-

Wabunge Ltd. operates a defined benefits plan for its employees. Both employees and the employer contribute to the plan. Details of the defined benefits plan...

(Solved)

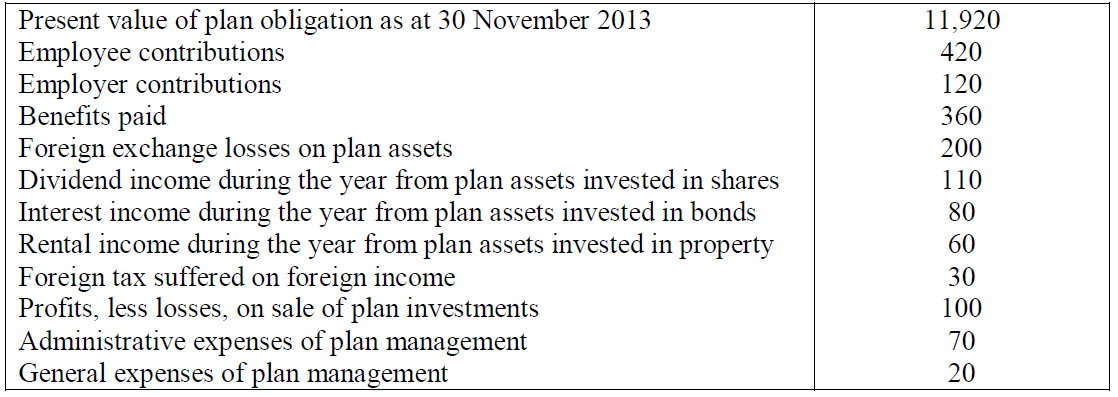

Wabunge Ltd. operates a defined benefits plan for its employees. Both employees and the employer contribute to the plan. Details of the defined benefits plan for the year ended 30 November 2013 were as follows:

The interest rate on high quality corporate debt (constant during the year) was 4.75% per annum.

Additional information:

1. Benefits paid employer contributions and employee contributions were all spread evenly over the year.

2. The past service cost arose as a result of an improvement to benefits offered to all plan members effective from 1 November 2012. In order to receive the benefit, plan members must have remained in employment until at least 30 November 2013. The figure above is the total expected cost as calculated by the actuary.

Required:

(i) The notes to the financial statements required by IAS 19: Employee Benefits (revised 2011) in respect or changes in plan assets, changes in the defined benefits plan obligation and amounts recognized in profit or loss and other comprehensive income

(ii) Statement of changes in net assets available for benefits for the plan itself as required by IAS 26 (Accounting and Reporting by Retirement Benefit Plans).

(NB: Round off all figures to the nearest shilling).

Date posted:

December 12, 2021

.

Answers (1)

-

A company has granted 10,000 cash-settled awards to each of its 500 employees on condition that the employees remain in its employment for the next...

(Solved)

A company has granted 10,000 cash-settled awards to each of its 500 employees on condition that the employees remain in its employment for the next three years. Cash is payable at the end of the three years based on the share price of the company's shares on such a date.

35 employees leave during year 1. The company estimates that 60 additional employees will leave during years 2 and 3. The share price at the end of year 1 is Sh.14.40.

40 employees leave during year 2. The company estimates that 25 additional employees will leave during year 3. The share price at the end of year 2 is Sh. 15.50.

22 employees leave during year 3. The share price at the end of year 3 is Sh. 18.20

Required:

Computations to show how the company would recognize the above awards.

Date posted:

December 11, 2021

.

Answers (1)

-

Baobab Ltd. was incorporated on 1 April 2000. In the year ended 31 March 2001, the company made a profit before taxation of Sh.10, 000,000...

(Solved)

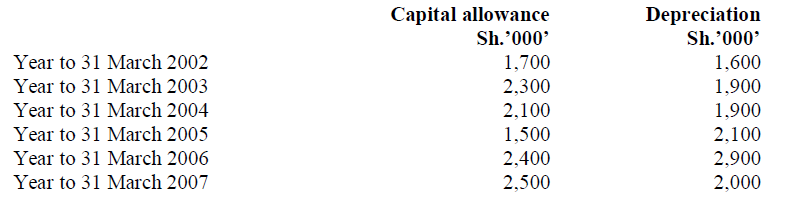

Baobab Ltd. was incorporated on 1 April 2000. In the year ended 31 March 2001, the company made a profit before taxation of Sh.10, 000,000 (depreciation charged being Sh.1, 000,000). The company had made the following capital additions:

Plant - Sh.4,800,000

Motor vehicles - Sh.1,200,000

Corporation tax is chargeable at the rate of 30%. Capital deductions are computed at the rate of 25% per annum on written-down value.

The company has prepared capital expenditure budgets as at 31 March 2001 which reveal the following patterns:

From 1 April 2007, capital allowances are expected to exceed depreciation charges each year.

Required:

(i). Compute the corporation payable for the year ended 31 March 2001

(ii). Compute the deferred tax charge for the year ended 31 March 2001 on:

- Full-provision basis

- Partial-provision basis

(Show the profit and loss account and balance sheet extracts with respect to the provisions under each method).

Date posted:

December 11, 2021

.

Answers (1)

-

Jahazi Group is estimating the deferred tax liability as at 31 May 2010 and has provided the following information:

1. Property, plant and equipment has a...

(Solved)

Jahazi Group is estimating the deferred tax liability as at 31 May 2010 and has provided the following information:

1. Property, plant and equipment has a cost and revalued amount of sh.100 million and accumulated depreciation of Sh.18 million. Total capital allowances on property, plant and equipment amount to Sh.30 million.

2. The group has available for sale(AFS) financial assets that were purchased during the year at a cost of sh. 10 million. There was a revaluation gain of sh.2 million reported in the AFS reserve.

3. The group spent Sh.50 million to develop a new product and out of which Sh.10 million has been charged in the income statement as amortization for the year. The balance of Sh.40 million is shown as intangible assets in the statement of financial position. The full amount of Sh.50 million was allowed for tax purposes in the year.

4. Total inventory was carried at Sh. 20 million which was the net realizable value. The cost of the inventory was Sh.22 million. There was an unrealized profit of Sh.1 million that had not been deducted from the inventory on consolidation.

5. The receivables amounted to sh.30 million after making a provision of Sh.2 million for a doubtful debt. The amount also included a foreign exchange gain of Sh.1 million. Exchange gains or losses and doubtful debts are only allowed for tax purposes when they are realized.

6. The trade and other payables of Sh.40 million include an accrual of Sh. 5 million which relates to pension and other employee benefits to be paid in the year 2011. These are only allowed for tax purposes when paid.

7. The deferred tax liability as at 1 June 2009 was Sh.8.5 million.

8. Assume that the temporary differences due to the revaluation of property, plant and equipment amount to Sh.2 million and the corporation tax rate is 30%.

Required:

Compute the deferred tax balance as at 31 May 2010 and the charge to the income statement for the year ended 31 May 2010.

Date posted:

December 11, 2021

.

Answers (1)

-

Explain the following methods of providing for deferred tax and indicate which is the preferred method under IAS 12(Income Taxes):

i) Nil provision.

ii) Partial provision.

iii) Full...

(Solved)

Explain the following methods of providing for deferred tax and indicate which is the preferred method under IAS 12(Income Taxes):

i) Nil provision.

ii) Partial provision.

iii) Full provision.

Date posted:

December 11, 2021

.

Answers (1)

-

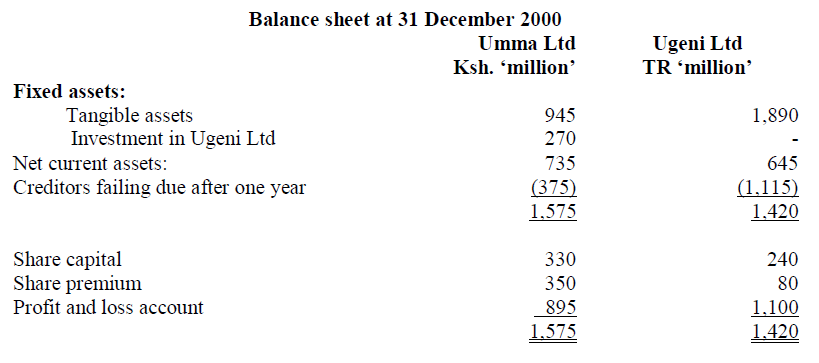

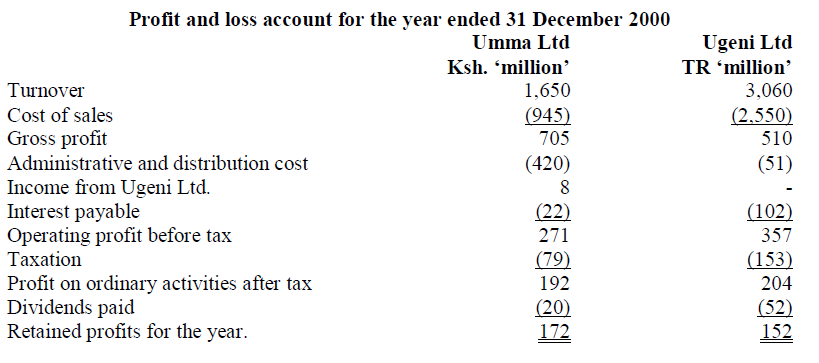

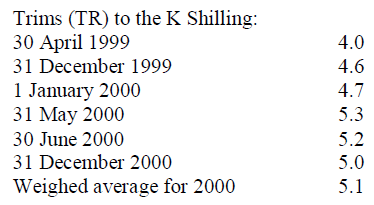

Umma Ltd. A public company quoted on the Nairobi Stock Exchange, owns 80% of Ugeni Ltd. A public company which is situated in a foreign...

(Solved)

Umma Ltd. A public company quoted on the Nairobi Stock Exchange, owns 80% of Ugeni Ltd. A public company which is situated in a foreign country, Timoa. The currency of this country is Trim(TR). Umma Ltd. acquired Ugeni Ltd. on 30 April 1999 for Ksh.220 million when the retained profits of Ugeni Ltd. were TR 610 million. Ugeni Ltd. has not issued any shares since acquisition. The following financial statements relate to the two companies.

Additional information:

1. During the year, Ugeni Ltd. sold goods to Umma for TR 104 million and made a profit of TR 26 million on the transaction. All of the goods, which were exchanged on 30 June 2000 remained unsold at the year end. At 31 December 1999 there were goods sold by Ugeni Ltd. to Umma Ltd held in the stock of Umma Ltd. These goods were valued at Ksh.6 million on which Ugeni Ltd. made a profit of Ksh.2 million.

2. Ugeni Ltd. paid the dividend for the year ended 31 December 2000 on 30 June 2000. No other dividend was proposed for the year. The tax effect has been accounted for and may be ignored.

3. The fair value of the net assets of Ugeni Ltd. at the date of acquisition was TR 1,040 million. The fair value increment all due to tangible fixed assets has not however been incorporated in the books of Ugeni Ltd.

4. Goodwill fractuates with changes in the exchange rate.

5. Tangible fixed assets are depreciated over five years on a straight-line basis with a full year’s charge provided in the year of acquisition.

6. A loan of Ksh.50 million was raised by Ugeni Ltd. from Umma Ltd on 31 May 2000. The loan is interest free and is repayable in 2009. The loan is included in the cost investment in Ugeni Ltd. An amount of TR 65 million had been paid to Umma Ltd on 31 December 2000 in part settlement on the loan. The amount had not been received by Umma Ltd. and had not been included in its financial statements as at 31 December 2000.

7. The following exchange rates are relevant for translation:

8. The functional currency of Ugeni Ltd was different from the presentation currency of the Group (Kshs).

Required:

(a). Consolidated profit and loss account for the year ended 31 December 2000

(b). Consolidated balance sheet as at 31 December 2000

(c). Statement for the movement in consolidated reserves for the year ended 31 December 2000

Date posted:

December 11, 2021

.

Answers (1)

-

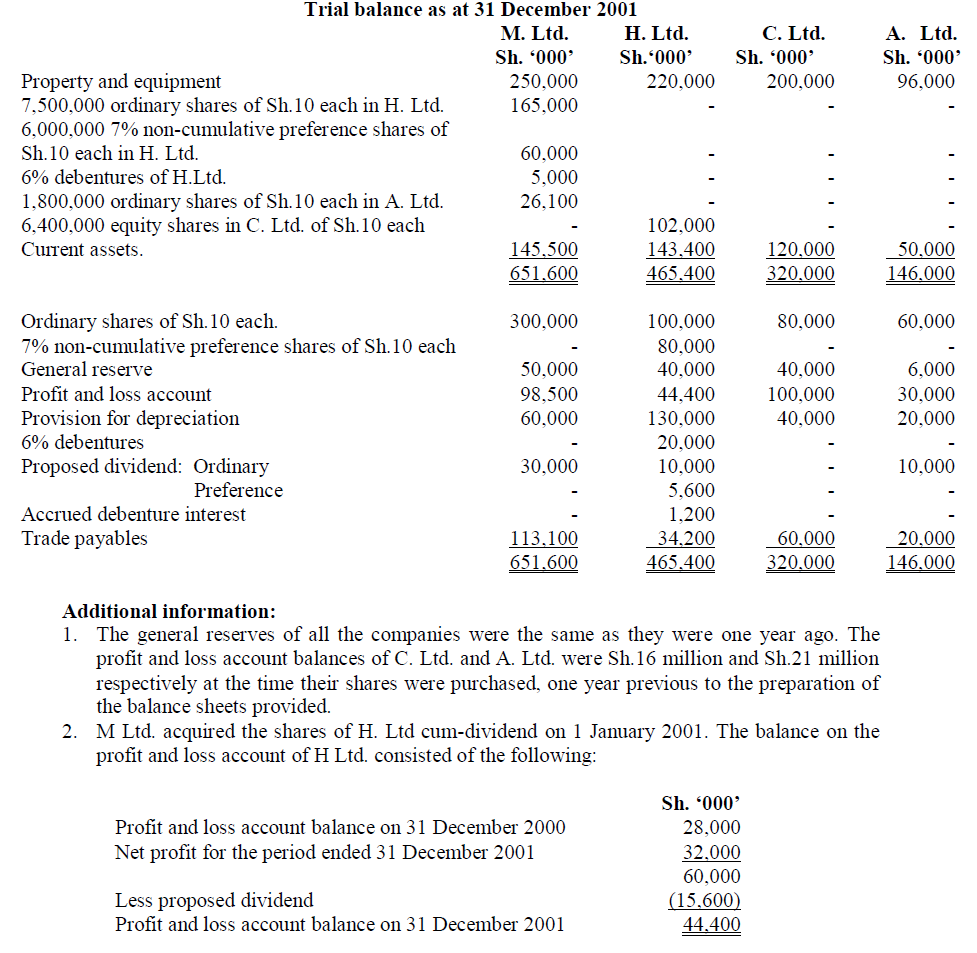

M Ltd. started operating several years ago. As a strategy to expand its operations, its management has in the recent past purchased shares from other...

(Solved)

M Ltd. started operating several years ago. As a strategy to expand its operations, its management has in the recent past purchased shares from other companies, whose trial balances are given below:

3. The balance on the profit and loss account of H. Ltd. at the acquisition date is after providing for preference dividend of Sh5.6 million and a proposed ordinary dividend of Sh.5 million, both of which were subsequently paid and credited to the profit and loss account of M. Ltd.

4. No entries have been made in the books of M Ltd. in respect of debenture interest due from, or proposed dividends from two of its investments, except that dividends due from A Ltd were credited to M Ltd.’s profit and loss account and the corresponding entry made in its debtors.

5. The debentures of H Ltd were purchased at par.

6. The stock in trade of H Ltd. on 31 December 2001 includes Sh.6 million in respect of goods purchased from M. Ltd. These goods had been sold by M. Ltd at such a price that M. Ltd earned a profit of 20% on the invoice price.

7. The group policy is to account for any associate company using the equity method. Goodwill arising on consolidation is amortized using the straight line method over a useful life of five years, (assuming a zero residual value) a proportionate charge being made for any period of control of less than a full year. All unrealized profit on closing stock is removed from the accounts of the company that realized it, giving a proportionate charge to the minority interest if appropriate.

8. Dividends to minority interest shareholders are shown as part of minority interest.

9. H Ltd. sold a fixed asset on 31 December 2001 to M Ltd. for Sh.20 million, making a 20% profit on the invoice price. H. Ltd. depreciates its assets at 20% using the straight line method. H Ltd.’s accountant erroneously used selling price for depreciation purposes, however the cost of assets reflected the correct amounts

Required:

A consolidated balance sheet of M Ltd. and its subsidiaries as at 31 December 2001

Date posted:

December 11, 2021

.

Answers (1)

-

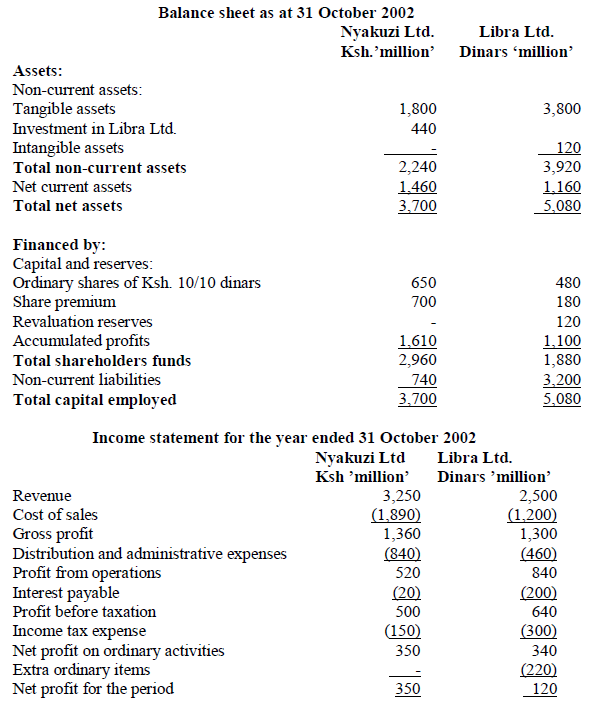

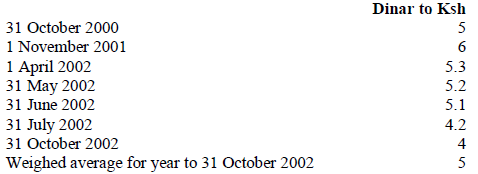

Nyakuzi Ltd., a public limited company, listed at the Stock Exchange, owns 80% of the ordinary share capital of Libra Ltd., a public limited company...

(Solved)

Nyakuzi Ltd., a public limited company, listed at the Stock Exchange, owns 80% of the ordinary share capital of Libra Ltd., a public limited company which is incorporated in a foreign country whose local currency is dinars.

Nyakuzi Ltd. acquired Libra Ltd. on 1 November 2001 for Sh.440 million when the retained profits of Libra Ltd. were 990 million dinars. Libra Ltd. has not issued any share capital nor revalued any of its assets since acquisition.

The directors of Nyakuzi Ltd. have now received the financial statements of their foreign subsidiary and intend to prepare the consolidated financial statements of the group for the year ended 31 October 2002.

The directors have been made aware of the fact that since the professional accountancy body in the foreign country does not require the mandatory compliance with International Accounting Standards (IAS’s) by its members, the accounting treatment of several items in the subsidiary’s financial statements may need adjustment to comply with relevant International Accounting Standards before being incorporated in the group’s consolidated financial statements.

The following financial statements relate to the two companies:

The following additional information relates to the financial statements of Libra Ltd. for the year ended 31 October 2002.

1. Under local accounting standards, Libra Ltd. had capitalized an asset “market shares” under intangible assets. This asset arose when Libra Ltd. acquired a company in the year ended 31 October 2002 and merged the companies activities with its own. This acquisition allowed Libra Ltd. to obtain a significant share of a specific market and therefore, the excess of the price paid over the fair value of assets is the “market shares” The amount capitalized was 120 million dinars and no amortization is charged by Libra Ltd. on “market shares”.

2. The amounts classified as extraordinary items in Libra Ltd’s income statement is made up as follows:

(i). Revaluation loss

A non-current assets was physically damaged during the year and an amount of 90 million dinars was written off its carrying value as an impairment loss. This asset had been revalued on 31 October 2000 and a credit of 60 million dinars still remains in the revaluation reserve in respect of this asset.

(ii). Change in accounting policy

A change in accounting policy for research expenditure was made during the period in order to comply with IAS 38. Prior to November 2001, research expenditure was capitalized. The amount included in extra-ordinary items is 130 million dinars.

3. The fair value of the net assets of Libra Ltd. at the date of its acquisition by Nyakuzi Ltd. was 2,400 million dinars after making changes to comply with the International Accounting

Standards (IAS’s). Goodwill fluctuates with changes in the exchange rate.

4. Nyakuzi Ltd. sold Ksh.150 million of components to Libra Ltd. on 31 May 2002, when the legal ownership of goods passed to Libra Ltd. Due to a problem in shipping; these goods were received by Libra Ltd. on 30 June 2002. Nyakuzi Ltd. made a profit of 20 per cent on selling price of the component. All of the goods had been utilized in the production process at 31 October 2002 but none of the finished goods had been sold at that date. Libra Ltd. had paid for the goods on 31.7.2002. This was the only inter-company transaction in the year. Foreign exchange gains/losses on such transactions are included in cost of sales by Libra Ltd.

5. A dividend of Ksh. 40 million had been paid by Nyakuzi Ltd. during the year.

6. The following exchange rates were relevant:

7. The directors have indicated that Libra Ltd. operates as a separate entity with little management interference from the holding company.

Required:

(a). A consolidated income statement for the year ended 31 October 2002

(b). A consolidated balance sheet for Nyakuzi Ltd. group as at 31 October 2002

(Show any exchange gains/losses arising in the consolidated financial statement)

Date posted:

December 10, 2021

.

Answers (1)

-

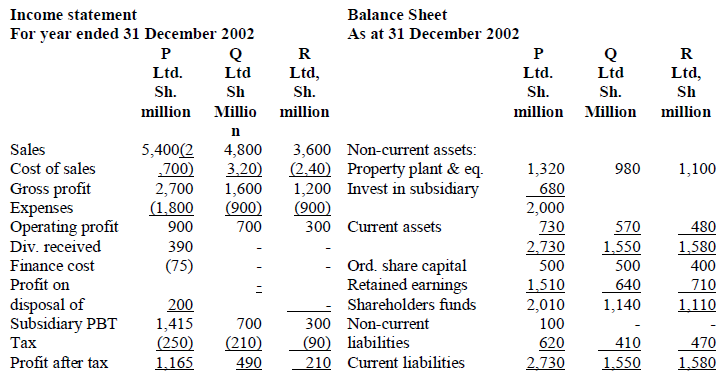

P. Limited is a company quoted on the Nairobi Stock Exchange. Its area of operations is capital equipment. It purchased 80% of the ordinary share...

(Solved)

P. Limited is a company quoted on the Nairobi Stock Exchange. Its area of operations is capital equipment. It purchased 80% of the ordinary share capital of Q Limited on 1 January 1998. Q Limited is a leading producer of cement and lime in the area. P. Limited purchased 75% of the ordinary share of the capital of R Limited on 1 January 1999. R. Ltd. is a leading producer of decorative coatings. This market has suffered a major decline since the investment was made. A suitable purchaser bought the complete shareholding on 31 August 2002. The proceeds of the sale were used to repay debt on 31 August 2002. The financial statements of the companies for the year ended 31 December 2002 are as follows:

Additional information:

1. P. Ltd. had purchased its shareholdings in Q Ltd and R Ltd. when the balances of retained earnings were Sh.100 million and Sh.200 million respectively. Neither Q Ltd nor R. Ltd has issued any ordinary shares since they were acquired by P Ltd. The fair values of the identifiable net assets of both Q Ltd. and R Ltd were equal to their carrying values at the dates of acquisition. The investment in R. Ltd had cost P. Ltd. Sh.570 million.

2. No impairment losses have occurred in respect of their investment.

3. P Ltd., Q Ltd. and R Ltd. had paid dividends of Sh.500 million, Sh.300 million and Sh.200 million respectively on 31 July 2002.

4. There is no tax charge on the sale of the investment in R. Ltd.

5. P. Ltd, Q Ltd and R Ltd. are managed as three separate business segments. The group ‘s primary segment reporting format is business segments. The board of directors of P Ltd decided to sell the shares in R Ltd when they met on 14 February 2002 to review the performance of the three companies for year ended 31 December 2001. There were no impairment losses in any of the assets of R Ltd prior to its sale. The directors did not announce the plan to sell R Ltd because they thought this would adversely affect the price at which they could sell the subsidiary. A public announcement was made on 31 August 2002.

6. The directors want the amount of the revenue, expenses, pre-tax profit and the tax expense of the discontinuing operation to be shown in separate column of the income statement and the amount of the cash flow attributable to the operating, investing, financing activities of the discontinuing operation shown in a separate column of the cash flow statement.

Required:

(a). Describe in the context of International Financial Reporting Standard (IFRS) 5 when a disposal group can be classified as a Held-For-Sale.

(b). In the context of P Ltd, state the day when the classification criteria for Held-For-Sale was met.

(c). State four items of information (other than those included in note 6 above.) which should be included in the financial statements in relation to the discontinued operation.

(d). The financial statements of all the group companies for the year ended 31 December 2001 were authorized for issue on 11 March 2002. Should the financial statement for the year ended 31 December 2001 disclose any information about the plan sale of R Ltd.

(e). Prepare the income statement of the group for the year ended 31 December 2002, with separate columns for “continuing Operation” “Discontinued operation” and “Enterprise as a whole” Sales, cost of sales and expenses in R Ltd accrue evenly over the year. The accounting policy note in the financial statements include the following clause: Operating results of subsidiaries sold during the financial year are included up to the date effective control ceased. There were no inter-company transactions.

(f). Prepare the group balance sheet as at 31 December 2002.

(g). A statement of changes in equity as at 31 December 2002 showing only one column for ‘retained earnings’.

Date posted:

December 10, 2021

.

Answers (1)

-

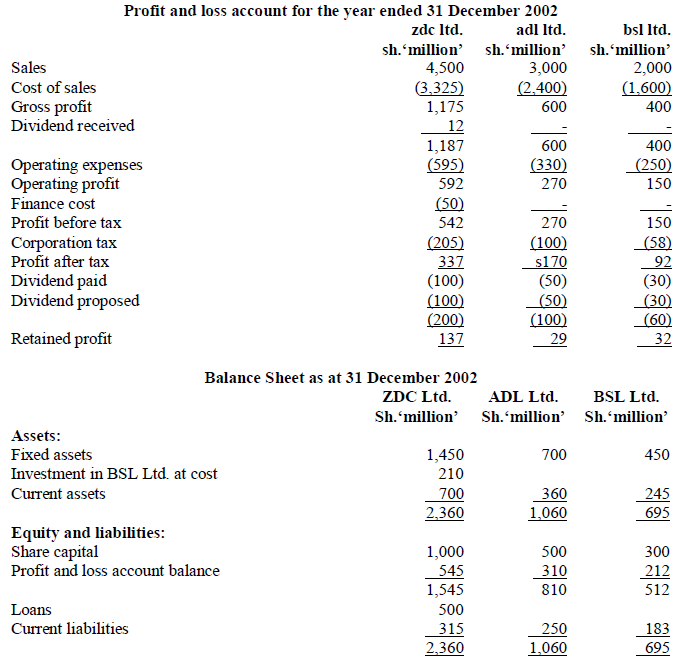

ZDC Ltd. acquired 40% of the ordinary shares of BSL Ltd. on 1 January 1999 for Sh.210 million when the credit balance on the profit...

(Solved)

ZDC Ltd. acquired 40% of the ordinary shares of BSL Ltd. on 1 January 1999 for Sh.210 million when the credit balance on the profit and loss account of BSL Ltd. was Sh.100 million.

On 1 July 2002, the directors of ZDC Ltd. acquired 90% of the ordinary shares of ADL Ltd. The purchase consideration was settled by the issue of 24 million ordinary shares of ZDC Ltd. which have a par value of Sh.20 but had a market value of Sh.32.50 as at 1 July 2002.

The financial statements of the three companies for the financial year ended 31 December 2002 are provided below:

Additional information:

1. On 1 January 2002, ZDC Ltd., held stock of goods purchased from ADL Ltd. during the year ended 31 December 2001 at a cost of Sh.25 million ADL Ltd. had made a profit of 20% on the selling price of the goods. None of the goods were included in the closing stock of ZDC Ltd. as at 31 December 2002.

2. During the year ended 31 December 2002, ADL Ltd made total sales of Sh.600 million to ZDC Ltd. The sales were made at a profit of 25% on cost of and one-fifth of the goods were included in the closing stock of ZDC Ltd. as at 31 December 2002. The sales were made evenly during the year.

3. The fair values of the fixed assets of ADL Ltd. as at 1 July 2002 were the same as the net book values.

4. As at 31 December 2002, ZDC Ltd. had in its closing stock, goods worth Sh.50 million which were purchased from BSL Ltd. BSL Ltd. had made a profit of Sh.10 million on this transaction.

5. ZDC Ltd. does not accrue its share of proposed dividends from group companies.

6. The trading results of ADL Ltd. accrued evenly during the year

7. ZDC Ltd. has not accounted for its cost of investment in ADL Ltd.

Required:

(a). The consolidated profit and loss account of ZDC Ltd. and its subsidiary ADL for the year ended 31 December 2002 using the:

(i). Acquisition method

(ii). Merger method

(b). The consolidated balance sheet of ZDC Ltd. and its subsidiary ADL Ltd. as at 31 December 2002 using the:

(i). Acquisition method

(ii). Merger method

Date posted:

December 10, 2021

.

Answers (1)

-

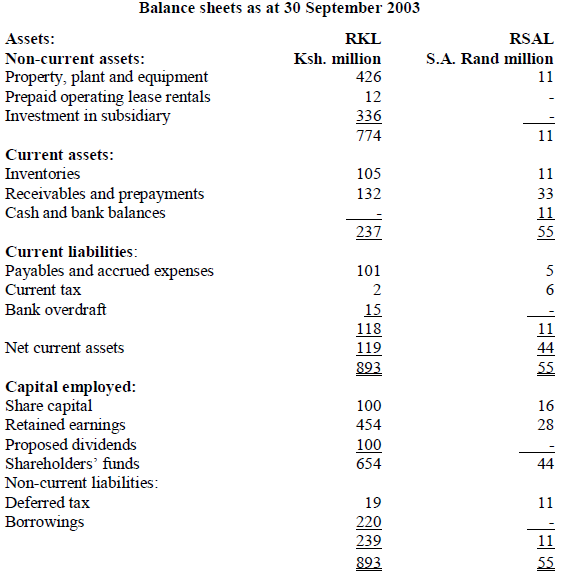

Rose Kenya Limited (RKL) exports roses to the flower auctions in Holland where its roses are consistently rated A1. In order to reduce over-reliance on...

(Solved)

Rose Kenya Limited (RKL) exports roses to the flower auctions in Holland where its roses are consistently rated A1. In order to reduce over-reliance on single supply source, RKL purchased 80% of the ordinary share capital of Roos South Africa Limited (RSAL) on 1 January 2003. Both companies make up their accounts to 30 September each year. Neither company has any trade with the other. Both companies compete for market share in the auctions in Holland. The operations of RSAL are carried out with a significant degree of autonomy from those of RKL.

The following are the draft financial statements of the two companies prepared in Kenya Shillings (Ksh.) for RKL and South African Rand (S.A. Rand) for RSAL.

Additional information:

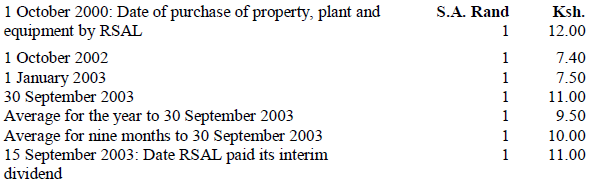

1. RKL financed part of the purchase price paid for the investment in RSAL by taking out a South African Rand denominated loan in South Africa at the time of purchase of the shareholding in RSAL. The amount of the loan was S.A Rand 20 million. The rate of interest on the loan is 10% fixed. Interest on the loan to 30 September 2003 has been paid in full.

2. Rates of exchanges between the Kenya Shilling (Ksh.) and the South African Rand (S.A. Rand) at different dates are as follows:

3. Trading by RSAL takes place evenly over the year. When demand is low on the auctions in Holland, domestic demand is high, and this evens out trading conditions.

4. The directors of RKL regard the S.A. Rand denominated loan as a hedge against the investment in RSAL. No capital repayments have been made nor are any foreseen in the grace period to 31 December 2005. The exchange loss on this loan should be accounted for in accordance with IAS 21 – The effects of Changes in Foreign Exchanges Rates.

5. Goodwill on the acquisition of RSAL is treated as an asset of RKL. The fair values of the identifiable assets and liabilities of RSAL on 1 January 2003 approximate book values.

6. The dividend paid by RSAL is deemed to relate to the twelve month period ended 30 September 2003. The directors of RKL state that the foreign exchange difference on the dividend paid of pre-acquisition net income should be deferred in the entirety until the foreign exchange entity is disposed of completely at some future date.

Required:

(a) The consolidated income statement of RKL and RSAL for the year ended 30 September 2003 in accordance with International Financial Reporting Standards (IFRSs).

(b) The consolidated statement of changes in equity for the year ended 30 September 2003 showing columns only for retained earnings and proposed dividends.

(c) The consolidated balance sheet as at 30 September 2003 in accordance with IFRSs, but in the same format as that of RKL.

(d) The effect on the reported profit for the year ended 30 September 2003 and the balance sheet as at 30 September 2003. if the goodwill arising on the acquisition is treated as an asset of the foreign entity.

Note: In all cases, ignore all adjustments relating to deferred tax. Goodwill amortisation should be shown as a separate line item charged in arriving at operating profit. Your answer should be correct to one decimal place.

Date posted:

December 10, 2021

.

Answers (1)

-

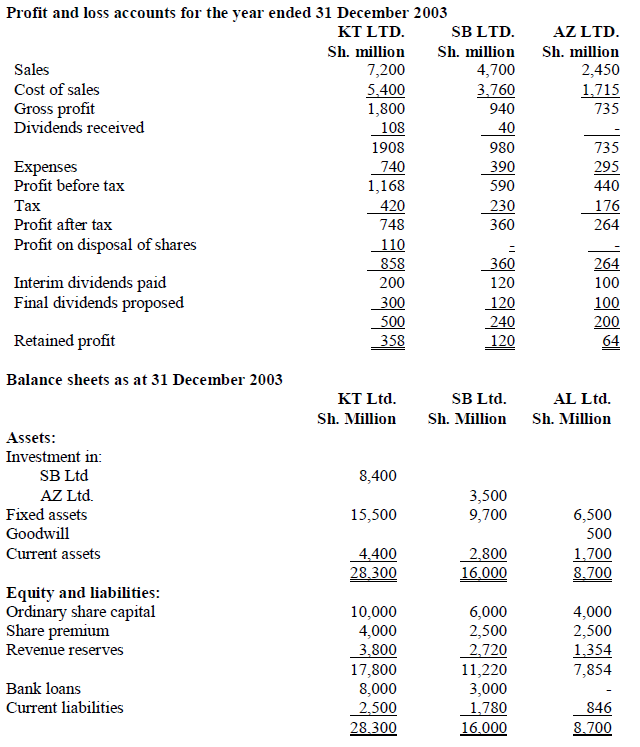

KT Ltd acquired 90% of the ordinary shares of Sh. 10 par value, in SB Ltd. on 1 January 2000 when SB Ltd. had revenue...

(Solved)

KT Ltd acquired 90% of the ordinary shares of Sh. 10 par value, in SB Ltd. on 1 January 2000 when SB Ltd. had revenue reserves of Sh.1, 500 million.

SB Ltd acquired 160 million ordinary shares of Sh.10 par value, in AZ Ltd. on 1 January 2001 when AZ Ltd. had revenue reserves of Sh.500 million.

The financial statements of the three companies for the year ended 31 December 2003 are provided below:

Additional Information:

1) On 31 December 2002, SB Ltd. held stock bought from KT Ltd. for Sh. 120 million and on which KT Ltd. had made a profit of 33% on cost.

2) In the year ended 31 December 2003, KT Ltd. made sales of Sh. 400 million to SB Ltd. at a profit of 20% on selling price. One-quarter of the goods purchased by SB Ltd. from KT Ltd. in the year remained unsold as at 31 December 2003.

3) All the three companies paid the interim dividends on 15 June 2003. No company has accrued its share of proposed dividend from either its subsidiary or associate company.

4) On 30 September 2003. KT Ltd. sold 1200 million ordinary shares held in SB Ltd. for Sh. 2,510 million.

5) Fair values of tangibles assets were not materially different from their book values on the date KT Ltd. acquired its control of SB Ltd. and on the date SB Ltd. acquired its holding in AZ Ltd.

Required:

(a) Consolidated profit and loss account for the year ended 31 December 2003.

(b) Consolidated balance sheet as at 31 December 2003.

Date posted:

December 10, 2021

.

Answers (1)

-

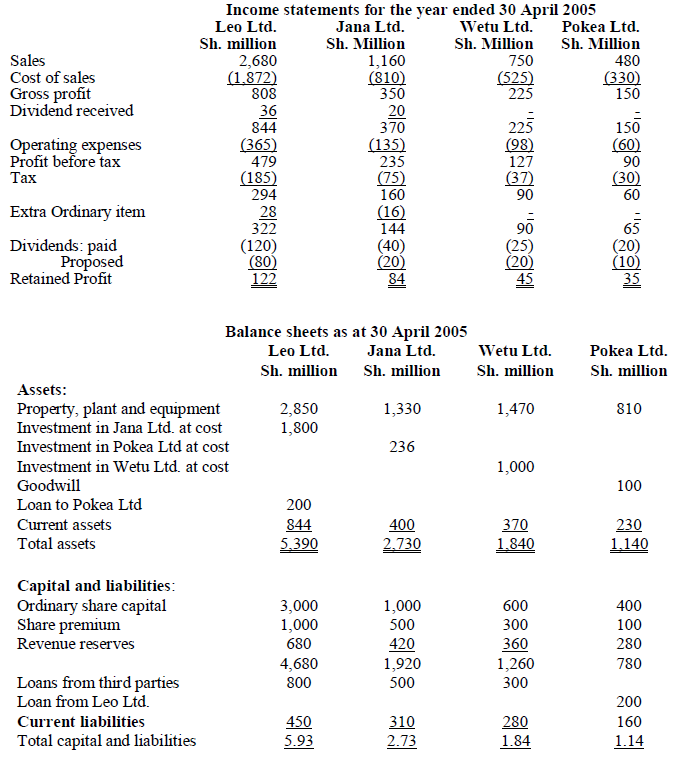

On 1 May 2002, Leo Ltd. acquired 75% of the issued ordinary shares of Jana Ltd. On that date, Jana Ltd. had revenue reserves ofSh.300...

(Solved)

On 1 May 2002, Leo Ltd. acquired 75% of the issued ordinary shares of Jana Ltd. On that date, Jana Ltd. had revenue reserves ofSh.300 million.

On 1 May 2001, Leo Ltd. had acquired 30% of the issued ordinary shares of Poke a Ltd. when the latter had revenue reserves of Sh.I00 million. Leo Ltd. exercises significant influence on Pokea Ltd. and has appointed two directors to the board of Pokea Ltd.

Jana Ltd. acquired 80% of the issued ordinary shares of Wetu Ltd. on 1 November 2000 when the revenue reserves of Wetu Ltd. were Sh.125 million. The revenue reserves balance of Wetu Ltd. on 1 May 2002 was Sh.200 million.

The financial statements of Leo Ltd. and its subsidiary and associate companies for the financial year ended 30 April 2005 are as follows:

Additional information:

1. During the year ended 30 April 2005, Jana Ltd. made sales of Sh.500 million to Leo Ltd. at a profit of 25% on cost.Sh.50 million of these goods were include in the closing stock of Leo Ltd. Included in the opening stock of Leo Ltd., were goods purchased from Jana Ltd. 31,'1 on which Jana Ltd. had made a profit of Sh.6 million. All the intra-group opening stock was disposed of during the period.

2. Leo Ltd. made sales of Sh.90 million to Pokea Ltd. during the year at a profit of 20% on selling price. One third of the goods purchased by Pokea Ltd. from Leo Ltd. in the period was included in the closing stock as at 30 April 2005.

3. As at 1 May 2002, property, plant and equipment owned by Jana Ltd. Were revalued upwards by Sh.200 million. This revaluation has not yet been incorporated in the books. These property, plant and equipment are still owned by the company. Depreciation is provided on the assets at the rate of 10% per .annum on the straight line basis from the date Leo Ltd. acquired its holding in Jana Ltd

4. Leo Ltd purchased the shares in Pokea Ltd. Cum-dividend. The dividends were subsequently paid by Pokea Ltd. In this respect, Leo Ltd. Received Sh.6 million dividends from Pokea Ltd. And credited the amount to its income statement for the year ended 30 April 2002

5. Leo Ltd. does not amortise the goodwill arising on acquisition of subsidiaries but instead determines the impairment of the goodwill occurring in a period which it charges to the group income statement.

The method is applied to premium arising on investment in an associate company.

For the year ended 30 April 2005, impairment of goodwill was determined as follows:

6. Included in the current assets of Leo Ltd. is Sh.80 million due from Jana Ltd. liabilities of Jana Ltd.

7. The companies have not accrued their share of proposed dividends from either their subsidiary or associate companies.

Required:

(a) Group income statement for the year ended 30 April 2005.

(b) Group balance sheet as at 30 April 2005.

The financial statements above should comply with the requirements of:

IFRS 3 - Business Combinations

IAS 28 - Accounting for Investments in Associates

Date posted:

December 10, 2021

.

Answers (1)

-

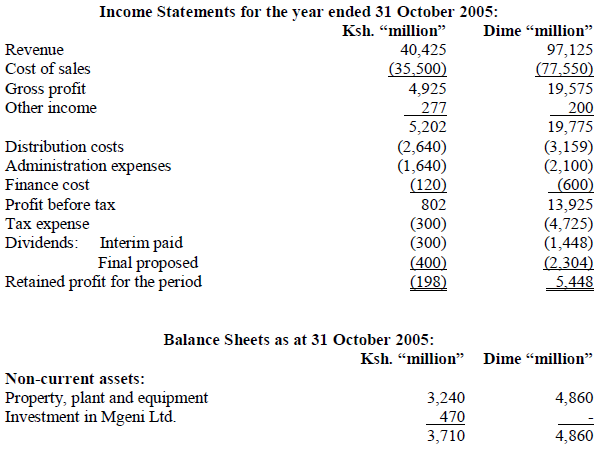

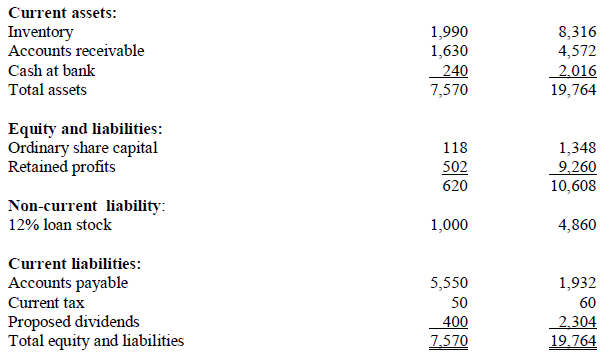

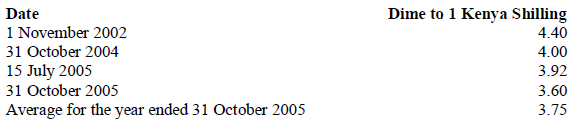

Mzalendo Ltd., a company quoted on the Nairobi Stock Exchange, ahs a foreign subsidiary, Mgeni Ltd., whose reporting currency is the Dime. The reporting currency...

(Solved)

Mzalendo Ltd., a company quoted on the Nairobi Stock Exchange, ahs a foreign subsidiary, Mgeni Ltd., whose reporting currency is the Dime. The reporting currency of Mzalendo Ltd., is the Kenya shilling (Ksh.). The financial statements of the two companies for the year ended 31 October 2005 were as follows:

Additional information:

1. Mzalendo Ltd. Acquired 75% of the ordinary share capital of Mgeni Ltd. On 1 November 2002 when the retained profits of Mgeni Ltd. Were Dime 2,876 million. The goodwill arising on the acquisition of Mgeni Ltd. is considered to be an asset of Mgeni Ltd. No amortisation of goodwill is charged on profits.

2. Other income reported by Mzalendo Ltd., is made up of interim dividend received from Mgeni Ltd., Mgeni Ltd., aid the dividend on 15 July 2005. Other income reported by Mgeni Ltd. is made up of the exchange gain on retranslating the 12% loan stock. The loan stock was obtained form a foreign country.

3. During the year ended 31 October 2005, Mzalendo Ltd., sold goods worth Ksh.900 million to Mgeni Ltd. Mzalendo Ltd. reported a profit of 25% on cost. Half of these goods were still in the inventory of Mgeni Ltd. As at 31 October 2005.

4. The relevant exchange rates at select dates were as follows:

Required:

a) Consolidated income statement for the year ended 31 October 2005 in Kenya Shillings.

b) Consolidated balance sheet as at 31 October 2005 in Kenya Shillings.

(Round the figures to the nearest 1 million where necessary)

Date posted:

December 10, 2021

.

Answers (1)

-

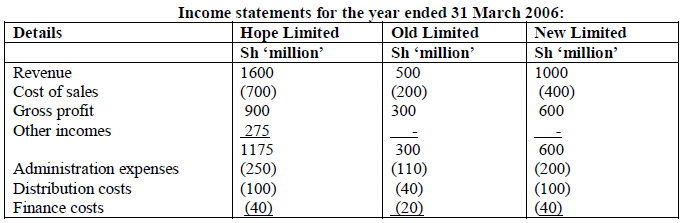

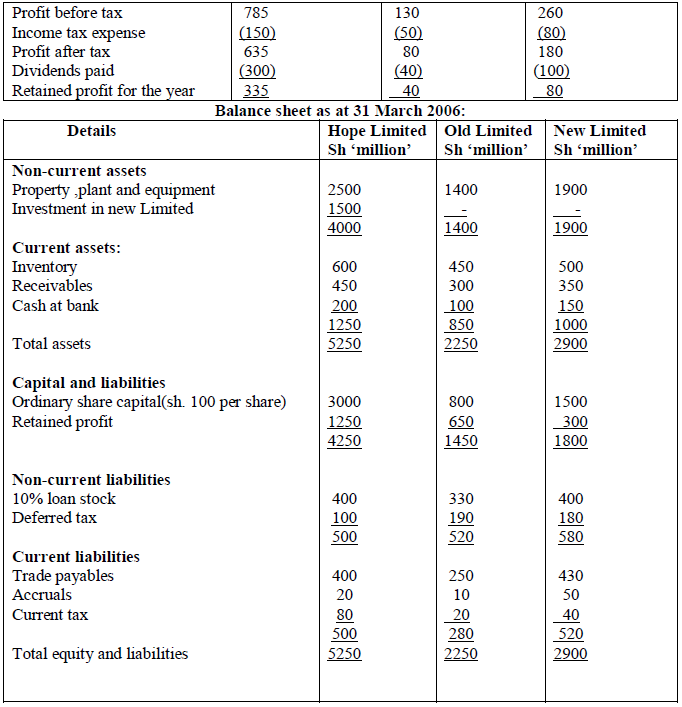

Hope Limited is a company quoted on the stock exchange. On 1 October 2005, the company sold off its entire shareholding of 80% in Old...

(Solved)

Hope Limited is a company quoted on the stock exchange. On 1 October 2005, the company sold off its entire shareholding of 80% in Old Limited and acquired 75% holding in New Limited. The following statements relate to the three companies:

Additional information

1. Hope Limited had acquired its investment in Old Limited on 1 April 2003 for shs. 900 million when the retained profits of Old limited amounted to sh. 300 million. By 31 March 2005, half of the goodwill on the acquisition of Old Limited had been impaired.

2. Hope Limited also acquired sh. 100 million of the 10% loan stock in New Limited on 1 October 2005.

3. During the year ended 31st March 2006, Hope Limited sold goods worth sh. 50 million to Old Limited before Old limited was disposed of.

In addition, Hope Limited sold goods worth sh.200 million to New Limited in the period after New Limited’s acquisition. Hope Limited reported a profit margin of 40% on all the inter company sales. Half of these goods were still held by by the subsidiaries by 31 March 2006.

4. The other incomes appearing in the income statement of Hope Limited are made up of profit on sale of Old Limited and dividends received from New Limited. All the companies paid their dividends on 31 December 2005. However, New Limited had not paid interest on loan stock. This unpaid interest was included as part of the accruals.

5. As at 31 March 2006, inter-company balances were as follows:

6. The fair values of all the net assets in the subsidiaries were the same as the book values on the dates of acquisitions except for an item of plant in the books of New Limited whose fair value was shs.10 million above the book value on 1 October 2005. The group depreciates plant at 20% per annum using the straight-line method.

7. No goodwill in either subsidiary company was impaired during the year ended 31 March 2006.

Required:

a) Consolidated income statement for the year ended 31 March 2006.

b) Consolidated statement of changes in equity (showing only the retained profits column)

c) Consolidated balance sheet as at 31 March 2006.

Date posted:

December 10, 2021

.

Answers (1)

-

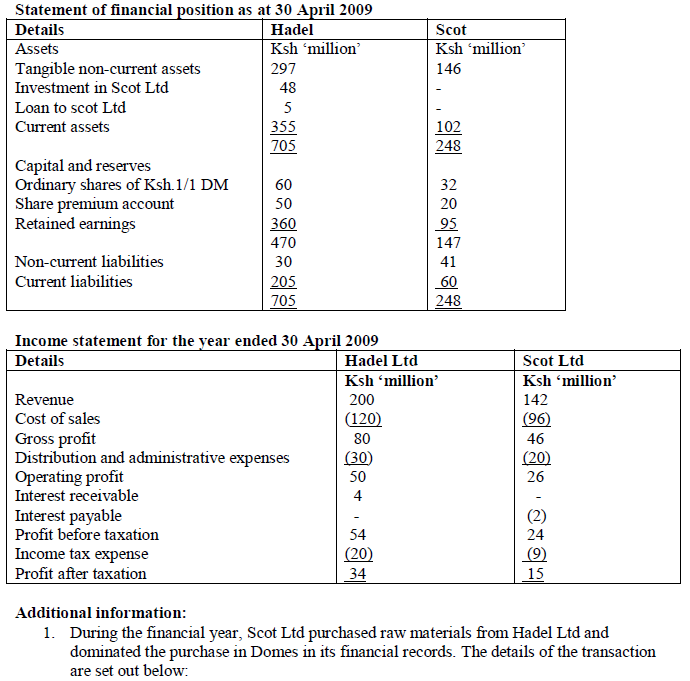

Hadel Ltd., a public limited company incorporated in Kenya owns 75% of the ordinary share capital of Scot Ltd.., a public limited company incorporated in...

(Solved)

Hadel Ltd., a public limited company incorporated in Kenya owns 75% of the ordinary share capital of Scot Ltd.., a public limited company incorporated in a foreign country. The reporting currency of Scot Ltd is the domes (DM) whereas that of Hadel Ltd is the Kenya shilling (Ksh). Hadel Ltd acquired its shareholding in Scot on 1 May 2008 at 120 million domes (DM) when the retained profits of Scot Ltd were 80 million domes (DM). Scot Ltd has not revalued its assets or issued any share capital since 1 May 2008.

The following are financial statements of Hadel Ltd and Scot Ltd.

Required:

Consolidated income statement for the year ended 30 April 2009.

Date posted:

December 10, 2021

.

Answers (1)

-

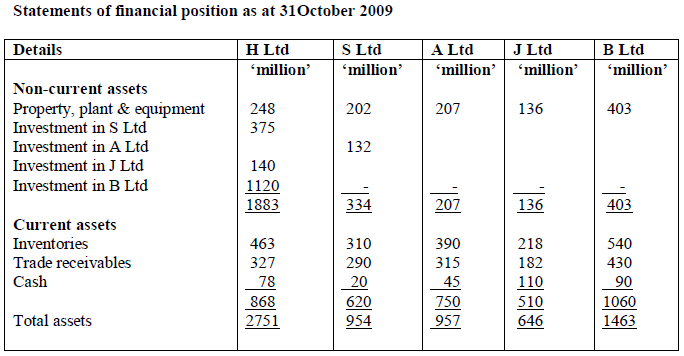

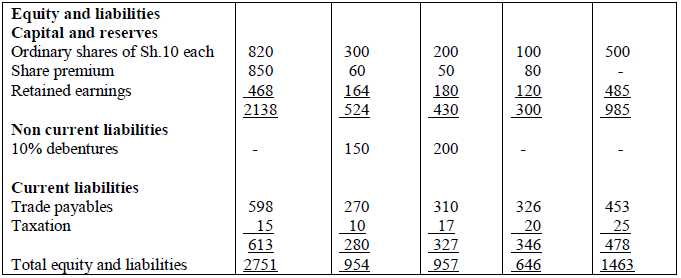

The statements of financial position of H Ltd, S Ltd, A Ltd, J Ltd and B Ltd as at 31 October 2009 are as follows:

(Solved)

The statements of financial position of H Ltd, S Ltd, A Ltd, J Ltd and B Ltd as at 31 October 2009 are as follows:

Additional information:

1. H Ltd purchased 75% of the ordinary shares of S Ltd on 1 November 2007, when the balance of the earnings of S Ltd was sh. 80 million.

2. S Ltd purchased 30% of the ordinary shares of A Ltd on 1 November 2007 were sh. 140 million.

3. H Ltd and another company, Ukwala Ltd, each bought 50% of the share capital of J Ltd on 1 May 2009. H Ltd and Ukwala Ltd have a joint control of J Ltd. Both companies are to account for their Joint venture using proportionate consolidation; combining items on a line by line basis. J Ltd’s retained earnings on 1 May 2009 were sh. 110 million.

4. On 1 May 2009, H Ltd acquired 45 million ordinary shares of shs. 10 each in B Ltd when the retained earnings of B Ltd were sh.400 million.

5. On 1 May 2009, the fair values of the identifiable net assets of B Ltd, approximated book value except for leasehold whose book value was sh. 40 million below its fair value. The property is depreciated to nil residual value over the term of the lease. On 1 May 2009, there were 10 years remaining of the lease.

6. On 1 November 2007, the book value of the identifiable net assets of A Ltd was sh. 20 million below their fair value. The assets revalued are not to be depreciated.

7. Included in the closing inventory of H Ltd is shs. 12 million worth of goods purchased from J Ltd which cost sh. 8 million.

8. In the year ended 31 October 2009, H Ltd sold goods to B Ltd at a price of sh. 15 million. H Ltd had marked up these goods by 50% on cost. B Ltd held 50% of these goods in its closing inventory on 31 October 2009.

9. As at 31 October 2009, H Ltd owed J Ltd sh. 12 million. As at the same date, S Ltd owed H Ltd sh. 13 million and A Ltd Sh 20 million. All the current accounts between the companies were in agreement.

10. As at 31 October 2009, it was estimated that since the date of acquisition, goodwill had suffered impairment loss by the following percentages:

S Ltd = 40%

B Ltd = 25%

The goodwill of J Ltd and the premium on acquisition of A Ltd had not been impaired since the date of acquisition.

11. It is groups’ policy to value the non-controlling interest at fair value or the market value. The fair value of the non-controlling interest in S Ltd at the date of acquisition was Sh. 120 million, while the fair value of the non-controlling interest in B Ltd, at the date of acquisition was shs. 124 million.

Required:

Consolidated statement of financial position as at 31 October 2009, J Ltd should be accounted for using the proportionate consolidation method as per IAS 31(Interest in Joint ventures)

Date posted:

December 10, 2021

.

Answers (1)

-

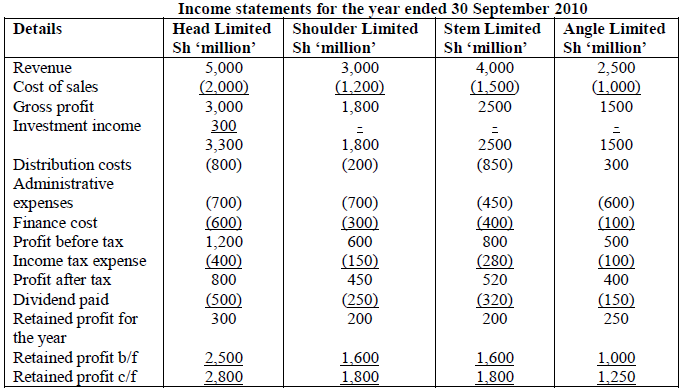

Head Limited sold off its entire shareholding of 80% in Shoulder Limited and acquired 75% of the shares of Stem Limited during the year ended...

(Solved)

Head Limited sold off its entire shareholding of 80% in Shoulder Limited and acquired 75% of the shares of Stem Limited during the year ended 30 September 2010. Head Limited also acquired 40% of the shares of Angle Limited.

The following income statements relate to the four companies:

Additional information:

1. Head Limited had acquired it s shareholding in Shoulder Limited at a cost of Sh 2200 million on 1 October 2007 when the retained earnings of Shoulder Limited were Sh.500 million. The ordinary share capital of Shoulder Limited was Sh. 2,000 million and there were no other reserves. The fair value of the non-controlling interest in Shoulder Limited on the same date was Sh.550 million.

2. During the year ended 30 September 2010, Head Limited acquired the investment in Stem Limited and Angle Limited. The details of the acquisitions are as follows:

On the date of its acquisition, Stem Limited had an item of plant that was Sh.270 million below its fair value. Plant is depreciated at 20% per annum with a full year’s charge in the year of purchase or revaluation.

3. On 1 July 2010, Head Limited sold its investment in Shoulder Limited at a price of Sh.3,430 million. This disposal has not been reflected in the income statement of Head Limited.

4. During the year, the companies traded as follows:

5. Goodwill of Shoulder Limited had been impaired by half as at 1 October 2009. Any goodwill arising in Stem Limited and Angle Limited is impaired by 20%.

6. All dividends were paid on 31 August 2010.

Required:

a) The group income statement for the year ended 30 September 2010.

b) The statement of changes in equity showing only the retained profits column.

Date posted:

December 10, 2021

.

Answers (1)

-

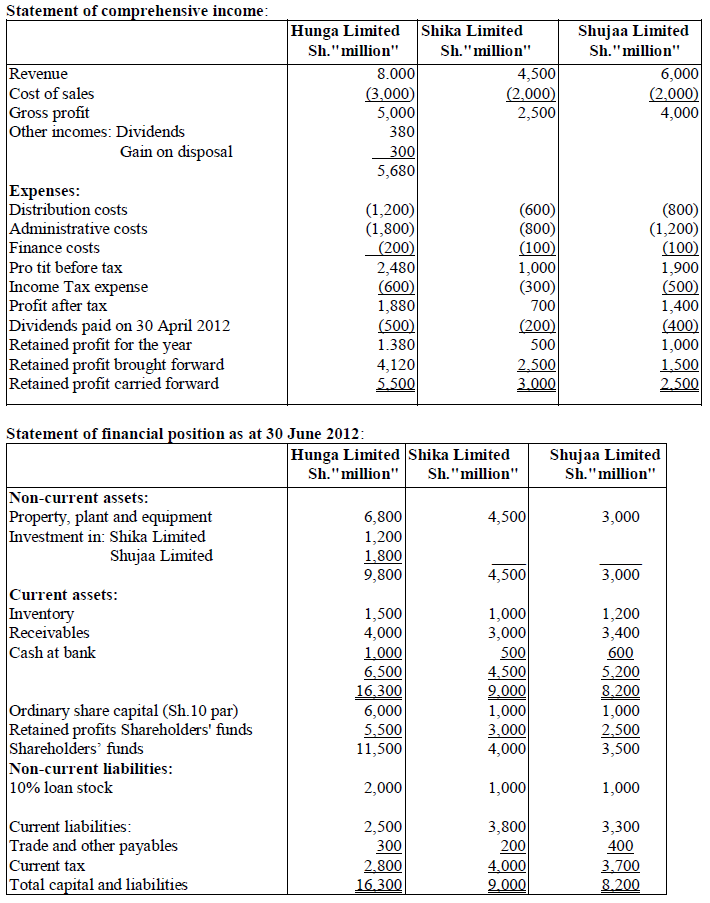

Hunga Limited, a company quoted on the securities exchange, acquired 80% of Shika Limited several years ago. On 1 January 2012 Hunga limited sold half...

(Solved)

Hunga Limited, a company quoted on the securities exchange, acquired 80% of Shika Limited several years ago. On 1 January 2012 Hunga limited sold half of its investment in Shika Limited and acquired 75% of the equity shares of Shujaa Limited.

The financial statements for the year ended 30 June 2012 for the three companies are as given below.

Additional information:

1. Hunga Limited had acquired its shareholding in Shika Limited for Sh.2,400 million when the retained profits of Shika Limited amounted to Sh. 1,500 million. There was no fair value adjustment at the time of this acquisition.

2. Hunga Limited sold half of the investment in Shika Limited for Sh.1.500 million. This disposal has already been accounted for by Hunga Limited but not by the group. The fair value of the remaining investment in Shika Limited was Sh.1, 300 million on the date of disposal.

3. Between 1 January 2012 and 30 June 2012. Hunga Limited sold to Shujaa Limited goods worth Sh.500 million reporting, a profit of Sh. 100 million. Half of the goods were still in the inventory of Shujaa Limited as at 30 June 2012.

4. Intercompany receivables and payables were as follows as at 30 June 2012:

5. As at 1 July 2011, half of the goodwill of Shika Limited had been impaired. The goodwills of the companies were not impaired in the current year to 30 June 2012. The group uses the partial goodwill method when preparing the consolidated financial statements.

Required;-

a) Group statement of comprehensive income for the year ended 30 June 2012.

b) Group statement of financial position as at 30 June 2012.

Date posted:

December 10, 2021

.

Answers (1)

-

Describe four shortcomings of cost accounting.

(Solved)

Describe four shortcomings of cost accounting.

Date posted:

February 15, 2019

.

Answers (1)