(a) Fundamental accounting concepts

These are the broad basic assumptions which underline the periodic financial accounts of

business enterprises. At present four fundamental accounting concepts are generally recognized;

(I) The Going Concern or Continuity Assumption

In accounting for an accounting entity, it is to be assumed that the accounting entity will

continue in operation for the foreseeable future. It is assumed that the accounting entity has

neither the intention nor the necessity of liquidation or of curtailing materiality the scale of

its operations. The assumptions provide the foundation for accrual accounting. When the

accounting entity ceases to be a going concern, the accounting approach changes from

accrual to realization and liquidation.

(II) Accrual / Matching Concept

This simply means that revenue should be matched against the expenses. The incurred in

the year in which they were incurred. This is shown when treating prepayment and accruals.

Accruals at the end of the year relating to expenses or income are added while prepayments

are deducted.

Under the basis, the effects of transactions and other events are recognized when this

occur (and not as cash or its equivalent is received or paid) and they are recorded in the

accounting records and reported in the financial statements or the periods which they relate.

Financial statements prepared on the accrued basis inform users not only of past

transactions involving the payment and receipt of cash but also of obligations to pay cash in

the future and resources that represent cash to be received in future.

(III) Consistency Concept

The accounting treatment of like items should be consistent e.g. in the application of the

particular method of depreciation lets say straight line method then it should be applied

consistently.

(IV) Prudence Concept

Uncertainties inevitably surround many transactions and revenue and profit, should not be

anticipated but recognized only when they are realized in the form of cash or other assets

which can be treated as cash.

Prudence is the inclusion of a degree of caution in the exercise of the judgments needed in

making the estimates required under conditions of uncertainty, such that assets or incomes

are not overstated and liabilities or expenses are not overstated.

(b) Accounting Bases

Extending from the four fundamental concepts are many other principles which are known as

accounting bases. They are defined in statement as the methods developed for applying

fundamental accounting concepts to financial transactions and items. For example;

- Stock Valuation

- Depreciation bases

(c) Accounting Policies

These are the specific accounting bases selected and consistently followed by a business

enterprise as being appropriate to its circumstances.

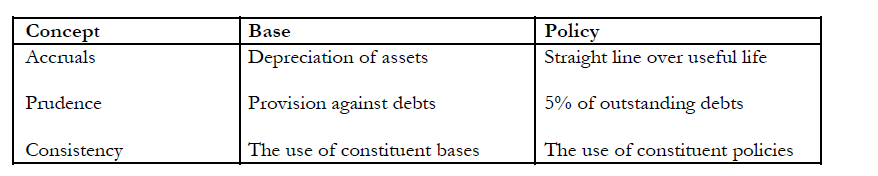

The following summary is fundamental for easy understanding.

Mutiso answered the question on

November 25, 2018 at 13:49