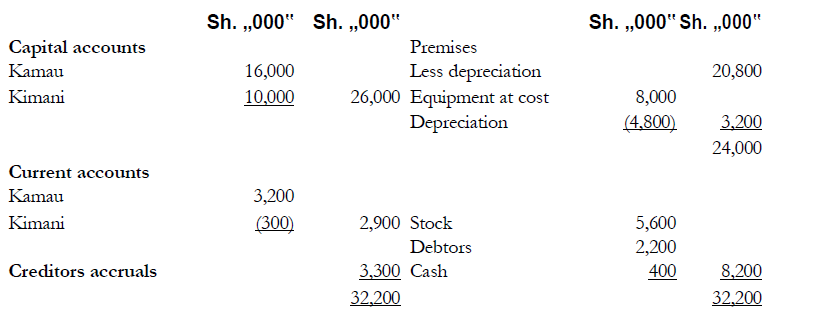

Kamau and Kimani are partners sharing profits and losses in the ratio 3:2 respectively. The

partnership agreement provides for Kimani to receive a salary of Sh.4,000,000...

(Solved)

Kamau and Kimani are partners sharing profits and losses in the ratio 3:2 respectively. The

partnership agreement provides for Kimani to receive a salary of Sh.4,000,000 per annum, and

interest on capitals for both partners at 5% per annum. The partnership balance sheet as at 31

December 1998 was as follows:

On I April 1999 Kimata was admitted to the partnership. He had been a salaried employee,

earning Sh.8, 000,000 per annum. The terms of his admission to the partnership were as

follows:

1. Kimata should introduce Sh. 12,000,000 in cash as capital into the business.

2. Goodwill should be valued at Sh.14, 000,000 for the purpose of his admission. It was

agreed that goodwill should not be included in the balance sheet of the new partnership.

3. Kimata should receive a salary as a partner of Sh.6 , 000,000 per annum.

Kimani's salary should be raised to Sh.6, 000,000.

4. Interest on capital should be raised from 5% to 6% per annum and calculated on the

capital accounts after the elimination of goodwill.

5. The new profit sharing ratio for Kamau, Kimani and Kimata should be 4:2:1

respectively.

In preparing the draft financial statements for the year ended 31 December 1999, the

partnership accountant, Otieno, calculated that the partnerships profit for the year was Sh.55,

155,000, and that the working capital of the business as at 31 December 1999 was:

Profit is assumed to accrue evenly during the year.

Partners cash drawings for the year were Kamau Sh.23,705,000, Kimani Sh.19,525,000 and

Kimata Sh.8,250,000.

Required:

(a) The profit and loss appropriation account for the year ended 3 1 December 1999.

(b) The current and capital accounts of the partners for the year ended 31 December

1999.

(c) Balance Sheet as at 31 December 1999.

Date posted:

November 16, 2018

.

Answers (1)

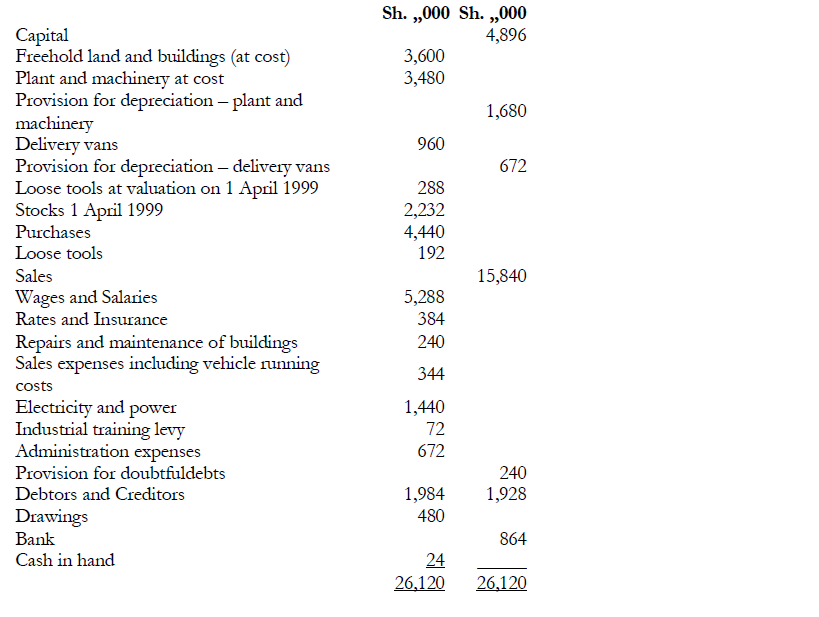

Mr. Ancentus Okwengo is the sole proprietor of a small business. The following trial balance

was extracted from his books at 31 March 2000.

(Solved)

Mr. Ancentus Okwengo is the sole proprietor of a small business. The following trial balance

was extracted from his books at 31 March 2000.

Additional information:

1. Closing stock on 3 1 March

2000 was Sh.2, 008,000.

Loose tools at valuation

Sh.384, 000.

2 .Provision is to be made for the following amount

owing on 3 1 March 2000: Electricity and power

Sh.192,000.

3. Payments in advance on 31 March

2000 were as follows: Van licenses

Sh.2,520 and rates Sh.13,800.

4. Depreciation on plant and machinery and delivery vans is to be provided at the rate of

20% and 25% respectively on cost at the end of the year.

5. Bad debts amounting to Sh.26,000 are to be written off and the provision for

doubtful debts is to be 10% of trade debtors.

Required:

A ten-column worksheet for the year ended 31 March 2000.

Date posted:

November 16, 2018

.

Answers (1)

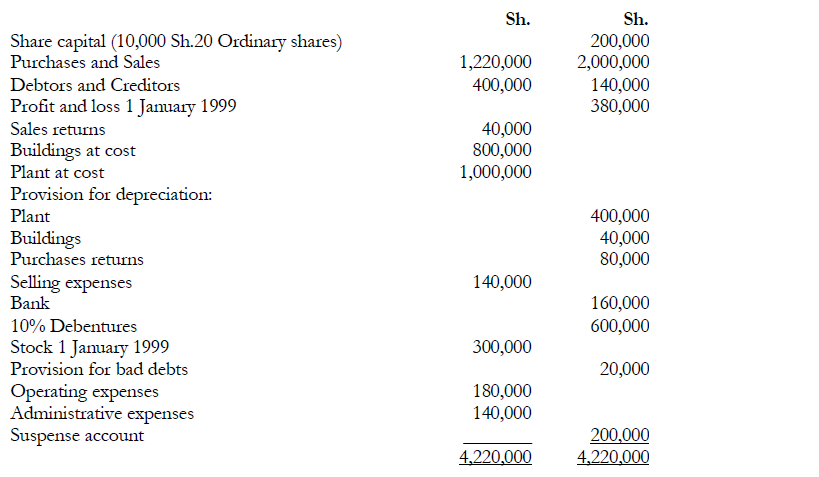

The trial balance of Zach Ltd. as at 31 December 1999 was as follows:

(Solved)

The trial balance of Zach Ltd. as at 31 December 1999 was as follows:

Additional information:

1. Stock at 31 December 1999 was Sh.360,000.

2. Sales returns of Sh.20,000 have been entered in the sales day book as if they were sales.

When this error was discovered, the debtors account had been corrected but the sales figure

was not rectified.

3. 5000 new shares were issued during the year at Sh.32. The proceeds have been credited to

the suspense account.

4. A fully depreciated plant which cost Sh.200,000 was sold during the year. No other entries except

bank have been made. The remaining balance on the suspense account after (2 and 3) above

represents the sale proceeds.

5. A debtor of Sh.20,000 has been declared bankrupt. A general provision is required at 5% of

debtors.

6. Rates of Sh.30,000 paid in December covering half year to 31 March 2000 have not been

entered in the books.

7. Debenture interest has not been paid.

8. Depreciation on plant is at 10% on cost and buildings at 2% on cost.

9. The directors propose to pay a dividend of Sh.2 per share and transfer Sh.20,000 to the

general reserve.

10. Corporation tax at a rate of 32'/2% on profits is estimated to be Sh.90,000.

Required:

(a)Suspense account for the year ended 3I December 1999

(b)Trading,profit and loss account for the year ended 31 December 1999.

(c) Balance sheet as at 31 December 1999.

Date posted:

November 15, 2018

.

Answers (1)

a) Internal control systems are designed, amongst other things, to prevent error and...

(Solved)

a) Internal control systems are designed, amongst other things, to prevent error and misappropriation.

Required:

Describe the errors and misappropriations that may occur if the following are not properly controlled: (i) Receipts paid into bank accounts;

ii)Payments made out of bank accounts; (iii) Interest and charges debited and credited to bank accounts.

(b) A book-selling company has a head office and 25 shops, each of which holds cash (banknotes, coins, and credit card vouchers) at the balance sheet date. There are no receivables. Accounting records are held at shops. Shops make returns to head office and head office holds its own accounting records. Your firm has been the external auditor to the company for many years and has offices near to the location of some but not all of the shops.

Required:

List the audit objectives for the audit of cash and state how you would gain the audit evidence in relation to those objectives at the year-end.

c) The external auditors of companies often write to companies’ bankers asking for details of bank balances and other matters at the year-end.

Required:

Explain why auditors write to companies’ bankers and list the matters you would expect banks to confirm.

Date posted:

May 11, 2018

.

Answers (1)