Tax incentives that have contributed to growth of financial markets in Kenya

- Capital gains are exempted from taxation

- Withholding tax on dividends of 5% is final.

- Flotation cost of securities is an allowable expense.

- Companies which issue a given percentage of shares to the public through the stock markets are taxed at a lower rate.

- The interest on government infrastructure bond is exempt from tax

- Venture capital companies enjoy a 10 year tax holiday

- Income from collective investments schemes is not taxable

- Stock taking services are zero rated. This enables firms to improve on accountability to the shareholders by maintaining up to date records

Wilfykil answered the question on February 25, 2019 at 11:45

-

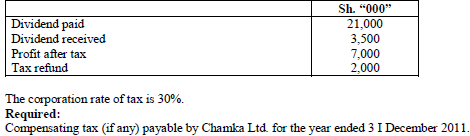

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

(Solved)

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

Date posted:

February 25, 2019

.

Answers (1)

-

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has...

(Solved)

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has ended up paying taxes on the same income more than once.

Required:

Explain to Mr. Maji Mengi the concept of double taxation treaty.

Date posted:

February 25, 2019

.

Answers (1)

-

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and...

(Solved)

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and COMESA, Mr. Jitendra Kumar, a prominent foreign businessman has contacted you seeking your advice on how he could reduce his liability to tax arising from expansion of his business operations into Kenya

Required:

A report addressing in clear and concise details, the following matters raised by Mr. Jitendra Kumar.

(a) The tax objectives under the COMESA treaty.

(b) Rules of origin provisions under the COMESA treaty.

Date posted:

February 25, 2019

.

Answers (1)

-

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

(Solved)

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

Date posted:

February 25, 2019

.

Answers (1)

-

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

(Solved)

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

Date posted:

February 25, 2019

.

Answers (1)

-

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

(Solved)

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

Income from United Kingdom (UK) UK £4,800 net Tax deducted amounted to UK £960. The average exchange rate during the year was 1 UK £ = 140 KSH, .A double taxation agreement exists between Kenya and United Kingdom.

Required:

The double taxation relief (in Kenya shillings) due to Daniel Otwori for the year ended 31 December 2006.

Date posted:

February 25, 2019

.

Answers (1)

-

Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:

(Solved)

Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:

From Kenya: Sh. 720,000

From Zambia Sh. 540,000 (net of tax of sh. 78,000)

Assume that Kenya has a double taxation agreement with Zambia

Required:

The double taxation relief due to Hodari Nkan for the year ended 31 December 2010

Date posted:

February 25, 2019

.

Answers (1)

-

Identify and explain instances when a capital statement may be required.

(Solved)

Identify and explain instances when a capital statement may be required.

Date posted:

February 25, 2019

.

Answers (1)

-

Outline the main types of duties to be levied on goods according to the provisions of the Customs and Excise Act (Cap.472).

(Solved)

Outline the main types of duties to be levied on goods according to the provisions of the Customs and Excise Act (Cap.472).

Date posted:

February 25, 2019

.

Answers (1)

-

Giving appropriate examples, distinguish between forward and backward tax shifting.

(Solved)

Giving appropriate examples, distinguish between forward and backward tax shifting.

Date posted:

February 25, 2019

.

Answers (1)

-

Define the term "shortfall distribution tax". Under what circumstances can a company be exempted from shortfall distribution tax?

(Solved)

Define the term "shortfall distribution tax". Under what circumstances can a company be exempted from shortfall distribution tax?

Date posted:

February 25, 2019

.

Answers (1)

-

Write brief notes on the bodies the tax payer may appeal to incase he/she is aggrieved by the manner in which an objection for tax...

(Solved)

Write brief notes on the bodies the tax payer may appeal to incase he/she is aggrieved by the manner in which an objection for tax assessment to the commissioner has been dealt with.

Date posted:

February 25, 2019

.

Answers (1)

-

Write brief notes on Objections by the taxpayer of an assessment done by the commissioner

(Solved)

Write brief notes on Objections by the taxpayer of an assessment done by the commissioner

Date posted:

February 25, 2019

.

Answers (1)

-

Explain five types of notices of assessment

(Solved)

Explain five types of notices of assessment

Date posted:

February 25, 2019

.

Answers (1)

-

What are the contents of a notice of assessment?

(Solved)

What are the contents of a notice of assessment?

Date posted:

February 25, 2019

.

Answers (1)

-

Write brief notes on back duty.

(Solved)

Write brief notes on back duty.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain the meaning of tax evasion

(Solved)

Explain the meaning of tax evasion

Date posted:

February 25, 2019

.

Answers (1)

-

It may be advantageous for a trader whose turnover is below the legislated turnover limits under the sixth schedule to the V AT Act to...

(Solved)

It may be advantageous for a trader whose turnover is below the legislated turnover limits under the sixth schedule to the V AT Act to register for VAT voluntarily. Under what circumstances could this be beneficial?

Date posted:

February 25, 2019

.

Answers (1)

-

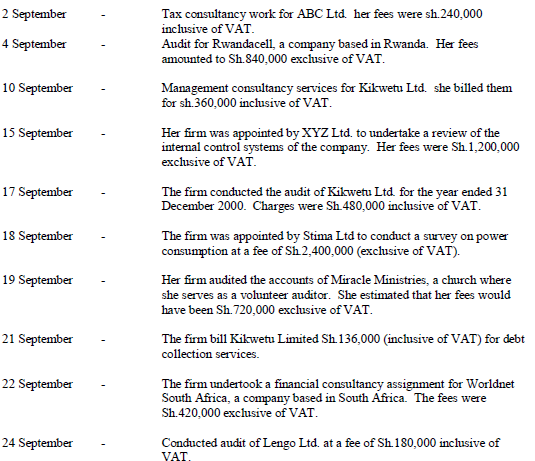

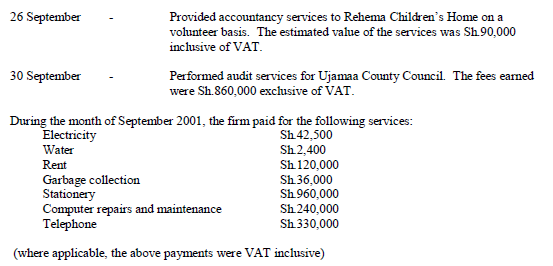

Mrs. Carol Wasike is a practicing accountant working under the style and name of Wasike and Associates. Her firm is registered for Value Added Tax...

(Solved)

Mrs. Carol Wasike is a practicing accountant working under the style and name of Wasike and Associates. Her firm is registered for Value Added Tax (VAT). During the month of September 2001, she undertook and completed the following assignments:

Required:

(a) Prepare a VAT Account for Wasike and Associates for the month of September 2001.

(b) The VAT you have computed in (a) above, was paid on 22 October 2001 since 20 October was on a Saturday. The VAT return was also submitted on the same day. How much additional tax would be payable, if any?

(c) Kikwetu Limited was the subject of a creditors voluntary winding up and the appropriate resolution was passed on 1 April 2002. By that time the company paid Wasike and Associates only Sh.240,000 for services rendered. Assuming that all the conditions for the refund of bad debt relief are met, calculate the amount of VAT bad debt relief.

Date posted:

February 25, 2019

.

Answers (1)

-

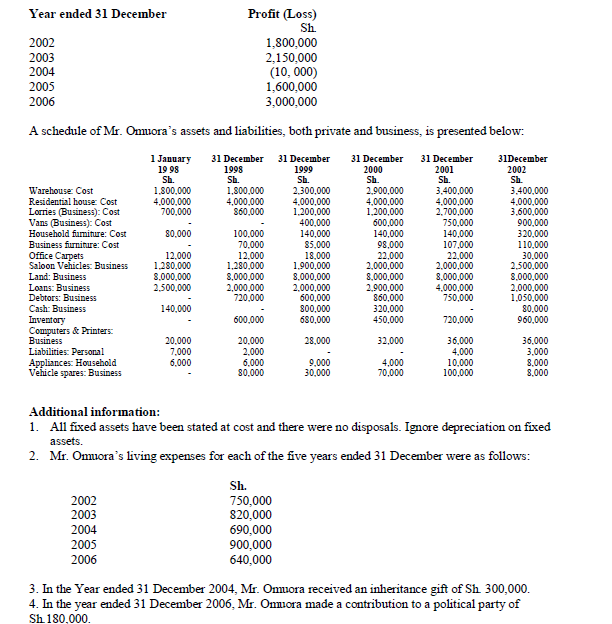

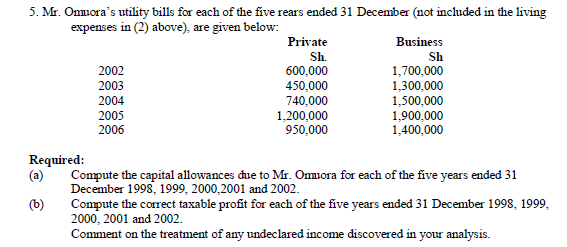

Mr. Joseph Omuora commenced a soft drinks distribution business on 1 January 1998. He has not been maintaining proper books of account and the Commissioner...

(Solved)

Mr. Joseph Omuora commenced a soft drinks distribution business on 1 January 1998. He has not been maintaining proper books of account and the Commissioner of Income Tax has raised doubts about the accuracy of the annual tax returns submitted by him.

You have been appointed to estimate the correct amounts of taxable incomes for the years ended 31 December 1998, 1999, 2000, 2001 for comparison with those disclosed in the annual returns. These returns had disclosed the following profits or losses:

Date posted:

February 25, 2019

.

Answers (1)