-

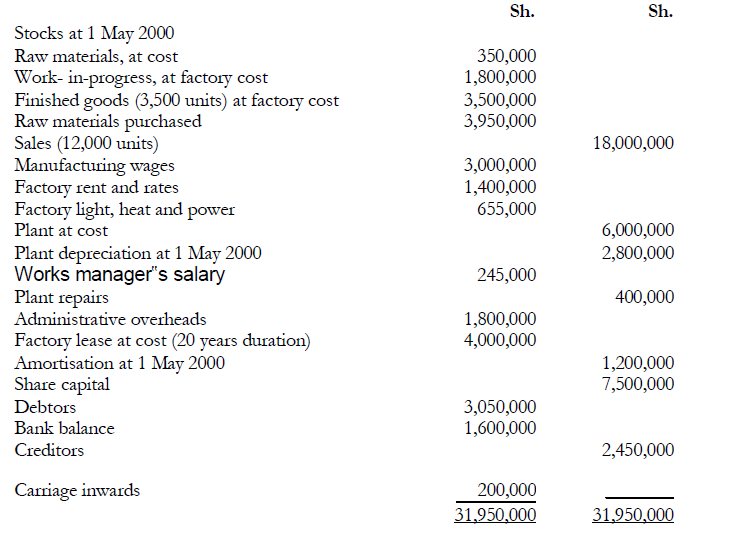

Kaluwax Ltd. manufactures one product which it sells to the wholesale trade. The following trial

balance was extracted from the books of the company at 30...

(Solved)

Kaluwax Ltd. manufactures one product which it sells to the wholesale trade. The following trial

balance was extracted from the books of the company at 30 April 2001:

The following additional information is available:

1. Plant depreciation is to be provided at 10% on the cost of plant owned at the year end.

2. Raw materials costing Sh.500,000 were in stock on 30 April 2001.

3. Finished goods are transferred to the warehouse as soon as they are completed. During the

year, 10,000 units were completed and transferred to the warehouse. Work-in-progress at

the end of the financial year (at factory cost) amounted to Sh.2,300,000.

4. There was no wastage or pilferage during the current year.

Required:

a) Manufacturing, trading and profit and loss account for the year ended 30 April 2001.

(12 marks)

b) Assume the facts as in (a) above, except that it had always been the company‟s

practice to transfer completed units from the factory to the warehouse at cost plus 25% and to

value stocks of finished goods at the transfer price for the trading account but at factory cost

for balance sheet purposes. Show how the manufacturing, trading and profit and loss account

for the year ended 30 April 2001 would appear.

Date posted:

November 16, 2018

.

Answers (1)

-

Kimeu commenced his business of making furniture on 1 April 2000. Due to his limited

accounting knowledge he has not maintained proper books of account. You...

(Solved)

Kimeu commenced his business of making furniture on 1 April 2000. Due to his limited

accounting knowledge he has not maintained proper books of account. You have been engaged

to examine his records and prepare appropriate accounts therefrom. You perform an

examination of the records and from interviews with Kimeu, you ascertain the following

information:

1. At the commencement of business on 1 April 2000, he deposited Sh.1,200,000 into a

business bank account. On the same day he brought into the firm his pickup and estimated

that it was worth Sh.660,000 then and that from 1 April 2000 it will have useful life of three

years.

2. To increase his working capital he borrowed Sh.400,000 at 15% interest per annum on 1

July 2000 from his sister but no interest has yet been paid.

3. On 1 April 2000, Sally was employed as a clerk at a salary of Sh.720,000 per annum.

4. He had drawn Sh.18,000 per week from the business account for private use during the

year.

5. He purchased timber worth Sh.1,960,000 out of which Sh.158,000 worth of stock was

retained in the workshop on 31 March 2001. He also spent Sh.960,000 on the purchase of

some equipment at the commencement of the business which he estimates will last him five

years.

6. Electricity bills received up to 31 January 2001 were Sh.240,000. Bills for the remaining two

months were estimated to be Sh.48,000. Motor vehicle expenses were Sh.182,000 while

general expenses amounted to Sh.270,000 for the year. Insurance premium for the year to

30 June 2001 was Sh.160,000. All these expenses have been paid by cheque.

7. Rates for the year to June 2001 were Sh.36,000 but these had not been paid.

8. Sally sent out invoices to customers for Sh.6,178,000 but only Sh.5,080,000had been

received by 31 March 2001. Debts totalling to Sh.17,000 were abandoned during the year as

bad. Other customers for jobs too small to invoice have paid Sh.726,000 in cash for work

done of which Sh.560,000 was banked . Kimeu used Sh.75,000 of the difference to pay for

his family‟s food stuff bought Kenya Charity Sweepstake tickets worth

Sh.24,000 and Sally used the rest on general expenses except for Sh.30,100 which was left

over in the drawer in the office on 31 March 2001.

9. You agree with Kimeu that he will pay you Sh.55,000 for accountancy fee.

Required:

a) Profit and loss account for the year ended 31 March 2001.

b) Balance sheet as at 31 March 2001.

Date posted:

November 16, 2018

.

Answers (1)

-

The Wide Trading Company Limited has an authorised capital of Sh.500,000 divided into

5,000 ordinary shares of Sh.100 each.

On 1 January 2001, the Board of directors...

(Solved)

The Wide Trading Company Limited has an authorised capital of Sh.500,000 divided into

5,000 ordinary shares of Sh.100 each.

On 1 January 2001, the Board of directors decided to issue 4,000 shares at Sh.125 each

payable as Sh.50 on application. Sh.50 on allotment (including the Sh.25 premium) and

Sh.25 on first and final call. The applications were receivable on 20 January 2001 when

allotment was made. The allotment money was receivable by 15 February 2001. The first

and final call was made on 15 March 2001 and the call money receivable by 31 March 2001.

Applications were received for 6,000 shares. The directors decided to refund money for

1,000 shares and the other applicants were allotted prorata with the excess money utilised to

meet part of the allotment money. The balance of the allotment money was received on the

due date. The first and final call was made and the call money received on the due date

except for allotees of 200 shares.

The 200 shares with calls arrears were forfeited on 10 April 2001 and sold for cash at Sh.85

eacg ib 12 April 2001.

Note: No other transactions took place during the above period.

Required:

i) Application and Allotment Account, First and Final Call Account, Ordinary Share

Capital Account. Share Premium Account, Calls in Arrears Account. Forfeited Shares

Account and the bank account.

ii) Balance sheet as at 12 April 2001

Date posted:

November 16, 2018

.

Answers (1)

-

Explain the following terms: (i) Share premium (ii) Rights issue

(Solved)

Explain the following terms: (i) Share premium (ii) Rights issue

Date posted:

November 16, 2018

.

Answers (1)

-

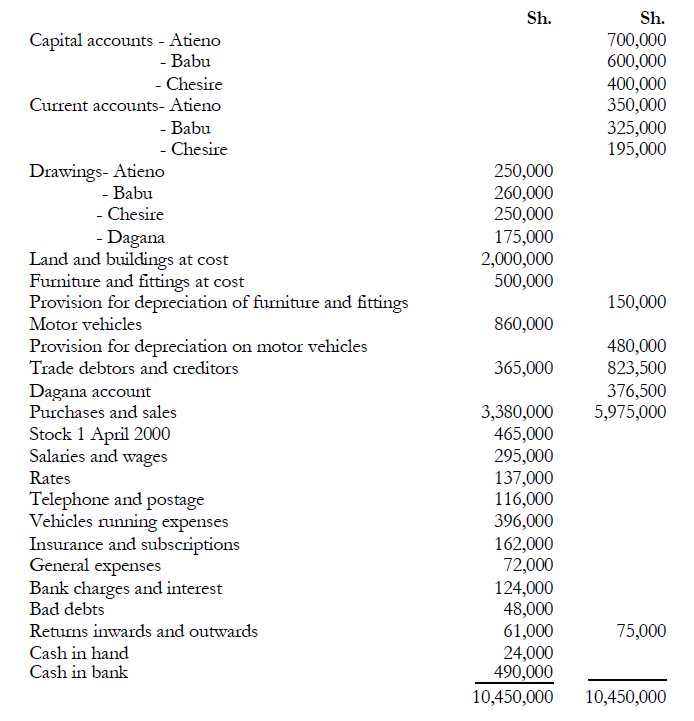

Atieno, Babu and Chesire have been trading in partnership sharing profits/losses in the ration of

5:3:2 respectively. On 1 April 2000 they admitted their manager, Dagana...

(Solved)

Atieno, Babu and Chesire have been trading in partnership sharing profits/losses in the ration of

5:3:2 respectively. On 1 April 2000 they admitted their manager, Dagana as a partner and the

profit sharing ratio was changed to 4:3:2:1 FOR Atieno, Babu, Chesire and Dagana respectively.

The partners valued the goodwill at Sh.510,000. Dagana paid Sh.200,000 as capital and his share

of goodwill, which should be based on capital contributions.

The partners do not wish to retain the goodwill account after admission of Dagana. The

admission of Dagana has not been fully recorded other than the cash receipt of Sh.376,500.

The following is the trial balance of the partnership as at 31 March 2001:

Notes:

1) Depreciation on furniture and fittings and motor vehicles is at 10% and 20% on reducing

balance respectively.

2) The closing stocks were valued at Sh.560,000.

3) Accrued salaries and wages and telephone bills amounted to Sh.24,000 and Sh.14,000

repectively.

4) Prepaid subscriptions and rates amounted to Sh.5,000 and Sh.25,000 respectively.

5) The partners decided that Dagana should be given a monthly salary of Sh.20,000 for the

whole year from 1 April 2000 to 31 March 2001.

6) Dagana took goods for own use at cost amounting to Sh.185,000. No entry has been made

in the books.

7) The old partners shared the cash paid by Dagana for part of his goodwill.

Required:

a) Trading, profit and loss account for the year ended 31 March 2001. (10 marks)

b) Partners capital accounts.

c) Partners current accounts.

d) Balance sheet as at 31 March 2001.

Date posted:

November 16, 2018

.

Answers (1)

-

Explain giving examples the distinguishing features of liabilities, provisions and reserves

(Solved)

Explain giving examples the distinguishing features of liabilities, provisions and reserves.

Date posted:

November 16, 2018

.

Answers (1)

-

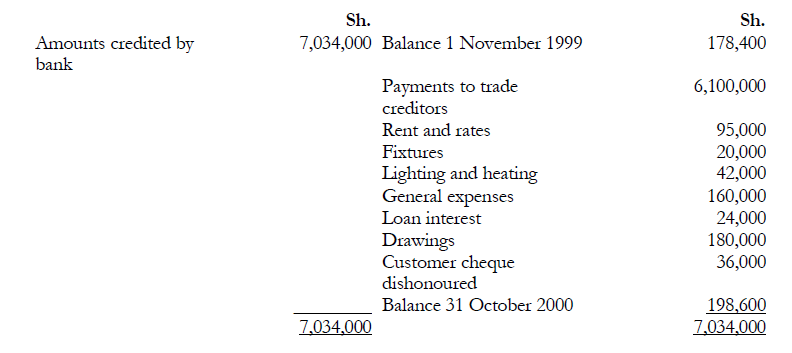

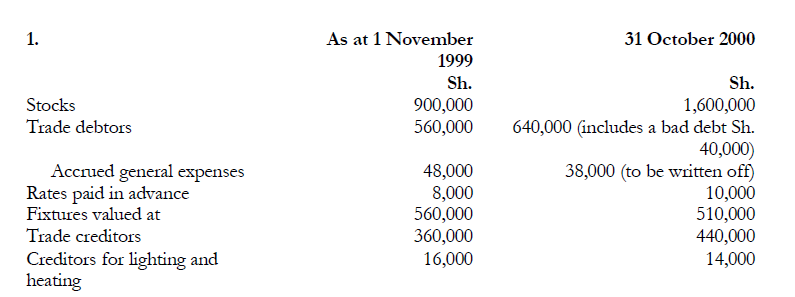

Nzioka is a grocer who had not kept complete books of account. The following was a summary of his bank statements for the ear ended...

(Solved)

Nzioka is a grocer who had not kept complete books of account. The following was a summary of his bank statements for the ear ended 31 October 2000:

The following information is also available

1. Trading receipts consists partly of cash and party of cheques. During the year. Nzioka had

paid out of his cash takings wages amounting to Sh.590.000 and sundry expenditure of Sh

28.000. He retained Sh.600 a week (assume 52 ~weeks in a year) pocket money and

maintained a balance of Sh.4.000 in the till tot-change. The balance of his takings. together

with cheques amounting to Sh.50,000 which he had cashed out of his takings was paid into

the bank.

2. Cheque drawn payable to trade creditors. But not presented at I November 1999

amounted to Sh56000 and at 3I October 2000 Sh.64.000.

3. All dishonoured cheques were re-presented and honoured during the year.

4. The loan interest was paid to the lender who had lent Nzioka Sh.800.000 some years ago

at a rate of 3°o p.a. The interest was duly paid half-yearly on 31 January and 31 July and

the loan was still outstanding at the close of the year.

5. Discounts allowed by trade creditors amounted to Sh.96.000 and those allowed to debtors

were Sh. 104.000.

Required:

(a) A statement of Nzioka's capital on 1 November 1999.

(b) Profit and loss account for the year ended 31 October 2000 and a balance sheet at

that date.

Date posted:

November 16, 2018

.

Answers (1)

-

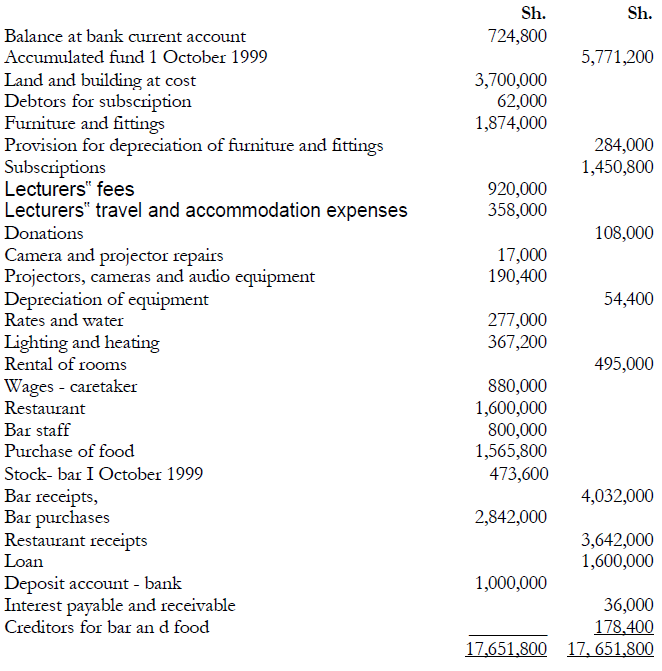

The following trial balance was extracted from the books of Literary and, Philosophical Society

as at 30 September 2000

(Solved)

The following trial balance was extracted from the books of Literary and, Philosophical Society

as at 30 September 2000:

Additional information:

1: The bar stock was valued at Sh.642.800 as at 30 September 2000.

2. It is expected that of the debtors for subscriptions, Sh.43.600 will not be collectable.

3. The interest account is net. The loan is at a concessional rate of 4% while I0% has been

earned on the deposit account. No changes have taken place all year in the principal sums

involved.

4. An invoice for Sh.43.000 of wine had been omitted from the records at the close of the year

although the wine had been included in the bar stock valuation.

5.Depreciation for the rear is to be provided as follows: Furniture and fittings Sh. 194.000

Projectors. Cameras etc. Sh. 19.000

Required:

(a) Bar and restaurant trading account for the year ended 30 September 2000.

(b) An income and expenditure account for the year ended 30 September 2000.

(c) A balance sheet as at 30 September 2000.

Date posted:

November 16, 2018

.

Answers (1)

-

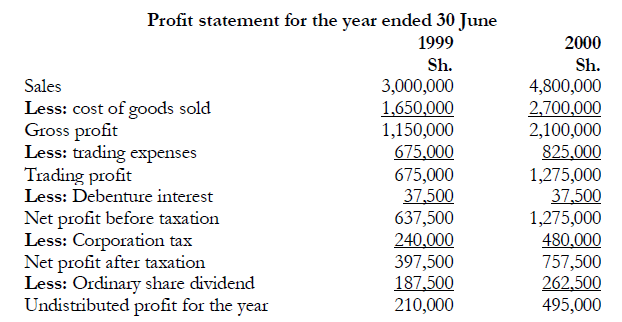

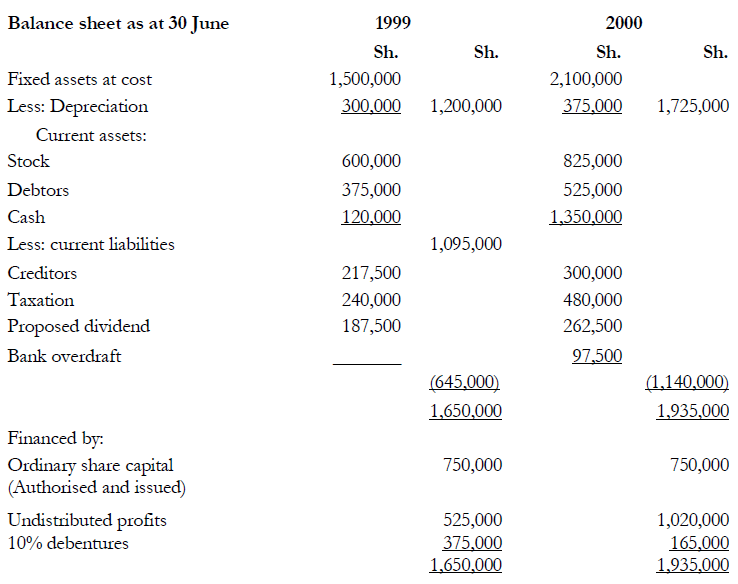

Munyah Ltd. is an expanding company and the following accounts relate to its operations for the years 1999 and 2000:

(Solved)

Munyah Ltd. is an expanding company and the following accounts relate to its operations for the years 1999 and 2000:

Required:

(i) Compute six accounting ratios for both 1999 and 200(1 which you feel would be of

particular value in assessing the Profitability and Liquidity of Munyah Ltd.

(ii) Comment on the current position of the company with the aid of the accounting ratios

computed in (i) above and any other information that you consider to be relevant.

Date posted:

November 16, 2018

.

Answers (1)

-

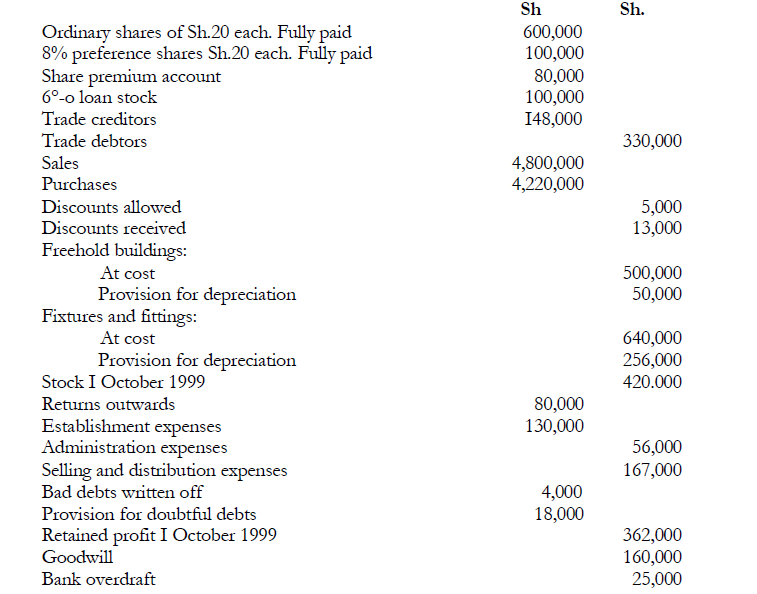

The following balances were extracted from the books of Wamu Traders Ltd.as at 30 September 2000

(Solved)

The following balances were extracted from the books of Wamu Traders Ltd.as at 30 September 2000:

The following additional information is available:

1. Depreciation is provided annually on the cost of fixed assets held at the end of the

financial year at the following rate:

Freehold buildings 20%

Fixtures and fittings 10%

2. The trade debtors balance includes Sh. 10,000 due from Musa who has now been declared

bankrupt. In the circumstances, it has been decided to write the debt off as a bad debt.

3. The provision for doubtful debts as at 30 September 2000 is to be 5°,% of trade debtors

4. Establishment expenses prepaid at 30 September 2000 amounted to Sh.4,000.

5. Administration expenses accrued at 30 September 2000 amounted to Sh.7.000.

6. The company paid the interest on the loan stock for the year, ended 30 September 2000 on 30

October 2000.

7. Closing stock was valued at Sh.560,000.

8. The company's directors propose that the preference share dividend be paid and a

dividend of 10% the ordinary shares he paid.

Required:

(i) Trading and profit and loss account and appropriation account for the sear ended 30

September 2000 of Wamu Traders Ltd.

(ii) Balance sheet as at 30 September 2000.

Date posted:

November 16, 2018

.

Answers (1)

-

Briefly state the reasons why a company would not wish to distribute all its profits to its

shareholders

(Solved)

Briefly state the reasons why a company would not wish to distribute all its profits to its

shareholders.

Date posted:

November 16, 2018

.

Answers (1)

-

Two accounting concepts or conventions could clash or there could be

inconsistency between them.

Give two examples of such situations and explain how the inconsistency should be

resolved.

(Solved)

Two accounting concepts or conventions could clash or there could be inconsistency between them.

Give two examples of such situations and explain how the inconsistency should be

resolved.

Date posted:

November 16, 2018

.

Answers (1)

-

Define the following accounting concepts and for each explain their implication in the preparation of financial Statements.

(i) The Going concern concept.

(ii) Business entity concept.

(iii) Materiality.

(iv)...

(Solved)

Define the following accounting concepts and for each explain their implication in the preparation of financial Statements.

(i) The Going concern concept.

(ii) Business entity concept.

(iii) Materiality.

(iv) Realisation.

Date posted:

November 16, 2018

.

Answers (1)

-

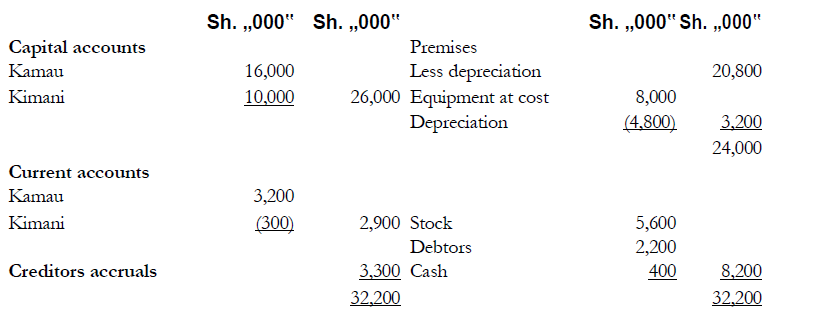

Kamau and Kimani are partners sharing profits and losses in the ratio 3:2 respectively. The

partnership agreement provides for Kimani to receive a salary of Sh.4,000,000...

(Solved)

Kamau and Kimani are partners sharing profits and losses in the ratio 3:2 respectively. The

partnership agreement provides for Kimani to receive a salary of Sh.4,000,000 per annum, and

interest on capitals for both partners at 5% per annum. The partnership balance sheet as at 31

December 1998 was as follows:

On I April 1999 Kimata was admitted to the partnership. He had been a salaried employee,

earning Sh.8, 000,000 per annum. The terms of his admission to the partnership were as

follows:

1. Kimata should introduce Sh. 12,000,000 in cash as capital into the business.

2. Goodwill should be valued at Sh.14, 000,000 for the purpose of his admission. It was

agreed that goodwill should not be included in the balance sheet of the new partnership.

3. Kimata should receive a salary as a partner of Sh.6 , 000,000 per annum.

Kimani's salary should be raised to Sh.6, 000,000.

4. Interest on capital should be raised from 5% to 6% per annum and calculated on the

capital accounts after the elimination of goodwill.

5. The new profit sharing ratio for Kamau, Kimani and Kimata should be 4:2:1

respectively.

In preparing the draft financial statements for the year ended 31 December 1999, the

partnership accountant, Otieno, calculated that the partnerships profit for the year was Sh.55,

155,000, and that the working capital of the business as at 31 December 1999 was:

Profit is assumed to accrue evenly during the year.

Partners cash drawings for the year were Kamau Sh.23,705,000, Kimani Sh.19,525,000 and

Kimata Sh.8,250,000.

Required:

(a) The profit and loss appropriation account for the year ended 3 1 December 1999.

(b) The current and capital accounts of the partners for the year ended 31 December

1999.

(c) Balance Sheet as at 31 December 1999.

Date posted:

November 16, 2018

.

Answers (1)

-

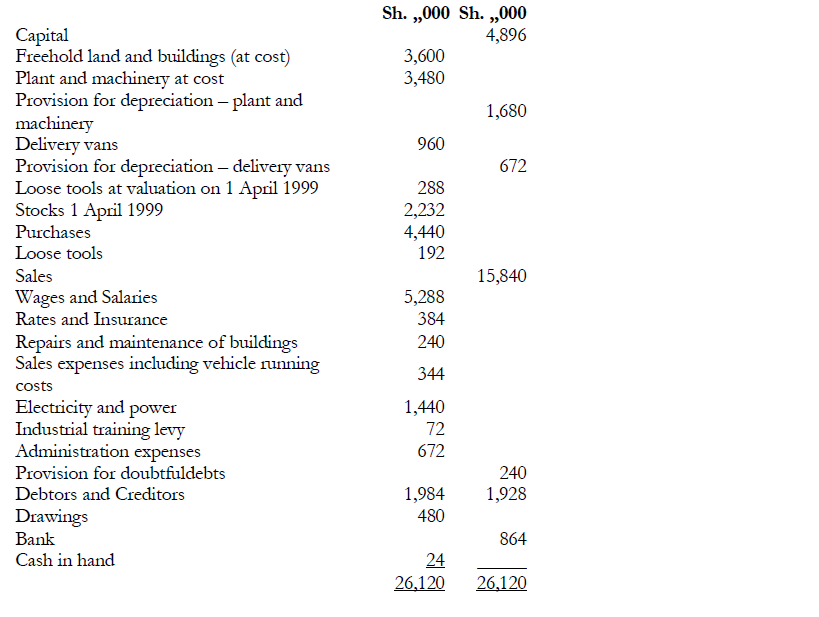

Mr. Ancentus Okwengo is the sole proprietor of a small business. The following trial balance

was extracted from his books at 31 March 2000.

(Solved)

Mr. Ancentus Okwengo is the sole proprietor of a small business. The following trial balance

was extracted from his books at 31 March 2000.

Additional information:

1. Closing stock on 3 1 March

2000 was Sh.2, 008,000.

Loose tools at valuation

Sh.384, 000.

2 .Provision is to be made for the following amount

owing on 3 1 March 2000: Electricity and power

Sh.192,000.

3. Payments in advance on 31 March

2000 were as follows: Van licenses

Sh.2,520 and rates Sh.13,800.

4. Depreciation on plant and machinery and delivery vans is to be provided at the rate of

20% and 25% respectively on cost at the end of the year.

5. Bad debts amounting to Sh.26,000 are to be written off and the provision for

doubtful debts is to be 10% of trade debtors.

Required:

A ten-column worksheet for the year ended 31 March 2000.

Date posted:

November 16, 2018

.

Answers (1)

-

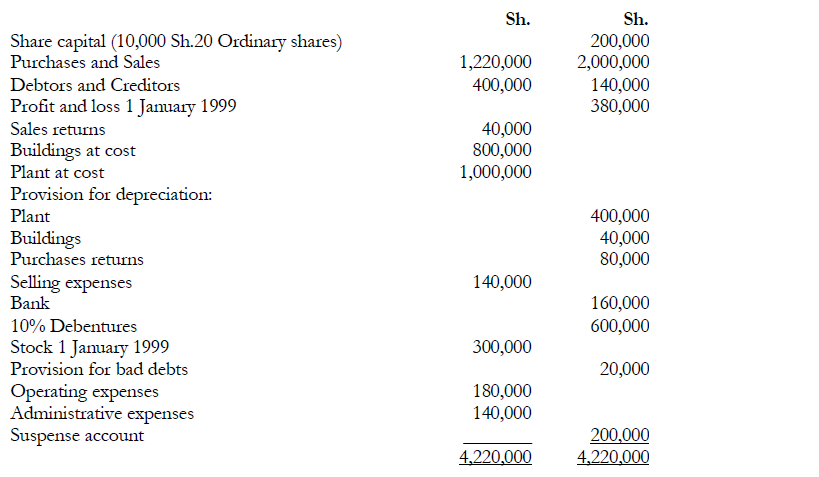

The trial balance of Zach Ltd. as at 31 December 1999 was as follows:

(Solved)

The trial balance of Zach Ltd. as at 31 December 1999 was as follows:

Additional information:

1. Stock at 31 December 1999 was Sh.360,000.

2. Sales returns of Sh.20,000 have been entered in the sales day book as if they were sales.

When this error was discovered, the debtors account had been corrected but the sales figure

was not rectified.

3. 5000 new shares were issued during the year at Sh.32. The proceeds have been credited to

the suspense account.

4. A fully depreciated plant which cost Sh.200,000 was sold during the year. No other entries except

bank have been made. The remaining balance on the suspense account after (2 and 3) above

represents the sale proceeds.

5. A debtor of Sh.20,000 has been declared bankrupt. A general provision is required at 5% of

debtors.

6. Rates of Sh.30,000 paid in December covering half year to 31 March 2000 have not been

entered in the books.

7. Debenture interest has not been paid.

8. Depreciation on plant is at 10% on cost and buildings at 2% on cost.

9. The directors propose to pay a dividend of Sh.2 per share and transfer Sh.20,000 to the

general reserve.

10. Corporation tax at a rate of 32'/2% on profits is estimated to be Sh.90,000.

Required:

(a)Suspense account for the year ended 3I December 1999

(b)Trading,profit and loss account for the year ended 31 December 1999.

(c) Balance sheet as at 31 December 1999.

Date posted:

November 15, 2018

.

Answers (1)