-

Explain briefly the terms prime cost and factory cost as used by manufacturing firms

(Solved)

Explain briefly the terms prime cost and factory cost as used by manufacturing firms.

Date posted:

November 22, 2018

.

Answers (1)

-

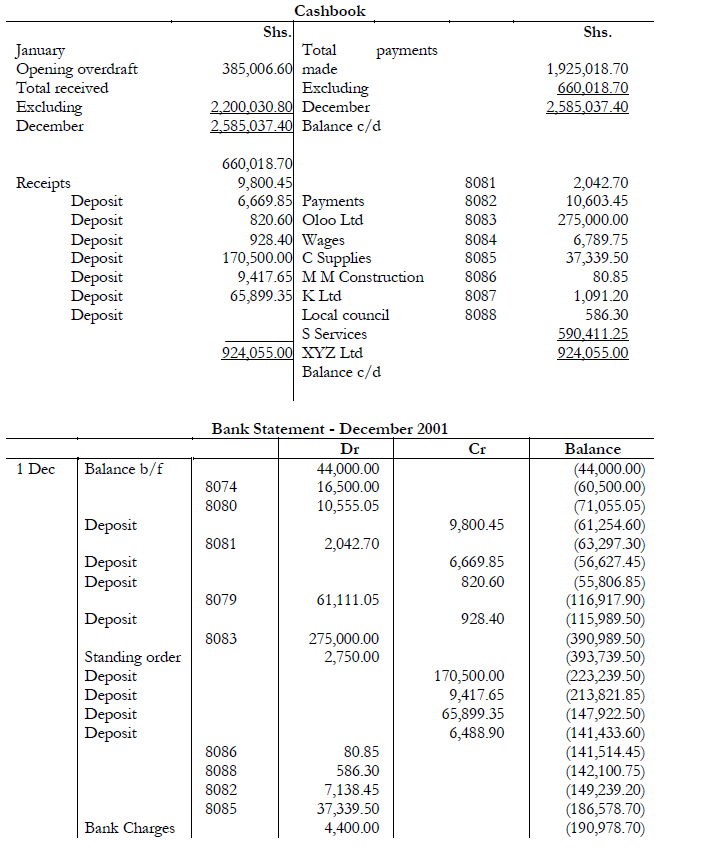

Sijui is having difficulty in preparing a bank reconciliation statement as at 31 December 2001.

He provides a summarized cashbook and a bank statement for the...

(Solved)

Sijui is having difficulty in preparing a bank reconciliation statement as at 31 December 2001.

He provides a summarized cashbook and a bank statement for the month of December as

shown below. Although the bank statement is correct his cashbook has several errors.

Required:

a) Prepare a corrected cashbook

b) A bank reconciliation as at 31 December and

c) A brief explanation as to the likely cause of the remaining difference.

Date posted:

November 21, 2018

.

Answers (1)

-

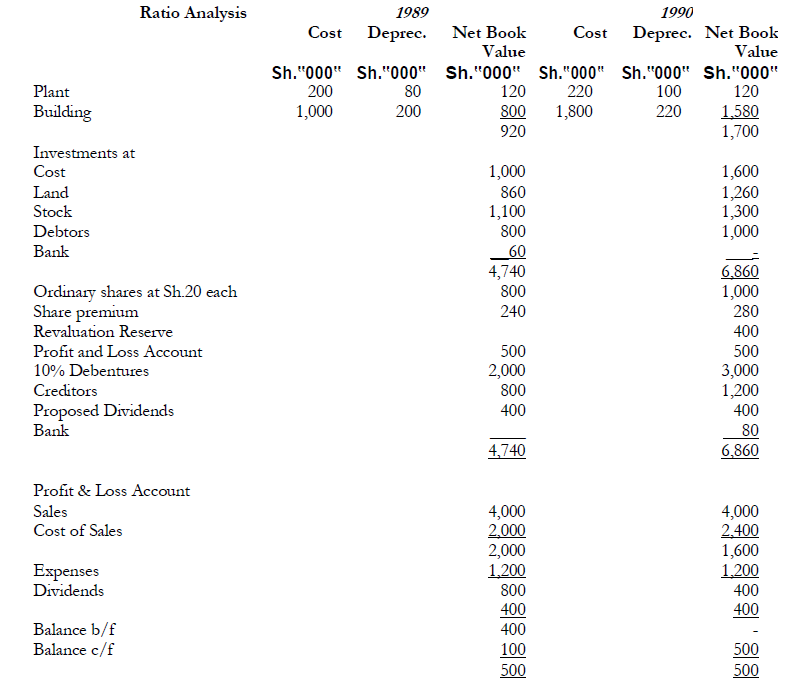

Calculate for Mvita Ltd. for 1989 and 1990 the following ratios:

Return on capital employed;

Debtors turnover;

Creditors turnover;

Current ratio;

Quick assets (acid test) ratio;

(Solved)

Calculate for Mvita Ltd. for 1989 and 1990 the following ratios:

Return on capital employed;

Debtors turnover;

Creditors turnover;

Current ratio;

Quick assets (acid test) ratio;

Gross profit percentage;

Net profit percentage;

Dividend cover;

Gearing ratio.

Using the summarised accounts given and ratios you have just prepared, comment on the

financial position and prospects of Mvita Ltd.

Date posted:

November 21, 2018

.

Answers (1)

-

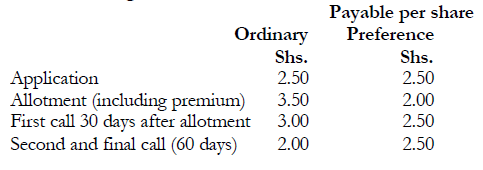

Kenya Caps Limited issued additional 100,000 ordinary shares and 50,000, 8% preference shares

on the following terms:

(Solved)

Kenya Caps Limited issued additional 100,000 ordinary shares and 50,000, 8% preference shares

on the following terms:

The par values were Sh.10 and Sh.9 for the ordinary and preference shares respectively. By 1

August 1993, applications had been received for 200,000 ordinary shares and 40,000 preference

shares. The directors rejected the application for 80,000 ordinary shares and refunded the

monies on 15 August 1993, and the remainder allotted five shares for every six shares applied

for. Surplus application monies were carried forward to allotment.

All allotment took place on 20 August 1993 and the due amounts were received by 31 August

1993. The first and second calls were received by the due dates except for 3,000 ordinary shares

which the directors declared forfeited on 20 November 1993. All the forfeited shares were

reissued as fully paid to another shareholder on 30 November 1993 for Sh.9 per share.

Assume that the number of shares outstanding prior to this additional issue amounted

to: Ordinary -300,000 shares of Sh.10 par

-50,000 7% preference shares of Sh.7 par

All these shares had been issued at par.

Required:

a) Journal entries including cash necessary to record the share transactions.

b) Prepare the share capital section of the Balance Sheet as at 31 December 1993.

c) What is the importance of issuing bonus shares?

Date posted:

November 21, 2018

.

Answers (1)

-

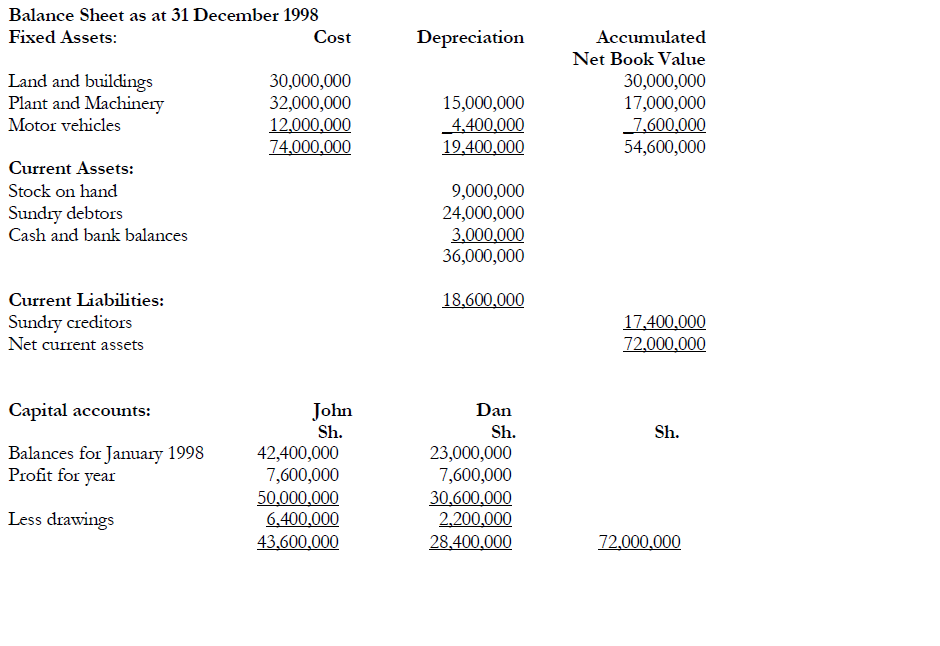

John and Dan are partners who run a wholesale shop. They share profits and losses equally. The accountant has provided a draft balance sheet as...

(Solved)

John and Dan are partners who run a wholesale shop. They share profits and losses equally. The accountant has provided a draft balance sheet as shown below:

From your examination of the books, you find that adjustments to the accounts are necessary in

respect of the following:

1) Sales included goods valued at Sh.700,000 which had been taken by Dan for his own

private use and debited to him in an account opened in the sales ledger. This is to be

treated as drawings.

2) The bills for electricity amounting to Sh.446,000 had not been paid.

3) A cheque for Sh.100,000 received from a debtor on 29 December 1998 had been put in the

drawer by the cashier and forgotten.

4) The amount for sundry debtors is shown net of a provision for doubtful debts of

Sh.600,000. The provision includes a bad debt of Sh.120,000. The revised provision for

doubtful debts was agreed at Sh.560,000.

5) A stock valued at Sh.3,300,000 was considered to have a net realizable value of

Sh.3,000,000. Some items of the stock for Sh.480,000 were not included in Sh.3,300,000.

6) Trade licenses for Sh.344,000 paid during the year had been charged to the profit and loss

account yet it will not expire until 31 March 1999.

7) Plant and machinery is considered to have a written down value of Sh.16,800,000.

8) During the year a building which cost Sh.5,800,000 was sold for Sh.5,600,000 and the

amount credited to freehold premises.

A cheque for Sh.406,000 received from a debtor and paid into the bank on 13 December 1998

had been returned on 31 December 1998 marked "refer to drawer". No entries were made in

the books of account.

Required:

a) A statement showing the correct adjustments and the adjusted profit for the year ended 31

December 1998.

b) A revised balance sheet as at 31 December 1998.

Date posted:

November 21, 2018

.

Answers (1)

-

The term "reserves" is frequently found in company balance sheets

Required:

(i) Explain the meaning of „reserves? in this context;

(ii) Give two examples of reserves and explain...

(Solved)

The term "reserves" is frequently found in company balance sheets

Required:

(i) Explain the meaning of „reserves‟ in this context;

(ii) Give two examples of reserves and explain how each of your examples comes into existence.

Date posted:

November 21, 2018

.

Answers (1)

-

List and briefly explain three ways in which the use of historical cost accounting may cause financial statements to be misleading.

(Solved)

List and briefly explain three ways in which the use of historical cost accounting may cause financial statements to be misleading.

Date posted:

November 21, 2018

.

Answers (1)

-

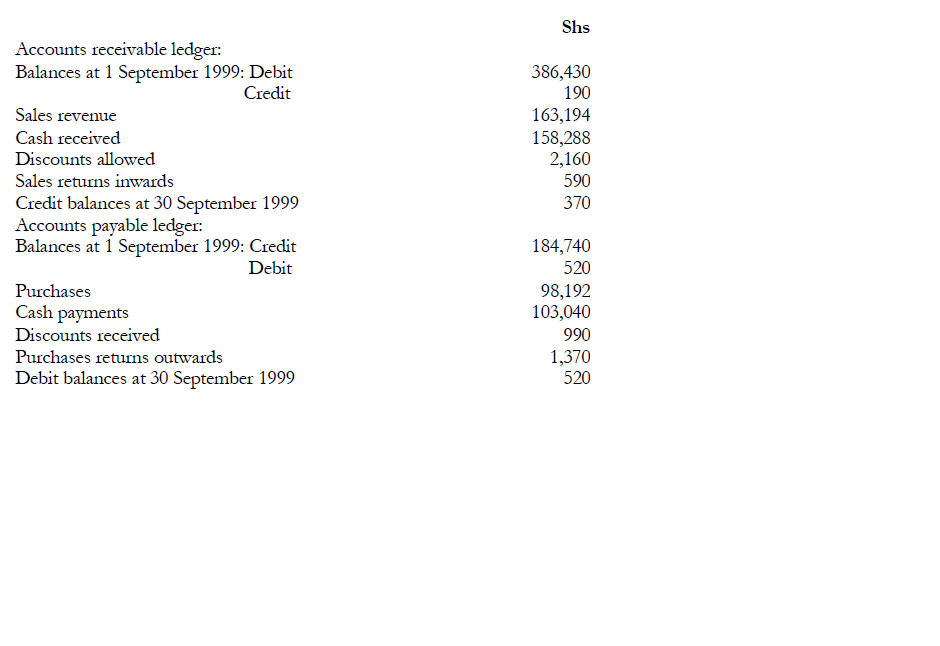

Otter, a limited liability company, operates a computerised accounting system for its accounts

receivable and accounts payable ledgers. The control accounts for the month of September...

(Solved)

Otter, a limited liability company, operates a computerised accounting system for its accounts

receivable and accounts payable ledgers. The control accounts for the month of September 1999

are in balance and incorporate the following totals:

Although the control accounts agree with the underlying ledgers, a number of errors have been

found, and there are also several adjustments to be made. These errors and adjustments are

detailed below:

(1) Four sales invoices totalling Shs 1,386 have been omitted from the records;

(2) A cash refund of Shs 350 paid to a customer, A Smith, was mistakenly treated as a

payment to a supplier with the same name;

(3) A contra settlement offsetting a balance of Shs 870 due to a supplier against the

accounts receivable ledger account for the same company is to be made;

(4) Bad debts totalling Shs1,360 are to be written off;

(5) During the month, settlement was reached with a supplier over a disputed account. As a

result, the supplier issued a credit note for Shs 2,000 on September 26. No entry has yet

been made for this;

(6) A purchases invoice for Shs 1,395 was keyed in as Shs 1,359;

(7) A payment of Shs 2,130 to a supplier, B Jones, was mistakenly entered to the account

of R Jones;

(8) A debit balance of Shs 420 existed in the accounts payable ledger at the end of August

1999. The supplier concerned cannot now be traced and it has been decided to write off

this balance.

Required:

Prepare the accounts receivable and accounts payable ledger control accounts as they should

appear after allowing, where necessary, for the errors and adjustments listed.

Date posted:

November 20, 2018

.

Answers (1)

-

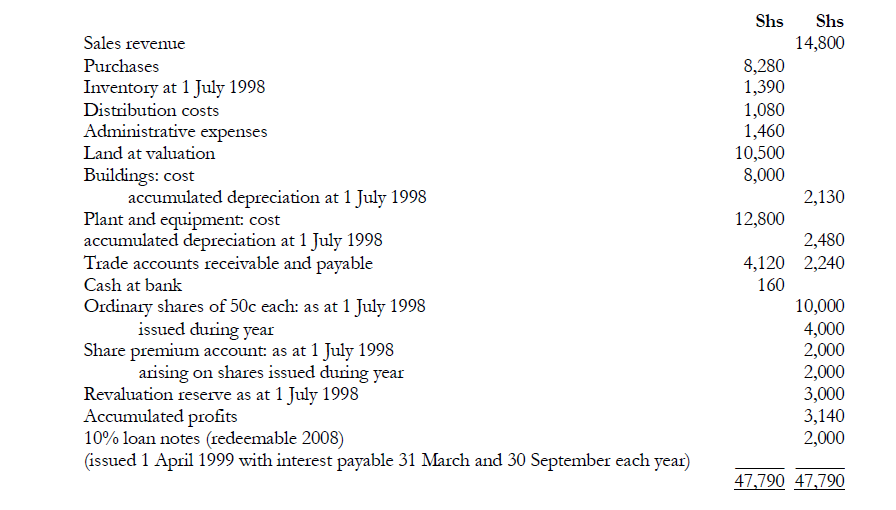

Atok, a limited liability company, compiles its financial statements to 30 June manually. At 30 June 1999, the company's list of account balances was as...

(Solved)

Atok, a limited liability company, compiles its financial statements to 30 June annually. At 30

June 1999, the company's list of account balances was as follows:

The following matters remain to be adjusted for in preparing the financial statements for

the year ended 30 June 1999:

(1) Inventory at 30 June 1999 amounted to Shs 1,560,000 at cost. A review of

inventory items revealed the need for some adjustments for two inventory lines:

(i) Items which had cost Shs 80,000 and which would normally sell for Shs 120,000

were found to have deteriorated. Remedial work costing Shs 20,000 would be needed

to enable the items to be sold for Shs 90,000.

(ii) Some items sent to customers on sale or return terms had been omitted from inventory

and included as sales in June 1999. The cost of these items was Shs 16,000 and they

were included in sales at Shs 24,000. In July 1999, the items were returned in good

condition by the customers.

(2) Depreciation is to be provided as follows:

Buildings: 2% per year on cost.

Plant and equipment: 20% per year on cost.

80% of the depreciation is to be charged in cost of sales, and

10% each in distribution costs and administrative expenses.

(3) The land is to be revalued to Shs 12,000,000. No change was required to the value

of the buildings.

(4) Accrued expenses and prepayments were:

(5) No dividends were paid during the year and no dividend is proposed for the year.

Required:

(a) Prepare the company's income statement for the year ended 30 June 1999 and balance

sheet as at that date for publication, complying as far as possible with the provisions of IAS1

Presentation of Financial Statements and other relevant International Accounting Standards.

(b) Prepare the statement of changes in equity as presented in IAS1. Notes to the financial

statements are not required.

Date posted:

November 20, 2018

.

Answers (1)

-

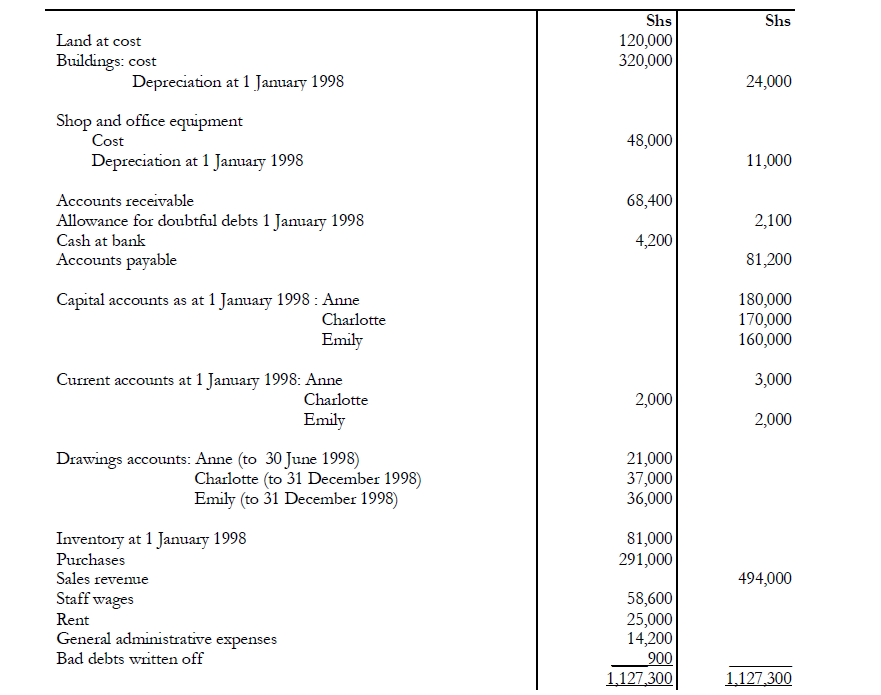

Anne, Charlotte and Emily have been in partnership for some years, sharing profits in the ratio

50.30.20 and preparing their financial statements to 31 December each...

(Solved)

Anne, Charlotte and Emily have been in partnership for some years, sharing profits in the ratio

50.30.20 and preparing their financial statements to 31 December each year.

On 30 June 1998 Anne retired and Charlotte and Emily decided to continue the partnership

sharing profits equally.

The partnership list of account balances at 31 December 1998, before making any adjustments

for Anne's retirement or for the asset revaluation was as follows.

Notes

(1) Profits are to be assumed to accrue equally in the periods before and after

Anne's retirement

(2) The balance due to Anne is to remain in the partnership from 1 July 1998 as a loan

carrying no interest until 1 January

(3) The value of the partnership goodwill at 30 June 1998 was agreed by all three partners at

Shs 200,000. Goodwill is not to appear in the balance sheet after the adjustments

necessary at 30 June 1998.

(4) It was decided, as part of the process of valuing Anne's share of the

partnership, to revalue the land at 30 June from Shs 120,000 to Shs 160,000. The

increased value is to be included in the balance sheet.

(5) The inventory at 31 December 1998 was Shs 90,000

(6) Accruals and prepayments at 31 December 1998 were:

Rent paid in advance to 31 March 1999 Shs 5,000

General administrative expenses:

Prepayments Shs 1,800

Accruals Shs 6,200

(7) The allowance for doubtful debts is to be increased to Shs 2,400

(8) Depreciation is to be provided as follows:

Buildings 2 % per annum straight line

Shop and office equipment 15 % per annum straight line

Required:

(a) Prepare the income statement and a statement showing the division of the profit for the

year ended 31 December 1998 and balance sheet as at that date;

(b) Show the partners' capital and current accounts for the year Anne‟s loan account

Date posted:

November 20, 2018

.

Answers (1)

-

After preparation of the trial balance or Bakari Brothers Enterprises as at 31 September 2005, the firm's accountant has been provided with the following additional...

(Solved)

After preparation of the trial balance or Bakari Brothers Enterprises as at 31 September 2005, the firm's accountant has been provided with the following additional information for the purpose of preparation of the final accounts:

1 Due to an oversight, discount has been allowed to a credit customer on the gross `

invoiced amount of Sh.80,000 at the rate 10%. The firm should have used a rate if 6%.

2 Electricity accrued amounts to Sh.36,710 while insurance premiums of Sh. 22,450 have

been prepaid.

3 In October 2005, the employees of the firm received a general salary increase,

backdated to 1 July 2005. Amounts totaling Sh.126,550 in salary arrears are payable to

former employees who left shortly before the salary award was announced and who

have not yet been traced. It has been decided that the salary packets will be opened and

the cash banked until the ex-employees are traced.

4 Wages due to casuals amounting to Sh. 464,120 for services rendered in the last week of

December 2005 were paid in January 2006 together with the salaries for the month of

December 2005 which amounted to Sh.301,700.

5 During the year, the exterior of the warehouse was repaired and repainted at a cost of

Sh.500,000. This"

amount was erroneously debited to office premises account. It is policy of Bakari

Brothers Enterprises to provide for depreciation on the closing balances of non-current

assets and this has already been done. The annual rate of depreciation on office

premises is 2% calculated on the straight-line basis.

6 In December 2005 2005, Bakari Brothers Enterprises had bought goods on credit from

CB Ltd. for Sh. 452,100 and has also sold goods on credit to the same company for

Sh.163,040. These amounts were correctly posted to their respective accounts.

However, these accounts are to be offset as at 31 December 2005 and the remaining

balance settled by cheque in January 2006.

7 The provision for discounts allowed to debtors, which at present has a balance of

Sh.229,530 needs to be reduced to Sh. 157,400.

8 Debts totaling Sh.64,800 are irrecoverable and should be written off. However, amount

of Sh.21,440

written off as a bad debt in the previous year has now been recovered in full but the

cheque in settlement has not been banked or posted in the accounts.

Required:

Journal entries, including narrations, necessary to record the above transactions in the books of

Bakari Bothers Enterprises.

Date posted:

November 20, 2018

.

Answers (1)

-

Outline the extent to which a trial balance is an indicator of correct book-keeping by an entity

(Solved)

Outline the extent to which a trial balance is an indicator of correct book-keeping by an entity.

Date posted:

November 20, 2018

.

Answers (1)

-

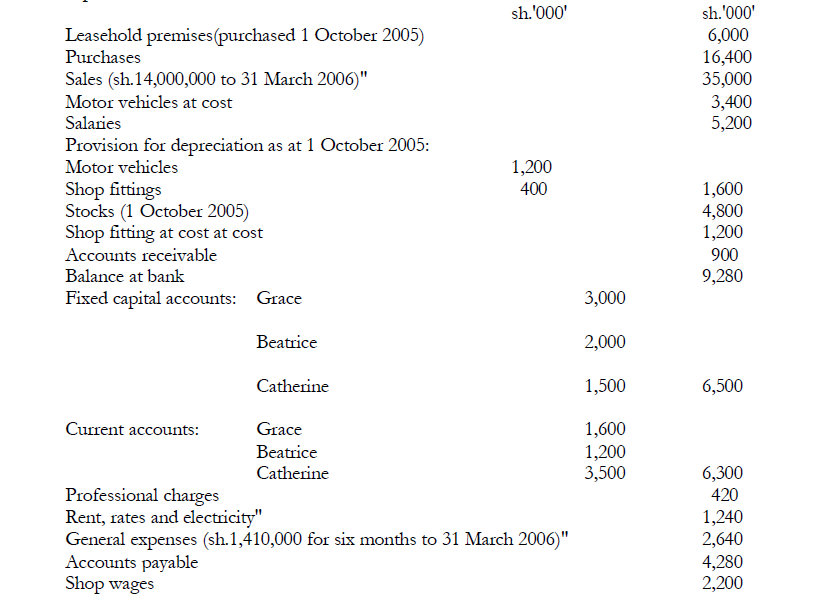

Grace and Beatrice were operating a retail business sharing profits and losses in the ratio of 2:1

respectively up to 31 March 2006 when they admitted...

(Solved)

Grace and Beatrice were operating a retail business sharing profits and losses in the ratio of 2:1

respectively up to 31 March 2006 when they admitted Catherine to the partnership. The partners

allowed payment of interest on partners' fixed capital accounts but did not allow for interest on

partners' current accounts.

The following balances were extracted from the partnership's book of account as at 30 September 2006:

Additional information:

1. On 31 March 2006 when Catherine was admitted as a partner, the profit sharing ratio

changed to Grace 2/5, Beatrice 2/5 and Catherine 1/5. For the purpose of admission,

goodwill was valued at Sh. 12,000,000 and was written off the books immediately. On 1

April 2006, Catherine paid Sh.5,000,000 which comprised her fixed capital of

sh.1,500,000 and her current account contribution of sh.3,500,000."

2. The partners also agreed that any apportionment of gross profit was to be made on the

basis of sales. The apportionment of expenses, unless otherwise indicated, were to be

on time basis.

3. On 30 September 2006, stock was valued at Sh.5,100,000.

4. Provision was to be made for depreciation on motor vehicles and shop fittings at the

rate of 20% and 5% per annum respectively, based on cost.

5 Salaries included the following partners drawings during the year:

Grace - Sh.600,000

Beatrice - Sh.480,000

Catherine - "Sh.250,000"

6 At 30 September 2006, rates paid in advance amounted to sh.260,000 while electricity

accrued amounted to sh.60,000.

7 A difference in the books of sh.120,000 that had been written off to general expenses as

at 30 September 2006 was later found to have been due to the following errors:

- Sales returns of sh.180,000 had been debited to sales but was omitted from the

- customers account.

- The purchase journal had been undercast by sh.200,000.

8 Doubtful debts (for which full provision was required) as at 31 March 2006 amounted

to Sh.120,000 and sh.160,000 as at 30 September 2006.

9 Professional charges included sh.200,000 paid in respect to the acquisition of leasehold

premises. These fees are to be capitalized as part of the lease, the total cost of which was

to be depreciated in 25 equal annual installments. Other premises owned by Beatrice

were leased to the partnership at Sh. 600,000 per annum but no rent had been paid or

credited to her for the year to 30 September 2006.

Required:

(a) Income statement for the year ended 30 September

2006.

(b) Balance sheet as at 30 September 2006.

(c ) Partners' current accounts.

Date posted:

November 20, 2018

.

Answers (1)

-

State any two circumstances that may hinder a firm from improving on the usefulness of its financial statements

(Solved)

State any two circumstances that may hinder a firm from improving on the usefulness of its financial statements.

Date posted:

November 20, 2018

.

Answers (1)

-

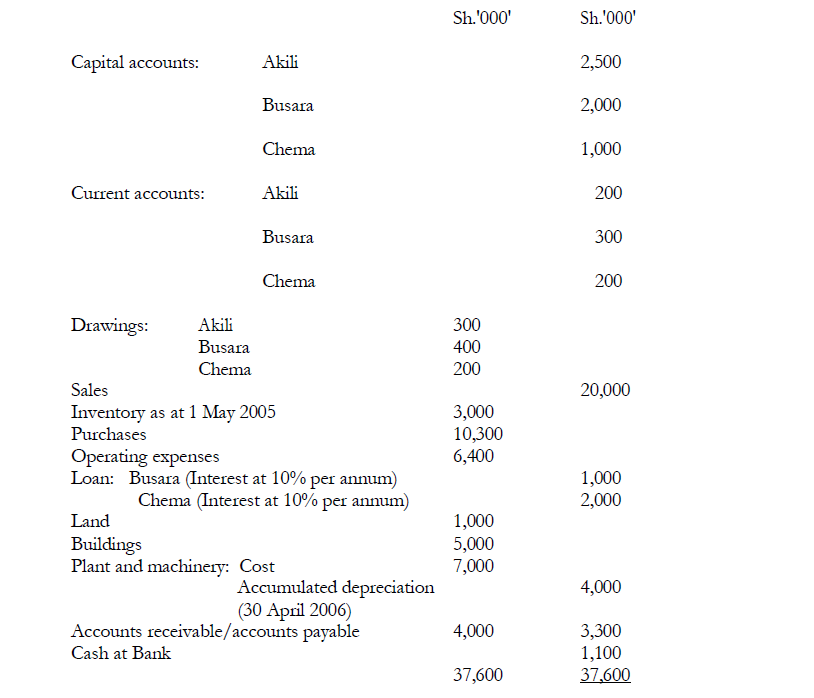

Akili, Busara and Chema are in partnership sharing profits sharing profits and losses equally after allowing for interest on capital at 5% per annum to...

(Solved)

Akili, Busara and Chema are in partnership sharing profits sharing profits and losses equally after allowing for interest on capital at 5% per annum to the partners and a salary to Busara of Sh.20,000 per month.

The trial balance of the partnership as at 30 April 2006 was as follows:

Additional Information

1. Closing inventory as at 30 April was valued at sh.2,400,000.

2. Interest on loans had not been paid.

3. Sales include credit sales of Sh.600,000 in respect of two items sold on the basis of

confirmation by the customers. The items had cost Sh.100,000 each. As at 30 April

2006, the customers had not confirmed whether they would buy the goods.

4. On 1 November 2005, the terms of th epartnership agreement were changed. The new

terms provided for:

- Profit sharing ratio of 5:3:2 for Askili, Busara and Chema respectively.

- Interest on capital at 5% per annum.

- Salaries of Sh.10,000 per month to Busara and Chema.

For the purpose of the change, goodwill was valued at Sh.1,200,000 and was to be written

off immediately while the land buildings were valued at Sh.2,000,000 and Sh.6,400,000

respectively.

Required:

a) Trading, Profit and loss and appropriation accounts for the year ended 30 April 2006

b) Partners' capital and current accounts

c) Balance sheet as at 30 April 2006

Date posted:

November 20, 2018

.

Answers (1)

-

Briefly explain why goodwill should be paid under the following circumstances: (i) By a partner on admission to a partnership. (ii) To a partner on...

(Solved)

Briefly explain why goodwill should be paid under the following circumstances: (i) By a partner on admission to a partnership. (ii) To a partner on retirement from a partnership

Date posted:

November 20, 2018

.

Answers (1)

-

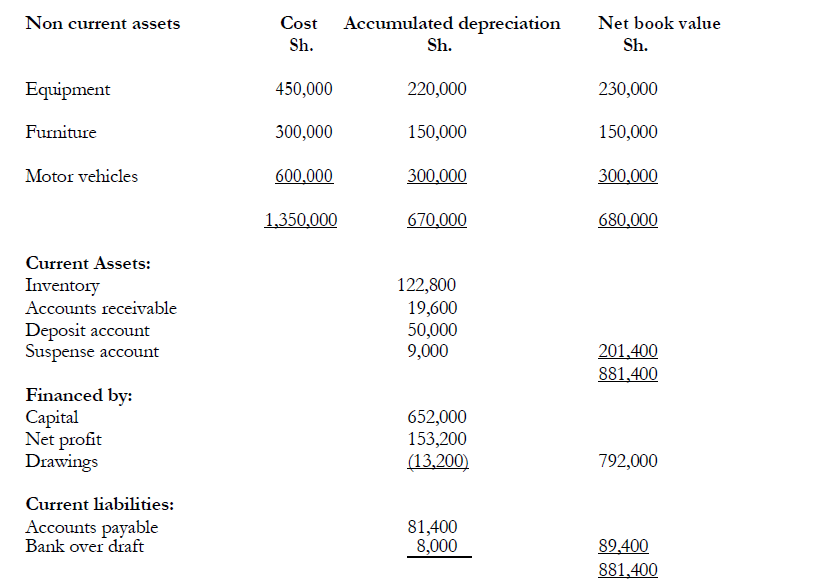

Ben Mogaka prepared the following draft balance sheet for BM Enterprises as at 31 December 2005

(Solved)

Ben Mogaka prepared the following draft balance sheet for BM Enterprises as at 31 December 2005:

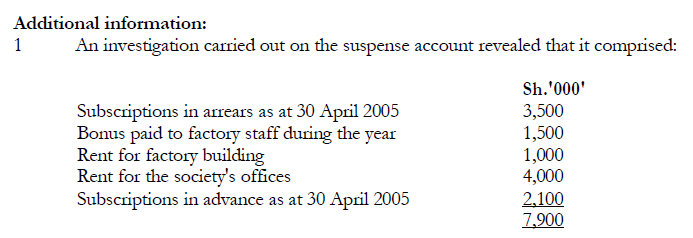

Additional information:

On further investigation, the suspense account was discovered to have resulted from the

following errors:

1. The sales of goods on credit to Alex Otis amounting to Sh.19,000 had been recorded in

the sales journal as sh.9,000.

2. A receipt of Sh.20,000 from sale of an item of equipment had been credited to sales

account. The equipment was shown in the books of account at costs of account of

Sh.90,000 and accumulated depreciation of Sh.72,000.

3. A credit note from a supplier, Simon Masound for Sh.15,000 had been omitted from the

books.

4. A bank overdraft for Sh.7,000 reflected in the cash book as at 31 December 2005 was

omitted In the trial balance.

5. A payment of Sh. 9,700 to Tom Wambugu, a creditor, was correctly entered in the cahs

book but posted to his personal account as Sh.7,900.

6. The debit side of rent expense account had been undercast by Sh.1,000.

7. A provision of Sh.2,000 for sundry expenses outstanding as at 31 December 2004 and

debited to sundry expenses at that dated had not been brought forward to the credit of

the account in the following period. No credit entry had been made in any other

account in respect to this account in respect to this item.

8. Discount received from the supplier of Sh.8,200 had been entered on the wrong side of

purchases ledger control account.

9. On 31 December, goods valued at Sh.9,600 (selling price) were returned by Jane Kerubo

(a debtor). No entry had been made in the books to reflect this transaction. These goods

were not included in the closing stock.

10. Discounts allowed were overcast by Sh.1,200.

Required:

(a) Journal entries to correct the above errors (Narration not required)

(b) Suspense account.

(c) Statement of corrected net profit for the year ended 31 December 2005

(d) Corrected balance sheet as 31 December 2005.

Date posted:

November 20, 2018

.

Answers (1)

-

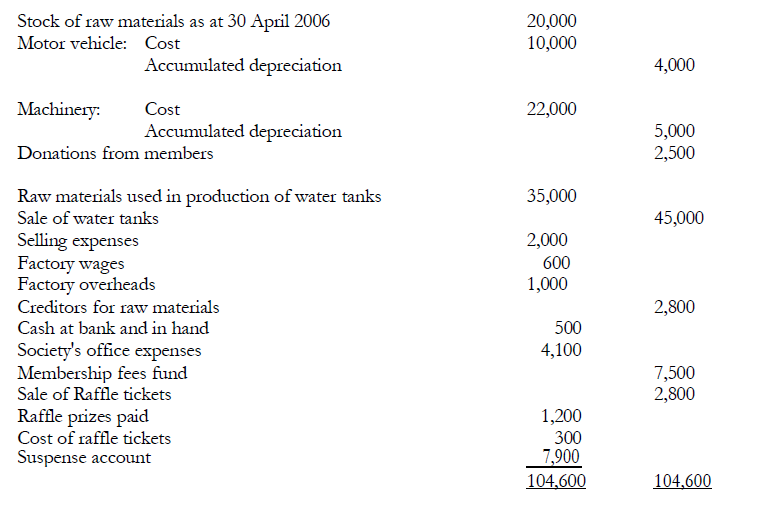

Umoja Women's Welfare Society sells water tanks at subsidised prices to its members and the

general public. The members' contributions are used to meet the cost...

(Solved)

Umoja Women's Welfare Society sells water tanks at subsidised prices to its members and the

general public. The members' contributions are used to meet the cost of manufacturing the

water tanks.

The trial balance extracted from the books of account of the society as at 30 April 2006 was as

follows:

2 Annual subscriptions in arrears as at 30 April 2006 amounted to Sh.2,000,000 while

subscriptions received in advance as at 30 April 2006 amounted to sh.1,500,000.

3 The membership fee is levied every ten years. The membership fees attributable to the

year ended 30 April 2006 amounted to sh.800,000

4 Accrued society's office expenses as at 30 April 2006 amounted Sh.400,000.

5 The motor vehicle usage should be apportioned to the factory and society's offices at

80% and 20% respectively. Depreciation should be provided on cost at 5% per annum

on machinery and 10% per annum on motor vehicles.

Required:

(a) Water tanks trading and profit and loss account for the year ended 30 April 2006

(b) Income and expenditure account for the year ended 30 April 2006

(c) Balance sheet as at 30 April 2006.

Date posted:

November 19, 2018

.

Answers (1)

-

Give five purposes of control accounts

(Solved)

Give five purposes of control accounts.

Date posted:

November 19, 2018

.

Answers (1)

-

While research and development costs of a project may meet the definition of an asset, the cost may not meet the criteria used in recognizing...

(Solved)

While research and development costs of a project may meet the definition of an asset, the cost may not meet the criteria used in recognizing an asset.

Define the term “asset” and explain the criteria used in recognizing an asset.

Date posted:

November 19, 2018

.

Answers (1)