-

Meza Ltd has an authorized share capital of Sh.20,000,000 divided into 1,500,000 ordinary shares of Sh.10 each and 250,000 8% preference shares of Sh.20 each.

An...

(Solved)

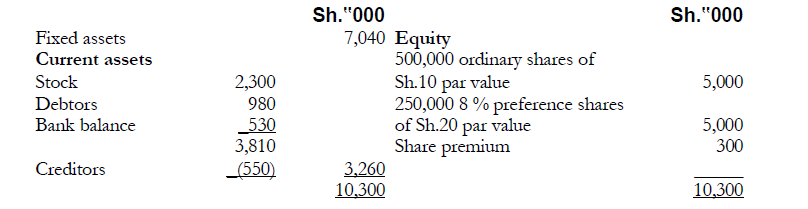

Meza Ltd has an authorized share capital of Sh.20,000,000 divided into 1,500,000 ordinary shares of Sh.10 each and 250,000 8% preference shares of Sh.20 each.

An extract of the balance sheet as at 30 June 2003 was as follows:

On 1 July 2003, the company offered 500,000 ordinary shares for sale to the public at Sh.15 each

payable as follows:

- On application Sh.7 including the premium

- On allotment Sh.5

- On first and final call, Sh.3

Applications were received on 15 July 2003 and allotment made on 31 July 2003. The allotment

money was received on 15 August 2003.

The first and final call was made on 15 September 2003 and the money received on 30

September 2003.

The company received applications for 650,000 shares. Applications for 25,000 shares were

rejected and the application money was refunded. The shares were then allocated to the

remaining applicants on a pro rata basis, the excess of the application money being carried

forward in part satisfaction of the amounts due on allotment.

An allotee of 3,000 shares failed to pay both the allotment and first and final call money and the

shares were forfeited on 13 October 2003.

The forfeited shares were then re-issued at Sh.12 each on 21 October 2003.

Required:

(a) Ledger accounts to record the above transactions

(b) Balance sheet as at 21 October 2003

Date posted:

November 17, 2018

.

Answers (1)

-

The following version of the receipts and payments account has been provided by the treasurer of Maendeleo Social club for the year ended 31 October...

(Solved)

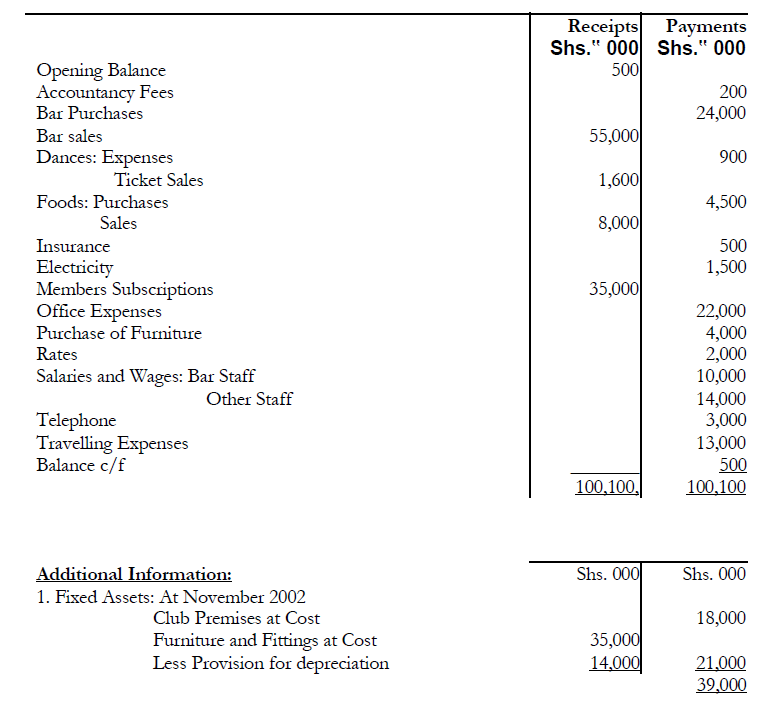

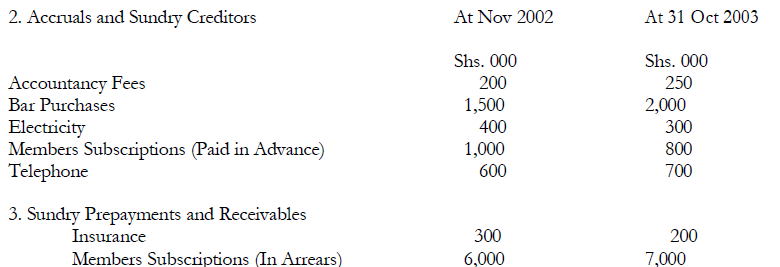

The following version of the receipts and payments account has been provided by the treasurer of Maendeleo Social club for the year ended 31 October 2003:

4. Maendeleo Social Club had a Bank Account, which had a balance of Shs. 2,500,000 on

1 Nov 2002. This Bank account was not used during the year to 31 Oct 2003and the

only entry made in this account was for the interest of shs. 200,000 which was credited

yo the bank on 31 Oct 2003.

5. Depreciation on Furniture and fittings is at the rate of 10% per annum on cost. A full

years depreciation is provided for any furniture bought during the year.

6. Bar stock was valued at shs. 7,000,000 0n 1 Nov 2002 and at Shs. 1,500,000 on 31

Oct 2003.

7. No Apportionment of costs is made between bar activities and other club activities.

Required:

i. Income and Expenditure Account for the year 31 Oct 2003.

ii. Balance Sheet

Date posted:

November 17, 2018

.

Answers (1)

-

The following are the summarized financial statements of Deweto limited

(Solved)

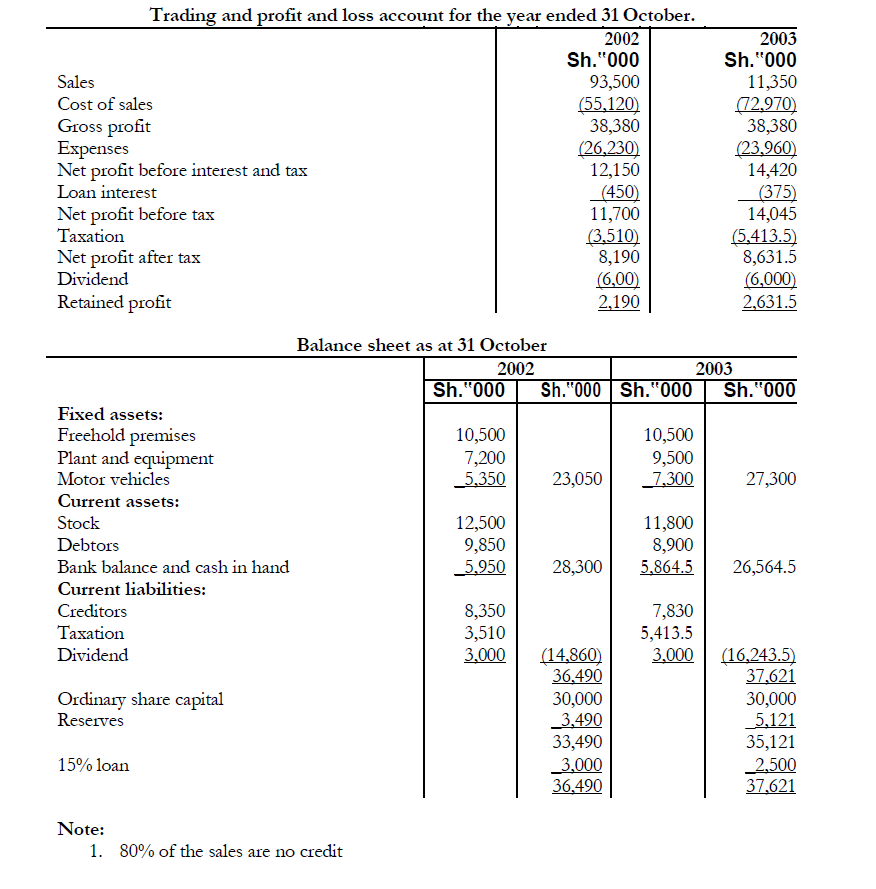

The following are the summarized financial statements of Deweto limited:

2. The stock as at 31 October 2001 was valued at Sh.13,000,000

Required:

(a) Calculate two ratios for each classification identified below for the financial years ended

31 October 2002 and 2003:

(i) Profitability ratios

(ii) Liquidity ratios

(iii) Gearing ratios

(iv) Activity ratios

(b) Comment on Deweto Ltd‟s profitability and liquidity positions.

Date posted:

November 17, 2018

.

Answers (1)

-

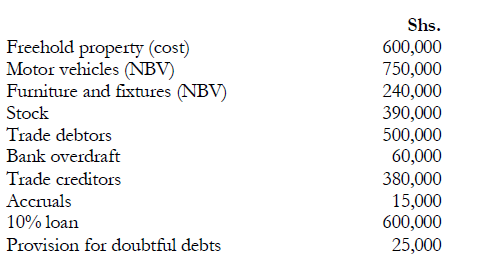

Muthusi is a businessman operating a retail business in a small town. Due to the size of his

business, he is not able to employ a...

(Solved)

Muthusi is a businessman operating a retail business in a small town. Due to the size of his

business, he is not able to employ a qualified accountant on a permanent basis.

The following information was extracted from the books of the business as at 31 October 2002:

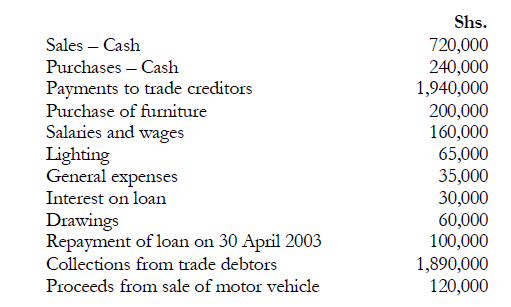

The following transactions took place during the financial year ended 31 October 2003:

1. Sales and purchases on credit amounted to Sh.2,080,000 and Sh.1,900,000 respectively.

2. The following transactions were carried out through the bank account:

3. The business depreciates motor vehicles at 20% per annum on a reducing balance basis. A full

year‟s depreciation is provided on a motor vehicle acquired in the course of the year

and no depreciation is provided on a motor vehicle disposed of in the course of the year.

The motor vehicle sold in the year had been purchased at Sh.250,000 and an

accumulated depreciation of Sh.122,000 had been provided on it at the time of disposal.

4. Furniture is depreciated at 10% per annum on cost and in proportion to the period used in

the year. The additional furniture was purchased on 1 May 20903 while the cost of furniture

held on 31 October 2002 was Sh.400,000

5. Loan interest paid was for one-half year up to 30 April 2003

6. The business received discounts of Sh.40,000 and allowed discounts of Sh.70,000 during the

year.

7. Bad debts of Sh.20,000 were written off. Provision for doubtful debts is to be maintained at

5% of the debtor‟s balance at the end of the year.

8. Accruals are in respect of lighting and on 31 October 2003, the amount accrued was

Sh.19,000

9. Muthusi‟s business obtains a normal gross profit rate of 25% on selling price.

Required:

(a) Trading and profit and loss account for the year ended 31 October 2003

(b) Balance sheet as at 31 October 2003.

Date posted:

November 17, 2018

.

Answers (1)

-

The following categories of people are recognized as users of the information

contained in financial statements:

- Owners.

- Financial analysts.

- Lenders.

For each of the above users of...

(Solved)

The following categories of people are recognized as users of the information

contained in financial statements:

- Owners.

- Financial analysts.

- Lenders.

For each of the above users of financial statements, identify the kind of information they

may require, why they require it and the decisions they make from that information.

Date posted:

November 17, 2018

.

Answers (1)

-

Briefly explain three circumstances under which “goodwill” can be recorded in a business firm's books of account

(Solved)

Briefly explain three circumstances under which “goodwill” can be recorded in a business firm's books of account.

Date posted:

November 17, 2018

.

Answers (1)

-

What is an “accounting policy”?

(Solved)

What is an “accounting policy”?

Date posted:

November 17, 2018

.

Answers (1)

-

Munyaka and Opiyo commenced trading on 1 May 2002 as wholesalers, sharing profits and losses in the ration 2:1, after allowing interest on the capital...

(Solved)

Munyaka and Opiyo commenced trading on 1 May 2002 as wholesalers, sharing profits and losses in the ration 2:1, after allowing interest on the capital introduced by the partners at the rate of 10% per annum. Opiyo was to receive a salary of Sh. 440,000 per annum. Munyaka and

Opiyo do not operate a complete set of accounting records.

The following summary of the bank statements for the year ended 30 April 2003 has been provided:

Receipts: Cash introduced as capital on 1 May 2002: Munyaka Sh. 3,500,000 and Opiyo

Sh. 2,000,000. Balance of receipts from customers amounted to Sh. 12,700,000.

Payments: Equipment Sh. 2,500,000: Pick-up Sh. 1,000,000: furniture and fittings Sh.

375,000: go-down rental Sh. 375,000, wages Sh. 1,772,000; salary of Sales

Manager Sh. 1,200,000; purchases for resale Sh. 9,900,000; rates Sh. 200,000;

repairs Sh. 62,500; insurance Sh. 55,000; motor expenses Sh. 186,500.

The following cash payments were made before banking the balance of the takings; Motor

expenses Sh. 129,000, wages Sh. 148,000; Sundry expenses Sh. 25,000; Drawings – Munyaka

Sh. 7,500 per week and Opiyo Sh. 6,000 per week.

Additional information:

1. The partners had taken goods for their domestic use as follows:

Munyaka Sh. 50,000; Opiyo Sh. 75,000 (both at selling price).

2. During the year to 30 April 2003, discounts allowed to customers amounted to Sh.

122,500 while discounts received from suppliers amounted to Sh. 55,000.

3. At 30 April 2003,l the amounts owing to suppliers amounted to Sh. 750,000 and the

amount owing by customers was Sh. 1,550,000. An amount of Sh. 200,000 owing by a

customer proved irrecoverable and was treated as a bad debt.

4. As at 30 April 2003, rates and insurance were prepaid to the extent of Sh. 25,000 and

Sh. 5,000 respectively. Stock on hand at cost amounted to Sh. 1,205,000.

5. The go-down had been occupied since 1 May 2002 at an annual rental of Sh. 500,000.

6. Depreciation is to be provided on a straight-line basis as follows: Motor vehicles 20%

per amount: Equipment, furniture and fittings at the rate of 10% per annum.

Required:

(a) Trading, profit and loss and appropriation accounts for the year ended 30 April 2003.

(b) Balance sheet as at 30 April 2003.

(Assume a 52 – week year)

Date posted:

November 17, 2018

.

Answers (1)

-

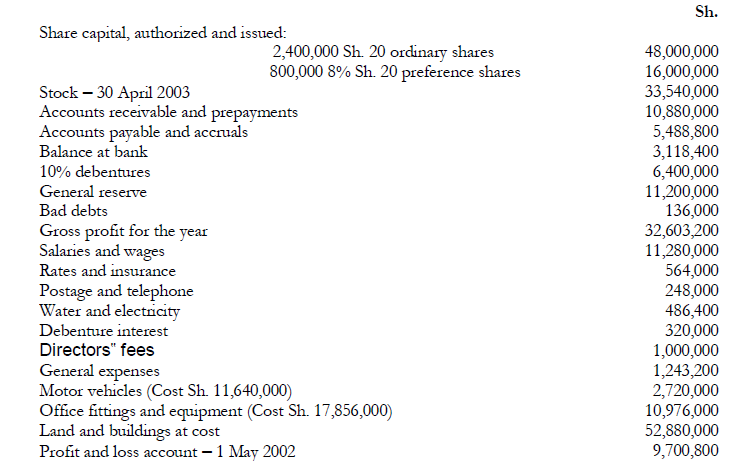

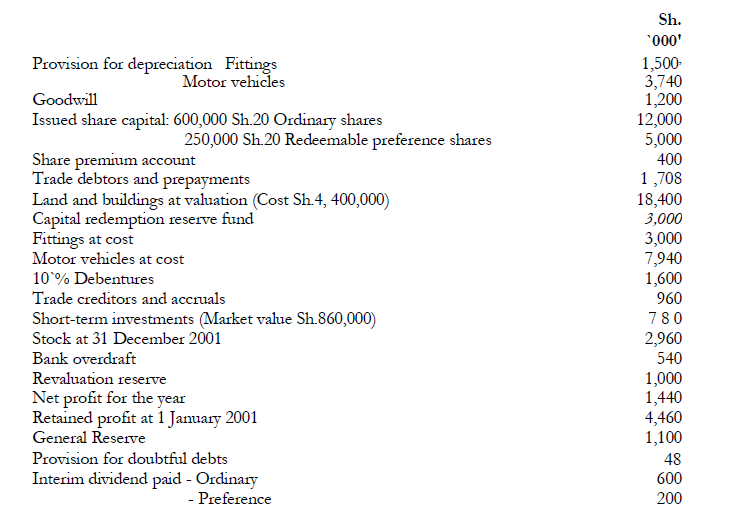

The following balances remained in the books of Ahadi Ltd. as at 30 April 2003 after the preparation of the trading account:

(Solved)

The following balances remained in the books of Ahadi Ltd. as at 30 April 2003 after the preparation of the trading account:

Additional information:

1. A bill for Sh. 219,200 in respect of electricity for the period up to 30 April 2003 has

not been accrued.

2. The amount for insurance includes a premium of Sh. 120,000 paid in January 2003

to cover the company for six months, February to July, 2003.

3. Office fittings and equipment are to be depreciated at 15% per annum on cost

and motor vehicles at 20% per annum on cost.

4. Provision is to be made for:

Directors‟ fees - Sh. 2,000,000

Audit fee - Sh. 480,000

The outstanding debenture interest.

5. The directors have recommended that:

- A sum of Sh. 4,800,000 be transferred to general reserve.

- The preference dividend be paid.

- A 10% ordinary dividend be paid.

Required:

(a) Profit and loss and appropriation accounts for the year ended 30 April 2003.

(b) Balance sheet as at 30 April 2003.

Date posted:

November 17, 2018

.

Answers (1)

-

You have recently been employed in a medium size company and deployed in the accounts department. Your head of section has given you the following...

(Solved)

You have recently been employed in a medium size company and deployed in the accounts department. Your head of section has given you the following extract from the cashbook for the month of April 2003.

The head of section further informs you that all receipts are banked intact and all payments are

made by cheque. On investigation, you discover the following:

1. Bank charges and commissions amounting to Sh. 272,000 entered on the bank

statement had not been entered in the cashbook.

2. Cheques drawn amounting to Sh. 534,000 had not been presented to the bank for

payment.

3. Cheques received totaling Sh. 1,524,000 had been entered in the cashbook and paid into

the bank, but had not been credited by the bank until May 2003.

4. A cheque for Sh. 44,000 had been entered as a receipt in the cashbook instead of a

payment.

5. A cheque for Sh. 50,000 had been debited by the bank by mistake.

6. A cheque received for Sh. 160,000 had been returned unpaid. No adjustment had been

made in the cashbook.

7. All dividends receivable are credited direct to the bank account. During the month of

April 2003. Dividends totaling Sh. 124,000 were credited by the bank and no entries had

been made in the cashbook.

8. A cheque drawn for Sh. 12,000 had been incorrectly entered in the cash book as Sh.

132,000.

9. The balance brought forward should have been Sh. 1,422,000.

10. The bank statement as at 30 April 2003 showed on overdraft of Sh. 2,324,000.

Required:

(i) The adjusted cashbook as at 30 April 2003.

(ii) Bank reconciliation statement as at 30 April 2003.

Date posted:

November 17, 2018

.

Answers (1)

-

Briefly explain why it is important for a business entity to prepare a bank reconciliation statement

(Solved)

Briefly explain why it is important for a business entity to prepare a bank reconciliation statement

Date posted:

November 17, 2018

.

Answers (1)

-

Differentiate between a petty cashbook and a three-column cashbook

(Solved)

Differentiate between a petty cashbook and a three-column cashbook.

Date posted:

November 17, 2018

.

Answers (1)

-

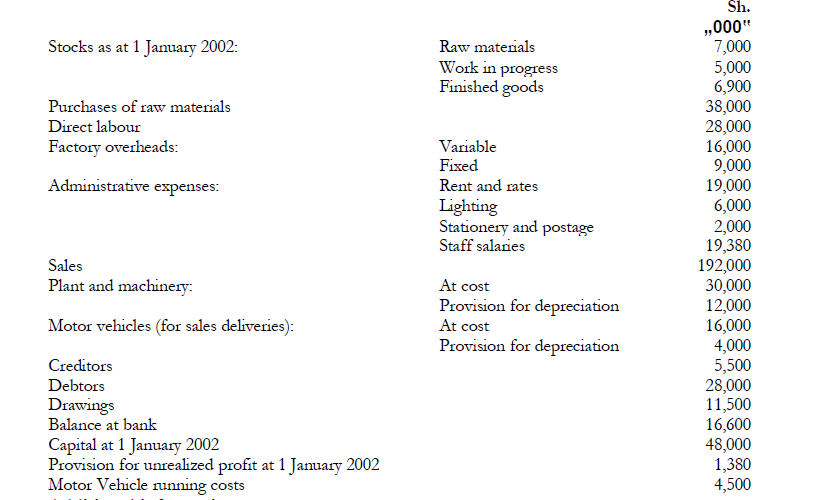

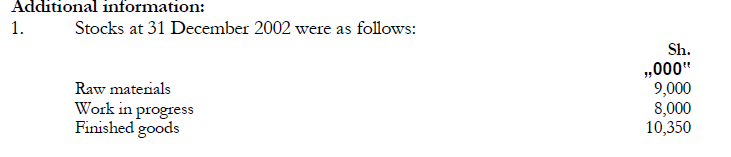

The following balances have been extracted from the books of Limuru Manufacturers, a small scale manufacturing enterprise, as at 31 December 2002:

(Solved)

The following balances have been extracted from the books of Limuru Manufacturers, a small scale manufacturing enterprise, as at 31 December 2002:

2. The factory output is transferred to the trading account at factory cost plus 25%

of factory profit.

3. Depreciation is provided at the rates shown below on the original cost of fixed

assets held at the end of each financial year.

Plant and machinery - 10% per annum

Motor vehicles - 25% per annum

4. Amounts accrued at 31 December 2002 for direct labour amounted to Sh. 3,000,000

and rent and rates prepaid at 31 December 2002 amounted to Sh. 2,000,000.

Required:

(a) Manufacturing, trading and profit and loss account for the year ended 31 December

2002.

(b) Balance sheet as at 31 December 2002.

Date posted:

November 17, 2018

.

Answers (1)

-

Write short notes to distinguish the following:

(a) Purchased goodwill and non-purchased goodwill.

(b) Amortisation and depreciation of fixed assets.

(c) Provisions and reserves.

(d) Compensating errors and errors...

(Solved)

Write short notes to distinguish the following:

(a) Purchased goodwill and non-purchased goodwill.

(b) Amortisation and depreciation of fixed assets.

(c) Provisions and reserves.

(d) Compensating errors and errors of principle

Date posted:

November 17, 2018

.

Answers (1)

-

Denticare Limited makes its accounts on 30 June every year. On 1 July 2001, the company's balance sheet included the following figures for non -current...

(Solved)

Denticare Limited makes its accounts on 30 June every year. On 1 July 2001, the company's balance sheet included the following figures for non-current assets:

The company's policy is to charge depreciation at the following rates:

A proportionate charge is made in the year of purchase, sale or revaluation of an asset.

During the year ended 30 June 2002, the following transactions took place:

1. On 1 January 2002 the company decided to adopt a policy of revaluing its buildings. A

professional valuer engaged for this purpose revalued the buildings at Sh.34

million.

2. On 1 Janua ry a plant that had cost Sh.3 million was sold for Sh.500, 000. Accumulated

depreciation on this plant on 30 June2001 amounted to Sh.2.3 million. A new plant was

then purchased at a cost of Sh.4 million.

3. On 1 April 2002 a new motor vehicle was purchased for Sh.300, 000 Part of the

purchase price was settled by exchanging another motor vehicle at an agreed value of

sh.120, 000 The balance of Sh.180,000 was paid in cash. The vehicle which was given in

part exchange had cost Sh.200, 000 and had a net book value of Sh.100, 000 as at 30

June 2001

Required:

(a) The following ledger accounts to record the above transactions:

(i) Buildings account.

(ii) Provision for depreciation: Buildings.

(iii) Plant and machinery account.

(iv) Provision for depreciation: Plant and Machinery.

(v) Motor vehicles account.

(vi) Provision for depreciation: Motor vehicles.

(b) Property, plant and equipment movement schedule for the year ended 30 June 2002.

Date posted:

November 17, 2018

.

Answers (1)

-

Masaba Company Ltd. is a retail provider with an authorised share capital of 800,000 Sh.20 ordinary shares and 250,000 8% Sh.20 redeemable preference shares.

The following...

(Solved)

Masaba Company Ltd. is a retail provider with an authorised share capital of 800,000 Sh.20 ordinary shares and 250,000 8% Sh.20 redeemable preference shares.

The following financial information reflects the position of the company as at 31 December

2001 after preparing the Trading, profit and loss account:

The following resolutions relating to year ended 31 December 2001 have been passed by the

board of directors of the company

1. Transfer Sh.500,000 to General Reserve.

2. Provide for 5% final dividend and final preference dividend on shares issued

and outstanding on 31 December 2001.

3. Make a bonus issue of 100,000 fully paid ordinary shares from the retained profits

account.

Required:

(i) The appropriations account of Masaba Company Ltd. for the year ended 31 December

2001.

(ii) The balance sheet of Masaba Company Ltd. as at 31 December 2001.

Date posted:

November 17, 2018

.

Answers (1)

-

Explain the legal provisions regarding the establishment and subsequent use of the following reserves: (i) Share premium account. (ii) Capital redemption reserve fund.

(Solved)

Explain the legal provisions regarding the establishment and subsequent use of the following reserves: (i) Share premium account. (ii) Capital redemption reserve fund.

Date posted:

November 17, 2018

.

Answers (1)

-

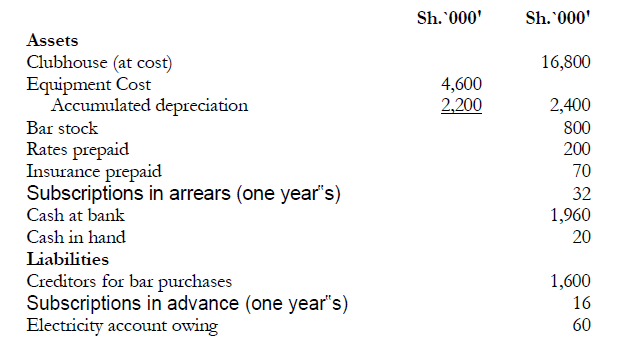

The Swara Sports Club had the following assets and liabilities as at 30 September 2002

(Solved)

The Swara Sports Club had the following assets and liabilities as at 30 September 2002:

The treasurer of the club, Mr. Lutomia is in process of drawing up the financial forecast of

the club for the coming year, ending on 30th September2003.

He wishes to prepare a forecast income and expenditure account for the year and a balance

sheet as at that date.

The following information has been collected to assist in the forecast:

1. The club has 300 members and it is intended to raise the subscriptions per member

from the current Sh.8,000 to Sh.10,000 per year. The members who have paid in

advance will be allowed subscriptions at the old rates. It is anticipated that the members

currently in arrears with their subscriptions will pay the arrears during the coming year.

It is also anticipated that the number of members whose subscriptions would be in

arrears and those who would have paid in advance on 30 September 2003 would be the

same as the corresponding numbers on 30 September 2002.

2. Extensions to the clubhouse are planned which will cost an estimated amount of

Sh.3,000,000. Of this sum, it is anticipated that Sh.2, 000,000 will be paid during the

year.

3. Some of the club's sports equipment which cost Sh.500,000 and has a written value of

Sh.200,000 will be sold for u estimated value of Sh.100,000 and replaced by new

equipment costing Sh.680,000. All equipment is depreciated on a straight-line basis over

four years and none of the equipment is more than three years old. A full year's

provision is charged in the year of acquisition and none in the year of disposal.

4. Bar purchases are made monthly on credit and paid for in the month following

purchase. It is anticipated that the same volume of business, which is fairly constant on

a monthly basis, will be realised during the coming year but that stock costs will rise by

25% from 1 October 2002. Bar stocks are normally held at the level of one half of one

month's purchases. The bar makes a gross profit margin of 20% on all sales regardless

of stock costs. Bar sales are on cash, all of which is banked daily. The barman, who is

paid Sh.20,000 per month, receives a commission of 5% of the gross profit for the year.

This is paid with his final wage cheque by the year end.

5. The club runs monthly social evenings and charges members Sh.2, 000 per head

admission. An average of 200 members attend each of these evenings. Expenses usually

amount to Sh. 1,400 per head.

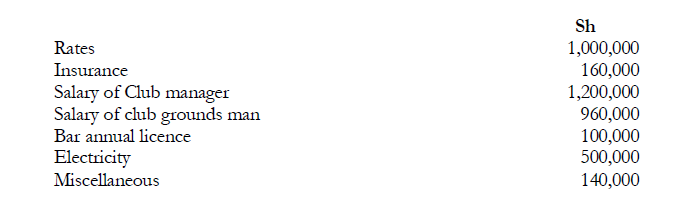

6. The following expenditure payments are expected to be made by the club during the

coming year:

The rates are paid on 1 January in respect of the following twelve months. The insurance

payment will be for the Period 1 April 2003 to 31 March 2004. One-fifth of electricity

consumption is in respect of the bar. All payments are made by cheque.

Required:

(a) Forecast bank account for the year ending 30 September 2003.

(b) Forecast bar. Trading, profit and loss account for the year ending 30 September 2003

(c) Forecast income and expenditure account for the year ending 30 September 2003.

(d) Balance sheet as at 30 September 2003.

Date posted:

November 17, 2018

.

Answers (1)

-

On 1 October 2001, Mr. Robert Kanyarna bought Premium Meat Suppliers Ltd., a business

dealing in meat products, for a cash price of Sh.8, 000,000. He...

(Solved)

On 1 October 2001, Mr. Robert Kanyarna bought Premium Meat Suppliers Ltd., a business

dealing in meat products, for a cash price of Sh.8, 000,000. He took over the following assets

and liabilities of the company:

Mr. Kanyama immediately opened a business bank account in which he deposited as working

capital, Sh.1, 600,000 from himself and Sh.4,000,000 being a long - term loan from J.K. Bank

Ltd. The loan from the bank carried an interest rate of 10% per year.

During the year ended 30 September 2002, Mr. Kanyama did not keep a full set of double -

entry accounting records but relied heavily on close and personal involvement in the business to

ensure proper control and safekeeping of assets of the business. In addition, daily cash

summaries were prepared and counterfoil cheque stubs and bank statements reconciled. The

following information relates to transactions in the year ended 30 September 2002:

1. Before banking proceeds from sales and debtors, payments were made out of cash as

summarised below:

2. A summary of cheques counterfoil stubs disclosed the following payments through

the bank:

3. Mr. Kanyama had, each week, made deposits into his business bank account all cash on

hand after payments in (I) above) except a till float of Sh.40,000 maintained throughout the

year. An examination of the pay-in slips and bank statements revealed total deposits of

Sh32,280,00Q, exclusive of capital and loan) during the year.

4. At 30 September 2002, Mr. Kanyama was owed Sh.592, 000 by debtors and owed

Sh1,720,000 to trade creditors. Wages outstanding at that date amounted to Sh.270, 000.

The stock at 30 September 2002 was valued at cost at Sh. 1, 160,000. The only cash on

hand at the year-end was in the till float.

5. Mr. Kanyama consulted with Chania Accountants and has accepted their advice to make a

provision of 2% per annum for depreciation on buildings and 10°/% per annum for

depreciation on plant and equipment. Mr. Kanyama also considers it prudent to provide for

the fact that 1% of the debtors outstanding at the year end will not honour their

obligations.

Required:

(a) Bank and cash accounts for the year ended 30 September 2002.

(b) Trading, profit and loss account for the year ended 30 September2002.

(c) Balance sheet as at 30 September 2002.

Date posted:

November 17, 2018

.

Answers (1)

-

Distinguish between each of the following pairs of terms:

(i) Receipts and revenue.

(ii) Balance sheet and statement of affairs.

(iii) Cash basis of accounting and accrual basis...

(Solved)

Distinguish between each of the following pairs of terms:

(i) Receipts and revenue.

(ii) Balance sheet and statement of affairs.

(iii) Cash basis of accounting and accrual basis of accounting.

(iv)Materiality and substance over form.

Date posted:

November 17, 2018

.

Answers (1)