-

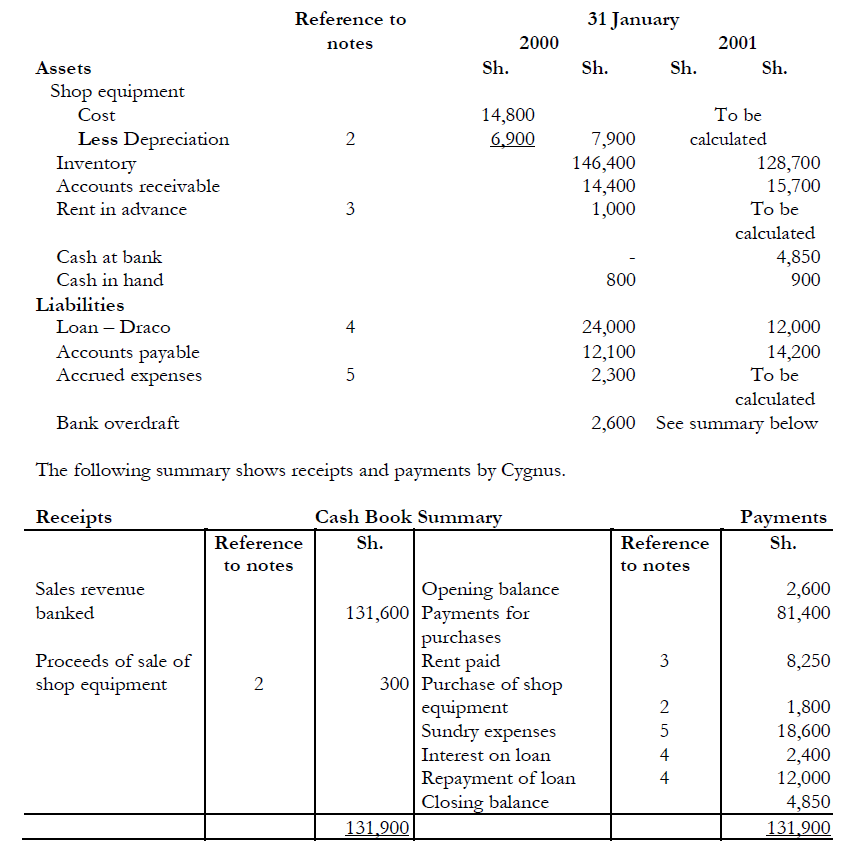

Cygnus is a sole trader selling antiques from a rented shop. He has not kept proper

accounting records for the year ended 31 January 2001, in...

(Solved)

Cygnus is a sole trader selling antiques from a rented shop. He has not kept proper

accounting records for the year ended 31 January 2001, in spite of his accountant‟s advice

after the preparation of his accounts for the year ended 31 January 2000.

His assets and liabilities at 31 January 2000 and 31 January 2001 were as follows:

Before banking the shop takings, Cygnus took various amounts as drawings.

Notes

(1) Cygnus fixes his selling prices by doubling the cost of all items purchased.

(2) During the year, Cygnus sold for Sh.300 equipment that had cost Sh.800, and had a

written down value at 1 February 2000 of Sh.200. He purchased further equipment on

1 August 2000 for Sh.1,800.

(3) Depreciation is charged at 10% per year on the straight-line basis, with no

depreciation in the year of sale and proportionate depreciation in the year of purchase.

(4) Rent is payable quarterly in advance on 1 January, 1 April, 1 July and 1 October

each year. On 1 July 2000, the annual rent was increased from Sh.6,000 to Sh.9,000.

(5) The loan from Draco carries interest at 10% per year payable annually on 31

December. On 31 December 2000, Cygnus repaid Sh.12,000 of the loan. The balance is

repayable on 31 December 2004.

(6) The accrued expenses at 31 January 2000 consist of the Sh.200 interest accrued

on Draco.s loan (see Note 4) and sundry expenses of Sh.2,100. At 31 January

2001, accruals for sundry expenses amounted to Sh.3,300.

Required:

(a) Prepare for Cygnus an income statement for the year ended 31 January 2001 and a

balance sheet as at that date.

Date posted:

November 24, 2018

.

Answers (1)

-

Briefly explain the following accounting Concepts. (i) Going concern (ii) Accruals (iii) Consistency (iv) Prudence or conservatism (v) Materiality

(Solved)

i) Going concern

ii) Accruals

iii) Consistency

iv) Prudence or conservatism

v) Materiality

vi) Substance over form

vii) Business entity concept

viii) Money measurement

ix) Historical cost

x) Objectivity

xi) Realization

xii) Duality

Date posted:

November 24, 2018

.

Answers (1)

-

What are accounting concepts, Bases, Policies?

(Solved)

What are accounting concepts, Bases, Policies?

Date posted:

November 24, 2018

.

Answers (1)

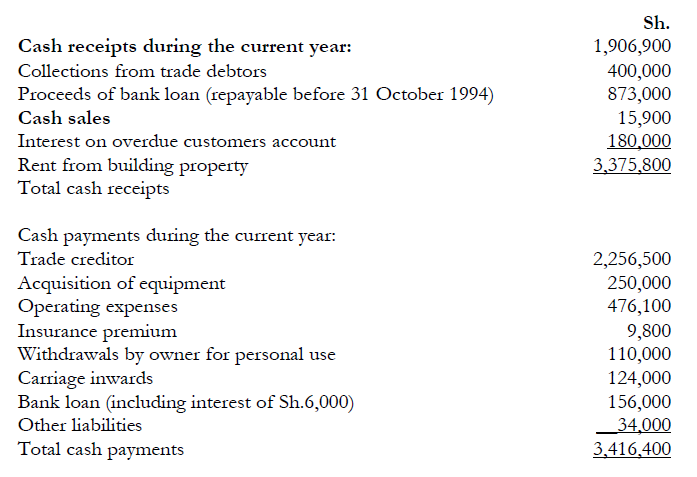

-

Mr. James Bulayi formed Malimia Traders, a sole proprietorship five years ago. His initial capital

injection was Sh.1,000,000 cash. For a number of years, Bulayi's wife...

(Solved)

Mr. James Bulayi formed Malimia Traders, a sole proprietorship five years ago. His initial capital

injection was Sh.1,000,000 cash. For a number of years, Bulayi's wife maintained the accounting

records, but early in 1993 she became seriously ill. Mr. Bulayi consulted a CPA firm whose

manager told him "you keep a record of your cash receipts and payments and a list of your

assets and liabilities, at the beginning and end of the year, and I will prepare financial statements

for you at the end of the year".

On 31 October 1993, Mr. Bulayi presented the following data to the Manager of the CPA firm.

Additional information:

i) Although the primary source of revenue is from trading Malimia Traders also earns income

from rent and interest. Malimia Trader conducts business from the ground floor of its twofloor

storey building. The first floor is rented to a shoe-retailer for a monthly rent. The

retailer pays 6 months rent in advance on 1 March and 1 September every year. Malimia

Traders increased rent from Sh.15,000 per month to Sh.20,000 per month with effect from

1 September 1993. Malimia Traders charges interest on overdue customers accounts, which

customers usually pay together with the principal amount due. Interest owing by customers

on 31 October 1993 was Sh.5,000.

ii) The following balances of assets and liabilities were extracted on 31 October 1992

iii) Sh.14,000 of debts had been written off during the accounting period, of which Sh.8,500

was from sales of the previous accounting year, Bulayi estimated that Sh.14,200 of the 31

October 1993 debtors balances may be uncollectable and a provision is required.

iv) Returns inwards and returns outward all applicable to current year's sales and purchases are

Sh.60,000 and Sh.50,000 respectively.

v) Cash discount taken by credit customers in the year are Sh.41,300 discounts on purchases

are Sh.64,000.

Depreciation is to be provided on reducing balance on fixed assets held at year end at the

rate of 5% per annum on building and 25% per annum on equipment. There were no

disposals of plant assets during the year.

Interest owing on the bank loan at 31 October 1993 is Sh.17,500. The amount paid for

insurance includes a premium of Sh 8,000 paid to cover the firm against fire for the Co. six

months to 31 January 1994.

Stock in hand on 31 October 1993 was valued at Sh985,000.

On 31 October 1993 the amounts owing to suppliers was Sh.523,000 and the amount

owing by customers was Sh,663,2000 (excluding interest on overdue accounts). All

purchases of stock are on credit.

Ground rent and land rates for the year amounted to Sh.50,000 The bills received in

respect of the two are not yet paid.

Required:

Malimia Traders' Trading, Profit and loss Account for the year ended 31 October 1993 and a

Balance Sheet as at that date.

Date posted:

November 24, 2018

.

Answers (1)

-

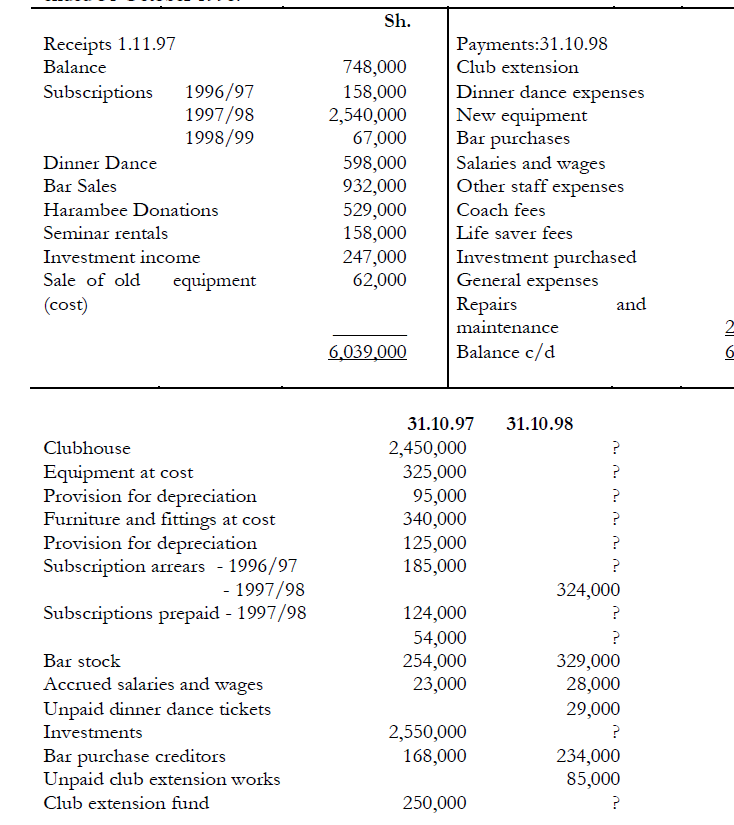

The treasurer of Watembezi Sports Club has presented the following information for the year ended 31 October 1998

(Solved)

The treasurer of Watembezi Sports Club has presented the following information for the year ended 31 October 1998

Notes:

1) The Harambee donations were for the extension of the club. The funds shall remain in this

account until the works, are completed when' the balance will be transferred to the

accumulated fund.

2) The depreciation on fixed assets is at 10% and 15% on cost on furniture and fittings; and

equipment respectively.

3) Equipment which had cost Sh.25,000 was sold on credit for Sh.14,000 to a member who

owed the club the money at the end of the year. The provision for depreciation on this

equipment was Sh.7,000. Another equipment sold for cash had an accumulated provision

for depreciation of Sh.19,000.

4) Audit fees of Sh.50,000 should be provided.

5) Subscription in arrears are written-off after 12 months.

Required:

a) Income and expenditure account for the year ended 31 October 1998

b) Balance as at 31 October 1998

Date posted:

November 24, 2018

.

Answers (1)

-

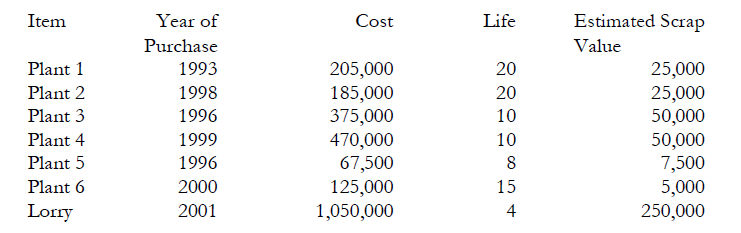

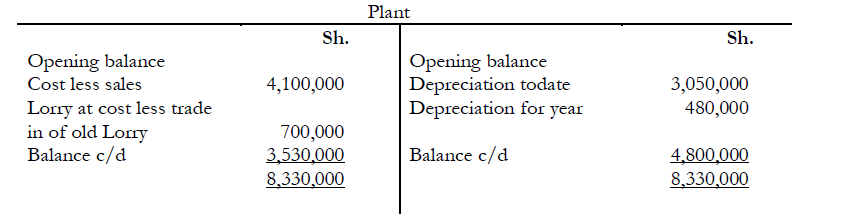

Reviewing the draft accounts of Uzee Ltd for the year ended 31 st December 2001 as prepared by the Chief Accountant, the Managing Director suggests...

(Solved)

Reviewing the draft accounts of Uzee Ltd for the year ended 31 st December 2001 as prepared by the Chief Accountant, the Managing Director suggests that the written down value of plant is too low. To support his argument he produces the following schedule of plant on hand at 31 December 2001:

After discussing the matter the following policy is agreed:

1) Each item of plant to be depreciated on a straight line basis to its estimated scrap value over

its estimated life.

2) A full year's depreciation to be charged in the year of

purchase. On investigation you ascertain that:

There is no plant register.

Plant which includes the lorry is shown in the accounts at cost less proceeds of sales.

3) For some years depreciation was charged at 15% on the reducing balance and then from 31st

December 1994 at 10% of cost less proceeds of sales on a straight line basis.

4) The Plant account for the year ended 31st December 2001 was:

You are required to show, after implementing the new policy:

a) The Plant Account as it should appear in the books of the company for the year ended 31st

December 2001

b) The entries which should appear in the Balance Sheet as on 31st December 2001 and

c) A note explaining the effect on the profits on the change of depreciation policy.

Date posted:

November 24, 2018

.

Answers (1)

-

Juhudi Ltd. has two accounts "A" and "B" with different banks. On 31 March 1995 the cash

book showed a balance of Sh.200,000 in Account" A"...

(Solved)

Juhudi Ltd. has two accounts "A" and "B" with different banks. On 31 March 1995 the cash

book showed a balance of Sh.200,000 in Account" A" and an overdraft of Sh. 90,000 in

account "B". However the bank statements obtained on the same day showed different

balances for the two accounts.

Further investigation reveals the following information: -

1. A deposit of Sh.60,000 made into account" A" on 1 March 1995 has been entered in

the cash book in account "B".

2. A withdrawal of Sh.20,000 from account" A" on 3 March 1995 has been debited in

the cash book in account "B".

3. Cheques of Sh.25,000 and Sh.30,000 deposited in account" A" on 9 March 1995 were

entered in the cash book in account"B". The second cheque has been dishonored by

the bankers. The entry for this dishonored cheque has been entered in the cash book

in account "B".

4. Cheques for Sh.40.000 and Sh.500.000 drawn on accounts" A" and "B" respectively

on 30 March 1995 were not paid by the banks until 5 April 1995.

5. Incidental charges of Sh.400 and Sh.1.000charged in the accounts" A" and "B"

respectively have not been entered in the cash book.

6. The bank has credited an interest of Sh.2.000 for account" A" and has debited bank

charges of Sh.1,500 to account "B". These transactions have not been entered in the

cash book.

7. Deposits of Sh.200,000 and Sh.140,000 made into the accounts" A" and "B"

respectively have not yet been credited by the bank.

8. Dividends amounting to Sh.8,000 had been paid direct to the bank in account "B".

9. A cheque for Sh.3.500 drawn on account" A" on 30 March 1995 in payment of an

electricity bill had been entered in the cash book as Sh.5,300.

Required:

i) The necessary adjustments in both cash books in order to correct the errors.

ii) Bank reconciliation statements for both cash books.

Date posted:

November 24, 2018

.

Answers (1)

-

Define the term bank reconciliation statement and indicate its three main functions

(Solved)

Define the term bank reconciliation statement and indicate its three main functions.

Date posted:

November 24, 2018

.

Answers (1)

-

Explain four ways in which the use of historical cost accounting may cause users of financial statements to be misled when prices are rising.

(Solved)

Explain four ways in which the use of historical cost accounting may cause users of financial statements to be misled when prices are rising.

Date posted:

November 24, 2018

.

Answers (1)

-

Comparability is a characteristic which adds to the usefulness of financial statements.

Required:

(a) Explain what is meant by the term „comparability? in financial statements,

referring to two...

(Solved)

Comparability is a characteristic which adds to the usefulness of financial statements.

Required:

(a) Explain what is meant by the term „comparability‟ in financial statements,

referring to two types of comparison that users of financial statements may make.

(b) Explain two ways in which the IAS (International Accounting Standards) aids the

comparability of financial information.

Date posted:

November 24, 2018

.

Answers (1)

-

Mutiso Mwema started his business in Gikomba as a carpenter on 1 January1990 and he has not

kept proper books of account. He engages you to...

(Solved)

Mutiso Mwema started his business in Gikomba as a carpenter on 1 January1990 and he has not

kept proper books of account. He engages you to examine his records and prepare appropriate

accounts. From your examination of the records and from interviews with Mr. Mwema you

ascertain the following information:

i) On starting the business on 1 January 1990, he put Sh.120,000 into a business bank

account. On the same day, Mr. Mwema brought into the firm his pickup and reckoned that

it was worth Sh. 66,000 then. He estimated that it will have another useful life of three

years.

ii) To increase his working capital he borrowed Sh.40,000 at 15% interest per annum on 1

April 1990 from his sister but no interest has yet been paid.

iii) On 1 January 1990 Miss Wambua was employed as a typist/clerk at a salary of Sh.72,000

per annum.

iv) Drawings were Sh.1,800 per week from the business account for private use during the

year.

v) He purchased timber worth Sh.196,000 out of which Sh.15,800 left in the workshop on 31

December 1990. He had also spent Sh.96,000 on some equipment at the commencement

of the business which he estimates will last him five years.

vi) Electricity bills received up to 31 October 1990 came to Sh.24,000. Motor vehicle expenses

were Sh.18, 200 while general expenses amounted to Sh.27,000 for the year. The insurance

premium for the year 31 March 1991 was Sh.16,000. All these expenses have been paid by

cheque.

vii) Rates for the year to 31 March 1991 came to Sh.3,600 but they had not yet been paid.

viii) Miss Wambua sent out invoices to customers for Sh. 617,800 but only Sh.508,000 had been

received by 31 December 1990. Debts totaling Sh.1,700 were abandoned during the year as

bad. Other customers for jobs too small to invoice have paid Sh.72,600 in cash for work

done of which Sh.56,000 was banked. Mr. Mwema used Sh. 7,500 of the difference to pay

for his family's food stuff, bought Kenya Charity Sweepstake tickets worth Sh.2,400 and

Miss Wambua used the rest of general expenses, except for Sh.3,010 which was left over in

the drawer in the office on 31 December 1990.

ix) You agree with Mr. Mwema that he will pay you Sh. 5,500 for accountancy fee.

Required:

Prepare Profit and Loss Account for the year ended 31 December 1990 and a Balance Sheet as

at that date.

Date posted:

November 22, 2018

.

Answers (1)

-

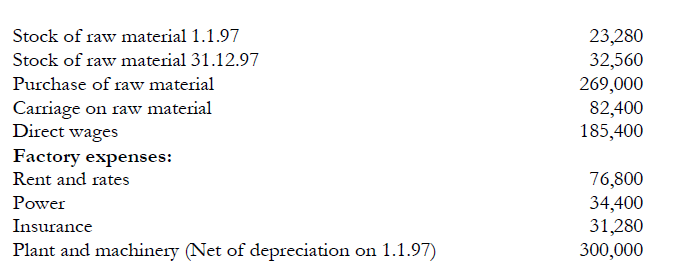

Rono Ltd. manufactures electric toys called Densta on small scale basis.

On 1 January 1997, 6000 units of Densta were in stock.

During 1997, the company manufactured...

(Solved)

Rono Ltd. manufactures electric toys called Densta on small scale basis.

On 1 January 1997, 6000 units of Densta were in stock.

During 1997, the company manufactured 200,000 units and sold 190,000 units at a price of Sh.6

each.

The following balances were extracted from the books of account on 31 December 1997.

The following additional information was available:

1) Stocks of work-in-progress on 1 January and 31 December 1997 were of insignificant value

and are to be ignored.

2) Plant and machinery are to be depreciated using reducing balance method at 10%.

3) Finished units of Densta are valued at factory cost.

4) Factory cost per unit of Densta was the same in 1996 and 1997.

Required:

i ) The manufacturing account for the year ended 31 December 1997, showing clearly the

prime cost and factory costs of producing Densta.

ii) The trading account for the year ended 31 December 1997.

Date posted:

November 22, 2018

.

Answers (1)

-

Explain briefly the terms prime cost and factory cost as used by manufacturing firms

(Solved)

Explain briefly the terms prime cost and factory cost as used by manufacturing firms.

Date posted:

November 22, 2018

.

Answers (1)

-

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4,536,000. On...

(Solved)

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4,536,000. On 3 April 1995, the

company bought its second lorry, KA 735 for Sh.2,740,000. On 3 June 1997, the first lorry, KA

620 was involved in an accident and was completely written off. The insurance company paid

the transport company Sh.l,350,000 for the loss. On 5 January 1998, the company bought its

third lorry, KB 327 for Sh.3,780,000. Depreciation on the lorries was provided at 10 per cent on

straight line basis. The policy of the company is to provide depreciation for the full year for all

acquisitions made at any time during the year and to ignore depreciation on any lorry sold or

disposed of during the year. All the lorries are insured. The company makes its accounts

annually to 31 December. In 1998, the company decided to change its depreciation rate from 10

to 15 per cent on straight line basis for all its lorries still in use retroactively, that is from year of purchase. An adjusting entry will be made in the accounts for the year 1998.

Required:

a) The motor lorries account for years 1994 to 1998.

b) A schedule of additional depreciation arising from change of depreciation rate, for years

1994 to 1997.

c) Provision for depreciation account for the same period.

d) Disposal of motor lorries account.

Date posted:

November 21, 2018

.

Answers (1)

-

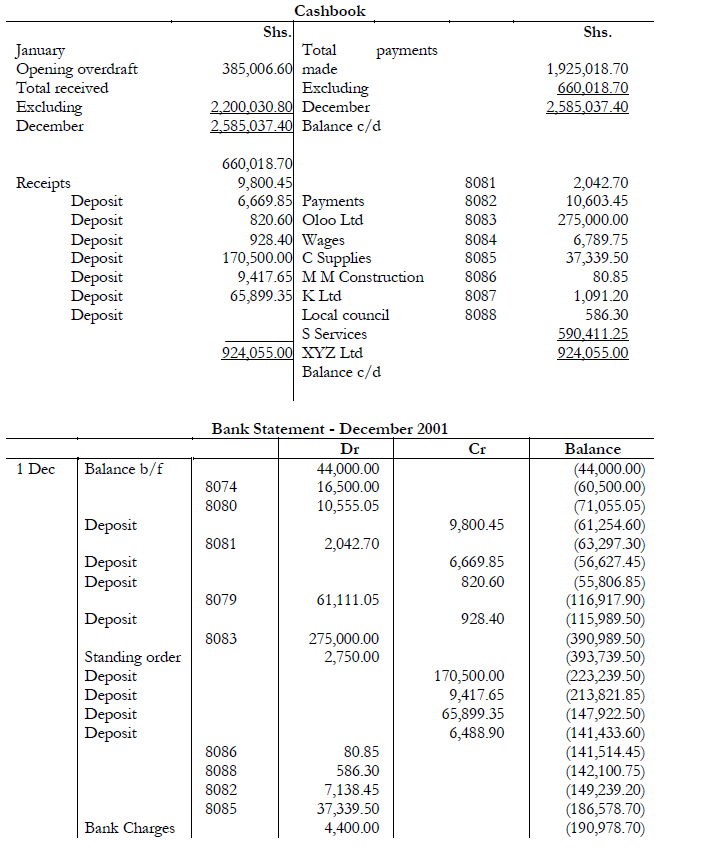

Sijui is having difficulty in preparing a bank reconciliation statement as at 31 December 2001.

He provides a summarized cashbook and a bank statement for the...

(Solved)

Sijui is having difficulty in preparing a bank reconciliation statement as at 31 December 2001.

He provides a summarized cashbook and a bank statement for the month of December as

shown below. Although the bank statement is correct his cashbook has several errors.

Required:

a) Prepare a corrected cashbook

b) A bank reconciliation as at 31 December and

c) A brief explanation as to the likely cause of the remaining difference.

Date posted:

November 21, 2018

.

Answers (1)

-

(a) What are the qualities of useful financial statements

(b) To what extent do International Accounting Standards assist in achieving some of these

qualities.

(Solved)

(a) What are the qualities of useful financial statements

(b) To what extent do International Accounting Standards assist in achieving some of these

qualities.

Date posted:

November 21, 2018

.

Answers (1)

-

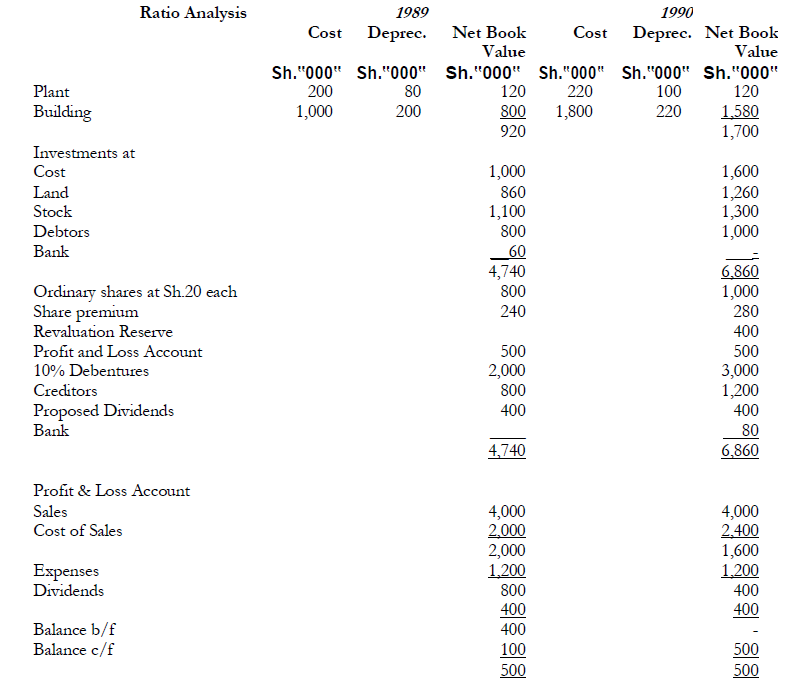

Calculate for Mvita Ltd. for 1989 and 1990 the following ratios:

Return on capital employed;

Debtors turnover;

Creditors turnover;

Current ratio;

Quick assets (acid test) ratio;

(Solved)

Calculate for Mvita Ltd. for 1989 and 1990 the following ratios:

Return on capital employed;

Debtors turnover;

Creditors turnover;

Current ratio;

Quick assets (acid test) ratio;

Gross profit percentage;

Net profit percentage;

Dividend cover;

Gearing ratio.

Using the summarised accounts given and ratios you have just prepared, comment on the

financial position and prospects of Mvita Ltd.

Date posted:

November 21, 2018

.

Answers (1)

-

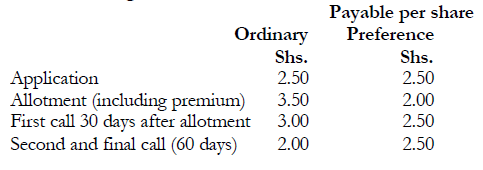

Kenya Caps Limited issued additional 100,000 ordinary shares and 50,000, 8% preference shares

on the following terms:

(Solved)

Kenya Caps Limited issued additional 100,000 ordinary shares and 50,000, 8% preference shares

on the following terms:

The par values were Sh.10 and Sh.9 for the ordinary and preference shares respectively. By 1

August 1993, applications had been received for 200,000 ordinary shares and 40,000 preference

shares. The directors rejected the application for 80,000 ordinary shares and refunded the

monies on 15 August 1993, and the remainder allotted five shares for every six shares applied

for. Surplus application monies were carried forward to allotment.

All allotment took place on 20 August 1993 and the due amounts were received by 31 August

1993. The first and second calls were received by the due dates except for 3,000 ordinary shares

which the directors declared forfeited on 20 November 1993. All the forfeited shares were

reissued as fully paid to another shareholder on 30 November 1993 for Sh.9 per share.

Assume that the number of shares outstanding prior to this additional issue amounted

to: Ordinary -300,000 shares of Sh.10 par

-50,000 7% preference shares of Sh.7 par

All these shares had been issued at par.

Required:

a) Journal entries including cash necessary to record the share transactions.

b) Prepare the share capital section of the Balance Sheet as at 31 December 1993.

c) What is the importance of issuing bonus shares?

Date posted:

November 21, 2018

.

Answers (1)

-

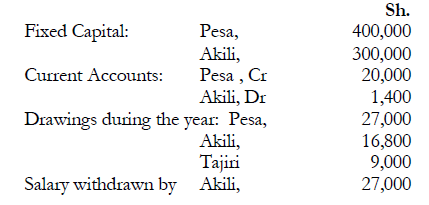

Pesa and Akili were in partnership preparing their accounts to 31 March and sharing profits and

losses in the ratio of 3:2 respectively. Interest was allowed...

(Solved)

Pesa and Akili were in partnership preparing their accounts to 31 March and sharing profits and

losses in the ratio of 3:2 respectively. Interest was allowed on fixed capital at 10% per annum.

Akili was entitled to a salary of Sh.3,000 per month. On 2 October 1995 the partners admitted

Tajiri a well known businessman into the partnership. On that day Tajiri introduced a Sum of

money which was equal to 50% of Pesa's fixed capital. The amount was credited to Tajiri's

capital account.

The new partnership agreement provided the following:

1) Interest on capital to be maintained at 10% per annum.

2) Tajiri is to receive a commission of 10% of the net profit before appropriations. This is due

to his business acumen.

3) Profits will be shared equally among the partners.

4) Akili is now entitled to a salary of Sh.3,500 per month.

The partners also agreed to guarantee Tajiri a minimum share of profit of Sh.62,000 per annum.

Any deficiency on that balance will be compensated by the other two partners in equal

proportions. For the purposes of admission of a partner, goodwill was valued at two years

purchase of average profits for the last three years. The profits for the years ended 31 March

1993, 1994 and 1995 were Sh.60,000, Sh.50,OOOand Sh.70,000 respectively. No goodwill

account is to be maintained in the books. Adjusting entries are to be made in the partners

current accounts. The net profit for the year ended 31 March 1996 was Sh.360,000. The profit

accrued evenly over the year.

The following are the partners balances on 1 April 1995:

Required:

a) Profit and Loss Appropriation Account for the year ended 31 March 1996.

b) Partners Current Accounts.

Date posted:

November 21, 2018

.

Answers (1)

-

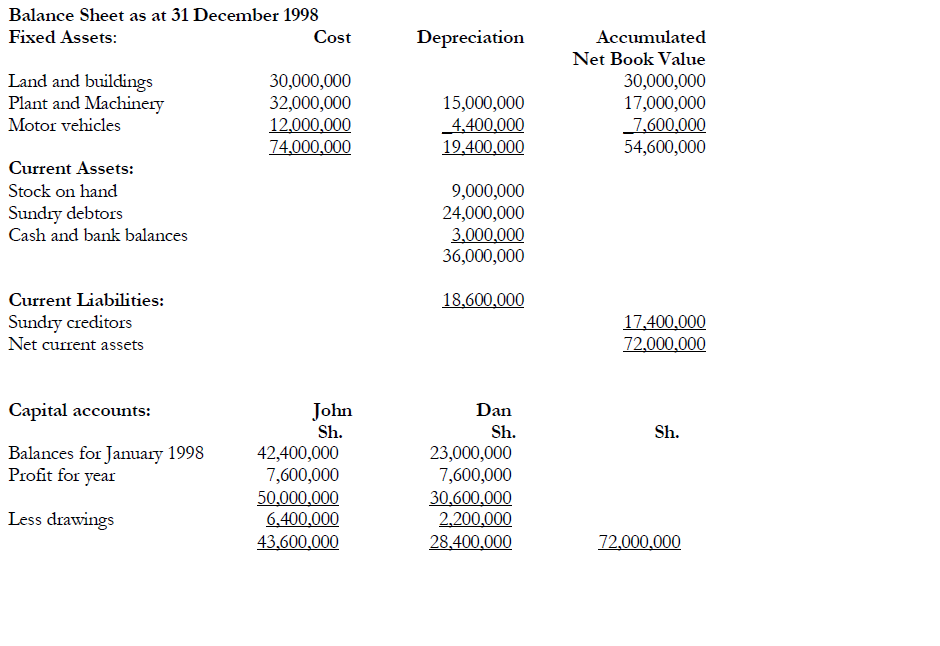

John and Dan are partners who run a wholesale shop. They share profits and losses equally. The accountant has provided a draft balance sheet as...

(Solved)

John and Dan are partners who run a wholesale shop. They share profits and losses equally. The accountant has provided a draft balance sheet as shown below:

From your examination of the books, you find that adjustments to the accounts are necessary in

respect of the following:

1) Sales included goods valued at Sh.700,000 which had been taken by Dan for his own

private use and debited to him in an account opened in the sales ledger. This is to be

treated as drawings.

2) The bills for electricity amounting to Sh.446,000 had not been paid.

3) A cheque for Sh.100,000 received from a debtor on 29 December 1998 had been put in the

drawer by the cashier and forgotten.

4) The amount for sundry debtors is shown net of a provision for doubtful debts of

Sh.600,000. The provision includes a bad debt of Sh.120,000. The revised provision for

doubtful debts was agreed at Sh.560,000.

5) A stock valued at Sh.3,300,000 was considered to have a net realizable value of

Sh.3,000,000. Some items of the stock for Sh.480,000 were not included in Sh.3,300,000.

6) Trade licenses for Sh.344,000 paid during the year had been charged to the profit and loss

account yet it will not expire until 31 March 1999.

7) Plant and machinery is considered to have a written down value of Sh.16,800,000.

8) During the year a building which cost Sh.5,800,000 was sold for Sh.5,600,000 and the

amount credited to freehold premises.

A cheque for Sh.406,000 received from a debtor and paid into the bank on 13 December 1998

had been returned on 31 December 1998 marked "refer to drawer". No entries were made in

the books of account.

Required:

a) A statement showing the correct adjustments and the adjusted profit for the year ended 31

December 1998.

b) A revised balance sheet as at 31 December 1998.

Date posted:

November 21, 2018

.

Answers (1)