i. The parent company is itself a wholly owned subsidiary or is a partially owned subsidiary of other entity and its owned ,including those not otherwise entitled to vote have been informed about and do not object to the parent presenting consolidated

statements .

ii. The parent company’s debt or equity instrument are not traded in a public market.

iii. The parent company did not file nor is it in the process of filing its financial statements with a securities commission or other regulatory organization for the purpose of issuing any class of instruments in a public market

iv. The ultimate or any intermediate parent produces consolidated financial statements available for public use that comply with IFRSs.

Wilfykil answered the question on February 12, 2019 at 09:06

-

Differentiate between full consolidation and equity method of accounting for subsidiaries and associate companies

(Solved)

Differentiate between full consolidation and equity method of accounting for subsidiaries and associate companies

Date posted:

February 12, 2019

.

Answers (1)

-

International Accounting Standard (IAS) 28, Investment in Associates prescribes the use of the equity method of accounting for investments in associates over which the investor...

(Solved)

International Accounting Standard (IAS) 28, Investment in Associates prescribes the use of the equity method of accounting for investments in associates over which the investor has significant influence.

Required:

i) Describe the term "significant influence" in the context of IAS 28.

ii) Explain four circumstances under which the investor is exempted from use of the equity method.

Date posted:

February 12, 2019

.

Answers (1)

-

Explain the circumstances in which an entity is permitted to change its accounting policies.

(Solved)

Explain the circumstances in which an entity is permitted to change its accounting policies.

Date posted:

February 12, 2019

.

Answers (1)

-

What meetings of creditors must be held and for what purpose in the course of a creditors’ voluntary winding up?

(Solved)

What meetings of creditors must be held and for what purpose in the course of a creditors’ voluntary winding up?

Date posted:

February 12, 2019

.

Answers (1)

-

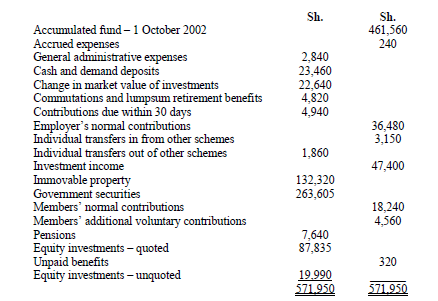

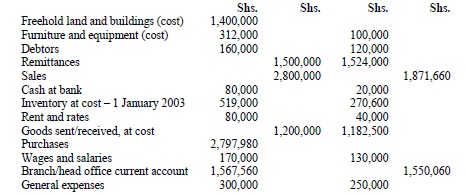

The following trial balance was extracted from the books of ABC Retirement Benefits Scheme for the year ended 30 September 2003:

Prepare:

(i) Statement of changes in...

(Solved)

The following trial balance was extracted from the books of ABC Retirement Benefits Scheme for the year ended 30 September 2003:

Date posted:

February 12, 2019

.

Answers (1)

-

Briefly explain the meaning of the term “abatement”

(Solved)

Briefly explain the meaning of the term “abatement”

Date posted:

February 12, 2019

.

Answers (1)

-

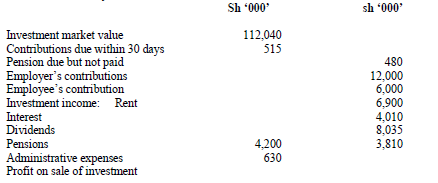

The following trial balance was extracted by the trustees of XYZ Retirement Benefit Scheme as at 31 May 2007

Prepare:

(i) Statement of changes in net assets...

(Solved)

The following trial balance was extracted by the trustees of XYZ Retirement Benefit Scheme as at 31 May 2007

Date posted:

February 12, 2019

.

Answers (1)

-

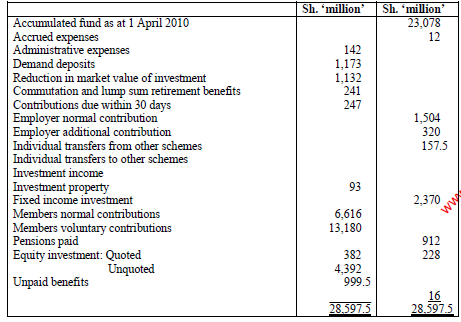

Prepare:

i) Statement of changes in net assets for the year ended 31 March 2011.

ii) Statement of net assets as at 31 March 2011

(Solved)

The following trial balance was extracted from the books of Juhudi Retirement Benefits Scheme as at 31 March 2011:

Date posted:

February 11, 2019

.

Answers (1)

-

Outline four categories of expenses that should be recognized in the income statement in accordance with International Accounting standard (IAS) 19 “Employee benefits”

(Solved)

Outline four categories of expenses that should be recognized in the income statement in accordance with International Accounting standard (IAS) 19 “Employee benefits”

Date posted:

February 11, 2019

.

Answers (1)

-

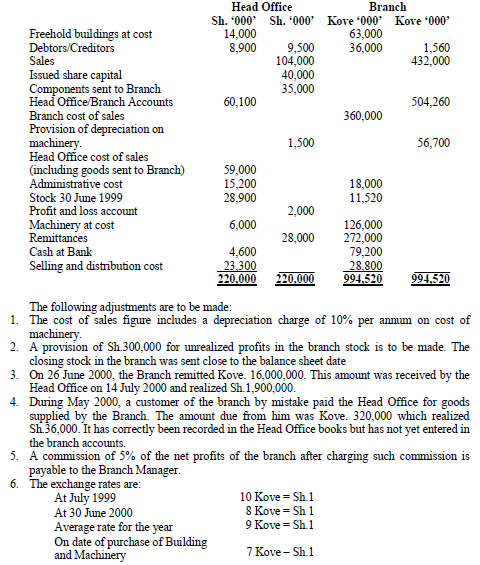

Prepare:

(a) Detailed trading and profit and loss accounts of the Head Office and the Branch for the year ended 30 June 2000.

(b) A Balance Sheet...

(Solved)

Mwenyeji Limited exported some of its products through an overseas branch whose currency is “Kove”. The trial balances of the Head Office and the Branch as at 30 June 2000 are as follows:

Date posted:

February 11, 2019

.

Answers (1)

-

Determine:

(a) A stock account and a mark-up account for each branch in column format

(b) A profit and loss account for each branch and combined total...

(Solved)

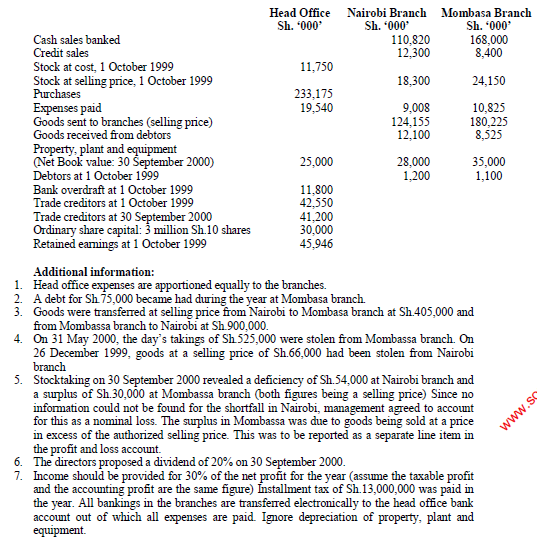

Trendsetters Limited operates two branches, one in Nairobi and one in Mombassa. These two branches are supplies from a warehouse in Athi River town where the Head Office of the Company is situated. All purchases are made at the head office. Goods are charged to both branches all selling price, which is head office cost plus 50%. All cash receipts in the branches are banked daily. The following figures relate to the company’s performance for the year ended 30 September 2000 and financial position as at that date.

Date posted:

February 11, 2019

.

Answers (1)

-

Determine:

(a) The cost of the inventories at the branch and the head office

(b) The trading profit and loss account for the year ended 31 March...

(Solved)

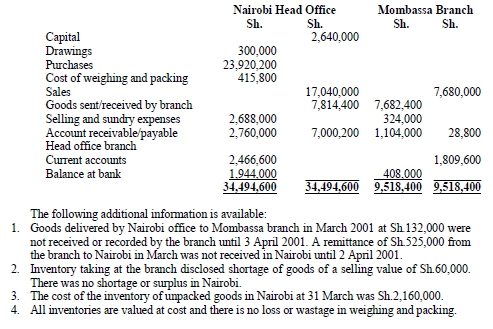

Joshua set up a business on 1 April 2000 in Nairobi with a branch in Mombasa. Purchases are made exclusively by Nairobi office where goods are weighed and packed before sale. The branch handles packed goods only from Nairobi and these are charged thereto at packed cost plus 10%. All sales by both branches are at a uniform gross profit of 25% on the packed cost.

The following balances have been extracted from the books of the business as at 31 March 2001

Date posted:

February 11, 2019

.

Answers (1)

-

Prepare the Mombasa Branch Stock Account and the Mombasa Branch Mark-up Account in the books of the Head office, and the Memorandum Trading and Profit...

(Solved)

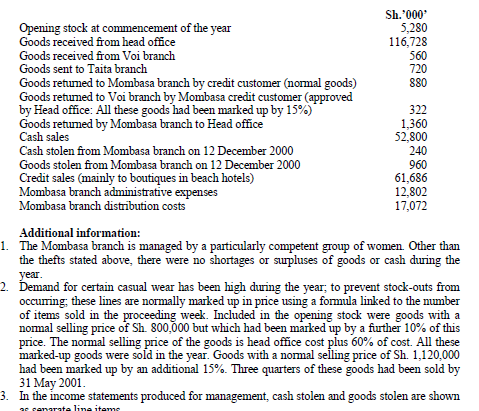

Victoria Gowns is a fashionable ladies-wear chain of clothing stores, started in Kakamega, but now present in all the major towns in Kenya and in Kampala, Uganda and in Dar-essalaam, Tanzania. The accounts of all the branches are maintained in the books of the head office, now situated in Nairobi. The figures below that refer to goods are stated at selling prices, following figures relate to transactions carried out by the Mombasa branch in the year ended 31 May 2001:

Date posted:

February 11, 2019

.

Answers (1)

-

Prepare in columnar form for the Nairobi branch, Busia branch and the combined business.

(a) The trading and profit and loss account for the year ended...

(Solved)

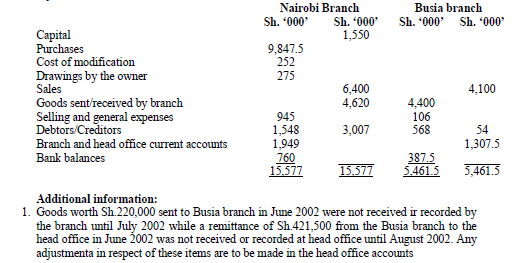

Traders Limited operates two branches one in the head office in Nairobi and the other in Busia. Purchases of stock are made exclusively by the head office branch which does some modification to the stocks before they are sold. Goods are sent to the Busia branch at modified cost plus 10% and all sales by both Busia branch and head office branch are made at a gross profit of 25% on the modified goods.

The trial balances as at 30 June 2002 before taking account of the under mentioned adjustments were:

Date posted:

February 11, 2019

.

Answers (1)

-

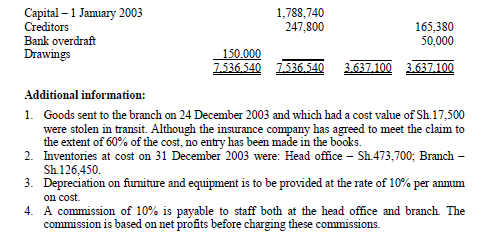

Determine:

(a) Head office and Branch profit and loss accounts for the year ended 31 December 2003.

(b) Branch current account and head office current account reconciling...

(Solved)

Mr. Mwadafu operates a sole proprietorship dealing in cement. The business has a head office in Mombasa and a branch in Athi River. The branch maintains its own books. As at 31 December 2003, the trial balances of the head office and the branch were as follows:

Date posted:

February 11, 2019

.

Answers (1)

-

Determine:

a) Branch trial balance in Kenya shillings after the necessary adjustments.

b) Trading profit and loss account (in Kenya shillings) for the head office, branch and...

(Solved)

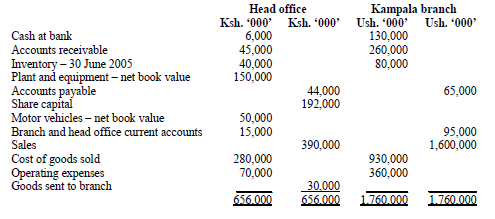

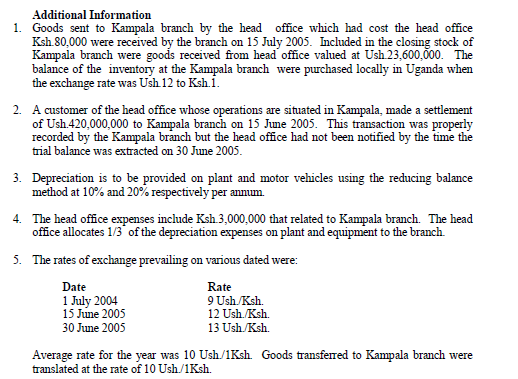

Beta East Africa Ltd. manufactures tubeless tyres at its head office plant located in Nairobi. It operates an overseas outlet at Kampala which maintains its own books of account. The tyres are transferred to the branch at head office cost plus 25% mark-up. All sales are at a uniform margin of 50%.

The trial balances extracted from the books o both the head office and the Kampala branch

as at 30 June 2005 were as follows:

Date posted:

February 11, 2019

.

Answers (1)

-

Determine:Trading profit and loss accounts for the head office, the two branches and combined business for the year ended 30 September 2008

(Solved)

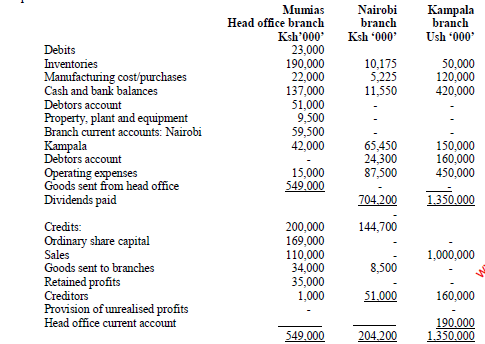

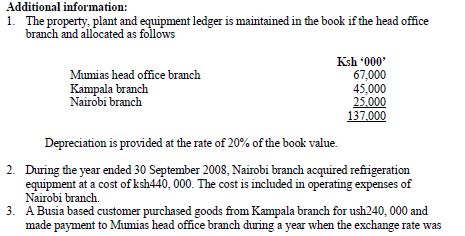

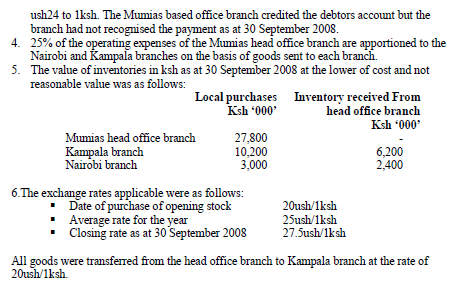

Impact Triangle ltd is a manufacturer of industrial ethanol. The head office of the company is in Mumias Kenya. The company has two other branches; one in Nairobi, Kenya and a foreign branch in Kampala Uganda. The reporting currency of the Kenya Branches is in Kenya shillings(Ksh) while the reporting currency of the Kampala branch is the Uganda Shilling(Ush)

The Nairobi and Kampala branches mainly deal with goods sent from Mumias branch. The goods are transferred from Mumias branch at a mark-up of 25% on cost to Nairobi and a margin of 25% to Kampala

The following trial balances were extracted from the books of the company as at 30 September 2008

Determine:Trading profit and loss accounts for the head office, the two branches and combined business for the year ended 30 September 2008

Date posted:

February 11, 2019

.

Answers (1)

-

Determine:

(i) Branch inventory accounts

(ii) Branch mark-up accounts

(iii) Branch debtors accounts

(iv) Branch cash accounts

(Solved)

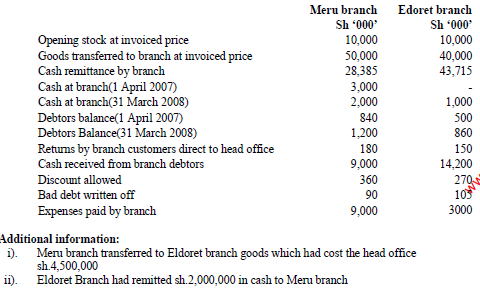

Sellwell Ltd operates a supermarket chain with a head office in Nairobi and branches in Meru and Eldoret.

Goods are transferred from the head office to Meru Branch at a mark-up of 25% and to Eldoret branch at a gross profit margin of 25%. The branches do not maintain separate books of accounts.

The following information relates to the transaction at both branches during the year ended 31 March 2008

Date posted:

February 11, 2019

.

Answers (1)

-

Briefly explain four purposes of the branch accounts to an organisation which sells goods through various outlets

(Solved)

Briefly explain four purposes of the branch accounts to an organisation which sells goods through various outlets

Date posted:

February 11, 2019

.

Answers (1)

-

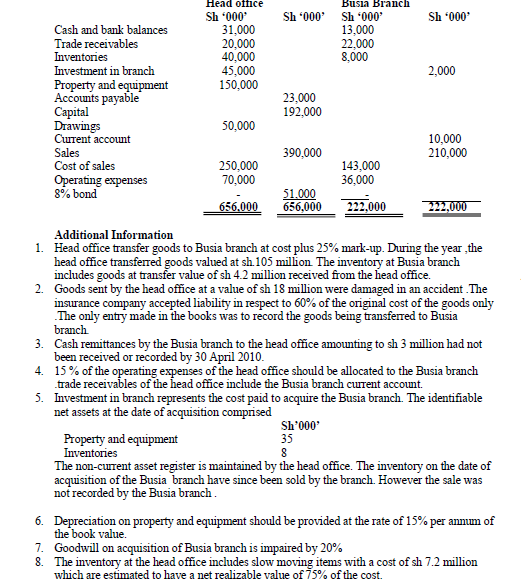

The trial balances below were extracted from the books of Shakers Enterprises with respect to its operations at the head office in Nakuru and Busia branch as at 30 April 2010.

(Solved)

The trial balances below were extracted from the books of Shakers Enterprises with respect to its operations at the head office in Nakuru and Busia branch as at 30 April 2010.

Date posted:

February 11, 2019

.

Answers (1)