In ABC overheads can be classified into:

Short-term variable overheads Long-term variable overheads and Fixed overheads

Short-term variable overheads:Cost that vary with production volume and therefore would be classified as variable costs in traditional absorption costing e.g indirect material costs which may vary with material inputs, direct labour, cost of power -varies with machine hours etc.

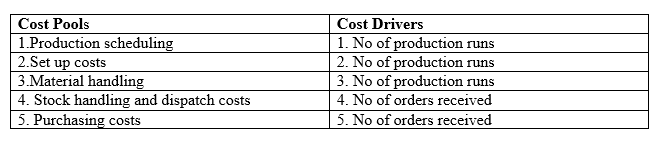

Long term variable costsThese are long term OH costs which do not vary with volume but do vary with other measures of activity (usually in the long term) e.g cost of support activities e.g such as stock handling costs, production scheduling, machine set up costs etc. These costs are fixed in the short term but vary in the long term according to the range and complexity of the products manufactured. ABC requires that these overheads be traced to products by transaction based cost drivers rather than volume based drivers.

Fixed OverheadsCosts which do not vary, for any given time period with any activity indicators e.g salary of MD- overhead with no clear variation method.

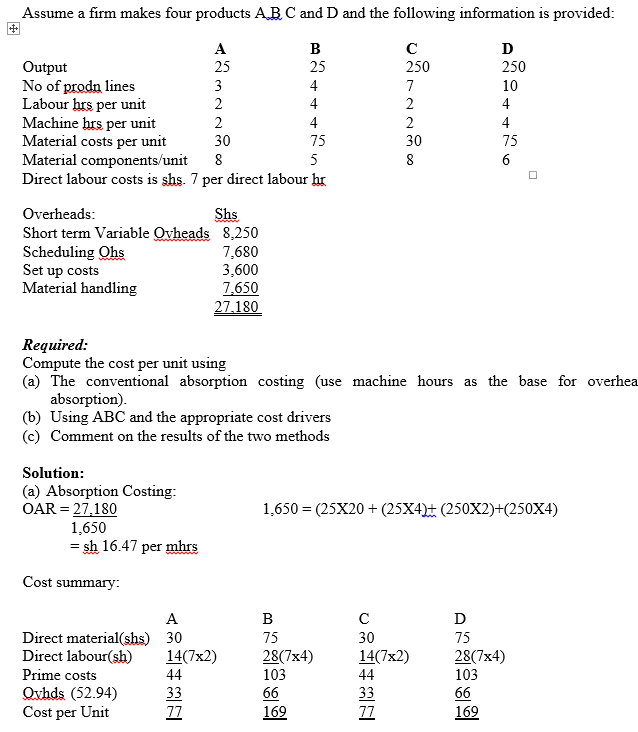

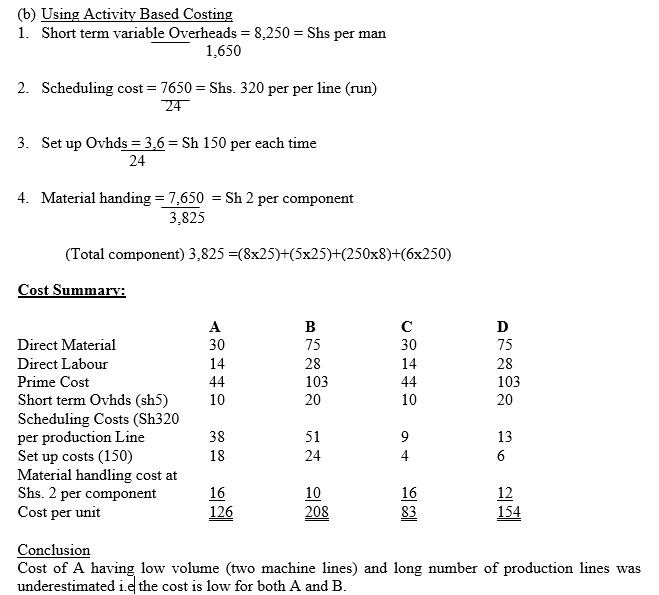

Illustration

Titany answered the question on

October 12, 2021 at 07:39