1. Tax deductible contribution to registered retirement benefit scheme

Income tax act have provided that contribution to registered retirement benefit schemes can be deducted from gross income before taxable income is determined. The tax deductible contributions is currently set at a maximum of sh. 24,000 per annum

These contributions achieve the twin aims of building retirement savings and reducing taxes paid.

- It should be noted that upon reaching the set retirement age, the retirement savings are still taxable under certain conditions when an individual desires to receive his retirement savings as a lump sum, a sum of Sh. 60,000 per full year worked suggest to a maximum of shs. 600,000 is deductible from the lump sum before the balance is taxed.

- Members of pension schemes or individual retirement scheme who opt to use their retirement savings to purchase an annuity (which will generate a periodic pension) will have various advantages.

- The first Sh. 300,000 of the total pensions or retirement annuities received annually are tax exempt

- Secondly personal relief is applied to reduce the taxable income further pension for pensioners over 65 years are now fully tax exempt.

- The income tax act has sometimes provided that contribution to registered schemes designed and established to enable savings for purchase of residencies can be deducted from gross income up to a maximum of 4000 per month of 48,000 per annum

- This has been enhanced by making interest earned on deposit of up to 3 million into such a scheme tax free. This avenue for savings and tax mitigation are difficult for banks to abide with. As a result so far only one financial institution i.e. housing finance has launched a saving product for this purpose

2. Mortgage interest deduction

Interest incurred on personal mortgages is deductible from gross income before arriving at taxable income subject to a limit of 12,500 per month or 150,000 per annum

However this facility is available in respect of one house which can be in the name of either spouse and the loan must have been borrowed from an approved institution by the CDT (commission of domestic taxes) which may constitute a bank, an insurance company or a housing finance company each registered under its respective act.

3. Individual investment in various assets so as to avoid taxes on gains

The suspension of taxation of capital gains for more than two decades means that individual have not been subjected to taxes on gains made on acquisition and subsequent disposal of assets such as immovable properties, equities and fixed income securities.

- An attempt on year 2000 to introduce tax on capital gains realized on sale of immovable property was unsuccessful after parliament rejected the enabling provision of the finance bill.

- It should be carefully noted that the tax exemption is where the acquisition and disposal of assets is not a business activity carried on under the presence of personal investment.

- Section 3 (2a) of the income tax act provides that income tax is changeable upon gains or profits from a business. In the definition section of the Act, business is defined to include any trade, profession, vocation and every manufacture venture or concern in the nature of trade.

- This clearly captures regular personal trading in assets of what nature. The acts will look at the motive of acquisition i.e. either for personal use or for subsequent disposal.

- These exempts can be enjoyed by investing through unit trust or other collective investments schemes such as mutual funds.

- Such investments vehicles are subject only to a final withholding tax on dividend and interest income.

4. Conducting business using a corporative entity so as to enable comprehensive deduction of business expenses

Expenses legitimately incurred in production of income are tax deductible regardless of the form of business. Conducting business using a corporate entity enables clear segmentation of business and personal expenses thus enhancing the deduction of certain expenses. This is especially in light of fact that the domestic tax department will scrutinize expenditure in the cause of audit

- Individual engage in various professions including entertainment can set up company’s labeled personal service companies to which they direct their income.

- This enables them to reduce taxable income by changing their gross income with certain tax deductible expenses which would otherwise not be deductible if they operates as an incorporated businesses

- Further due to separation of business and owners in a company set up any dealing with the company would be treated at arm’s length.

5. Establishment of charitable trust or foundations

Section 10 of the 1st schedule of the income tax act provides that the income of an institution body of persons or irrevocable trust of a public character establishment solely for the purposes of poverty elevation or distress of the public as the advancement of religion or education or for public benefit shall be tax exempt. Section 13 provides that the income of a registered trust is exempt from income tax. The finance act 2006 further provides that contribution made to a tax exempt entity shall be deductible from taxable income

Wilfykil answered the question on February 25, 2019 at 12:19

-

Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies

(Solved)

Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies.

Required:

i) Citing examples distinguish between a tax refund” and a “tax credit”

ii) Evaluate the fundamental role of tax refunds and tax credits in a government’s developments agenda

Date posted:

February 25, 2019

.

Answers (1)

-

In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.

(Solved)

In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.

In addition, the company earned an investment income of Sh. k60 million. Dividend paid to members for the year amounted to Sh. 98 million.

The corporation tax rate is 30%

Required:

Shortfall tax, inclusive of penalties (if any) payable by the company for the year ended 31 December 2011.

Date posted:

February 25, 2019

.

Answers (1)

-

Justify the imposition of shortfall tax on companies

(Solved)

Justify the imposition of shortfall tax on companies

Date posted:

February 25, 2019

.

Answers (1)

-

A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).

(Solved)

A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).

Required;

i) Explain three reasons that have motivated the formation of LTUs.

ii) As a tax consultant in a country that intends to form an LTU, describe three key functional areas of an LTU.

Date posted:

February 25, 2019

.

Answers (1)

-

Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.

(Solved)

Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.

Date posted:

February 25, 2019

.

Answers (1)

-

Describe ways in which related parties could be transfer pricing systems to avoid tax

(Solved)

Describe ways in which related parties could be transfer pricing systems to avoid tax

Date posted:

February 25, 2019

.

Answers (1)

-

Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.

(Solved)

Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.

Date posted:

February 25, 2019

.

Answers (1)

-

Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.

(Solved)

Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.

Date posted:

February 25, 2019

.

Answers (1)

-

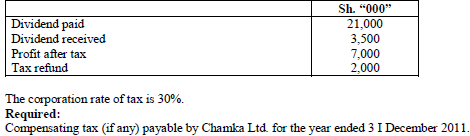

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

(Solved)

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

Date posted:

February 25, 2019

.

Answers (1)

-

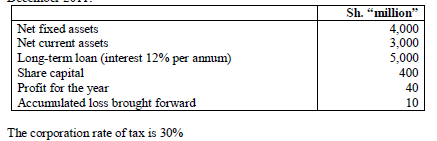

Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31...

(Solved)

Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31 December 2011:

Required:

i) Justify the argument that the company was thinly capitalized.

ii) Compute the company's interest tax shield.

Date posted:

February 25, 2019

.

Answers (1)

-

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has...

(Solved)

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has ended up paying taxes on the same income more than once.

Required:

Explain to Mr. Maji Mengi the concept of double taxation treaty.

Date posted:

February 25, 2019

.

Answers (1)

-

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and...

(Solved)

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and COMESA, Mr. Jitendra Kumar, a prominent foreign businessman has contacted you seeking your advice on how he could reduce his liability to tax arising from expansion of his business operations into Kenya

Required:

A report addressing in clear and concise details, the following matters raised by Mr. Jitendra Kumar.

(a) The tax objectives under the COMESA treaty.

(b) Rules of origin provisions under the COMESA treaty.

Date posted:

February 25, 2019

.

Answers (1)

-

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

(Solved)

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

Date posted:

February 25, 2019

.

Answers (1)

-

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

(Solved)

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

Date posted:

February 25, 2019

.

Answers (1)

-

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

(Solved)

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

Income from United Kingdom (UK) UK £4,800 net Tax deducted amounted to UK £960. The average exchange rate during the year was 1 UK £ = 140 KSH, .A double taxation agreement exists between Kenya and United Kingdom.

Required:

The double taxation relief (in Kenya shillings) due to Daniel Otwori for the year ended 31 December 2006.

Date posted:

February 25, 2019

.

Answers (1)

-

A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high...

(Solved)

A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high as expected by these countries and regions:

Required:

i. Briefly describe the concept of ‘tax havens’

ii. Summarize three benefits that might accrue to an investor in a tax haven

Date posted:

February 25, 2019

.

Answers (1)

-

Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:

(Solved)

Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:

From Kenya: Sh. 720,000

From Zambia Sh. 540,000 (net of tax of sh. 78,000)

Assume that Kenya has a double taxation agreement with Zambia

Required:

The double taxation relief due to Hodari Nkan for the year ended 31 December 2010

Date posted:

February 25, 2019

.

Answers (1)

-

A generalized system of preference (GSP) applies where a country grants preferential treatment to goods and services received from another country.

(Solved)

A generalized system of preference (GSP) applies where a country grants preferential treatment to goods and services received from another country.

Required:

Describe three general conditions to be fulfilled for goods or services from one country to benefit from a GSP.

Date posted:

February 25, 2019

.

Answers (1)

-

Explain how the tax legislation in your country attempts to prevent creative accounting by multinational companies

(Solved)

Explain how the tax legislation in your country attempts to prevent creative accounting by multinational companies

Date posted:

February 25, 2019

.

Answers (1)

-

“Many objectives of the Common Market for Eastern and Southern African (COMESA) treaty remain elusive due to emerging challenges”. Highlight four such challenges

(Solved)

“Many objectives of the Common Market for Eastern and Southern African (COMESA) treaty remain elusive due to emerging challenges”. Highlight four such challenges

Date posted:

February 25, 2019

.

Answers (1)