-

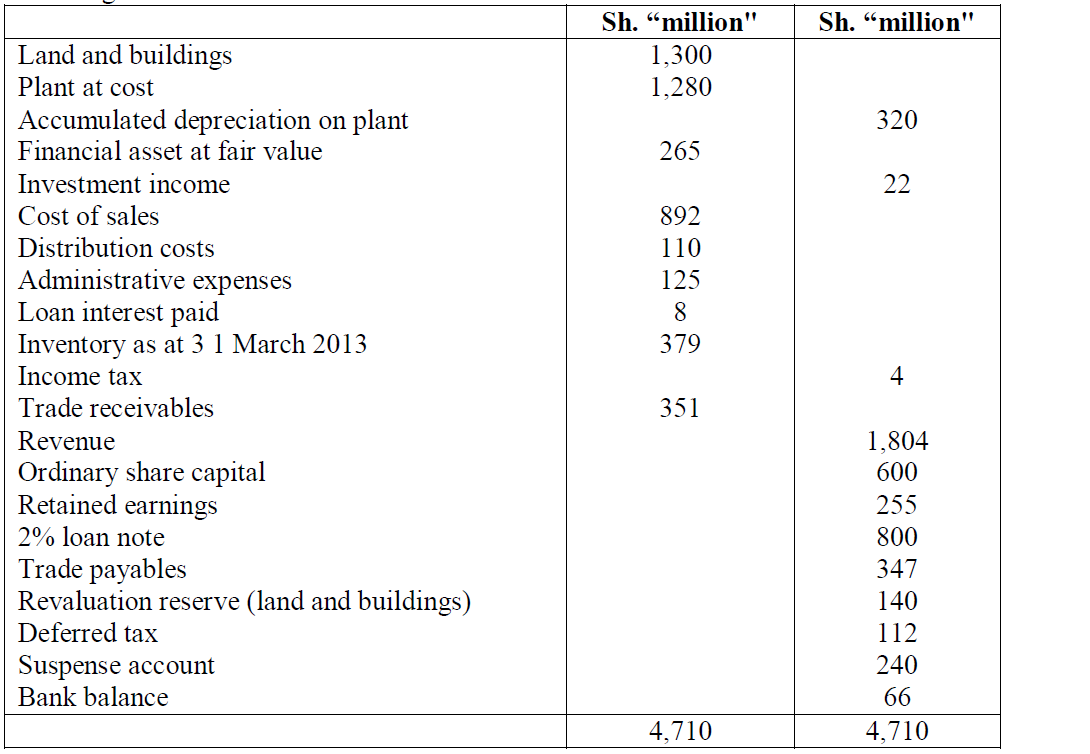

The following trial balance relates to Ndovu Limited as at 31 March 2013:

(Solved)

The following trial balance relates to Ndovu Limited as at 31 March 2013:

Additional information:

1. The value of land in the trial balance is given as Sh.300 million. The buildings were revalued on 31 March 2013 at Sh.920 million. The estimated useful life of buildings was 20 years as at 1 April 2012. Depreciation on buildings is charged at 60% to cost of sales and 20% each to distribution costs and administrative expenses.

2. The company constructed its own plant at a total cost of Sh.240 million. The plant was brought into use on 1 October 2012 but its cost had not been capitalized. Instead, its cost had been included in the cost of sales. Plant is depreciated at 12.5% per annum using the reducing balance method (time apportioned) and charged to the cost of sales.

3. The fair value of the investments held at fair value was Sh.271 million as at 3 1 March 2013.

4. The balance of tax on the trial balance represents an overprovision of previous years" tax.

The estimate of tax for the current year is Sh.187 million. At 31 March 2013, there were Sh.400 million of taxable temporary differences. For deferred, tax assume an average tax rate of 30%.

5. The 2% loan note was issued on 1 October 2012 under the terms that require a large premium on repayment. The effective interest rate therefore is 6% per annum.

6. The suspense account relates to a rights issue of shares that was made on 1 January 2013. The terms of the issue were one share for every four held at Sh.8 per share. The par value of each share is Sh.5. The issue was fully subscribed.

Required:

Prepare the following statements in a format suitable for publication:

a) Statement of comprehensive income for the year ended 31 March 2013.

b) Statement of financial position as at 31 March 2013.

Date posted:

February 14, 2019

.

Answers (1)

-

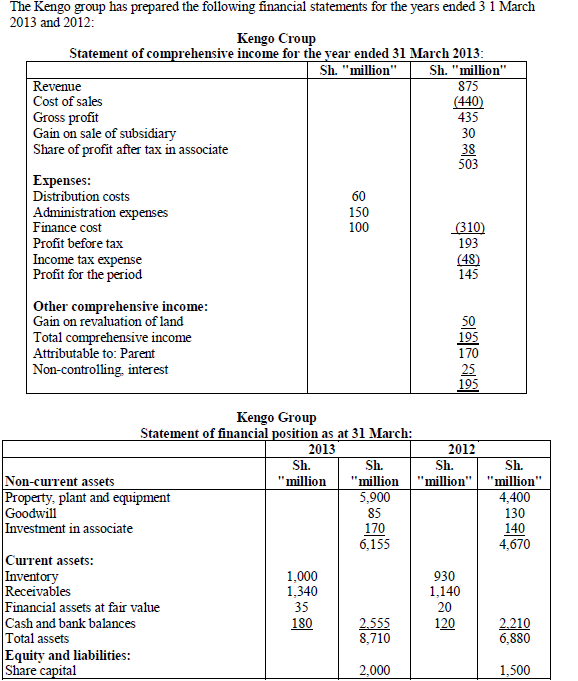

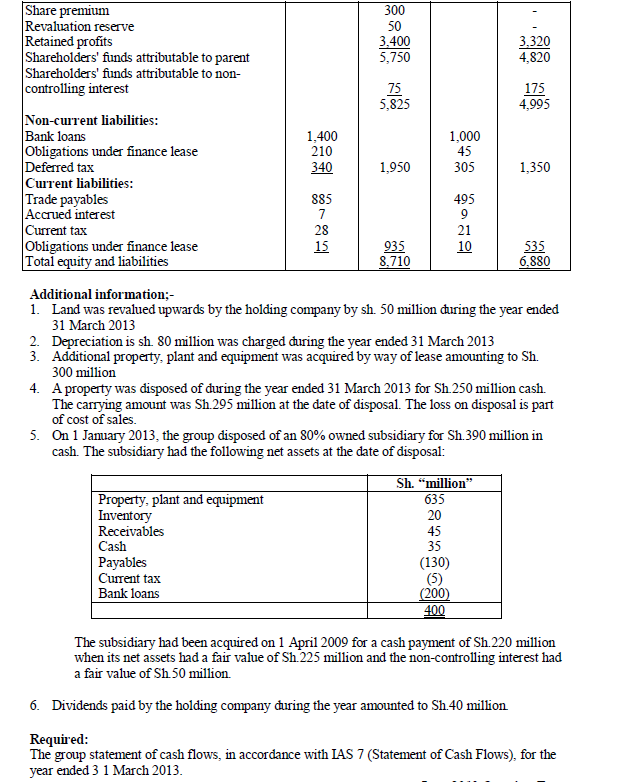

The Kengo group has prepared the following financial statements for the years ended 31st March 2013 and 2012:

(Solved)

The Kengo group has prepared the following financial statements for the years ended 31st March 2013 and 2012:

Date posted:

February 14, 2019

.

Answers (1)

-

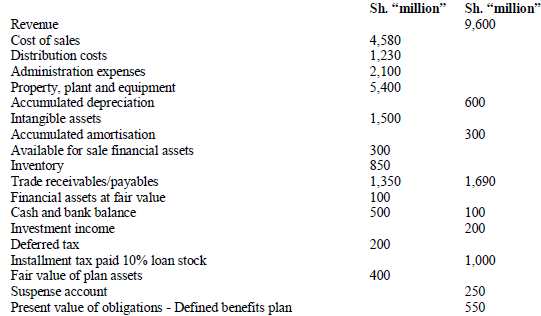

The following trial balance relates to Mapema Limited, a quoted company, as at 30 April 2013:

(Solved)

The following trial balance relates to Mapema Limited, a quoted company, as at 30 April 2013:

Required:

Prepare for publication purposes:

a) A statement of comprehensive income for the year ended 30 April 2013.

b) A statement of changes in equity for the year ended 30 April 2013.

c) A statement of financial position as at 30 April 2013.

Date posted:

February 14, 2019

.

Answers (1)

-

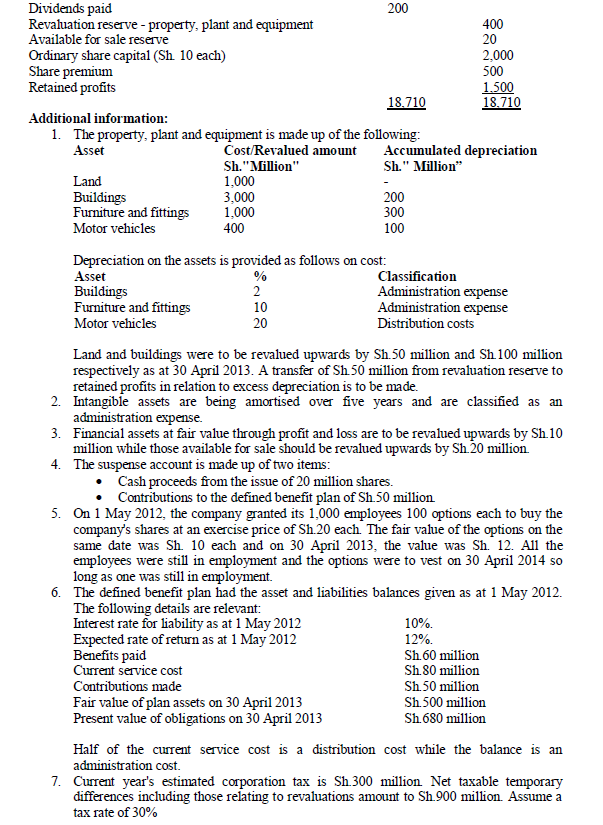

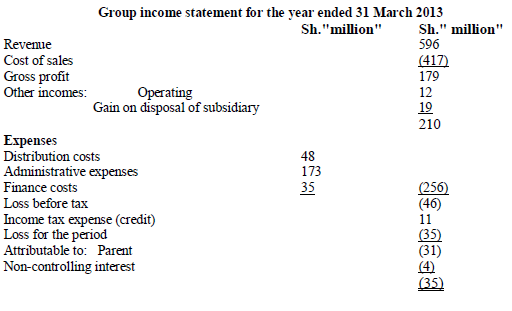

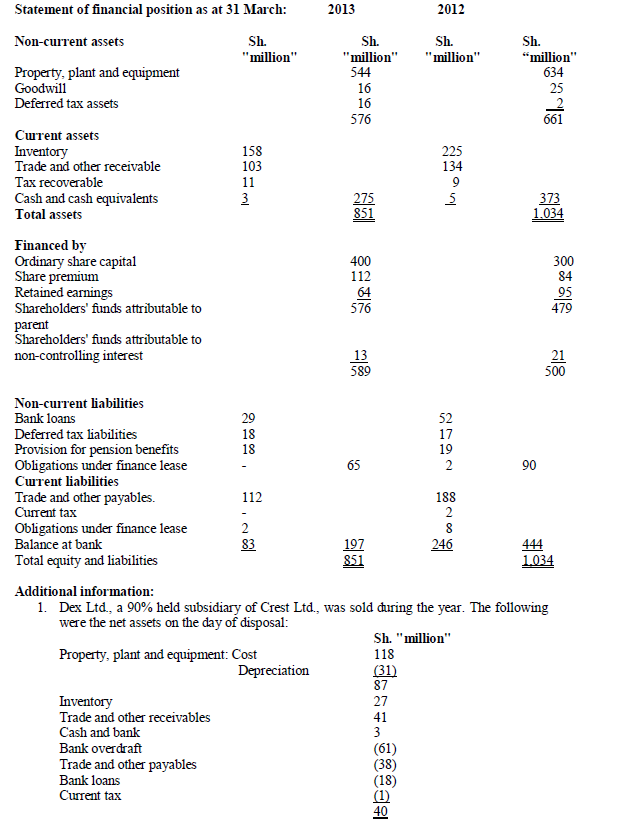

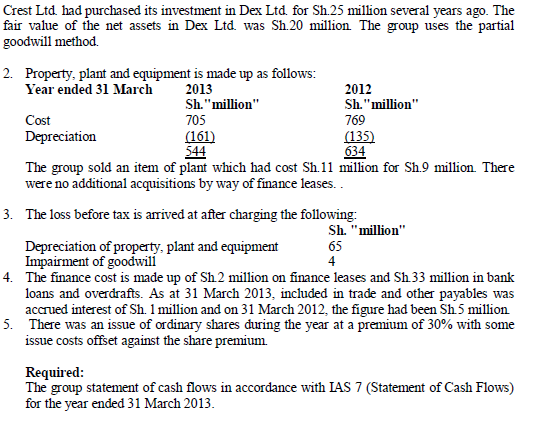

The following financial statements relate to the Crest group for the year ended 31 March 2013:

(Solved)

The following financial statements relate to the Crest group for the year ended 31 March 2013:

Date posted:

February 14, 2019

.

Answers (1)

-

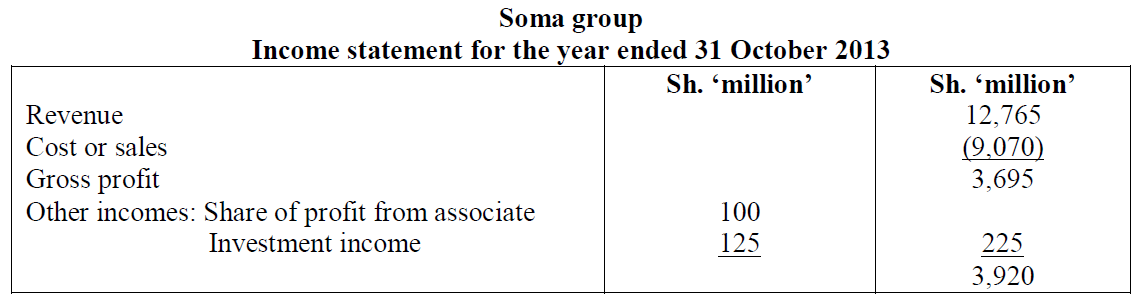

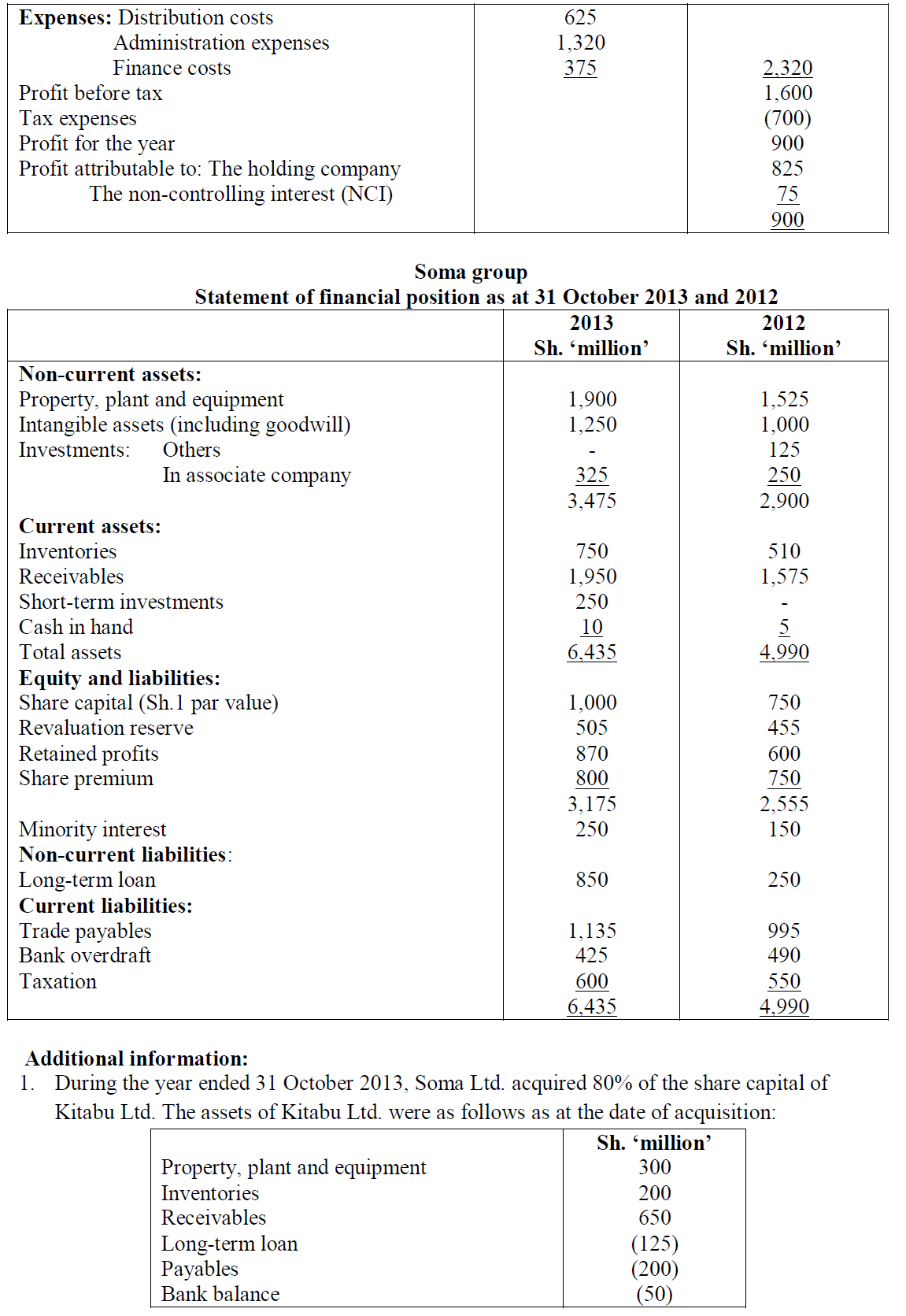

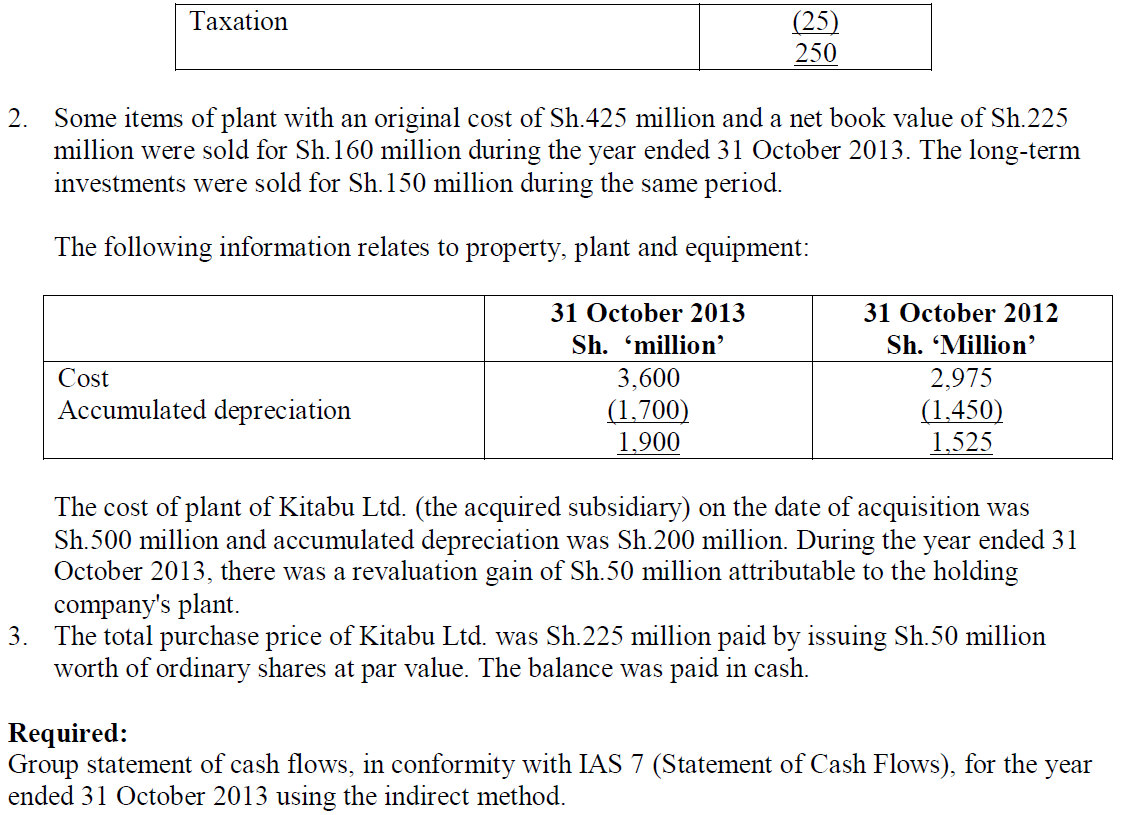

The following are the group income statement and group statement or financial position of Soma group of companies, for the financial year ended 31 October...

(Solved)

The following are the group income statement and group statement or financial position of Soma group of companies, for the financial year ended 31 October 2013:

Date posted:

February 14, 2019

.

Answers (1)

-

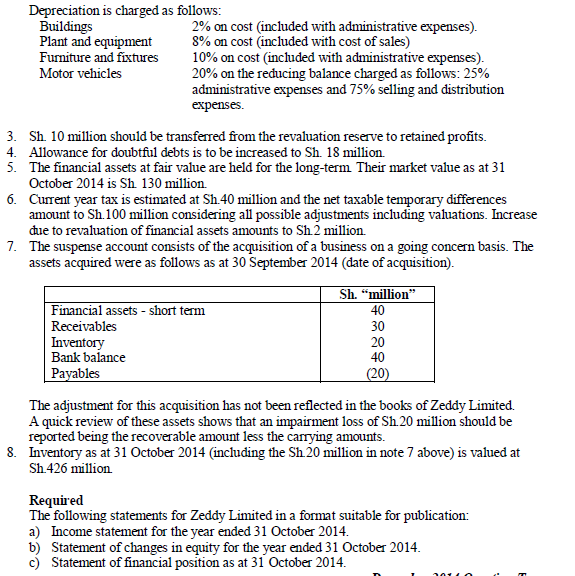

Zeddy Limited is a company quoted at the securities exchange. The following trial balance was extracted from the books of the company as at 31...

(Solved)

Zeddy Limited is a company quoted at the securities exchange. The following trial balance was extracted from the books of the company as at 31 October 2014:

Date posted:

February 14, 2019

.

Answers (1)

-

Explain the meaning of the following terms as used in pension accounts

(i) Funded schemes.

(ii) Experience adjustments.

(Solved)

Explain the meaning of the following terms as used in pension accounts

(i) Funded schemes.

(ii) Experience adjustments.

Date posted:

February 14, 2019

.

Answers (1)

-

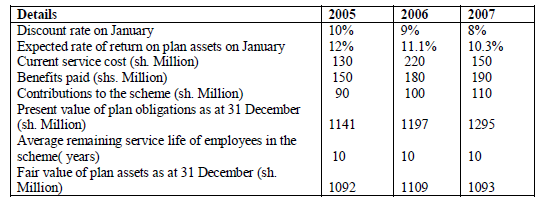

The following relates to Waastaafu Retirement Benefits Scheme, a defined benefit plan, for the years ended 31 December 2005, 2006, and 2007:

(Solved)

The following relates to Waastaafu Retirement Benefits Scheme, a defined benefit plan, for the years ended 31 December 2005, 2006, and 2007:

Additional information:

1. As at 1 January 2005, the present value of plan obligations and fair value of plan assets were both sh. 1000 million.

2. Net cumulative unrecognized actuarial gains as at 1 January 2005 were sh. 140 million.

3. Assume all transactions occurred at the year end.

Required:

i) Actuarial gains or losses on the present value of plan obligations.

ii) Actuarial gains or losses on fair value of plan assets.

iii) Net pension cost to be charged in the income statement.

iv) Scheme balances to be reflected in the balance sheet

Date posted:

February 14, 2019

.

Answers (1)

-

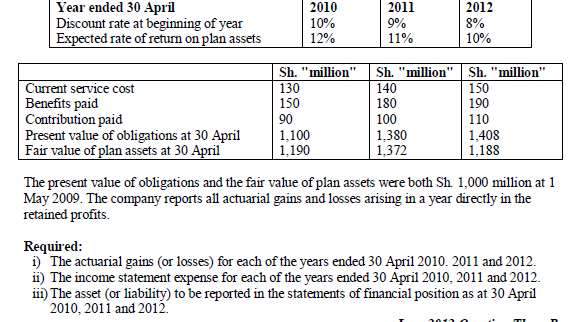

Zedkey Ltd. operates a defined benefit pension plan The following financial data relates to the scheme for the past three years ended 30 April 2012:

(Solved)

Zedkey Ltd. operates a defined benefit pension plan The following financial data relates to the scheme for the past three years ended 30 April 2012:

Date posted:

February 14, 2019

.

Answers (1)

-

In the context of IAS 19 (Employee Benefits), evaluate:

(i) When an amount should be recognized as a defined benefit liability.

(ii) The treatment of actuarial gains...

(Solved)

In the context of IAS 19 (Employee Benefits), evaluate:

(i) When an amount should be recognized as a defined benefit liability.

(ii) The treatment of actuarial gains or losses.

(iii) The items that should be recognized in the income statement.

Date posted:

February 14, 2019

.

Answers (1)

-

With reference to IFRS 2 'Share Based Payments', outline three types of share based payment transactions.

(Solved)

With reference to IFRS 2 'Share Based Payments', outline three types of share based payment transactions.

Date posted:

February 14, 2019

.

Answers (1)

-

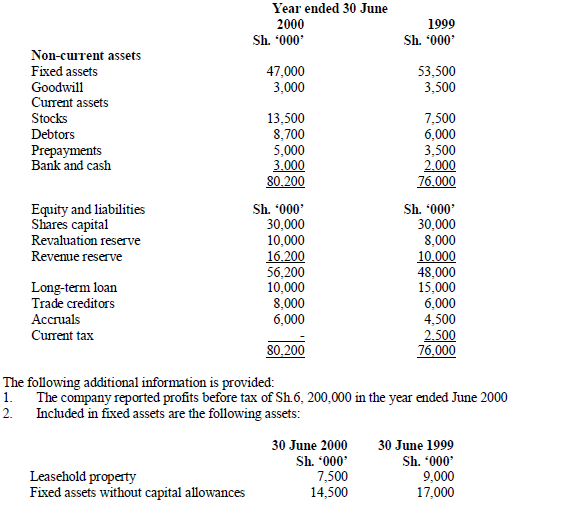

Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000,...

(Solved)

Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000, the company changed to deferred tax method and the new policy was to be applied retroactively to the accounts of the years ended 30 June 1999 and 2000.

The following are the balance sheets of the company for the two years ended 30 June 1999 and 2000 before incorporating tax expense for the year 2000

No acquisition or disposal of fixed assets took place in the year ended 30 June 2000

3. Written down value of fixed assets were Sh.22, 500,000 and Sh.18, 000,000 as at 30 June 1999 and 2000 respectively

4. Stocks as at 30 June 2000 are net of a general provision for price fluctuation of 10% of the cost. The provision is not allowed for tax purposes.

5. Accruals include leave passage provision of Sh.2, 500,000 as at 30 June 1999 and Sh.1, 800,000 as at June 2000

6. Prepayments for the year 2000 include Sh.2, 000,000 allowed as a deduction on computation of current tax.

7. Assets subjects to wear and tear allowance were first revalued in 1999 and revaluation repeated in 2000. No adjustments were made to the tax base of the assets following the revaluations.

8. Foreign exchange loss balances amounted to Sh.3, 600,000 and Sh.2, 800,000 on 30 June 1999 and 2000 respectively.

9. Donations in the year 2000 were Sh.5, 000,000.

10 Tax rates in 1999 and 2000 were 40% and 50% respectively.

Current tax for a year is paid on 15 September of the following financial year.

Required:

a) Current tax for the year ended 30 June 2000

b) Using the method recommended by the revised IAS 12, calculate deferred tax expense or income for the years 1999 and 2000

c) The current tax account, deferred tax account and revaluation account for the years 1999 and 2000

Date posted:

February 14, 2019

.

Answers (1)

-

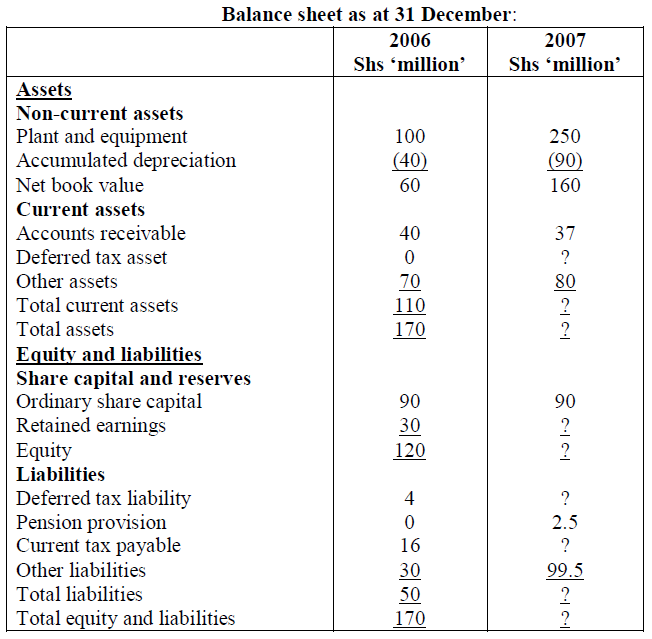

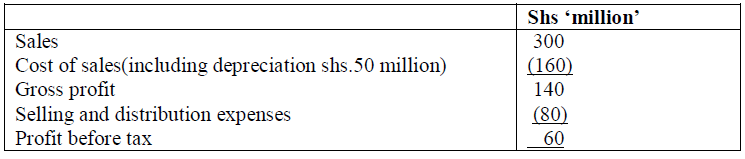

The following incomplete balance sheet relate to Concorde Ltd for the years ended 31 December 2007:

(Solved)

The following incomplete balance sheet relate to Concorde Ltd for the years ended 31 December 2007:

Additional information:

1. The company reported an accounting profit before tax of sh.60 million for the year ended 31 December 2007. This profit was arrived at as shown below:

2. The company declared a dividend of sh.10 million for the year ended 31 December 2007.

3. Depreciation on plant and equipment is provided at the rate of 20% on straight-line basis. Plant and equipment qualify for capital allowances at the rate of 25% of cost on straight –line basis.

4. Accumulated tax depreciation as at 31 December 2006 was sh.50 million. On 1 February 2007, the company purchased additional costing sh.150 million. The company’s policy is to charge a full year’s depreciation in the year of purchase and none in the year of disposal.

5. Included in selling and distribution expenses is sh.5 million representing an expense which was disallowed by the tax authorities.

6. The company charged the income statement with sh.14 million representing pension costs for the year ended 31 December 2007. Sh.11.5 million of this amount was allowed for tax purposes.

7. The company made a general provision for bad debts of sh.3 million for the year ended 31 December 2007. There were no bad debts written off during the year.

8. On 31 July 2007, the company made a tax payment of sh.15 million.

9. Corporation rate of tax is 30%.

10. The company separately accounts for deductible and taxable temporary differences.

Required:

i) Determine the charge in the income statement for current tax and deferred tax expenses.

ii) Prepare the income statement showing the retained profit balance.

iii) Prepare the complete balance sheet.

Date posted:

February 14, 2019

.

Answers (1)

-

Maji Limited had a deferred tax liability of Sh. 105 million as at 1 June 2010. During the year ended 31 May 2011, the...

(Solved)

Maji Limited had a deferred tax liability of Sh. 105 million as at 1 June 2010. During the year ended 31 May 2011, the company had the following items with regard to estimating deferred tax:

1. The carrying amount of property, plant and equipment as at 31 May 2011 was Sh.980 million. This included some buildings which were revalued upwards by Sh 50 million at 31 May 2010 which had a remaining useful life of 10 years at that date. The company's accounting policy is to treat revaluation surpluses as realized on disposal of the revalued assets. The tax base of property, plant and equipment as at 31 May 2011 was Sh 640 million.

2. Deferred development expenditure amounted to Sh.45 million at year end (Sh.40 million as at 31 May 2010). Sh.10 million of additional development expenditure was incurred during the year and the remaining difference between 2010 and 2011 figures relates to development expenditure amortized for products that have started being commercially produced. All development expenditure is allowed for tax purposes.

3. Included in current assets is an amount of Sh.40 million due in respect of some patent royalties on one of the company's older products which is now being produced by other companies. Patent royalties are taxed only when received.

4. The company’s tax rate proposals.

Required:

i) The deferred tax balance as at 31 May 2011 and the relevant journal entry.

ii) The directors of Maji Limited have proposed that deferred tax should be discounted and also provided on the share of post-acquisition profits in its subsidiary and associate companies.

Comment on these proposals.

Date posted:

February 14, 2019

.

Answers (1)

-

Lami Limited had a deferred tax liability as at I May 2011 of Sh.100 million. For the purposes of preparing financial statements for the year...

(Solved)

Lami Limited had a deferred tax liability as at I May 2011 of Sh.100 million. For the purposes of preparing financial statements for the year ended 30 April 2012, the following additional information is available:

1. Property, plant and equipment has a carrying amount of Sh.1,200 million and a tax base of Sh.1,000 million. Some land and buildings were revalued upwards by Sh.50 million during the year ended 30 April 2012.

2. Intangible assets consisting of trade licences being amortized over five years had a carrying amount of Sh 60 million. This was allowed for tax purposes in full two years ago.

3. The company has available for sale financial assets with a carrying amount of Sh.20 million and financial assets at fair value through profit and loss of Sh. 10 million. Both financial assets reported losses in fair value of Sh.2 million each as at 30 April 2012.

4. Inventory is shown at the lower of cost and net realisable value. The cost is Sh.800 million while the net realizable value is Sh.780 million.

5. Receivables had a carrying amount of Sh.500,million after making an allowance for doubtful debt of Sh.20 million and an exchange gain of Sh.40 million (unrealized). Both the allowance and exchange gain arc not allowed for tax purposes.

6. Trade and other payable are stated at Sh. 900 million after making provision for discount of Sh. 10 million.

7. Assume a tax rate of 30%.

Required

i) Compute the relevant temporary differences.

ii) Show the journal entry to record changes in the deferred tax liability

Date posted:

February 14, 2019

.

Answers (1)

-

Justify the provision of deferred tax using temporary differences in the financial statements of a reporting entity.

(Solved)

Justify the provision of deferred tax using temporary differences in the financial statements of a reporting entity.

Date posted:

February 14, 2019

.

Answers (1)

-

IAS 32 'Financial Instruments: Disclosure and Presentation' states that the purpose of the disclosures required by this standard is to provide information that will enhance...

(Solved)

IAS 32 'Financial Instruments: Disclosure and Presentation' states that the purpose of the disclosures required by this standard is to provide information that will enhance understanding of the significance of on-balance-sheet and off-balance-sheet financial instruments to an enterprise’s financial position, performance and cash flow and assist in assessing the amounts, timing and certainty of future cash flows associated with those instruments. State and briefly describe three types of financial risks described in the standard, in relation to transactions in financial instruments.

Date posted:

February 14, 2019

.

Answers (1)

-

With reference to IAS 39(Financial Instruments: Recognition and Measurement), explain how financial instruments are initially recognized and subsequently measured in the books of a reporting...

(Solved)

With reference to IAS 39(Financial Instruments: Recognition and Measurement), explain how financial instruments are initially recognized and subsequently measured in the books of a reporting entity.

Date posted:

February 14, 2019

.

Answers (1)

-

With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

(Solved)

With reference to IAS 37 (Provisions, Contingent Liabilities and Contingent Assets), differentiate between a 'constructive obligation' and a 'contingent liability'.

Date posted:

February 14, 2019

.

Answers (1)

-

Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will...

(Solved)

Discuss the approach taken by International Financial Reporting Standard (IFRS) 9 in measuring and classifying financial assets and the main effect that IFRS 9 will have on accounting for financial assets.

Date posted:

February 14, 2019

.

Answers (1)