Advantages of telex are;

- Speed

- Reliability of written communication.

- 24-hour service.

- Ability to receive messages outside office hours.

- Foreign languages can be translated at leisure before replying.

Most businesses are telex subscribers, hence convenient to use.

marto answered the question on February 5, 2019 at 09:07

-

What is a balance sheet?

(Solved)

What is a balance sheet?

Date posted:

January 28, 2019

.

Answers (1)

-

The trial balance of S. Juma, a sole trader, did not balance on 30 April 1995. The

difference was put in the suspense account. The final...

(Solved)

The trial balance of S. Juma, a sole trader, did not balance on 30 April 1995. The

difference was put in the suspense account. The final accounts, which were then

prepared, showed a net profit of Sh.64, 000.

During audit, the following errors were noted:

(1) A loan from ABD Bank of Sh. 10,000 was entered correctly in cashbook but was not

posted to the ledger.

(2) A cheque of Sh.4,000 for rent received was not entered in the books.

(3) Closing stock was overvalued by Sh.1, 500.

(4) Discount allowed of Sh.500 was entered in the discount received account.

(5) The opening stock was understated by Sh.3,200.

(6) Prepaid insurance of Sh.220 had been included in the profit and loss account.

(7) Goods destroyed by fire amounting to Sh. 12,000 were written off in the profit and loss

account.

However the insurance company has agreed to compensate the full amount.

Required:

(a) Journal entries to correct the errors.

(b) Statement of corrected profit.

(c) Suspense account.

Date posted:

November 26, 2018

.

Answers (1)

-

The draft final account for the year ended 30 June 1994 of central limited, car dealers, show a

gross profit of Sh 90,000 and a net...

(Solved)

The draft final account for the year ended 30 June 1994 of central limited, car dealers, show a

gross profit of Sh 90,000 and a net profit of Sh 2,250,000. After subsequent investigations

the following discoveries were made:

1. A debt of Sh. 75,000 due from J. Mema to the company was written off as

irrecoverable in the company‟s books in January 1994. Since preparing the

draft accounts, J.Mema has settled the debt in full.

2. The company‟s main warehouse was burgled in February 1994, when goods costing Sh.

5,000,000 were stolen. This amount has been shown in the draft account as an overhead

item “Loss due to burglary”. Although the insurance company denied liability

originally, in the past days or two that decision it has changed and central limited have

advised that Sh. 3,500,000 will be paid in settlement.

3. Discounts received in March 1994 of Sh. 52,500 have been credited, in error,

to purchases.

4. On 2 January 1994, a car, which had cost the company Sh. 450,000, was taken from the

showroom for the use of one of the company‟s sale representatives whilst

on company business. In the showroom, the is car had a Sh. 600,000 price label.

Effect has not been given to this transfer in the books of the company, although the

car was not included in the trading stock valuation at 30 June 1994.the company

provides for depreciation on motor vehicles at the rate of 25% of the cost of vehicles

held at the end of each financial year.

5. Goods bought and received from P.Nene on 29 June 1994 at a cost of Sh 300,000

were not recorded in the company‟s books of account until early July 1994.

Although they were unsold on 30june 1994, the goods in question were not included

in the stock valuation at that date.

6. The company is hoping to market a new car accessory product in January 1995. The

venture is to be launched with an advertising campaign commencing in July 1994. The

cost of this campaign is Sh. 1,250,000 and this has been debited in the

company‟s profit and loss account for the year ended 30 June 1994, and is included

in current liabilities as a provision, notwithstanding the confident expectations that the

new product will be a success.

7. On June 30 1994, the company paid an insurance premium of Sh. 150,000, the renewal

being for the year commencing 1 July 994. This premium was included n the

insurances of Sh. 275,000 debited in the draft profit and loss account.

Required:

(a) The journal entries necessary to effect corrections of all the above errors.

(b) A computations of the corrected gross profit and net profit for the year ended 30 June

1994

Date posted:

November 26, 2018

.

Answers (1)

-

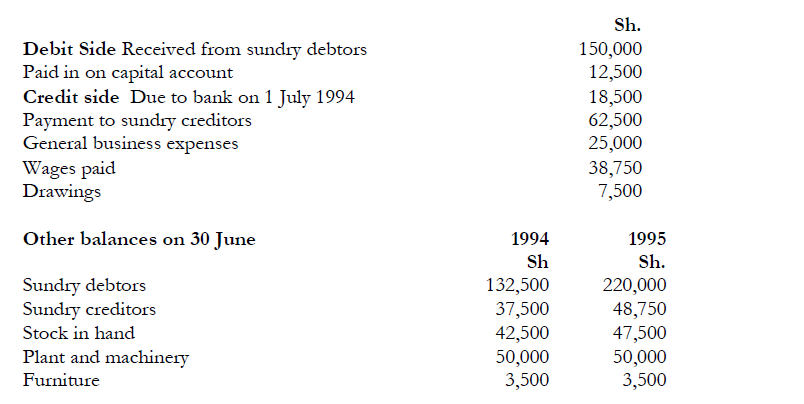

Jackson Ndambuki, a businessman in Kangundo, does not maintain a double entry

bookkeeping system.

On 1 July 1994 his capital was Sh. 172,500. An analysis of his...

(Solved)

Jackson Ndambuki, a businessman in Kangundo, does not maintain a double entry

bookkeeping system.

On 1 July 1994 his capital was Sh. 172,500. An analysis of his cashbook for the year to 30

June 1995 gives the following particulars:

Discounts allowed and received amounted to Sh. 15,000 and Sh.7,500 respectively.

Interest of 5 per cent per annum is to be provided on capital at the beginning of the year.

(Ignore payments in and drawings)

Depreciate plant and machinery at 10 per cent and furniture at 5 per cent on the book value. A

provision for doubtful debts of 5 per cent is to be made on sundry debtors.

Required:

(a) Trading, Profit and Loss Account for the year ended 30 June 1995.

(b) Balance Sheet as at that date.

Date posted:

November 26, 2018

.

Answers (1)

-

Explain the meaning and significance of the revenue realization principle.

(Solved)

Explain the meaning and significance of the revenue realization principle.

Date posted:

November 26, 2018

.

Answers (1)

-

Define the term accounting standard and give four reasons why a professional accounting body issues accounting standards.

(Solved)

Define the term accounting standard and give four reasons why a professional accounting body issues accounting standards.

Date posted:

November 26, 2018

.

Answers (1)

-

List the principal distinctions between partnerships and limited companies

(Solved)

List the principal distinctions between partnerships and limited companies

Date posted:

November 26, 2018

.

Answers (1)

-

The trial balance of Bidii Retailers, which was extracted on 30 September 1996, included

the following items:

Sh.

Sales ledger control account 550,885

Purchases ledger control account 391,330

Suspense account...

(Solved)

The trial balance of Bidii Retailers, which was extracted on 30 September 1996, included

the following items:

Sh.

Sales ledger control account 550,885

Purchases ledger control account 391,330

Suspense account in trial balance (debit balance) 11,550

The following additional information is available:

1. The balances from sales ledger were: Debit balances Sh.555, 555 Credit

balances Sh.6, 170

2. The balances from purchases ledger were: Credit balances Sh.388.88:

Debit balances Sh.5, 555.

3. The sales ledger includes a debit balance of Sh.3, 500 for Moco Fishing Ltd., and the

purchase ledger includes a credit balance of Sh.4, 000 relating to the same firm. The debit

balance will be offset against the credit balance and the difference will be settled in cash.

4 . Included in the credit balance on the sales ledger is a balance of Sh.3, 000 in the name of

John Oloo. This arose because a sales invoice of Sh.3, 000 had earlier been posted in error

from the sales daybook to the debit of the account of Peter Oloo in the purchases ledger.

5. An allowance of Sh.1,500 against some damaged goods had been omitted from the appropriate

account in the sales ledger. This allowance had been included in the control account.

6. An invoice for Sh.2.280 had been entered in the purchase daybook as Sh.3,270.

7. A cash receipt from a credit customer for Sh.1,725 had been entered in the cash book as

Sh.1,225.

8. The purchase day book had been overcast by Sh.5,000.

9. The bank balance of Sh.6,000 had been included in the trial balance, in error, as an overdraft.

10. The book-keeper had been instructed to write off Sh.2,500 from c ustomer XYZ's account as a

bad debt, and to reduce the provision for bad and doubtful debts by Sh.3,500. He

however wrote off Sh.3,500 from the customers' account. He then increased the

provision for bad and doubtful debts by Sh.2,500.

11. The debit balance on the insurance account in the nominal ledger of Sh. 17,050 had

been included in the Trial balance as Sh.17,500.

Required:

(a) Corrected sales ledger control, purchase ledger control, and suspense accounts balances.

(b)Reconcile the sales ledger balances with the corrected sales ledger control account balance,

and also the purchases Ledger balances with the corrected purchase ledger control

balance.

Date posted:

November 26, 2018

.

Answers (1)

-

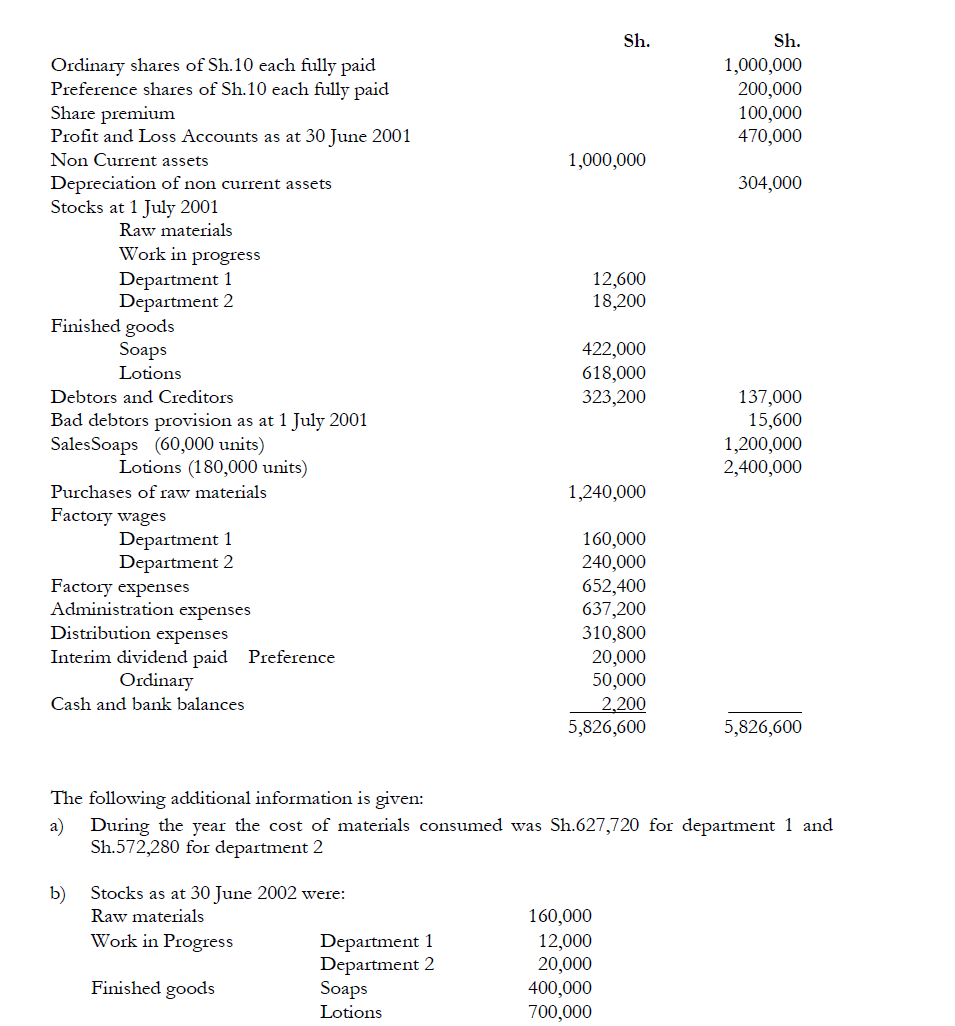

Sabuni Ltd manufactures and sells soaps and Lotions. The two products pass through two manufacturing departments 1 and 2. You are supplied with the following...

(Solved)

Sabuni Ltd manufactures and sells soaps and Lotions. The two products pass through two manufacturing departments 1 and 2. You are supplied with the following trial balance as at 30 June 2002.

c) Depreciation is to be provided on Non current assets at the rate of 10 per cent per annum

on cost. additional non current assets were purchased on 1 January 2002 at a cost of

Sh.80,000.The annual depreciation charge is to be divided among manufacturing

,administration and distribution in the ratio of 8:1:1.

d) Prepaid and accrued administration amount to Shs.1,800 and Shs.3,000 respectively.

e) Bad debts of Sh.3,200 are to be written off and a provision for doubtful debts to be

increased to Sh.16,000.This should be taken as a distribution cost.

f) The following allocations are to be made.

- Manufacturing expenses (between dept 1 and dept 2) in proportion to manufacturing

wages

- Administration expenses (between soaps and Lotions) in proportion to number of

units sold

- Distribution expenses (between soaps and Lotions) in the proportion of sales value.

- Cost of goods manufactured in dept 1 (between soaps and Lotions) in the ration of

5:4.

- Cost of goods manufactured in dept 2 (between soaps and Lotions) in the ration of

1:5

g) Corporation tax payable for the year is Sh.160,000.

h) The directors propose a final dividend of sh.100,000.

Required:

a) i) A manufacturing account showing the results of department 1 and 2 ,

ii) Trading, Profit and Loss account showing the results of soaps and

Lotions, for the year ending 30 June 2002.

b) A balance sheet as at 30 June 2002.

Date posted:

November 26, 2018

.

Answers (1)

-

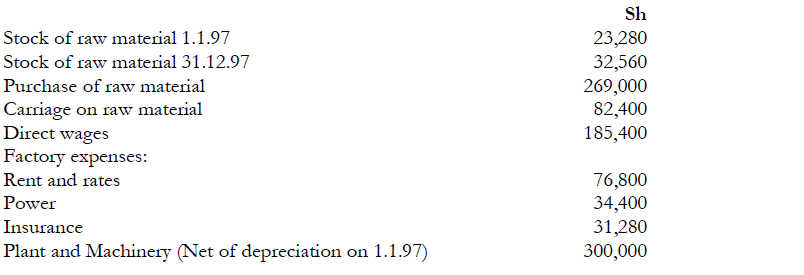

Rono Ltd. manufactures electric toys called Densta on small scale basis. On 1 January 1997, 6000 units of Densta were in stock. During 1997, the...

(Solved)

Rono Ltd. manufactures electric toys called Densta on small scale basis. On 1 January 1997, 6000 units of Densta were in stock. During 1997, the company manufactured 200,000 units and sold 190,000 units at a price of Sh.6 each. The following balances were extracted from the books of account on 31 December 1997.

The following additional information was available:

1. Stocks of work-in-progress on 1 January and 31 December 1997 were of

insignificant value and are to be ignored.

2. Plant and machinery are to be depreciated using reducing balance method at 10 %.

3. Finished units of Densta are valued at factory cost.

4. Factory cost per unit of Densta was the same in 1996 and 1997.

Required:

(i) The manufacturing account for the year ended 31 December 1997, showing

clearly the prime cost and factory costs of producing Densta.

(ii) The trading account for the year ended 31 December 1997.

Date posted:

November 26, 2018

.

Answers (1)

-

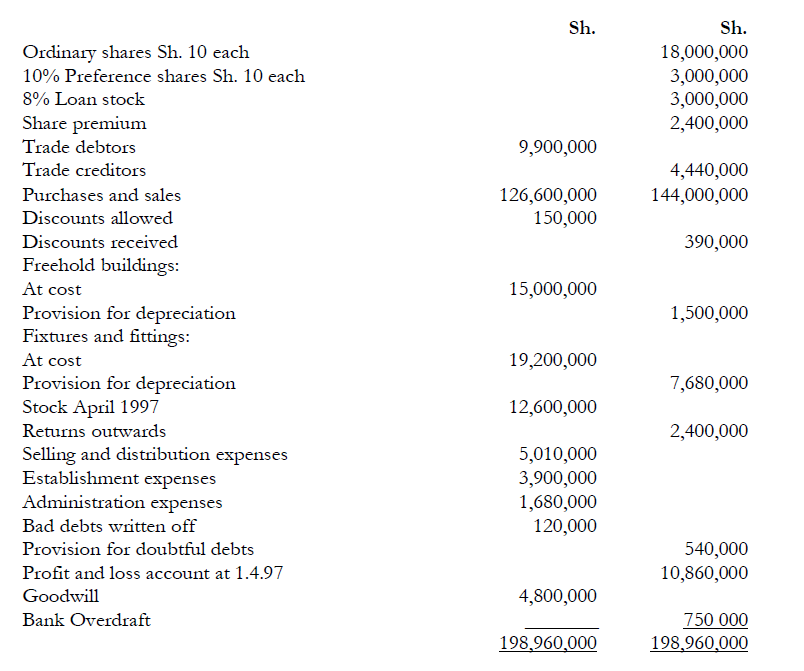

The following trial balance was extracted from the books of Mapema Traders Ltd. as at 31 March 1998:

(Solved)

The following trial balance was extracted from the books of Mapema Traders Ltd. as at 31 March 1998:

Additional information:

1. The debtors balance includes Sh.600,000 due from Otieno who has now been

declared bankrupt and it has been decided to write-off this debt as a bad debt.

2. The provision for doubtful debts is to be adjusted to 5 % of trade debtors at

31 March 1998.

3. Establishment expenses prepaid at 31 March 1998 amount to Sh.

120,000. The difference is to be written off during the year.

4. Administration expenses accrued due at 31 March 1998 amounted to Sh.210,000.

5. The company paid the interest on the loan stock for the year ended 31

March 1998 on 28 May 1998.

6. Gross profit is at the rate of 20% of sales.

7. Depreciation is provided annually on the cost of fixed assets held at the end of

the year at the following rates:

Freehold buildings 2 %

Fixtures and fittings 10%

8. The company's directors propose that the preference share dividend be paid, a

dividend of 10% on the ordinary shares to be paid and to transfer an amount of

Sh.7,500,000 to General Reserve.

Required:

The trading and profit and loss account for the year ended 31 March 1998 of Mapema Traders

Ltd. and a balance sheet as at that date.

Date posted:

November 26, 2018

.

Answers (1)

-

Write explanatory notes on the following accounting concepts:

(a) Materiality;

(b) Prudence;

(c) Consistency.

(Solved)

Write explanatory notes on the following accounting concepts:

(a) Materiality;

(b) Prudence;

(c) Consistency.

Date posted:

November 26, 2018

.

Answers (1)

-

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4, 536,000.

On...

(Solved)

Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day

bought its first lorry, registration number KA 620, for Sh.4, 536,000.

On 3 April 1995, the company bought its second lorry, KA 735 for Sh.2, 740,000.

On 3 June 1997, the first lorry, KA 620 was involved in an accident and was completely written

off. The insurance company paid the transport company Sh.1, 350,000 for the loss. On 5

January 1998, the company bought its third lorry, KB 327 for Sh.3, 780,000. Depreciation on

the lorries was provided at 10 per cent on straight -line basis. The policy of the company is to

provide depreciation for the full year for all acquisitions made at any time during the year and to

ignore depreciation on any lorry sold or disposed of during the year. All the lorries are insured.

The company makes its accounts annually to 31 December.

In 1998, the company decided to change its depreciation rate from 10 to 15 per cent on straight

line basis for all its lorries still in use retroactively, that is from year of purchase. An adjusting

entry will be made in the accounts for the year 1998.

Required:

1. The motor lorries account for years 1994 to 1998.

2. A schedule of additional depreciation arising from change of depreciation rate, for years

1994 to 1997.

3. Provision for depreciation account for the same period.

4. Disposal of motor lorries account.

Date posted:

November 26, 2018

.

Answers (1)

-

The cashbook column of Tatua Traders Company Ltd. had an overdraft of Sh.532, 400 as at 31

October 1998, which did not agree with balance as...

(Solved)

The cashbook column of Tatua Traders Company Ltd. had an overdraft of Sh.532, 400 as at 31

October 1998, which did not agree with balance as per bank statement of the same date.

On checking through the relevant records and documents, some details were established as

shown below:

1. Bank charges and interest on overdraft as per the bank statement amounted to Sh. 12,450

and Sh. 135,480 respectively.

2. A debtor deposited Sh.254, 500 to the bank direct.

3. Insurance premium of the mortgaged property amounting to Sh.35, 485 was paid direct

by the bank.

4. Standing orders of Sh. 138,000 have been effected by the bank.

5. Cheques for Sh.354, 890 which were banked on 29 October 1998 were credited by the

bank on 5 November 1998.

6. Cheques drawn by the company amounting to Sh.745, 964 had not been presented for

payment as at 31 October 1998.

7. A cheque for Sh.74, 500 was debited by the bank as Sh.47, 500.

8. The payments side of the cashbook was undercast by Sh.32, 000.

9. The bank had debited the account with another customer's cheque of Sh.27, 500 but had

not yet corrected the mistake on 31 October 1998.

Required:

(a) Make adjustments in the cash book and show the adjusted cash book balance.

(b) A bank reconciliation statement as at 31 October 1998.

Date posted:

November 26, 2018

.

Answers (1)

-

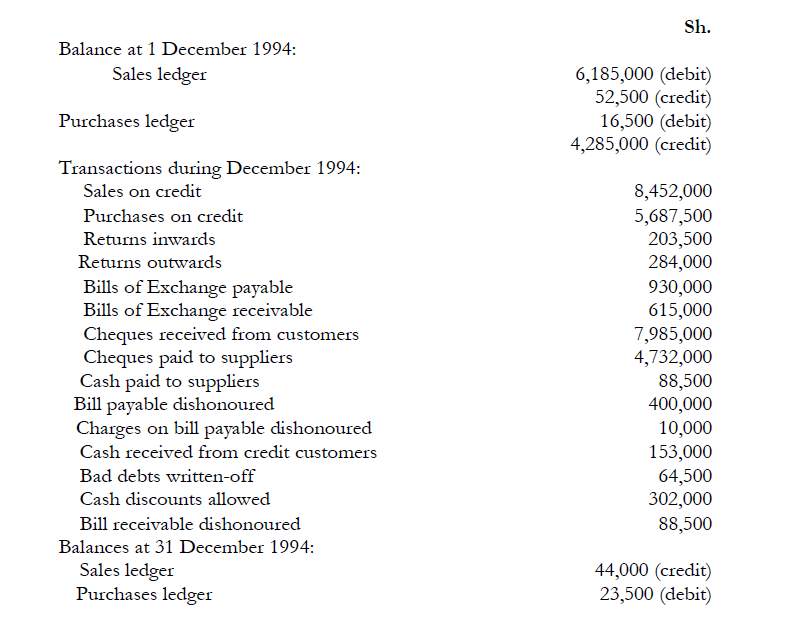

XML Ltd. maintains control accounts in its business records. The balances and transactions relating to the company's control accounts for the month of December 1994...

(Solved)

XML Ltd. maintains control accounts in its business records. The balances and transactions relating to the company's control accounts for the month of December 1994 are listed below:

Required:

Post the sales ledger and the purchases ledger control accounts for the month of December

1994 and derive the respective debit and credit closing balances on 31 December 1994.

Date posted:

November 26, 2018

.

Answers (1)

-

Explain the purposes for which control accounts are prepared in a business organisation

(Solved)

Explain the purposes for which control accounts are prepared in a business organisation.

Date posted:

November 26, 2018

.

Answers (1)

-

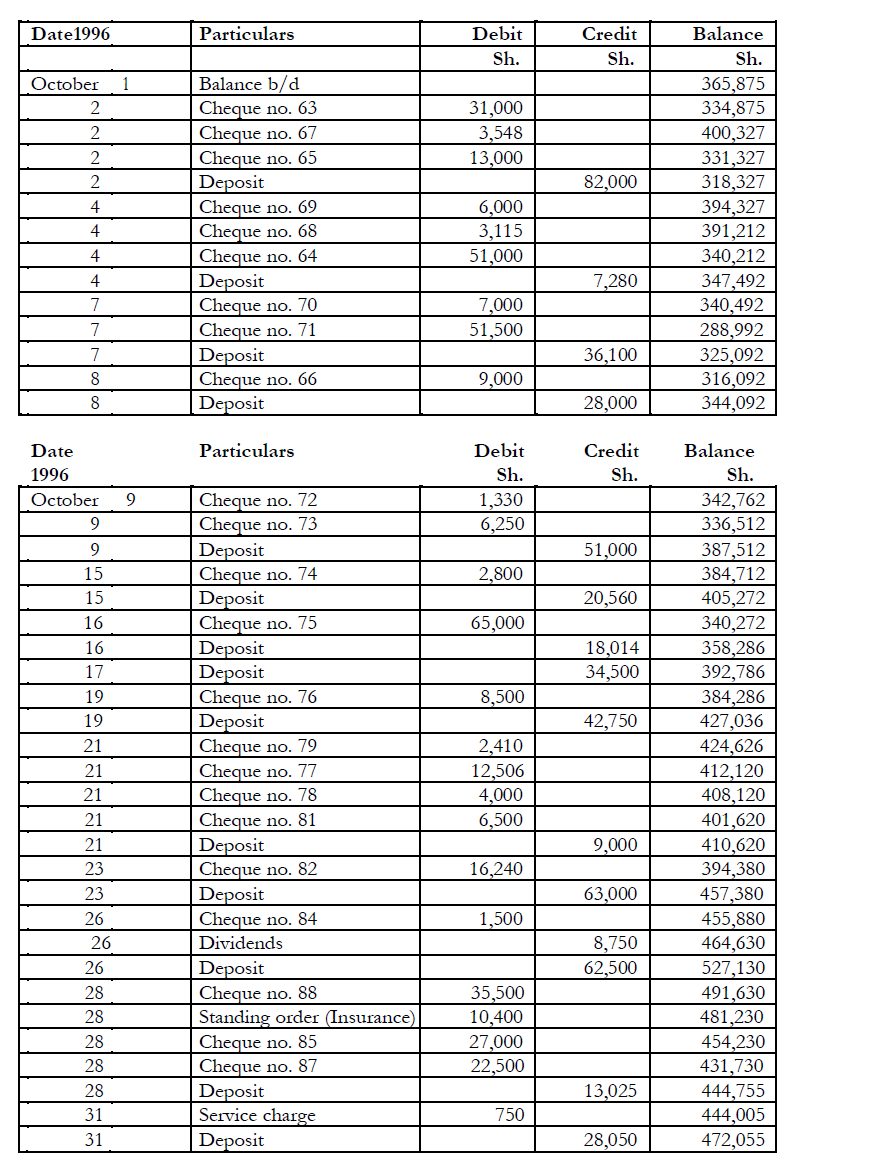

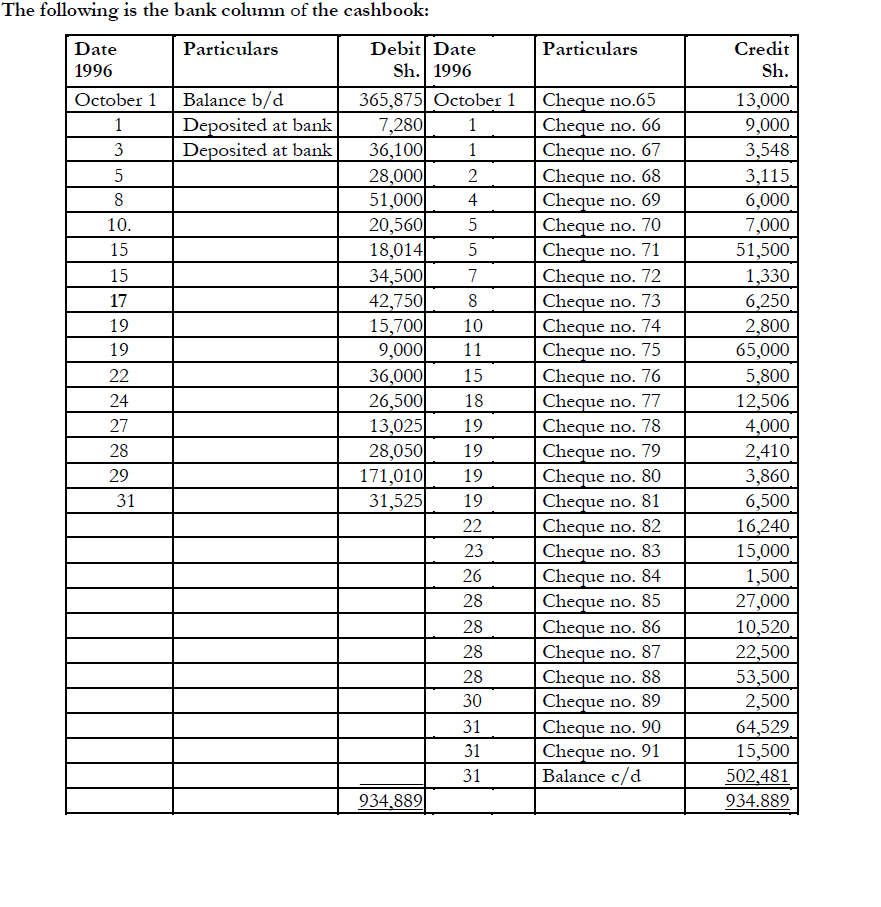

The following is the bank statement of Kakamega Retail Traders for the month of October 1996:

(Solved)

The following is the bank statement of Kakamega Retail Traders for the month of October 1996:

Notes:

1. The bank reconciliation on 30 September 1996 showed that one deposit was in transit and

two cheques had not yet been presented to the bank.

2. Deposits of Sh.62, 500 and Sh.36, 000 had been entered in the cash book as Sh.26,500

and Sh.36,000 and in the bank statement as Sh.62,500 and Sh.63,000, respectively.

3. A cheque from Mkulima for Sh.15,700 was deposited on 18 October 1996 but

was dishonoured and the advice was received on 4 November 1996.

4. Counterfoils for cheques no. 76 and no. 88 showed they had been drawn for Sh.5,800 and

Sh.35,500 respectively.

Required:

(a) A correct cashbook balance.

(b) A bank reconciliation statement on 31 October 1996.

Date posted:

November 25, 2018

.

Answers (1)

-

What is the purpose of preparing a bank reconciliation statement?

(Solved)

What is the purpose of preparing a bank reconciliation statement?

Date posted:

November 25, 2018

.

Answers (1)

-

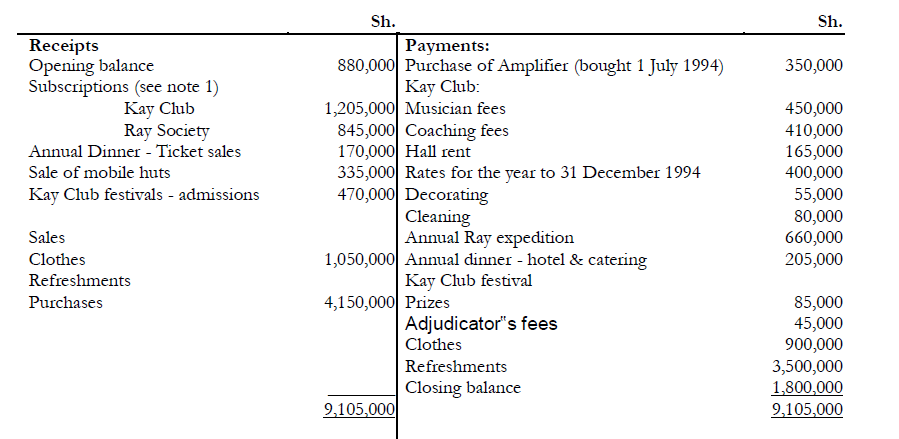

The treasurer of Kay Club and Ray Society has prepared the following receipts and payments

account for the year ended 31 December 1994:

(Solved)

The treasurer of Kay Club and Ray Society has prepared the following receipts and payments

account for the year ended 31 December 1994:

Note. It is the policy of the Society NOT to take into account subscriptions in arrear until

theyare paid.

1) The mobile hut which was sold during 1994 had been valued at Sh.400,000 on 31

December 1993, and was used for the society's activities until sold on 30 June 1994.

2) Immediately after the sale of the mobile hut, the Society rented a new hall at Sh.165,000 per

annum.

3) The above receipts and payments account is a summary of the society's bank account for

the year ended 31 December 1994; the opening and closing balances shown above were the

balances shown in the bank statements on 31 December 1993 and 1994 respectively.

4) All cash is banked immediately and all payments are made by cheque.

5) A cheque for Sh.l00,000 drawn by the society on 28 December 1994 for stationery was not

paid by the bank until 4 January 1995.

6) The Society's assets and liabilities at 31 December 1993 and 1994, in addition to those

mentioned earlier, were as follows:

Required:

a) The Society's Income and Expenditure Account for the year ended 31 December

1994, and balance sheet as at that date. (Comparative figures are not required).

b) Outline the advantages of income and expenditure accounts as compared with

receipts and payments accounts.

Date posted:

November 25, 2018

.

Answers (1)

-

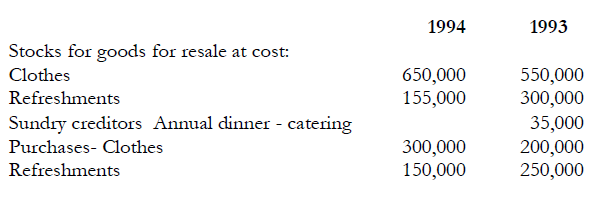

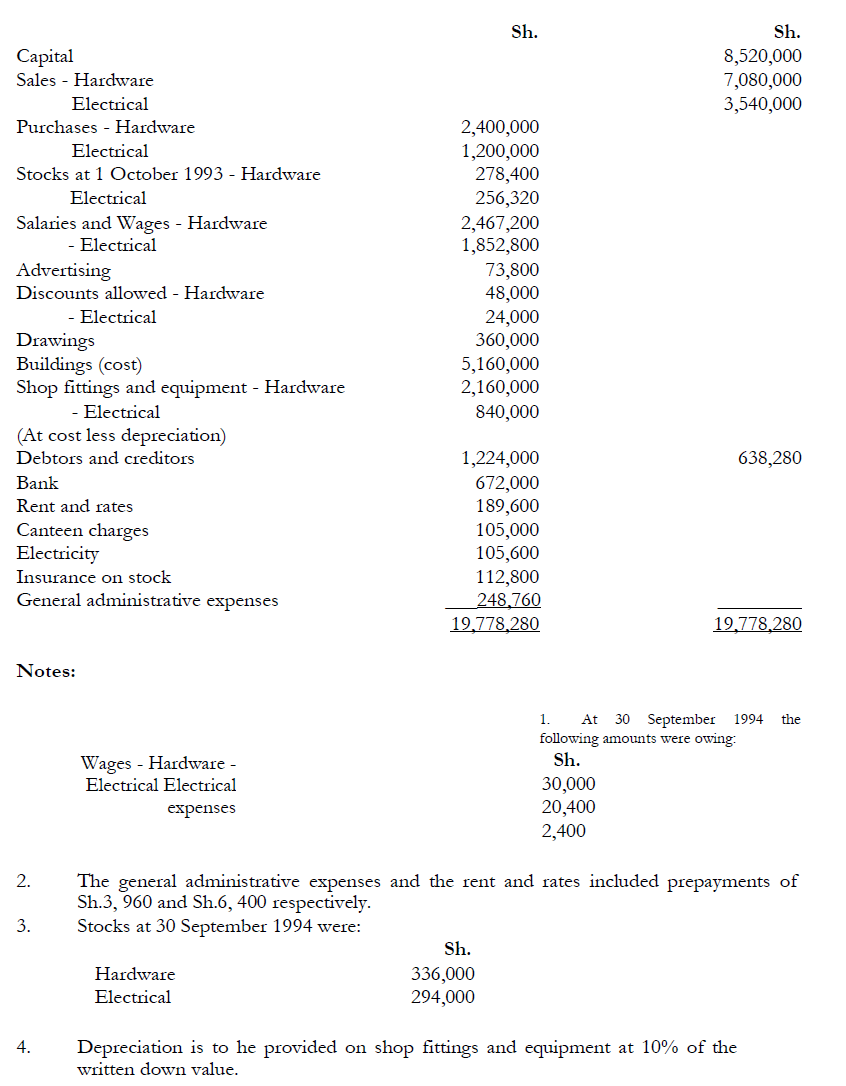

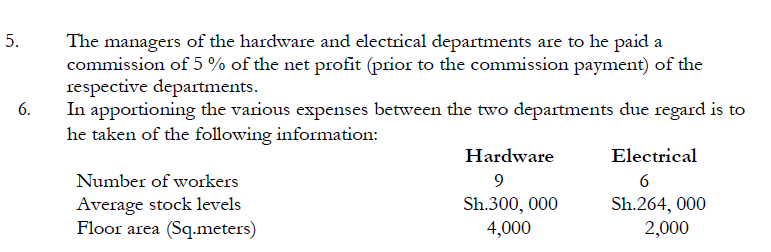

Manga Munene is the proprietor of a retail business, which has two main departments, which

sell hardware and electrical goods, respectively. He had previously prepared his...

(Solved)

Manga Munene is the proprietor of a retail business, which has two main departments, which

sell hardware and electrical goods, respectively. He had previously prepared his annual accounts

in such a way that the relative profitability of the two departments was not ascertainable, but

now he wishes to attempt to identify the profit attributable to each department in order that he

may pay a bonus to the more successful of the departmental managers. At 30 September 1994,

the balances in the books of the business were as follows:

The general administrative expenses are primarily incurred in relation to the processing

of purchases and sales invoices.

Required:

(a) A schedule showing the basis on which you have apportioned the various expenses

between the two departments.

(b) The departmental and combined Trading and Profit and Loss Account for the year

ended 30 September 1994.

(c) Balance Sheet at 30 September 1994.

Date posted:

November 25, 2018

.

Answers (1)