Determine Extracts of the statement of comprehensive income for the years ended 31 December 2009 and 2010

(Solved)

On 1 January 2009, Kamulu Limited leased a machine from General Machines Ltd. under a finance lease agreement. Kamulu Limited was to make installment lease payments of Sh. 14,000,000 every six months on 30 June and 31 December in arrears.The first payment was made on 30 June 2009.The fair value of the machine was Sh.60,000,000 with an estimated useful life of 3 years.The interest rate implicit in the lease was 10% per six months.

Determine Extracts of the statement of comprehensive income for the years ended 31 December

2009 and 2010.

Date posted:

February 8, 2019

.

Answers (1)

Calculate the Deferred tax account: Equip Agencies Ltd. purchased an equipment for Sh.4,000,000 on 1 July 2008. Depreciation on equipment is provided on a straight line basis at the rate...

(Solved)

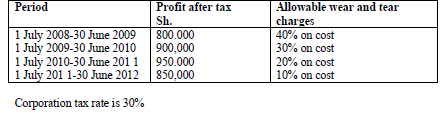

Equip Agencies Ltd. purchased an equipment for Sh.4,000,000 on 1 July 2008. Depreciation on equipment is provided on a straight line basis at the rate of 25% per annum.

During the four years from 1 July 2008 to 30 June 2012 the profit after tax and allowed

wear and tear charges for tax purpose were as follows:

Calculate the Deferred tax account

Date posted:

February 8, 2019

.

Answers (1)

Calculate the Taxable profits: Equip Agencies Ltd. purchased an equipment for Sh.4,000,000 on 1 July 2008. Depreciation on equipment is provided on a straight line basis at the rate...

(Solved)

Equip Agencies Ltd. purchased an equipment for Sh.4,000,000 on 1 July 2008. Depreciation on equipment is provided on a straight line basis at the rate of 25% per annum.

During the four years from 1 July 2008 to 30 June 2012 the profit after tax and allowed

wear and tear charges for tax purpose were as follows:

Calculate the Taxable profits

Date posted:

February 8, 2019

.

Answers (1)