex limited manufactures three garden furniture products A B and C. The budgeted unit cost and resource requirements of each of these items are detailed...

(Solved)

Chemex limited manufactures three garden furniture products A B and C. The budgeted unit cost and resource requirements of each of these items are detailed below.

These volumes are believed to equal the market demand for these products. The fixed

overhead costs are attributed to the three products on the basis of direct labour hours. The

labour rate is Shs 40 per hour. The cost of the timber is Shs 20 per square metre. The

products are made from a specialist timber.

A memo from the procurement manager advises you that because of a problem with the

supplier it is to be assumed that this specialist timber is limited in supply to 20,000 square

metres per annum.

The sales director has already accepted an order for 5,000 A, 1,000B and 1,500C, which if

not supplied would incur a financial penalty of Shs 20,000. These quantities are included in

the market demand estimates above.

The selling prices of the three products are:

A = Shs 200

B = Shs 500

C = Shs 400

Required

a) Determine the optimum production plan and state the net profit that this should

yield per annum.

b) Calculate and explain the maximum prices, which should be paid per square metre in

order to obtain extra supplies of the timber.

Date posted:

May 10, 2021

.

Answers (1)

-

SIMTON Limited has been operating a standard cost system and has accumulated the following information in relation to variances in its monthly management accounts:

ii. Out...

(Solved)

SIMTON Limited has been operating a standard cost system and has accumulated the following information in relation to variances in its monthly management accounts:

ii. Out of category B, connective action has eliminated 70% of variances, but the

remainder has continued.

iii. The cost of investigating averages is Shs 3,500 and that of connecting variances

averages Shs 5,500.

iv. The average size of any variance not connected is Shs 5,250 per month and the

company‟s policy is to assess the present value of such costs at 24% per

annum for a period of five months.

Required

(a) Prepare two decision trees, to present the position if an investigation is;

(i) Carried Out

(ii) Not carried

(b) Recommend, with supporting calculations, whether or not the company

should follow a policy of investigating variances as a matter of routine.

(c) Explain briefly two types of circumstances that will give rise to variances in category A

and two to those of category B.

(d) Mention any one variation in the information used that you feel would be beneficial to

the company of you wised to improve the quality of the decision making rule

recommended in (b) above. Explain briefly why you have suggested it.

Date posted:

May 10, 2021

.

Answers (1)

-

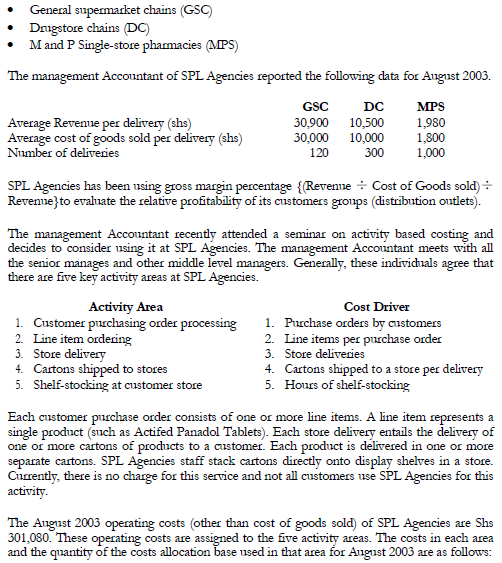

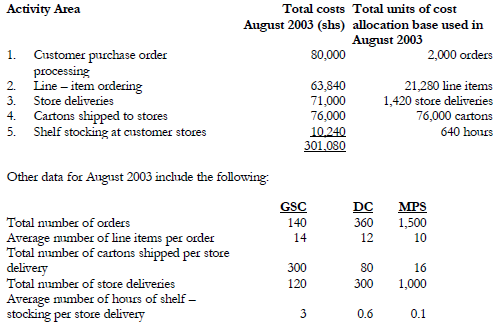

SPL Agencies specializes in the distribution of pharmaceutical products. They buy from pharmaceutical companies and resells to each of three different markets.

Required:

(a) Compute the August...

(Solved)

SPL Agencies specializes in the distribution of pharmaceutical products. They buy from pharmaceutical companies and resells to each of three different markets.

Required:

(a) Compute the August 2003 gross – margin percentage for each of its three distribution

markets and SPL Agencies operating income.

(b) Compute the August 2003 rate per unit of the cost allocation base for each of the five

activity areas.

(c) Compute the operating income of each distribution market in August 2003 using the

activity based costing information. Comment on the results.

Date posted:

May 8, 2021

.

Answers (1)

-

Majimbo Ltd. Is a multi-divisional company operating in several countries. Division X wants

to buy component for its final product. Suppliers outside Majimbo Ltd. Have given...

(Solved)

Majimbo Ltd. Is a multi-divisional company operating in several countries. Division X wants

to buy component for its final product. Suppliers outside Majimbo Ltd. Have given two bids

for sh.30,000 and 31,800. The supplier who bid sh.31,800 will in turn buy some raw

materials for sh.4,500 from Division Z of Majimbo Ltd. Which has spare capacity that will

increase A‟s contribution to overall company profits by sh.3,000. The supplier who

bids sh.30,000 will not buy any materials from Majimbo Ltd.

Required:

a) Prepare a diagram of the cash flow for both alternatives.

Does the use of the international market prices lead to optimal decision for Majimbo Ltd.? Explain

b) Suppose Division Y is working at full capacity and can provide the needed part to

Division X or to an outside customer at an assumed market price of sh.31,800. if market

pricing were the rule, division Y would have to meet the sh.31,000 bid. Further, assume

that the outlay costs to Y of filling the order were sh.22,500. Finally assume that Y,

unlike the outside suppler does not buy from Z because Majimbo Ltd is so large and

communications are so bad that the division Y management is unaware of this alternative.

c) Will the use of sh.31,800 as a transfer price lead to optimal decisions for Majimbo

Ltd? Show the net effects on cash flows.

Date posted:

May 8, 2021

.

Answers (1)

-

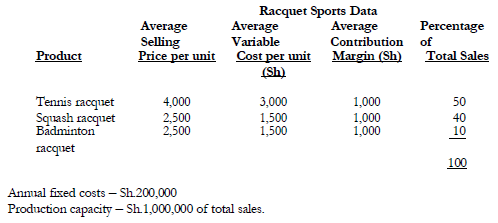

Racquet Sports produces a variety of racquets for the sports industry. It makes racquets for tennis, squash and badminton. The table below presents the relevant...

(Solved)

Racquet Sports produces a variety of racquets for the sports industry. It makes racquets for tennis, squash and badminton. The table below presents the relevant data for the products produced.

Required:

a) (i) Determine the contribution percentage on each shillings of sales for each of the

products produced and sold.

(ii) What is the overall contribution that each sales shillings provides toward covering

the firm‟s fixed costs, that is overall break-even point in shillings sales?

(iii) Determine the profits if the plants operates at 70 per cent of the plant capacity.

b) Explain the limitations of the techniques you have used to solve part (a) above.

Date posted:

May 8, 2021

.

Answers (1)

-

Paul Akili, an aggressive entrepreneur, is working on some make – or – buy decisions and a

related inventory system. For one such product, he decides...

(Solved)

Paul Akili, an aggressive entrepreneur, is working on some make – or – buy decisions and a

related inventory system. For one such product, he decides to use the classic economic – lot

– size model with no stockouts to determine an optimal order quantity. He initially

predicts that annual demand will be 2000 units, that each unit will cost sh.2,565, that the

incremental cost of processing each order (and receiving the ordered goods) will be Sh.3,819

in this case, and the incremental cost of storage will be sh.342 per physical unit per year.

Assume that the inventory cycle precisely repeats every year.

Required:

a) What is the optimal order quantity?

b) What are the total relevant costs of inventory from following your policy in (a) above?

c) Suppose that Paul Akili is incorrect in his sh.3,819 incremental – costs – per order

prediction but is precisely correct in all other predictions.

State and solve the equation to predict the maximum amount Paul Akili should pay to

discover the true incremental cost per order if:

(i) This true costs is sh.1,881 per order and

(ii) In the absence of any knowledge to the contrary, Paul Akili implement the

solutions in (a) above and will not alter it for one full year.

a) What happens t your answer in (c) above if we admit that Paul Akili has also made

errors in predicting demand price and the cost of storage?

d) Suppose Paul Akili implements the solution in (a) above for two years.

e) Further supposes that all of his initial predictions were, and are, correct except that the

actual incremental cost of storage is sh.1,140 per average unit.

If it costs Akili a total of sh.228 to alter his inventory policy, state the equation to

determine the cost of prediction error of not changing his inventory policy at the

beginning of the second year.

Date posted:

May 8, 2021

.

Answers (1)

-

Africa 1 and Kenya 1 are competing importers of lightweight industrial pick-up truck, the

“Miracle”. Market research suggests that there is demand for such vehicles of

about...

(Solved)

Africa 1 and Kenya 1 are competing importers of lightweight industrial pick-up truck, the

“Miracle”. Market research suggests that there is demand for such vehicles of

about 1,200 units per year evenly spread over the year and that bearing in mind the

facilities available on the truck, its price should be around Sh.550,000 but discounts may be

available. The price to the dealer is about Sh.400,000 depending upon exchange rates.

The management Accountant at Africa 1 has the task of determining the price to charge for the

vehicle that will give the greatest monthly profit from the sale of Miracles. Past experience

suggest that Africa1‟s market share and profit will give the greatest monthly profit

from the sale of Miracles. Past experience suggest that Africa1‟s market share and

profit depends not only on the price it charges, but also the price that Kenya 1 charges.

The following pattern seems to have emerged;

If both companies share the same price, then Africa 1 secures about 45% of the market and

Kenya 1 , 55%.

When Kenya 1 has a lower price, then Africa 1 loses about 3% market share for every

Sh.10,000 price difference. On the other hand, when Kenya1 has a higher price, then Africa

1 gains 2% market share over and above the 45% per sh.10,000 price difference. From

africa1‟s point of view, kenya1 normally changes its prices monthly.

Africa1‟s Management Accountant has ruled out trial and error pricing an has

decided to develop a simulation model to investigate price behaviour patterns based on

monthly periods.

Required:

a) Develop a simulation model from Africa1‟s point of view, using algebra, showing:

i An expression for monthly profits;

ii An expression for market share when Kenya1‟s price is the same as Africa 1‟s;

iii An expression for market share when Kenya1‟s price is higher than Africa1‟s;

iv An expression for market share when Kenya1‟s price is lower than Africa1‟s.

b) Draw a flow diagram to show how the model would be used to simulate pricing and

demand behaviour using a computer.

Date posted:

May 8, 2021

.

Answers (1)

-

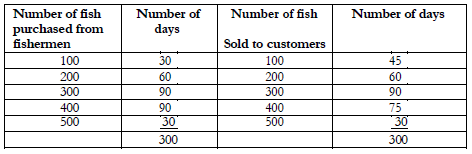

Peter Oloo is a fishmonger in Kisumu. As a result of adverse business changes in the region,

the supply and demand for fish are subject to...

(Solved)

Peter Oloo is a fishmonger in Kisumu. As a result of adverse business changes in the region,

the supply and demand for fish are subject to random variations making it difficult to

project the next day‟s business.

Management accounts in relation to the previous 300 days reveal the following mode of behaviour:

Peter Oloo buys each fish at Sh.40 and sells it for Sh.60 if sold on the same day; if the fish is

sold the following day it will fetch only Sh.20. If not sold during the second day its value

drops to zero and Peter Oloo do nates it to children‟s home. Peter Oloo‟s Policy is to

satisfy the days demand from the fresh fish first; and any further demand will be satisfied

from the stock of fish from previous day. Failure to satisfy demand costs Peter Oloo Sh.20

for every fish supplied to the customer. There are no back orders in the business.

Required:

a) Simulate Peter Oloo's operations for 8 days clearly indicating profits made each day.

b) What are the average daily profits for Peter Oloo?

Use the following random numbers

573423709751483681320931644925928345

Date posted:

May 8, 2021

.

Answers (1)

-

LP Ltd. produces two products, K-A and K-B by a joint process. One unit of input

X processed in Department 1 total will yield three units...

(Solved)

LP Ltd. produces two products, K-A and K-B by a joint process. One unit of input

X processed in Department 1 total will yield three units of product K – A and two units

of K – B. The variable operating costs in Sh.2.50 per unit of input X processed. Each

unit of product K-A can either be sold at the split-off point for Sh.10 per unit or

processed further in Department 2 to for product K-C. One unit of product K-A is

needed to produce one unit of K-C. Variable processing costs incurred in Department 2

amount to Sh.7.50 per unit of K-A processed and each unit of K-C can be sold at a

price of Sh.22.50 product K-B can be sold at Sh.8.75 per unit at the split-off point.

Highly skilled labour is required in each of the two departments and the total available

labour force is limited to 80,000 hours per week. To process one unit of X requires 1.5

direct-labour hours. If K-A is processed further, three hours per unit of K-A processed

are needed. Furthermore raw material X can be acquired up to a maximum quantity of

40,000 units per week.

The company „s market survey shows that the maximum weekly demand for product K-A is

40,000 units and for product K-C is 5,000 units. The survey further concludes that virtually any

amount of product K-B can be sold immediately without difficulty. Weekly production does not

have to be equal to weekly sales for any of the company‟s products.

However, since all three products are perishable, any unsold quantity at the end of the

week will be discarded.

Required:

(i) Formulate a linear programe to determine the optimal weekly production mix for

LP Ltd. that maximizes profits subject to the various production, market and technology constraints.

Do not solve for optimal values but clearly define your variables.

(ii) Independent of (a) above, assume that at the optimum, the marginal values

associated with the maximum market demand for K-A constraint, the maximum

market demand for K-C constraint and the maximum supply of X constraint are

Sh.10, Sh.15 and Sh.15 respectively. Assume further that all other constraints have

zero marginal values.

What is the maximum achievable contribution? Show calculations.

Date posted:

May 8, 2021

.

Answers (1)

-

Briefly give five examples of business applications of linear programming.

(Solved)

Briefly give five examples of business applications of linear programming.

Date posted:

May 8, 2021

.

Answers (1)

-

Through the end of 1993, Viatu Ltd., a shoe manufacturer had always sold its products

through distributors. In 1993, the turnover was Sh.87,500,000 and net profit...

(Solved)

Through the end of 1993, Viatu Ltd., a shoe manufacturer had always sold its products

through distributors. In 1993, the turnover was Sh.87,500,000 and net profit was 10 per cent

of turnover. Total fixed expenses (manufacturing and selling) were Sh.17,500,000.

During 1993, a number of Viatu's competitors had begun selling their products

through distributors. Viatu's marketing research group was asked to predict the effects of

eliminating distributors from the channels of distributors and selling direct to retailers.

The group was instructed to predict both changes in sales volume and changes in selling

expenses, under the provision that the selling price per unit would remain unchanged.

The marketing analysis yielded the following predictions:

Turnover in1994 would drop 20 percent from the 1993 figures, but net profit for 1994

would rise to Sh.9,100,000 owing to savings in selling expenses.

This net savings in selling expenses from eliminating the “middleman” was

impressive, since total fixed expenses manufacturing and selling) would increase to

Sh.18,900,000 because of the additional warehouse and delivery facilities required:

If the 1993 distribution system were continued, however, 1994, results would replicate 1993.

Required:

a) What was the breakeven point (turnover) under the original situation prevailing in 1993?

b) What would be the breakeven point (turnover) under the proposed situation for 1994?

c) On the basis of this analysis, Viatu Ltd, adopted the new direct-distribution plan for

1994, and reduced 1994 production on the 70,000,000 turnover level. Unfortunately, it

became clear by early December 1994 that sales would reach only 66,500,000 and

Viatu cut back productions so that no ending inventory remained.

Variable costs per unit and total fixed costs were as predicted.

Compute the cost of Viatu‟s prediction error.

Assume that sales would have been Sh.87,500,000 if the 1993 distribution system had

been continued.

Date posted:

May 8, 2021

.

Answers (1)

-

Mitumba Ltd. has set the following standards:

Required:

Comprehensive computation showing the yield, mix and price variances.

(Solved)

Mitumba Ltd. has set the following standards:

Required:

Comprehensive computation showing the yield, mix and price variances.

Date posted:

May 8, 2021

.

Answers (1)

-

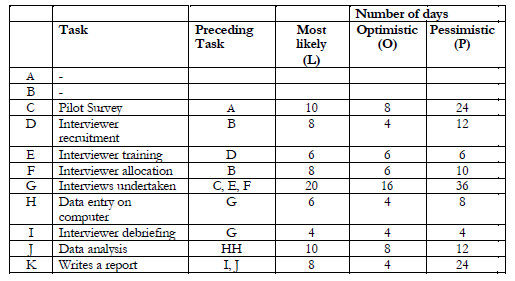

Uchunguzi Ltd. plans to conduct a questionnaire survey. The table below shows the tasks involved, the immediately proceeding tasks and for each task duration the...

(Solved)

Uchunguzi Ltd. plans to conduct a questionnaire survey. The table below shows the tasks involved, the immediately proceeding tasks and for each task duration the most likely estimate (L), optimistic estimate (O) and the pessimistic estimate (P).

Using the project evaluation and review technique (PERT) the meantime, M and standard

deviation O. for the duration of each task are estimated from t he most likely (L), Optimistic

(O) pessimistic (P) estimates by using the formulae:

M = 0.08333 (4L + O + P)

O = 0.08333 (P – O)

Required:

a) Compute the mean duration and standard deviation for each task.

b) The project is budgeted to cost Sh.500,000. Actual costs per day are Sh.10,000.

Can the project be implemented within the budget?

Date posted:

May 8, 2021

.

Answers (1)

-

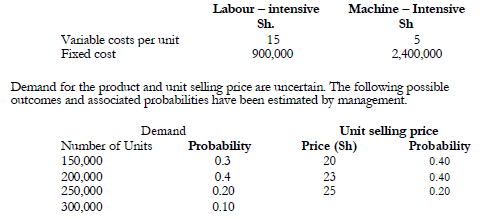

Mwendandamu Company Ltd. can produce a product using either labour-intensive or machine-intensive operations. Cost of each method are as follows:

Required:

a) Develop probability tree to show...

(Solved)

Mwendandamu Company Ltd. can produce a product using either labour-intensive or machine-intensive operations. Cost of each method are as follows:

Required:

a) Develop probability tree to show the possible profits from labour-intensive and

machine-intensive production.

b) Determine the following for each production method:

i Expected profits;

ii Probability of at least breaking even;

iii Probability of profits of at least Sh.1,000,000.

c) Which production method do you prefer and why?

d) Discuss other factors that Mwendamu Company Ltd.'s management should

consider before deciding on the production method.

Date posted:

May 8, 2021

.

Answers (1)

-

Chakula Engineering Company Limited (CECL) recently sent their chief designer to the

USA and UK to review developments in the American and British Markets. He has...

(Solved)

Chakula Engineering Company Limited (CECL) recently sent their chief designer to the

USA and UK to review developments in the American and British Markets. He has now

returned with details of a new type of food mixer that is being developed over there. CECL

are considering the design and manufacture of a liquidizer gadget attachment to be used as

an extra gadget for the new mixer when it is sold in Kenya. The chief designer‟s notes

show that 10% of the experts he questioned in both the UK and USA believed the new

mixer would reach the Kenyan market in a year‟s time, whereas 30% thought it

would be launched in four year‟s time, and the remainder suggested a five-year delay

before it reached Kenyan.The presents value (PV) of net cash flows form making and selling

the liquidizer are estimated by the company to be sh.8 million, if the market develops one

year from now and sh.3.2 million if it develops five years from now.

CECL have not developed a liquidizer before, and whilst it immediate development would

cost Sh.2 million, they feel they have only a 50% chance of a successful development at

present. A number of alternative courses of action present themselves. The company could

abandon the whole project, or wait for one year to see if the mixer has penetrated the

Kenyan market. They would then abandon or develop the liquidizer at a PV cost of Sh.1.8

million, with a 70% chance of success, but they would be late into the market and the PV of

their receipts they estimate at Sh.4.8 million, including the expenditure of Sh.400,000 on

acquiring extra product data during the second year of delay, and the chance of a successful

development would be 90%. At this point, however, the mixer could only come on the

market at the four or five year point from now.

Required:

Using a decision tree approach, advise the company on the course of action to adopt.

Date posted:

May 8, 2021

.

Answers (1)

-

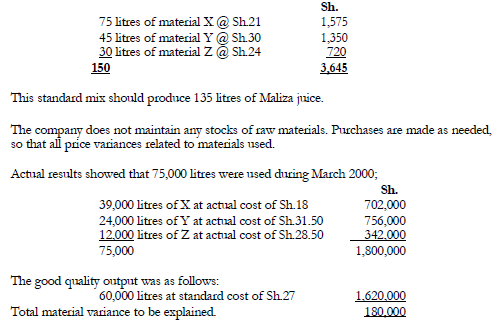

Uganda Ltd. has the following standards for producing an alcoholic beverage:

Every 100 litres of input should yield 80 litres of Chovi, the finished product.

The production...

(Solved)

Uganda Ltd. has the following standards for producing an alcoholic beverage:

Every 100 litres of input should yield 80 litres of Chovi, the finished product.

The production manager is supposed to make the largest possible amount of finished

product for the least cost. He has some leeway to alter the combination of materials within

certain wide limits, as long as the finished product meets specified quality standards. Actual

results showed that 400,000 litres of Chovi were produced during last week. The raw

materials used in this production were 280,000 litres of 590N and 240,000 litres of KAG. No

price variances were experienced during the period.

Required:

a) A presentation of yield and mix variances.

b) Comment on the performance of the manager.

Date posted:

May 8, 2021

.

Answers (1)