P Ltd., a company incorporated in Kenya is listed in all the East African securities exchanges. P Ltd. uses the Kenya shilling (Ksh.) as the...

(Solved)

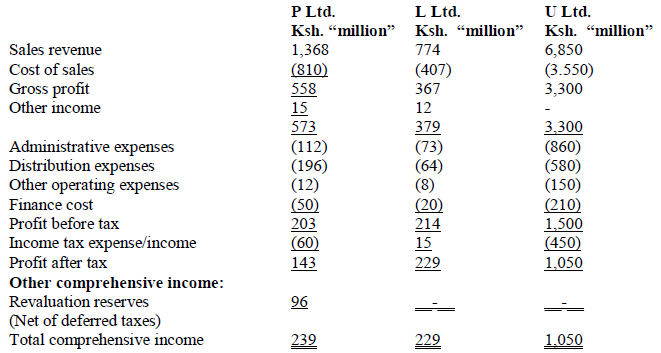

P Ltd., a company incorporated in Kenya is listed in all the East African securities exchanges. P Ltd. uses the Kenya shilling (Ksh.) as the reporting currency. On 1 April 2012, P Ltd. acquired a controlling interest in L Ltd.

On 1 October 2012, P Ltd. also acquired a controlling interest in U Ltd., a Ugandan. company that uses the Uganda shilling (Ush.) to report its financial results. The statements of comprehensive income for the three companies for the year ended 31 March 2013 are as set out below:

Additional information:

1. P Ltd. acquired 75% of L Ltd. through an exchange of 3.5 million equity shares of Ksh. 10 each.

The market value of the equity shares as at that date was Ksh.28 each. The fair value of the net assets of L Ltd, as at the date of acquisition was Ksh. 100 million.

2. P Ltd. acquired 60% of U Ltd. on 1 October 2012 for Ksh.47.5 million paid in cash. The fair value of the net assets of U Ltd. on that date amounted to Ush. 1,800 million. As at 31 March 2013, the exchange gain on retranslation of the net investment in U Ltd. was determined as Ksh.6.2 million.

3. During the year ended 31 March 2013, P Ltd. sold goods to L Ltd. for Ksh.28 million at cost plus 25%. 40% of these goods were still held within the group as at 31 March 2013.

4. P Ltd. operates some machines that pose an environmental hazard, for which they have an

irrevocable agreement to undertake decommissioning of the machines at the end of their useful life at a cost of Ksh. 18 million. The management estimates the remaining useful life of the machines to be 5 years and the relevant discount rate to be 12%. This item has not been accounted for.

5. The goodwill on acquisition of U Ltd. was considered to be impaired by 30% as at 31 March 2013.

6. On 1 January 2013, P Ltd. sold 1/3 (one third) of its investment in L Ltd. for a cash consideration of Ksh.62 million. The fair value of the net assets on that date was Ksh. 184 million. P Ltd. will account for the 50% interest in L Ltd. using the equity method in accordance with IFRS 11 (Joint Arrangements).

7. The following exchange rates are relevant:

8. Incomes and expenses of all the three companies were deemed to accrue evenly throughout the year.

Required:

(a) Goodwill on acquisition of L Ltd. and U Ltd.

(b) Consolidated statement of comprehensive income for P Ltd. for the year ended 31 March 2013. (NB: Round off the Ush. to the nearest Kenya shilling)

Date posted:

February 13, 2019

.

Answers (1)

With reference to IAS 31 (Interests in Joint Ventures), explain the three types of joint ventures.

(Solved)

With reference to IAS 31 (Interests in Joint Ventures), explain the three types of joint ventures.

Date posted:

February 13, 2019

.

Answers (1)

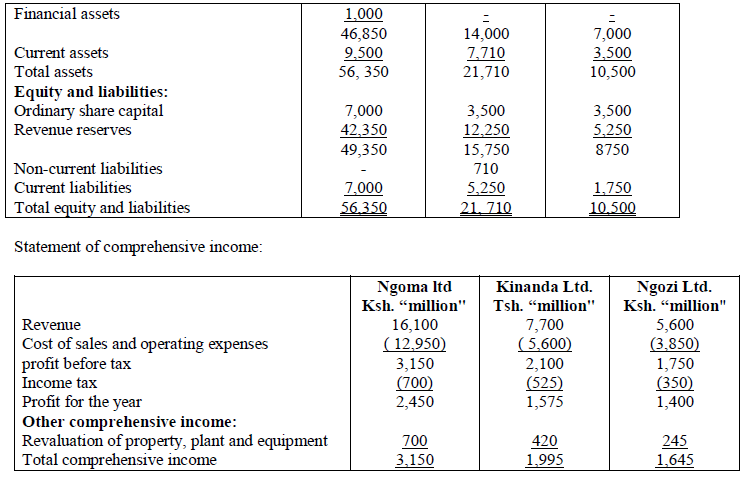

The following is an extract of the summarized financial statements of Ngoma Ltd, Kinanda Ltd. and Ngozi Ltd. for the year ended 30 September 2013:

(Solved)

The following is an extract of the summarized financial statements of Ngoma Ltd, Kinanda Ltd. and Ngozi Ltd. for the year ended 30 September 2013:

Additional information:

1. The functional currency of both Ngoma Ltd. and Ngozi Ltd. is the Kenya shilling (Ksh.) while the functional currency of Kin and a Ltd. is the Tanzania shilling (Tsh.).

2. Ngoma Ltd. acquired 80% of Kinanda Ltd. on 1 October 2011 for Ksh.18, 200 million when the revenue reserves of Kinanda Ltd. were Tsh.6, 300 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

3. Ngoma Ltd. acquired 40% of Ngozi Ltd. on 1 October 2008 for Ksh.3, 150 million when the revenue reserves of Ngozi Ltd. were Ksh.2, 450 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

4. Ngoma Ltd. advanced a 5 year loan of Ksh.1, 000 million to Kinanda Ltd. on 30 September 2012. This loan is included in the financial assets and non-current liabilities of Ngoma Ltd. and Kinanda Ltd. respectively. Kinanda Ltd. had recorded the loan at the exchange rate prevailing as at 30 September 2012.

5. An impairment test conducted on 30 September 2013 revealed that cumulative impairment losses in respect of the investment in Ngozi Ltd. were Ksh.1 ,000 million, of which Ksh.250 million related to the current financial year. No impairment losses were necessary in respect of the investment in Kinanda Ltd.

6. The group's policy is to value the non-controlling interest at fair value at the date of acquisition. The fair value of the non-controlling interest of Kinanda Ltd. at 1 October 2011 was Tsh.2, 100 million.

7. Ngoma Ltd. has a building which is located in the same country as Kinanda Ltd. The building was acquired on 30 September 2012 and is carried at a cost of Tsh.2.500 million. The property is depreciated over 10 years on a straight line basis. As at 30 September 2013, the property was revalued to Tsh.3, 500 million. Depreciation has been charged for the year but the revaluation has not been taken into account in the preparation of financial statements as at 30 September 2013.

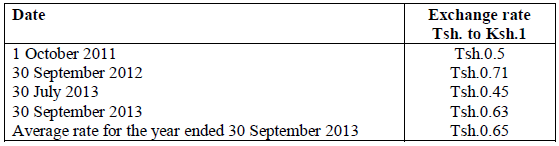

8. Relevant exchange rates are as follows:

Required:

a) Consolidated statement of comprehensive income for the year ended 30 September 2013.

b) Consolidated statement of financial position as at 30 September 2013.

Date posted:

February 13, 2019

.

Answers (1)

Explain the term 'accounting theory' and indicate why it is important in the practice of accounting.

(Solved)

Explain the term 'accounting theory' and indicate why it is important in the practice of accounting.

Date posted:

February 13, 2019

.

Answers (1)

Citing reasons, explain why it is important for a reporting entity to provide a social and environmental report in the annual financial statements.

(Solved)

Citing reasons, explain why it is important for a reporting entity to provide a social and environmental report in the annual financial statements.

Date posted:

February 13, 2019

.

Answers (1)

Many corporate boards are now agreed on the need to take responsibility for any potential or actual social impact caused by their companies’ activities. This...

(Solved)

Many corporate boards are now agreed on the need to take responsibility for any potential or actual social impact caused by their companies’ activities. This is done through a social responsibility report.

Required:

(a) Write short notes on five issues/stakeholders that may be addressed by a company’s social responsibility report.

(b) Explain five benefits that would accrue to a company from the reporting of the company’s social responsibility activities.

(c) Comparing conventional financial accounting reporting with social responsibility reporting, list and explain five challenges peculiar to social responsibility accounting

Date posted:

February 13, 2019

.

Answers (1)

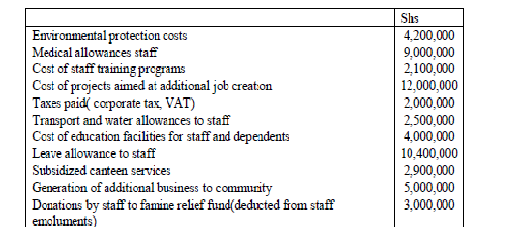

The following information was extracted from the books of Engwen Ltd. As at 30 June 2008

(Solved)

The following information was extracted from the books of Engwen Ltd. As at 30 June 2008

The company’s activities had a negative impact on the cost of living of the community, which increased by shs.3, 500,000 during the year ended 30 June 2008.

Required:

A statement of net social benefits to staff and community for the year ended 30 June 2008.

Date posted:

February 13, 2019

.

Answers (1)

The International Accounting Standards Board (IASB) is currently working with other accounting standards setting bodies in the world to have a global application of International...

(Solved)

The International Accounting Standards Board (IASB) is currently working with other accounting standards setting bodies in the world to have a global application of International Financial Reporting Standards. An important point of focus is conceptual framework.

Required:

Explain the importance of a conceptual framework and the key issues that such a framework should address.

Date posted:

February 13, 2019

.

Answers (1)

The International Accounting Standards Board (IASB) Framework for the preparation and presentation of financial statements has seven main sections. Analyse any four sections and indicate...

(Solved)

The International Accounting Standards Board (IASB) Framework for the preparation and presentation of financial statements has seven main sections. Analyse any four sections and indicate how they contribute to the quality of financial statements.

Date posted:

February 13, 2019

.

Answers (1)