-

Explain the three main types of hedge as provided in IAS 39 (Financial Instruments: Recognition and Measurement) and their accounting treatment.

(Solved)

Explain the three main types of hedge as provided in IAS 39 (Financial Instruments: Recognition and Measurement) and their accounting treatment.

Date posted:

February 14, 2019

.

Answers (1)

-

With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

(Solved)

With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

Date posted:

February 14, 2019

.

Answers (1)

-

The distinction between a provision and a contingent liability is irrelevant. Discuss.

(Solved)

The distinction between a provision and a contingent liability is irrelevant. Discuss.

Date posted:

February 14, 2019

.

Answers (1)

-

Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will...

(Solved)

Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will have on accounting for financial assets.

Date posted:

February 14, 2019

.

Answers (1)

-

(a) IAS 16: property, plant and equipment gives certain criteria to be satisfied before an item of property, plant and equipment should be recognized as...

(Solved)

(a) IAS 16: property, plant and equipment gives certain criteria to be satisfied before an item of property, plant and equipment should be recognized as an asset. State these criteria and state the value at which the asset should be measured initially. Give six examples of directly attributable costs that could be included in the value and four examples of cost that should not be included in the value.

(b) Chumuki Supermarket Limited is a quoted company which runs 22 Supermarket stores throughout Kenya. 12 of these stores are situated in and around Nairobi and all 12 are supplied by Chumuki’s central go down situated in the industrial area of Nairobi. Pricing, marketing and human resources policies are decided centrally by Chumuki. All stores are managed in the same way and management run the business on a store-by-store profit basis.

Recently, the Githurai store has seriously under performed against its budget for the year ending 31 December 2000. Rising insecurity in the area together with difficulties in obtaining access to the store have seriously adversely affected its financial performance. The Githurai store together with the Kahawa store were purchased from Ruiru Superstores on 1 January 1998 for Sh.25 million and Sh.25 million and Sh.15 million respectively plus goodwill of Sh.8 million for both stores. The stores are being depreciated on the straightline method to nil residual value over 20 years the goodwill is being amortized to nil on the straight line basis over the same period. The Githurai store could be sold for Sh.15 million net. Its value in use is Sh.20 million. Management have performed a “bottom-up” test in relation to the goodwill and the purchase prices of the stores and are satisfied that a 'top-down' test is not needed.

Required:

State in detail how the impairment loss should be recognized for the Githurai cash-generating unit in the financial Statements for the year ending 31 December 2000: neither depreciation nor amortization has yet been charged for this period. State also the carrying value of the Githurai cash-generating unit after the impairment loss has been recognized. Ignore deferred tax.

Date posted:

February 14, 2019

.

Answers (1)

-

Identify and explain five indicators which show that an impairment loss to a fixed asset may have occurred.

(Solved)

Identify and explain five indicators which show that an impairment loss to a fixed asset may have occurred.

Date posted:

February 14, 2019

.

Answers (1)

-

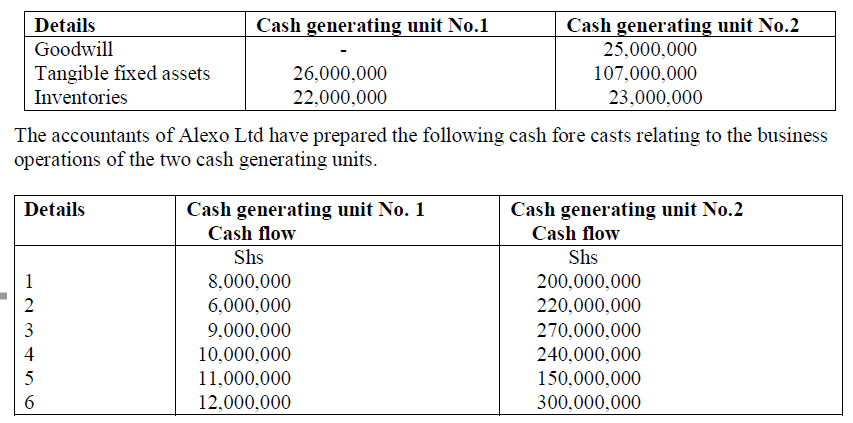

The following information is provided relating to the carrying amount of the assets comprising the cash generating units of Alexo Ltd as at 30 September...

(Solved)

The following information is provided relating to the carrying amount of the assets comprising the cash generating units of Alexo Ltd as at 30 September 2009:

Date posted:

February 14, 2019

.

Answers (1)

-

Briefly explain any three factors that may indicate that a financial asset is impaired.

(Solved)

Briefly explain any three factors that may indicate that a financial asset is impaired.

Date posted:

February 14, 2019

.

Answers (1)

-

International Financial Reporting Standard (IFRS) 6 (Exploration for and Evaluation of Mineral Resources) provides guidance on how tangible and intangible assets used to explore the...

(Solved)

International Financial Reporting Standard (IFRS) 6 (Exploration for and Evaluation of Mineral Resources) provides guidance on how tangible and intangible assets used to explore the existence of mineral resources can be accounted for and presented.

Required

Briefly explain four factors that indicate that such assets have been impaired.

Date posted:

February 14, 2019

.

Answers (1)

-

Explain how an impairment loss is measured according to IAS 36 (Impairment of Assets).

(Solved)

Explain how an impairment loss is measured according to IAS 36 (Impairment of Assets).

Date posted:

February 14, 2019

.

Answers (1)

-

On 1 January 2006, Matopeni Primary School acquired a bus at a cost of Sh.6.000.000 to enable students from a nearby village commute to school...

(Solved)

On 1 January 2006, Matopeni Primary School acquired a bus at a cost of Sh.6.000.000 to enable students from a nearby village commute to school free of charge. The school estimated that the bus had a useful life of 10 years. Or 31 December 2010, the bus sustained damage in a road accident requiring Sh. 1,200.000 to be restored to a usable condition. The restoration did not affect the useful life of the asset. The cost of a new bus to deliver a similar service was Sh.7, 500,000 as at 31 December 2010.

Required:

Evaluate the impairment loss attributable to the bus using the requirements of IPSAS 21 (Impairment of Non-Cash Generating Assets). Use the restoration cost approach.

Date posted:

February 14, 2019

.

Answers (1)

-

With reference to IPSAS 21 (Impairment of Non-Cash Generating Assets), explain the following terms:

i) Government business enterprise

ii) Carrying amount

iii) Recoverable service amount

(Solved)

With reference to IPSAS 21 (Impairment of Non-Cash Generating Assets), explain the following terms:

i) Government business enterprise

ii) Carrying amount

iii) Recoverable service amount

Date posted:

February 14, 2019

.

Answers (1)

-

a) In the context of International Accounting Standard (IAS) 21 (The Effects of Changes in Foreign Exchange Rates), explain two factors that should be considered...

(Solved)

a) In the context of International Accounting Standard (IAS) 21 (The Effects of Changes in Foreign Exchange Rates), explain two factors that should be considered in determining an entity's functional currency.

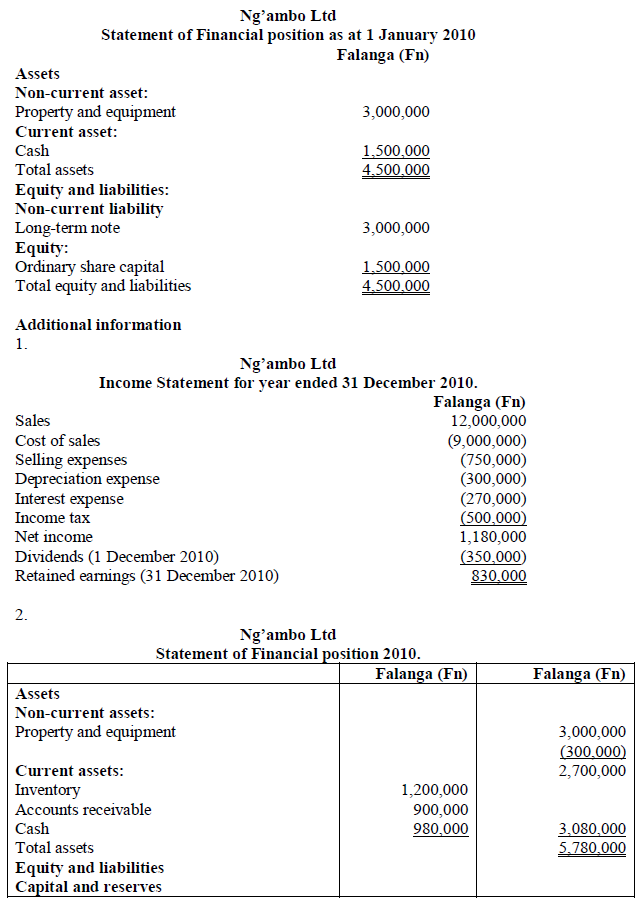

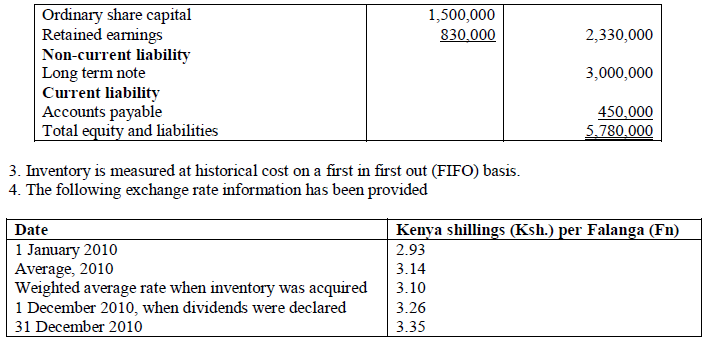

b) Ufanisi Ltd. is a Kenyan-based company that uses the Kenya Shilling (Ksh) as its presentation currency. On 1 January 2010, the company established a wholly owned

subsidiary, Ng'ambo Ltd., in a foreign country known as Ugenini, In addition to Ufanisi Ltd. making an equity investment in the subsidiary, a long term note payable to an Ugenini bank was negotiated to purchase property and equipment. The currency used in Ugenini is known as the Falanga (Fn). The subsidiary began operations with the following statement of financial position as at 1 January 2010:

Required:

Translate the following financial statements of Ng'ambo Ltd. using the temporal method:

i) Income statement for the year ended 31 December 2010.

ii) Statement of financial position as at 31 December 2010.

Date posted:

February 13, 2019

.

Answers (1)

-

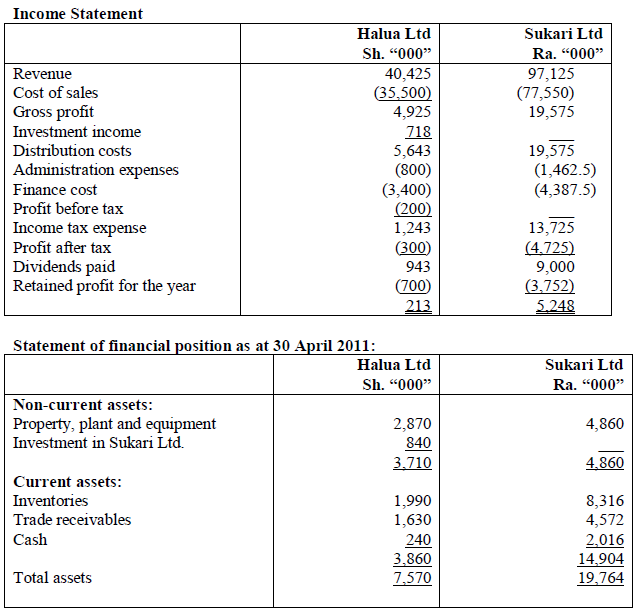

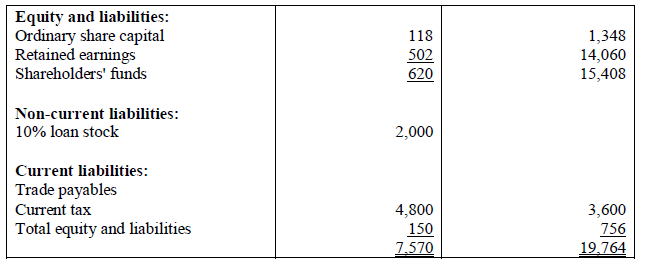

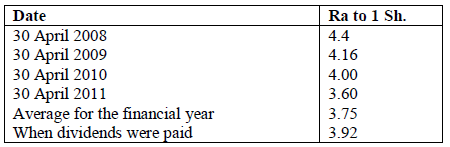

Halua Ltd., a local company, acquired 75% of the ordinary share capital of Sukari Ltd., a foreign company on 1 May 2008. Sukari Ltd.'s functional...

(Solved)

Halua Ltd., a local company, acquired 75% of the ordinary share capital of Sukari Ltd., a foreign company on 1 May 2008. Sukari Ltd.'s functional currency is the Rupia (Ra).

The following financial statements relate to the two companies for the year ended 30 April 2011:

Additional information:

1. Halua Ltd. acquired the shares in Sukari Ltd. when the retained earnings in Sukari Ltd. were Ra 2,876,000.

2. During the year, Halua Ltd. sold goods worth Sh.5 million to Sukari Ltd. and reported a gross profit margin of 20% on selling price. Half of these goods were still in the inventory of Sukari Ltd. as at the year end.

3. Included in the receivables of Halua Ltd. is Sh.500,000 due from Sukari Ltd.

4. The translation differences in the consolidated financial statements at 30 April 2010 relating to the translation of Sukari Ltd. (excluding goodwill) were Sh.208,000. Retained earnings on the same date in Sukari Ltd.'s financial statements in the post-acquisition period as at 30 April 2010 amounted to Sh. 1,372,000.

5. The group uses the partial goodwill method and no impairment loss has been reported so far.

6. The following exchange rates are relevant.

Required:

a) Consolidated income statement for the year ended 30 April 2011.

b) Consolidated statement of changes in equity for the year ended 30 April 2011.

c) Consolidated statement of financial position as at 30 April 2011.

Date posted:

February 13, 2019

.

Answers (1)

-

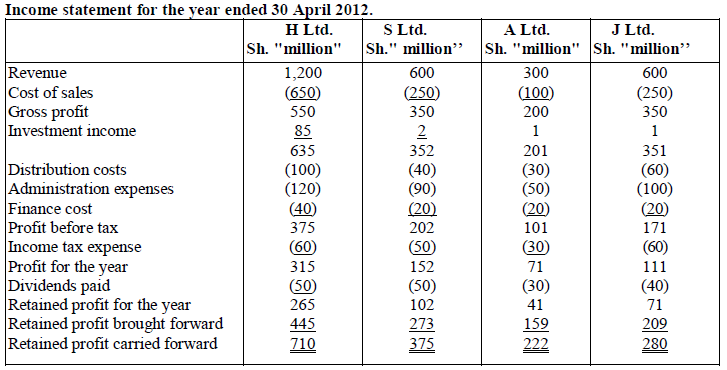

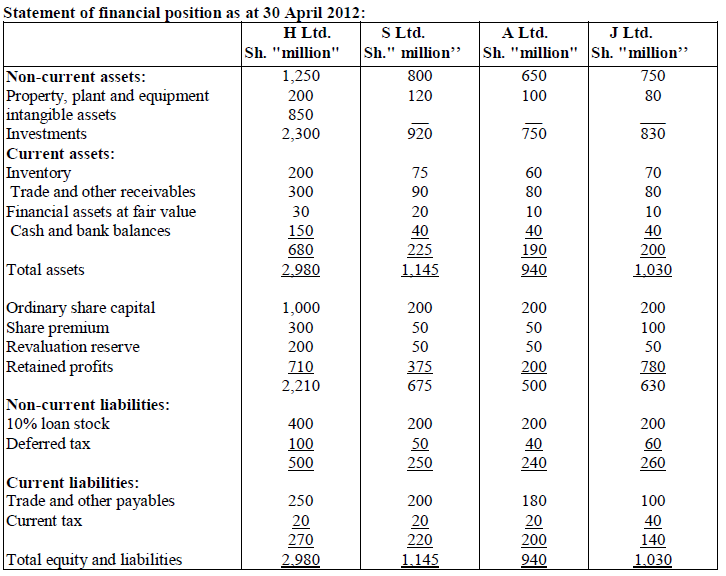

The following financial statements relate to H Ltd. and its investment companies S Ltd., A Ltd. and J Ltd. for the year ended 30 April...

(Solved)

The following financial statements relate to H Ltd. and its investment companies S Ltd., A Ltd. and J Ltd. for the year ended 30 April 2012:

Additional information:

1. H Ltd, acquired the investments in the other companies as follows:

2. The fair value of the non-controlling interest in S Ltd. was Sh.75 million on 1 May 2008.

3. During the year ended 30 April 2012, II Ltd. sold goods lo S Ltd. and A Ltd. as follows:

4. On 1 May 2010, H Ltd. sold S Ltd. an item of plant for Sli.200 million reporting a 25% profit on the initial cost plant. The group charges depreciation at 20% per annum on cost on plant.

5. All the goodwills of the three companies in which H Ltd. has invested are estimated to be impaired by 25% in the year ended 30 April 2012. No impairment losses have been reported in the past.

6. Included in trade and other receivables and trade and other payables arc the following outstanding balances:

- Due from S Ltd. to II Ltd. - Sh.50 million

- Due from A Ltd. to II Ltd. - Sh.10 million

- Due from H Ltd. to J Ltd. - Sh.40 million

In the books of S Ltd. the amount due to H Ltd. was shown at Sh.40 million because S Ltd. had sent a cheque Sh.10 million but H Ltd. had not recorded the cheque. All the other balances were in agreement.

7. The group uses the full goodwill method and proportionate consolidation as per IAS 31 (Joint Ventures).

8. All dividends and interest had been paid by the end of the year.

Required:

a) Consolidated income statement for the year ended 30 April 2012.

b) Consolidated statement of financial position as at 30 April 2012.

Date posted:

February 13, 2019

.

Answers (1)

-

Explain the following terms as used in IAS 21 (The Effects of Changes in Foreign Exchange Rates):

i) Functional currency.

ii) Presentation currency.

(Solved)

Explain the following terms as used in IAS 21 (The Effects of Changes in Foreign Exchange Rates):

i) Functional currency.

ii) Presentation currency.

Date posted:

February 13, 2019

.

Answers (1)

-

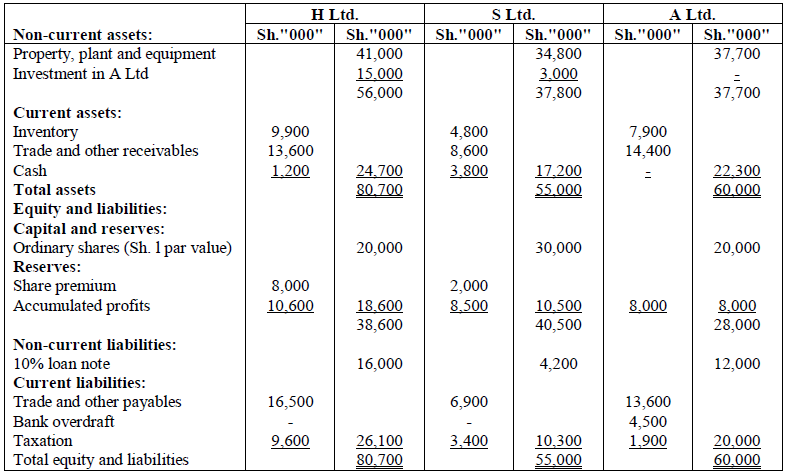

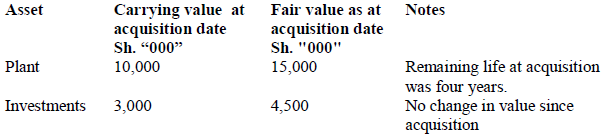

a) In the context of IAS 21 (The Effects of Changes in Foreign Exchange Rates), critically appraise the concepts on which the closing rate and...

(Solved)

a) In the context of IAS 21 (The Effects of Changes in Foreign Exchange Rates), critically appraise the concepts on which the closing rate and the temporal methods are based indicating which factors should be taken into account when choosing between the two methods.

b) H Ltd., a publicly listed company, acquired the following investments:

- On 1 April 2012, the company purchased 24 million shares in S Ltd. This acquisition was made by way of an immediate share exchange of two shares in H Ltd. for every three shares in S Ltd. plus a cash payment of Sh. l per one share of S Ltd. This cash payment will be payable on 1 April 2015. The market price of H Ltd.'s shares on 1 April 2012 was Sh.2 each.

- On 1 October 2012, the company purchased 6 million shares in A Ltd. by paying an immediate Sh.2.50 in cash for each share.

The statements of financial position of H Ltd., S Ltd. and A Ltd. as at 31 March 2013 were as follows:

Additional information:

1. Below is a summary of the results of a fair value exercise S Ltd. carried out as at the date of acquisition:

The book values of the net assets of A Ltd as at the date of acquisition were considered to be a reasonable approximation to their fair values.

2. The profits of S Ltd. and A Ltd. for the year to 3 1 March 2013 were Sh.4.5 million and Sh.6 million respectively. No dividends have been paid by any of the companies during the year. Profits are deemed to accrue evenly throughout the year.

3. In January 2013, A Ltd. sold goods to H Ltd. at a selling price of Sh.4 million. These goods had cost A Ltd. Sh.2.4 million. H Ltd. had Sh.2.5 million (at cost to H Ltd.) of these goods still in inventory as at 31 March 2013.

4. Depreciation is charged on a straight-line basis. A full year's depreciation is charged in the year of acquisition.

5. Based on H Ltd.'s cost of capital which is 10% per annum. Sh. l receivable in three years' time can be taken to have a present value of Sh.0.75.

6. H Ltd. has not yet accounted for the acquisition of S Ltd. but has recorded the investment in A Ltd.

Required:

Consolidated statement of financial position as at 31 March 2013 in accordance with international financial reporting standards (IFRSs)

Date posted:

February 13, 2019

.

Answers (1)

-

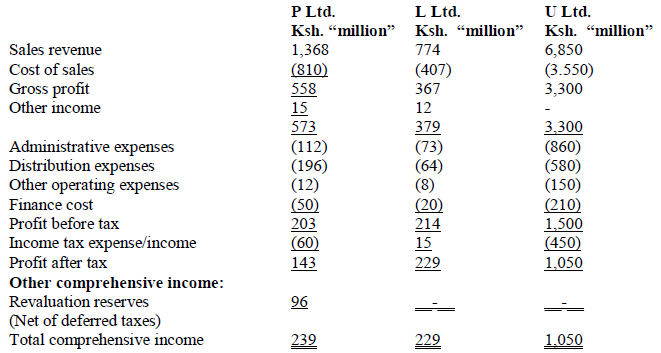

P Ltd., a company incorporated in Kenya is listed in all the East African securities exchanges. P Ltd. uses the Kenya shilling (Ksh.) as the...

(Solved)

P Ltd., a company incorporated in Kenya is listed in all the East African securities exchanges. P Ltd. uses the Kenya shilling (Ksh.) as the reporting currency. On 1 April 2012, P Ltd. acquired a controlling interest in L Ltd.

On 1 October 2012, P Ltd. also acquired a controlling interest in U Ltd., a Ugandan. company that uses the Uganda shilling (Ush.) to report its financial results. The statements of comprehensive income for the three companies for the year ended 31 March 2013 are as set out below:

Additional information:

1. P Ltd. acquired 75% of L Ltd. through an exchange of 3.5 million equity shares of Ksh. 10 each.

The market value of the equity shares as at that date was Ksh.28 each. The fair value of the net assets of L Ltd, as at the date of acquisition was Ksh. 100 million.

2. P Ltd. acquired 60% of U Ltd. on 1 October 2012 for Ksh.47.5 million paid in cash. The fair value of the net assets of U Ltd. on that date amounted to Ush. 1,800 million. As at 31 March 2013, the exchange gain on retranslation of the net investment in U Ltd. was determined as Ksh.6.2 million.

3. During the year ended 31 March 2013, P Ltd. sold goods to L Ltd. for Ksh.28 million at cost plus 25%. 40% of these goods were still held within the group as at 31 March 2013.

4. P Ltd. operates some machines that pose an environmental hazard, for which they have an

irrevocable agreement to undertake decommissioning of the machines at the end of their useful life at a cost of Ksh. 18 million. The management estimates the remaining useful life of the machines to be 5 years and the relevant discount rate to be 12%. This item has not been accounted for.

5. The goodwill on acquisition of U Ltd. was considered to be impaired by 30% as at 31 March 2013.

6. On 1 January 2013, P Ltd. sold 1/3 (one third) of its investment in L Ltd. for a cash consideration of Ksh.62 million. The fair value of the net assets on that date was Ksh. 184 million. P Ltd. will account for the 50% interest in L Ltd. using the equity method in accordance with IFRS 11 (Joint Arrangements).

7. The following exchange rates are relevant:

8. Incomes and expenses of all the three companies were deemed to accrue evenly throughout the year.

Required:

(a) Goodwill on acquisition of L Ltd. and U Ltd.

(b) Consolidated statement of comprehensive income for P Ltd. for the year ended 31 March 2013. (NB: Round off the Ush. to the nearest Kenya shilling)

Date posted:

February 13, 2019

.

Answers (1)

-

With reference to IAS 31 (Interests in Joint Ventures), explain the three types of joint ventures.

(Solved)

With reference to IAS 31 (Interests in Joint Ventures), explain the three types of joint ventures.

Date posted:

February 13, 2019

.

Answers (1)

-

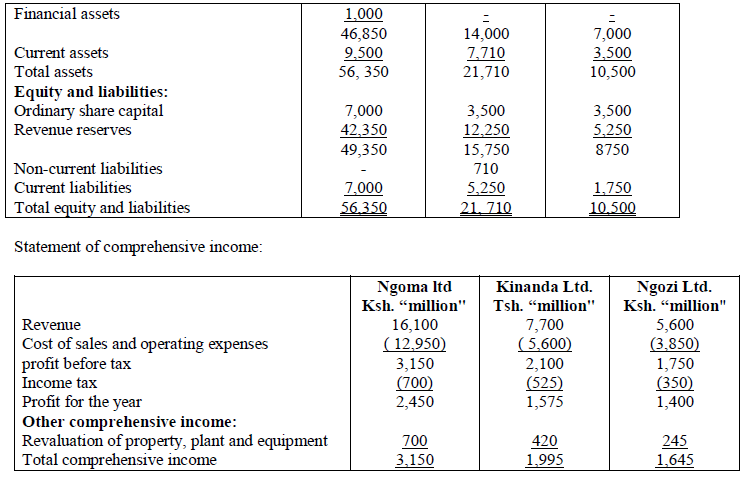

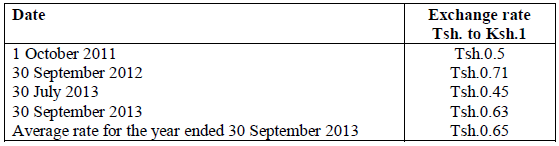

The following is an extract of the summarized financial statements of Ngoma Ltd, Kinanda Ltd. and Ngozi Ltd. for the year ended 30 September 2013:

(Solved)

The following is an extract of the summarized financial statements of Ngoma Ltd, Kinanda Ltd. and Ngozi Ltd. for the year ended 30 September 2013:

Additional information:

1. The functional currency of both Ngoma Ltd. and Ngozi Ltd. is the Kenya shilling (Ksh.) while the functional currency of Kin and a Ltd. is the Tanzania shilling (Tsh.).

2. Ngoma Ltd. acquired 80% of Kinanda Ltd. on 1 October 2011 for Ksh.18, 200 million when the revenue reserves of Kinanda Ltd. were Tsh.6, 300 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

3. Ngoma Ltd. acquired 40% of Ngozi Ltd. on 1 October 2008 for Ksh.3, 150 million when the revenue reserves of Ngozi Ltd. were Ksh.2, 450 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

4. Ngoma Ltd. advanced a 5 year loan of Ksh.1, 000 million to Kinanda Ltd. on 30 September 2012. This loan is included in the financial assets and non-current liabilities of Ngoma Ltd. and Kinanda Ltd. respectively. Kinanda Ltd. had recorded the loan at the exchange rate prevailing as at 30 September 2012.

5. An impairment test conducted on 30 September 2013 revealed that cumulative impairment losses in respect of the investment in Ngozi Ltd. were Ksh.1 ,000 million, of which Ksh.250 million related to the current financial year. No impairment losses were necessary in respect of the investment in Kinanda Ltd.

6. The group's policy is to value the non-controlling interest at fair value at the date of acquisition. The fair value of the non-controlling interest of Kinanda Ltd. at 1 October 2011 was Tsh.2, 100 million.

7. Ngoma Ltd. has a building which is located in the same country as Kinanda Ltd. The building was acquired on 30 September 2012 and is carried at a cost of Tsh.2.500 million. The property is depreciated over 10 years on a straight line basis. As at 30 September 2013, the property was revalued to Tsh.3, 500 million. Depreciation has been charged for the year but the revaluation has not been taken into account in the preparation of financial statements as at 30 September 2013.

8. Relevant exchange rates are as follows:

Required:

a) Consolidated statement of comprehensive income for the year ended 30 September 2013.

b) Consolidated statement of financial position as at 30 September 2013.

Date posted:

February 13, 2019

.

Answers (1)