-

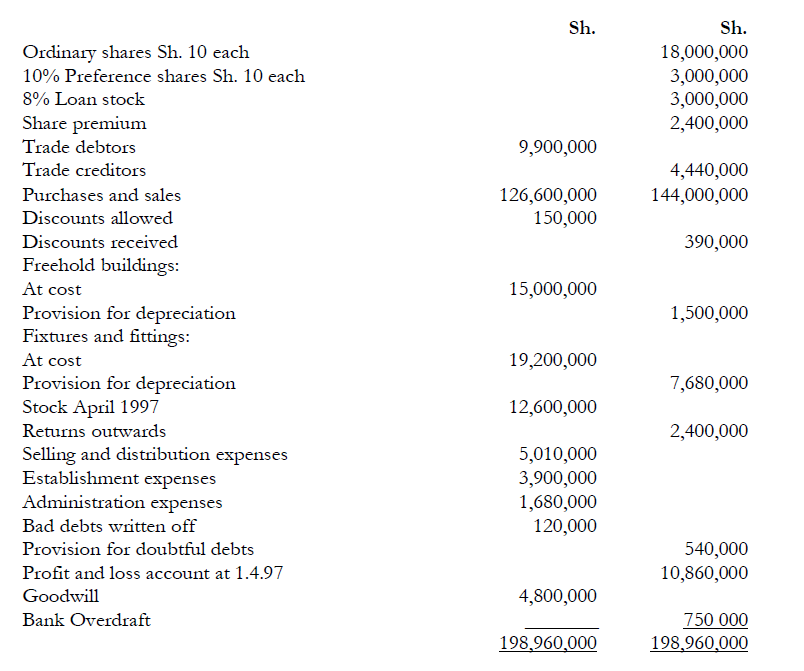

The following trial balance was extracted from the books of Mapema Traders Ltd. as at 31 March 1998:

(Solved)

The following trial balance was extracted from the books of Mapema Traders Ltd. as at 31 March 1998:

Additional information:

1. The debtors balance includes Sh.600,000 due from Otieno who has now been

declared bankrupt and it has been decided to write-off this debt as a bad debt.

2. The provision for doubtful debts is to be adjusted to 5 % of trade debtors at

31 March 1998.

3. Establishment expenses prepaid at 31 March 1998 amount to Sh.

120,000. The difference is to be written off during the year.

4. Administration expenses accrued due at 31 March 1998 amounted to Sh.210,000.

5. The company paid the interest on the loan stock for the year ended 31

March 1998 on 28 May 1998.

6. Gross profit is at the rate of 20% of sales.

7. Depreciation is provided annually on the cost of fixed assets held at the end of

the year at the following rates:

Freehold buildings 2 %

Fixtures and fittings 10%

8. The company's directors propose that the preference share dividend be paid, a

dividend of 10% on the ordinary shares to be paid and to transfer an amount of

Sh.7,500,000 to General Reserve.

Required:

The trading and profit and loss account for the year ended 31 March 1998 of Mapema Traders

Ltd. and a balance sheet as at that date.

Date posted:

November 26, 2018

.

Answers (1)

-

Write explanatory notes on the following accounting concepts:

(a) Materiality;

(b) Prudence;

(c) Consistency.

(Solved)

Write explanatory notes on the following accounting concepts:

(a) Materiality;

(b) Prudence;

(c) Consistency.

Date posted:

November 26, 2018

.

Answers (1)

-

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4, 536,000.

On...

(Solved)

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4, 536,000.

On 3 April 1995, the company bought its second lorry, KA 735 for Sh.2, 740,000.

On 3 June 1997, the first lorry, KA 620 was involved in an accident and was completely written

off. The insurance company paid the transport company Sh.1, 350,000 for the loss. On 5

January 1998, the company bought its third lorry, KB 327 for Sh.3, 780,000. Depreciation on

the lorries was provided at 10 per cent on straight -line basis. The policy of the company is to

provide depreciation for the full year for all acquisitions made at any time during the year and to

ignore depreciation on any lorry sold or disposed of during the year. All the lorries are insured.

The company makes its accounts annually to 31 December.

In 1998, the company decided to change its depreciation rate from 10 to 15 per cent on straight

line basis for all its lorries still in use retroactively, that is from year of purchase. An adjusting

entry will be made in the accounts for the year 1998.

Required:

1. The motor lorries account for years 1994 to 1998.

2. A schedule of additional depreciation arising from change of depreciation rate, for years

1994 to 1997.

3. Provision for depreciation account for the same period.

4. Disposal of motor lorries account.

Date posted:

November 26, 2018

.

Answers (1)

-

The cashbook column of Tatua Traders Company Ltd. had an overdraft of Sh.532, 400 as at 31

October 1998, which did not agree with balance as...

(Solved)

The cashbook column of Tatua Traders Company Ltd. had an overdraft of Sh.532, 400 as at 31

October 1998, which did not agree with balance as per bank statement of the same date.

On checking through the relevant records and documents, some details were established as

shown below:

1. Bank charges and interest on overdraft as per the bank statement amounted to Sh. 12,450

and Sh. 135,480 respectively.

2. A debtor deposited Sh.254, 500 to the bank direct.

3. Insurance premium of the mortgaged property amounting to Sh.35, 485 was paid direct

by the bank.

4. Standing orders of Sh. 138,000 have been effected by the bank.

5. Cheques for Sh.354, 890 which were banked on 29 October 1998 were credited by the

bank on 5 November 1998.

6. Cheques drawn by the company amounting to Sh.745, 964 had not been presented for

payment as at 31 October 1998.

7. A cheque for Sh.74, 500 was debited by the bank as Sh.47, 500.

8. The payments side of the cashbook was undercast by Sh.32, 000.

9. The bank had debited the account with another customer's cheque of Sh.27, 500 but had

not yet corrected the mistake on 31 October 1998.

Required:

(a) Make adjustments in the cash book and show the adjusted cash book balance.

(b) A bank reconciliation statement as at 31 October 1998.

Date posted:

November 26, 2018

.

Answers (1)

-

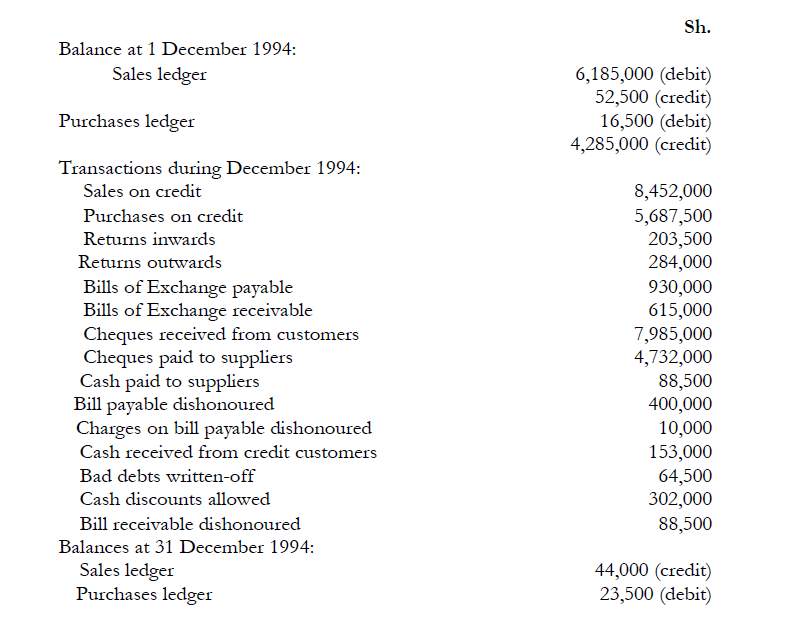

XML Ltd. maintains control accounts in its business records. The balances and transactions relating to the company's control accounts for the month of December 1994...

(Solved)

XML Ltd. maintains control accounts in its business records. The balances and transactions relating to the company's control accounts for the month of December 1994 are listed below:

Required:

Post the sales ledger and the purchases ledger control accounts for the month of December

1994 and derive the respective debit and credit closing balances on 31 December 1994.

Date posted:

November 26, 2018

.

Answers (1)

-

Explain the purposes for which control accounts are prepared in a business organisation

(Solved)

Explain the purposes for which control accounts are prepared in a business organisation.

Date posted:

November 26, 2018

.

Answers (1)

-

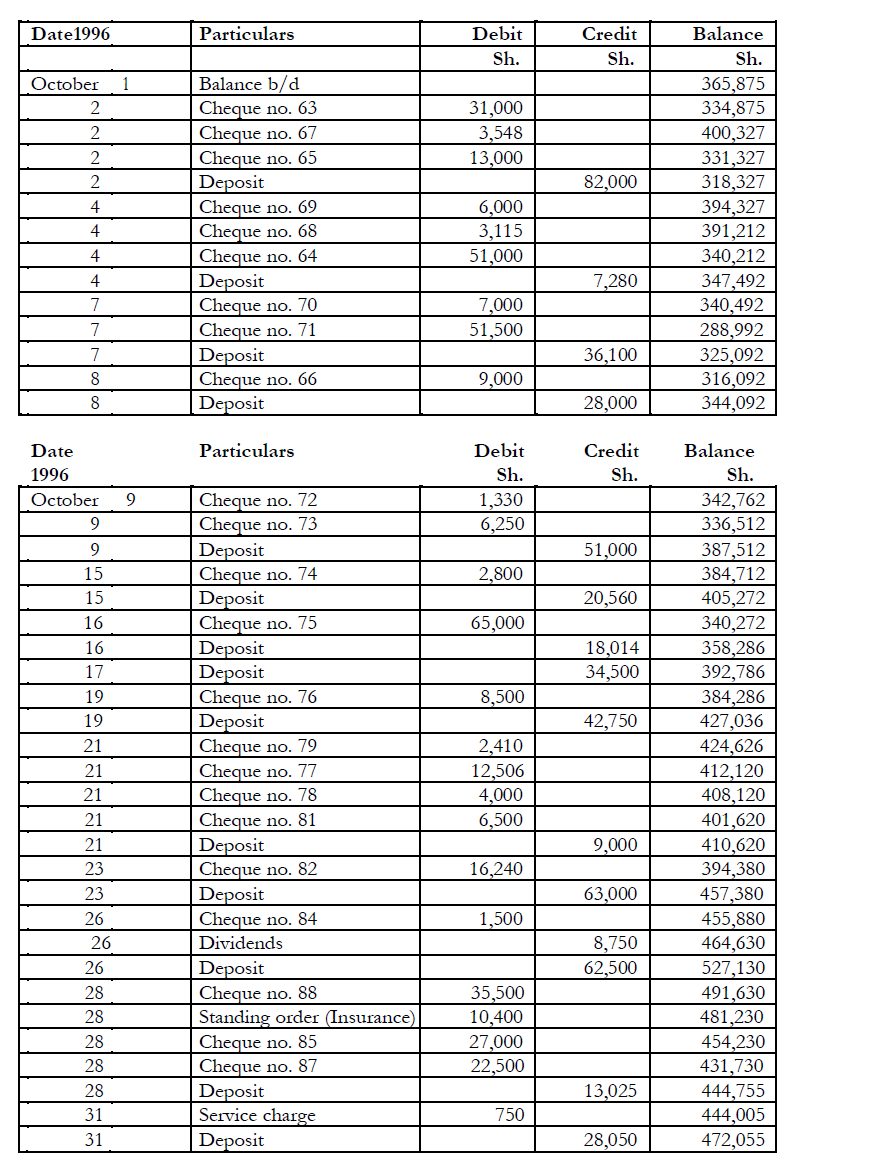

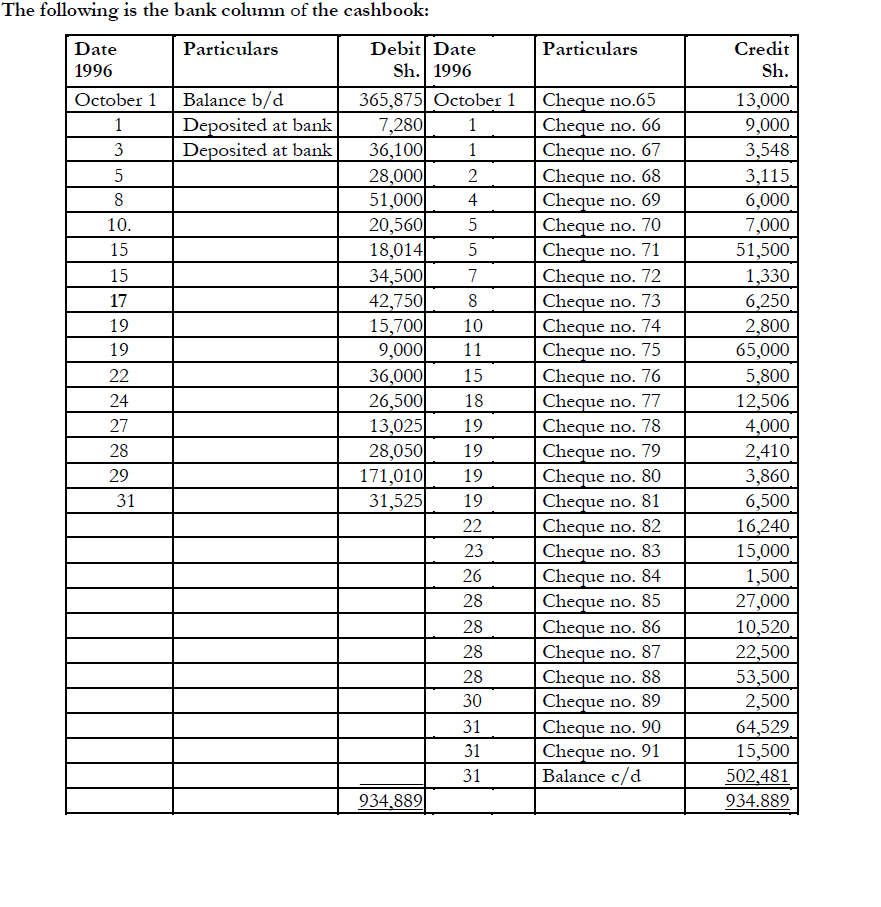

The following is the bank statement of Kakamega Retail Traders for the month of October 1996:

(Solved)

The following is the bank statement of Kakamega Retail Traders for the month of October 1996:

Notes:

1. The bank reconciliation on 30 September 1996 showed that one deposit was in transit and

two cheques had not yet been presented to the bank.

2. Deposits of Sh.62, 500 and Sh.36, 000 had been entered in the cash book as Sh.26,500

and Sh.36,000 and in the bank statement as Sh.62,500 and Sh.63,000, respectively.

3. A cheque from Mkulima for Sh.15,700 was deposited on 18 October 1996 but

was dishonoured and the advice was received on 4 November 1996.

4. Counterfoils for cheques no. 76 and no. 88 showed they had been drawn for Sh.5,800 and

Sh.35,500 respectively.

Required:

(a) A correct cashbook balance.

(b) A bank reconciliation statement on 31 October 1996.

Date posted:

November 25, 2018

.

Answers (1)

-

What is the purpose of preparing a bank reconciliation statement?

(Solved)

What is the purpose of preparing a bank reconciliation statement?

Date posted:

November 25, 2018

.

Answers (1)

-

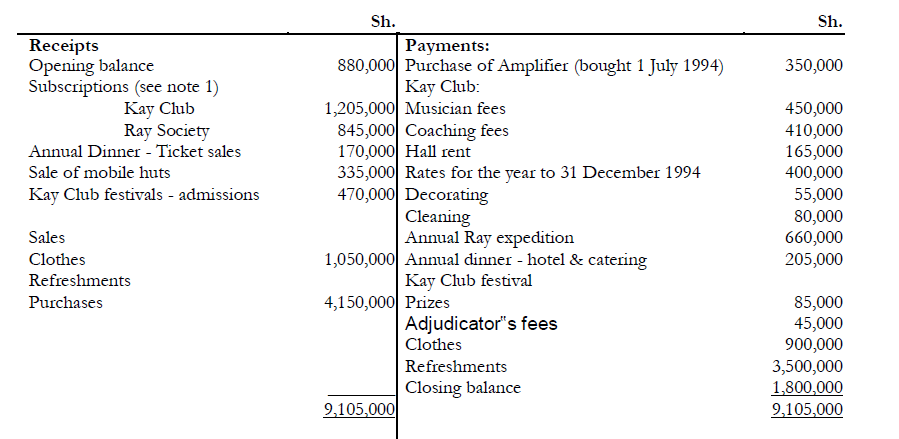

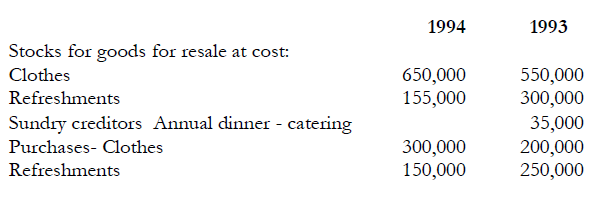

The treasurer of Kay Club and Ray Society has prepared the following receipts and payments

account for the year ended 31 December 1994:

(Solved)

The treasurer of Kay Club and Ray Society has prepared the following receipts and payments

account for the year ended 31 December 1994:

Note. It is the policy of the Society NOT to take into account subscriptions in arrear until

theyare paid.

1) The mobile hut which was sold during 1994 had been valued at Sh.400,000 on 31

December 1993, and was used for the society's activities until sold on 30 June 1994.

2) Immediately after the sale of the mobile hut, the Society rented a new hall at Sh.165,000 per

annum.

3) The above receipts and payments account is a summary of the society's bank account for

the year ended 31 December 1994; the opening and closing balances shown above were the

balances shown in the bank statements on 31 December 1993 and 1994 respectively.

4) All cash is banked immediately and all payments are made by cheque.

5) A cheque for Sh.l00,000 drawn by the society on 28 December 1994 for stationery was not

paid by the bank until 4 January 1995.

6) The Society's assets and liabilities at 31 December 1993 and 1994, in addition to those

mentioned earlier, were as follows:

Required:

a) The Society's Income and Expenditure Account for the year ended 31 December

1994, and balance sheet as at that date. (Comparative figures are not required).

b) Outline the advantages of income and expenditure accounts as compared with

receipts and payments accounts.

Date posted:

November 25, 2018

.

Answers (1)

-

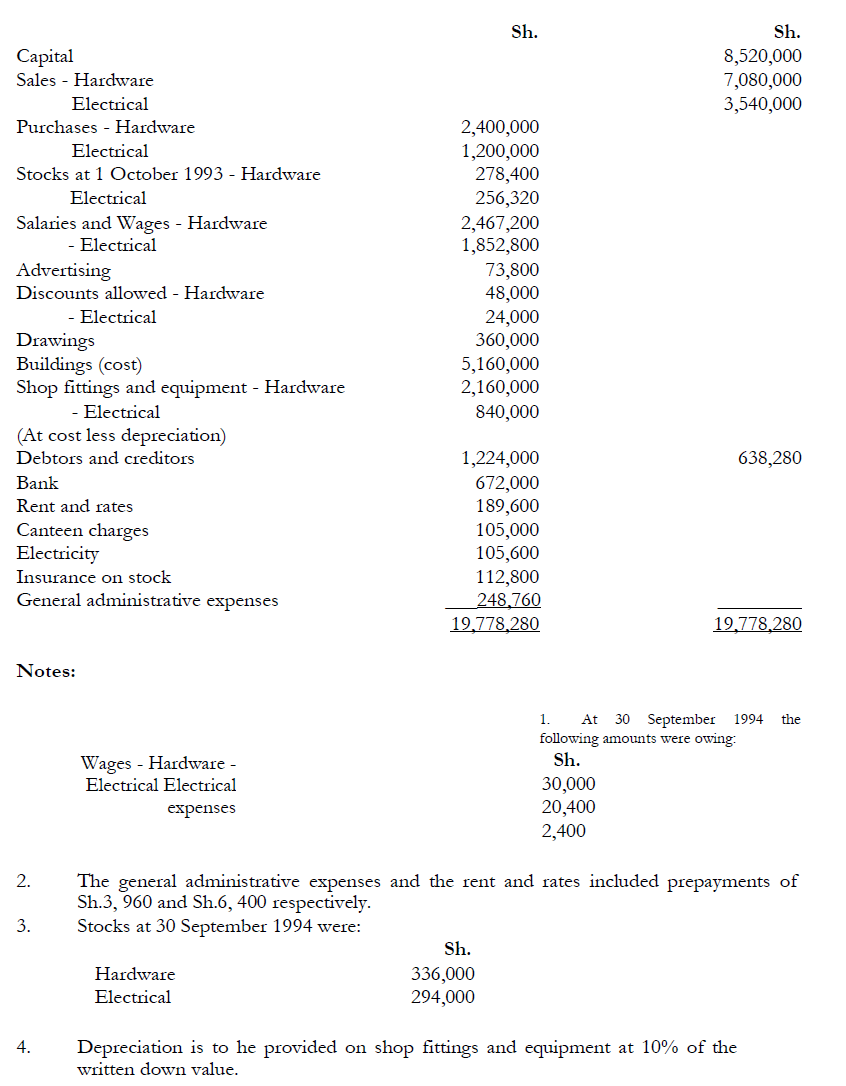

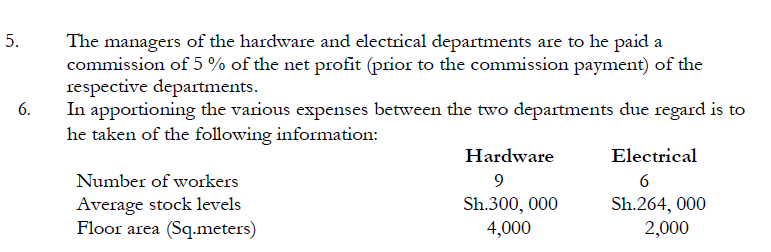

Manga Munene is the proprietor of a retail business, which has two main departments, which

sell hardware and electrical goods, respectively. He had previously prepared his...

(Solved)

Manga Munene is the proprietor of a retail business, which has two main departments, which

sell hardware and electrical goods, respectively. He had previously prepared his annual accounts

in such a way that the relative profitability of the two departments was not ascertainable, but

now he wishes to attempt to identify the profit attributable to each department in order that he

may pay a bonus to the more successful of the departmental managers. At 30 September 1994,

the balances in the books of the business were as follows:

The general administrative expenses are primarily incurred in relation to the processing

of purchases and sales invoices.

Required:

(a) A schedule showing the basis on which you have apportioned the various expenses

between the two departments.

(b) The departmental and combined Trading and Profit and Loss Account for the year

ended 30 September 1994.

(c) Balance Sheet at 30 September 1994.

Date posted:

November 25, 2018

.

Answers (1)

-

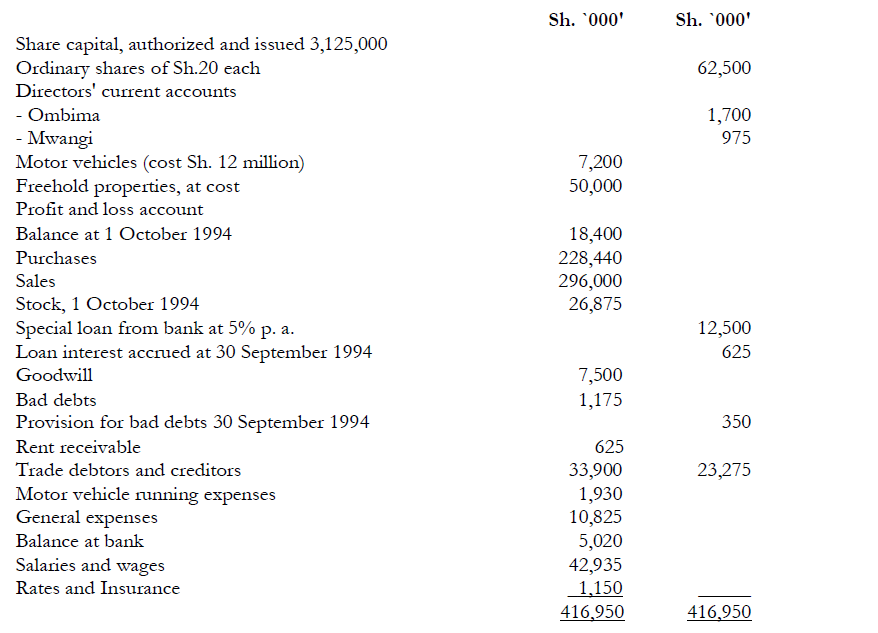

The following trial balance was extracted from the books of Hiza Ltd. as on 30 September 1995

(Solved)

The following trial balance was extracted from the books of Hiza Ltd. as on 30 September 1995:

You are given the following information:

1. Stock in trade, 30 September 1995 was Sh.28, 875,000.

2. The provisions for bad debts is to be increased to Sh.750,000.

3. Salaries and .wages outstanding at 30 September 1995 is Sh.500,000.

4. Rates and insurance paid in advance at 30 September 1995 is Sh. 155,000.

5. The item 'rent receivable Sh.625,000 includes Sh. 125,000 in respect of the period from 1

October 1995 to 31 December 1995.

6. Provision is to be W de for depreciation of motor vehicles at the rate of 20 per cent

per annum on cost.

7. During the year to 30 September 1995, Ombima, one of the directors took goods (cost

Sh.437,500) out of business stock for his own use. No entry for this transaction has

been made in the books.

Required:

(a) Trading and Profit and Loss Account for the year to 30 September 1995.

(b) Balance Sheet as at that date.

Date posted:

November 25, 2018

.

Answers (1)

-

With reference to International Accounting Standards explain the following:

(a) Fundamental accounting concepts

(b) Accounting bases

(c) Accounting policies

(Solved)

With reference to International Accounting Standards explain the following:

(a) Fundamental accounting concepts

(b) Accounting bases

(c) Accounting policies

Date posted:

November 25, 2018

.

Answers (1)

-

James Mbuvi started a taxi business in Nairobi in March 1990 under the firm name Mbuvi

Taxis. The firm had two vehicles KA and KB which...

(Solved)

James Mbuvi started a taxi business in Nairobi in March 1990 under the firm name Mbuvi

Taxis. The firm had two vehicles KA and KB which had been purchased for Sh.560,000 and

Sh.720,000 respectively earlier in the year.

In February 1992 vehicle KB was involved in an accident and was written off. The insurance

company paid the firm Sh.160,000 for the vehicle. In the same year the firm purchased two

vehicles, KC and KD for Sh.800,000 each.

In November 1993' vehicle KC was sold for Sh.716,000. In January 1994 vehicle KE was

purchased for Sh.840,000. In March 1994 another vehicle KF was purchased for Sh.960.000.

The firm's policy is to depreciate vehicles at the rate of 25 per cent on cost on vehicles on hand

at the end of the year irrespective of the date of purchase. Depreciation is not provided for

vehicles disposed of during the year. The firm's year ends on 31 December.

Required:

(a) Calculate the amount of depreciation charged in the profit and loss account for each of the five

years.

(b) Prepare the motor vehicle account (at cost).

(c) Calculate the profit or loss on disposal of each of the vehicles disposed of by the company.

Date posted:

November 25, 2018

.

Answers (1)

-

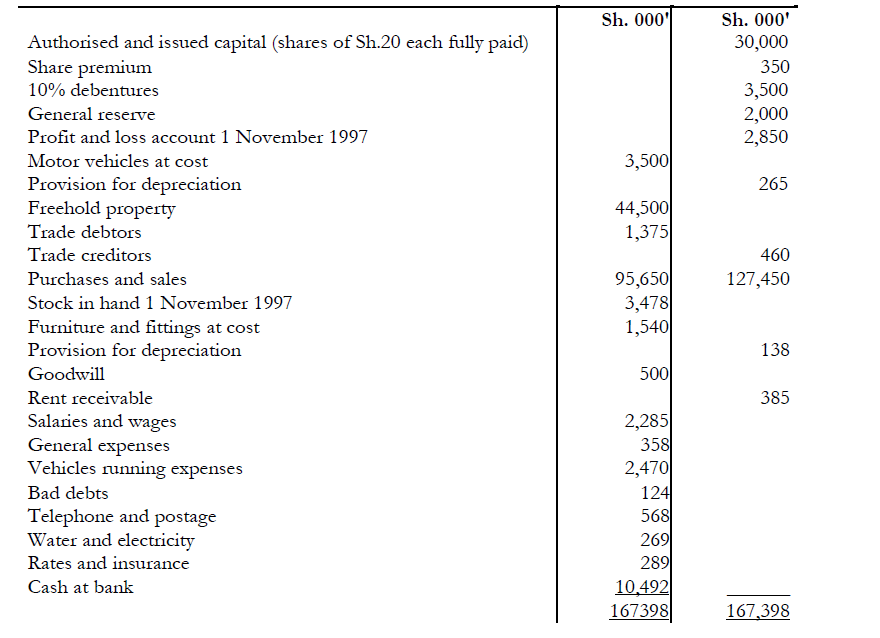

The Chief Accountant of KK Ltd. has extracted the following trial balance as at 31 October 1998:

(Solved)

The Chief Accountant of KK Ltd. has extracted the following trial balance as at 31 October 1998:

Notes:

1. Credit sales amounting to Sh. 165,000 were made on 31 October 1998 but no entries were

made in the books.

2. Returns outwards amounting to Sh. 128,000 were dispatched on 31 October 1998 but no

entries were made in the books.

3. Closing stock was valued at Sh.4, 398,000.

4. Accrued salaries and telephone bills amounted to Sh. 134,000 and Sh.55, 000 respectively.

5. Rent for the month of October 1998 amounting to Sh.35, 000 had not been received

from the tenant.

6. Provision for depreciation on furniture and fittings and the motor vehicles are 10% and

20% on cost respectively.

7. Provision for bad and doubtful debts of 5 % on trade debtors should be made.

8. Corporation tax should be provided at 35 % of the net profit before tax.

9. The directors propose a dividend of 15% on issued share capital and a transfer of

Sh.2, 500,000 to the general reserve.

10. The debenture interest has not yet been paid.

Required:

(a) Trading, profit and loss account for the year ended 31 October 1998.

(b) Balance sheet as at 31 October.

Date posted:

November 25, 2018

.

Answers (1)

-

List and explain five characteristics of a partnership

(Solved)

List and explain five characteristics of a partnership.

Date posted:

November 24, 2018

.

Answers (1)

-

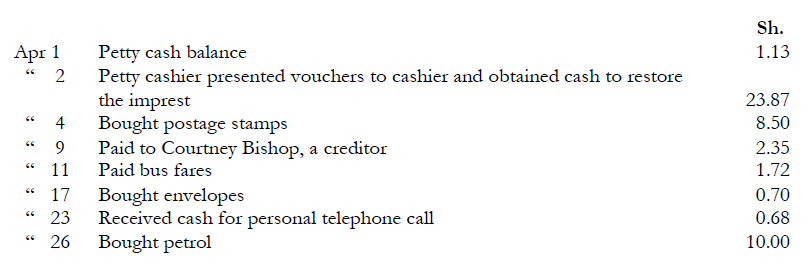

Kathryn Rochford keeps her petty cashbook on the imprest system, the imprest being Sh.25. For the month of April 20X9 her petty cash transactions were...

(Solved)

(a) Kathryn Rochford keeps her petty cashbook on the imprest system, the imprest being Sh.25. For the month of April 20X9 her petty cash transactions were as follows:

(i) Enter the above transactions in the petty cashbook and balance the petty

cashbook at 30 April, bringing down the balance on 1 May.

(ii) On 1 May Kathryn Rochford received an amount of cash from the cashier

to restore the imprest. Enter this transaction in the petty cashbook.

(b) Open the ledger accounts to complete the double entry for the following:

(i) The petty cash analysis columns headed Postage and Stationery and Travelling Expenses;

(iii) The transactions dated 9 and 23 April 20X9.

Date posted:

November 24, 2018

.

Answers (1)

-

Why do some businesses keep a petty cashbook as well as a cashbook?

(Solved)

Why do some businesses keep a petty cashbook as well as a cashbook?

Date posted:

November 24, 2018

.

Answers (1)

-

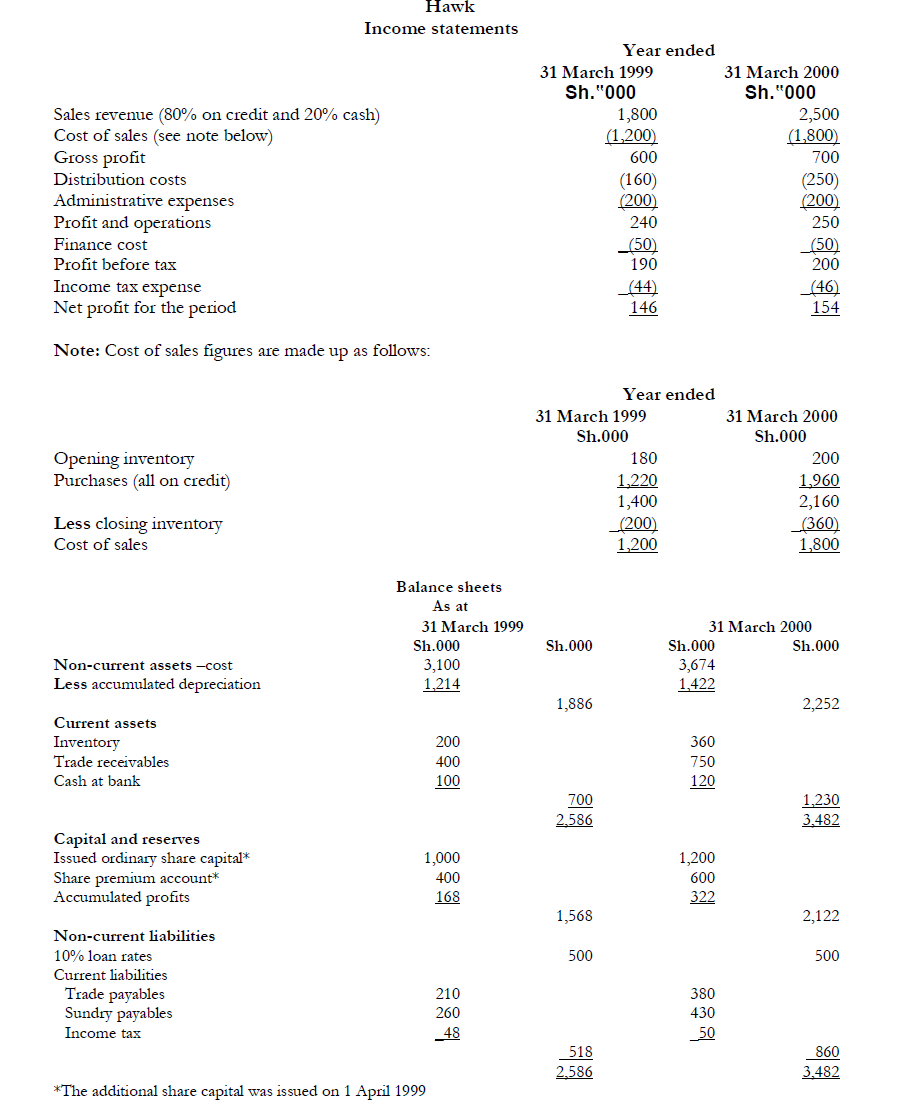

The directors of Hawk, a limited liability company, wish to compare the company's most recent financial statements with those of the previous year. The company's...

(Solved)

The directors of Hawk, a limited liability company, wish to compare the company's most recent financial statements with those of the previous year. The company's financial statements are given below:

Required:

(a) Calculate, for each of the two years, eight accounting ratios which should assist the directors

in their comparison, using closing figures for balance sheet items needed.

(b) Suggest possible reasons for the changes in the ratios between the two years.

Date posted:

November 24, 2018

.

Answers (1)

-

Briefly explain the following accounting Concepts. (i) Going concern (ii) Accruals (iii) Consistency (iv) Prudence or conservatism (v) Materiality

(Solved)

i) Going concern

ii) Accruals

iii) Consistency

iv) Prudence or conservatism

v) Materiality

vi) Substance over form

vii) Business entity concept

viii) Money measurement

ix) Historical cost

x) Objectivity

xi) Realization

xii) Duality

Date posted:

November 24, 2018

.

Answers (1)

-

What are accounting concepts, Bases, Policies?

(Solved)

What are accounting concepts, Bases, Policies?

Date posted:

November 24, 2018

.

Answers (1)