-

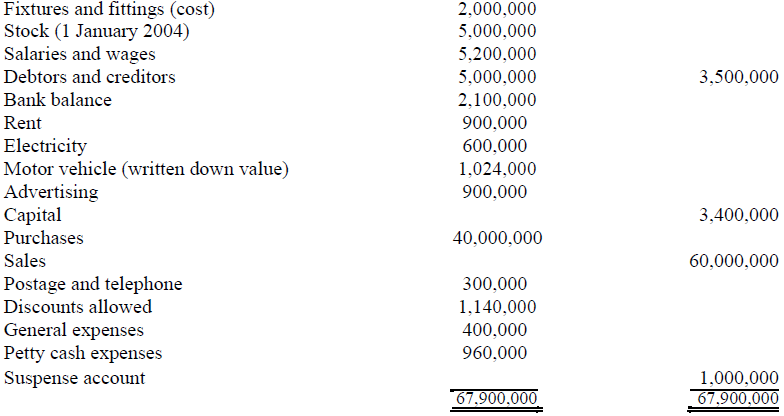

The following trial balance was extracted from the books of Hari Singh as at 31December 2004:

Additional information:

1. Closing stock as at 31 December 2004 was...

(Solved)

The following trial balance was extracted from the books of Hari Singh as at 31December 2004:

Sh. Sh

Drawings 1,600,000

Cash 676,000

Petty cash 100,000

Additional information:

1. Closing stock as at 31 December 2004 was valued at Sh.7,500,000

2. Petty cash balance represents the month end imprest amount. As at 31 December 2004, the petty

cashier had vouchers amounting to Sh40,000 which had not been reimbursed by the main

cashier.

3. Discounts allowed amounting to Sh.100,000 had been posted to the debit of the debtors account.

4. Sales had been undercast by Sh400,000.

5. The motor vehicle, which had been purchased on 1 January 2002, was being depreciated at

20% per annum on the reducing balance basis. The original cost of the motor vehicle was

Sh.2,000,000. It has been decided that the motor vehicle be depreciated at 6% per annum on the

straight line basis and to make the change effective from the date of purchase.

6. Cash withdrawn from the bank for business use amounting to Sh400,000 had not been entered

in the bank column of the cash book.

7. No entry bas been made for stock valued at Sh1,000,000 taken by the proprietor for personal

use.

8. Telephone bills amounting to Sh.100,000 were unpaid as at 31 December 2004.

9. Advertising expenses include the cost of a sales campaign conducted during the year of

Sh.600,000. It is expected that the benefits of this campaign will be enjoyed or the next three

years.

10. Fixtures and fittings are to be depreciated at 20%. per annum on cost.

Required:

a) Trading, profit and loss account or the year ended 31 December 2004.

b) Balance sheet as at 31 December 2004.

Date posted:

May 16, 2019

.

Answers (1)

-

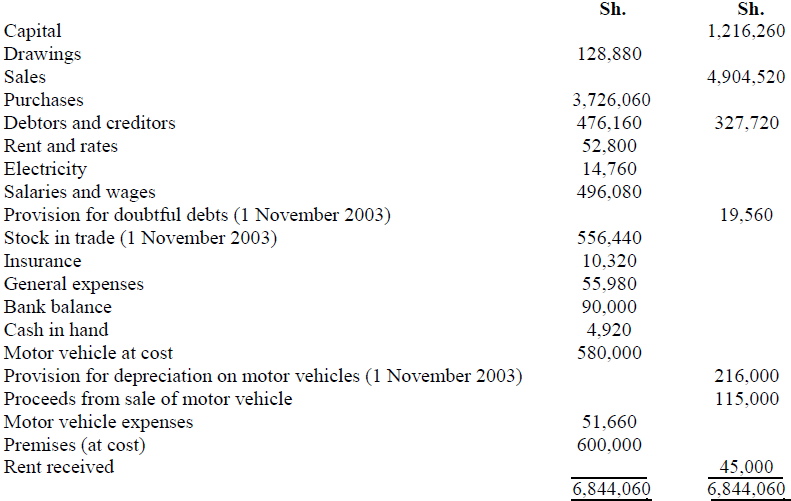

The following trial balance was extracted from the books of Mohammed Kagame, a sole trader, as at

31 October 2004:

1. Stock in trade a s at...

(Solved)

The following trial balance was extracted from the books of Mohammed Kagame, a sole trader, as at

31 October 2004:

1. Stock in trade a s at 31 October 2004 was valued at Sh593,040.

2. Rates and insurance were prepaid to the extent ofSh.2,400 and Sh.2,820 respectively, as at 3 J

October 2004,

3. Electricity due as at 31 October 2004 amounted to Sh.6,000.

4. The provision for doubtful debts is to be adjusted to S% of the debtors remaining after taking into

account that Sh.20, 1 60 of the debtors were to be regarded as bad.

5. Rent receivable as at 31 October 2004 was Sh. 15,000

6. Depreciation has been and is to be charged on motor vehicles at the rate of 20% per annum on the

straight line basis. No depreciation is to be charged on premises.

7. In November 2003, a motor vehicle which had been purchased or Sh.160,000 on I November

2000, was sold for Sh.115,000. The only record of this disposal is the entry in the proceeds from

sale of motor vehicle account.

Required:

a) Trading and profit and loss account or the year ended 31 October 2004

b) Balance sheet as at 3 I October 2004.

Date posted:

May 16, 2019

.

Answers (1)

-

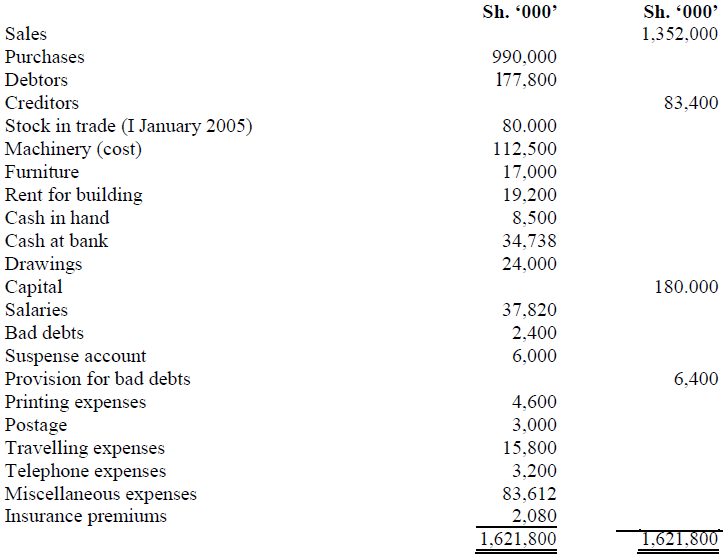

The following balances were extracted from the books of Patel and Sons in respect of the year ended

31 December 2005:

1. Old furniture which stood in...

(Solved)

The following balances were extracted from the books of Patel and Sons in respect of the year ended

31 December 2005:

1. Old furniture which stood in the books (as at I January 2005) at Sh.2,400,000 was disposed of at

Sh.1,160,000 during the year in part exchange for new furniture costing Sh.2,080,000. A net

invoice of Sh.920,000 in respect of this transaction was erroneously passed through the Purchases

Day Book.

2. The suspense account represented money advanced to a sales team detailed to undertake a sales

campaign in the Rift Valley Province. On returning, the sales team disclosed that Sh.2,400,000

was used for travelling, Sh.1,000,000 for legal fees and Sh.1,800,000 for miscellaneous

expenses. The balance was yet to be refunded by 31 December 2005.

3. The business is conducted 10 a rented building and 50% or the building is used for

accommodation of the business owner's family.

4. Depreciation is to be provided on the straight line basis at 10%) per annum on machinery and 5%

per annum on furniture. Depreciation is to be applied for the whole year regardless of date of

purchase of the asset.

5. Total bad debts for the year amounted to Sh.4,000,000. Provision for doubtful debts is to be

maintained at 5% of the outstanding debtors

6. Closing stock amounted to Sh100,000,000

7. Insurance premiums cover the one year period ended 31 January 2006.

Required:

a) Trading and profit and loss account for the year ended 31 December 2005.

b) Balance sheet as at 31 December 2005

Date posted:

May 16, 2019

.

Answers (1)

-

The following balances were extracted from the books of Biashara Kubwa Enterprise, a wholesale

business, as at 31 October 2011:

...

(Solved)

The following balances were extracted from the books of Biashara Kubwa Enterprise, a wholesale

business, as at 31 October 2011:

Sh.

Drawings 660,000

Trade receivables 990,000

Purchases 2,303,840

Sales returns 79,420

Capital 4,104,100

Trade payables 330,000

Sales 4,691,280

Purchase returns 120,340

Discount received 93,720

Provision for depreciation: Motor vehicle 176,000

Fixtures and fittings 63,800

Allowance for doubtful debts 44,000

15% bank loan 220,000

Salaries and wages 1,034,000

Discount allowed 54,560

Bank balance 568,260

Cash in hand 26,400

Electricity expenses 103,840

Rent and rates 54,560

Freehold premises (cost) 1,569,700

Fixtures and fittings (cost) 334,400

Motor vehicles (cost) 462,000

Stationery 34,320

Postage and telephone expenses 44,000

Insurance premiums 13,200

Bad debts written off 15,840

Motor vehicle expenses 84,920

Inventory (1November 2010) 1,393,480

Interest on bank loan 16,500

Additional information:

1. The following were the values provided on inventory as at 31 October 2011:

Replacement cost Sh. 1,036,400

Net realizable value Sh. 1,366,200

2. Sales include Sh. 300,000 worth of goods sold by Biashara Kubwa Enterprise agents', who are

allowed 15% commission on such sales. The transaction has not been recorded in the books.

3. Depreciation is to be provided as follows:

Fixtures and fittings 10% per annum on reducing balance basis. Motor vehicles

15% per annum on straight line basis

4. Annual insurance premium amounted to Sh. 12,000

5. As at 31 October 2011, there was a balance of Sh. 65,000 received from a customer in cash

6. Salaries and wages were in arrears of Sh. 35,000

7. The electricity bill for the month of October of Sh. 14,500 was received on 5 November 2011

8. Stationery stock amounted to Sh. 8,750

9. An allowance of 5% is to be maintained for doubtful debts

10.Goods worth Sh. 48,840 had been distributed to potential customers as free samples

Required:

(a) Income statement for the year ended 31 October 2011

(b) Statement of financial position as at 31 October 2011

Date posted:

May 16, 2019

.

Answers (1)

-

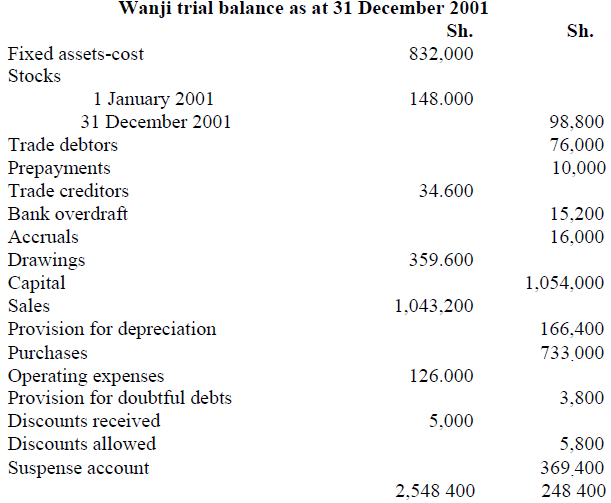

On 31 December 2001 an inexperienced book-keeper working for Wanji, a sole trader, extracted a

trial balance. Due to errors committed by the book-keeper, the trial...

(Solved)

On 31 December 2001 an inexperienced book-keeper working for Wanji, a sole trader, extracted a

trial balance. Due to errors committed by the book-keeper, the trial balance failed to balance by

Sh.369.400. He placed the difference in a suspense account as shown below:

Investigations carried out after preparing the above trial balance detected the following errors:

1. The total of the sales day book for December 2001 was overcast by Sh.25,700.

2. On 2 July 2001 the business purchased office equipment for Sh.40.000. These were debited to

purchases account.

3. Depreciation on the equipment is at the rate of 10% per annum on cost and based on the period

(months) of usage in the year.

4. A payment to a creditor by cheque of Sh.8.500 was erroneously credited to the creditor's account.

5. A payment of Sh.4.500 for telephone expenses was debited to telephone account as Sh.5.400.

6. An amount of Sh.15.000 received from a debtor was not posted to the debtor's account

from the cash book.

7. An amount of discounts received of Sh.2.500 was debited to discounts allowed account.

8. Purchases day book for October 2001 was undercast by Sh.28,000.

9. Assume the business had reported a net profit of Sh.85,800 before adjusting for the above errors.

Required:

(a) The adjusted trial balance and the correct balance of the suspense account

(b) Journal entries to correct the errors (Narrations not required)

(c) Suspense account starting with the balance determined in the adjusted trial balance in (a) above.

(d) The adjusted net profit for the year.

Date posted:

May 16, 2019

.

Answers (1)

-

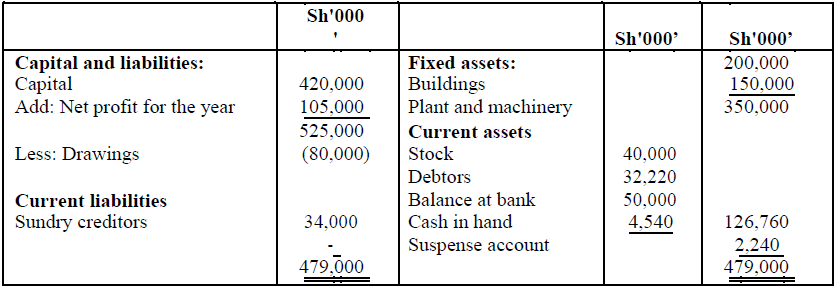

Ali Osman is a sole trader who operates a retail business. His balance sheet as at 30 April 2004 was as

follows:

Although the trial balance did...

(Solved)

Ali Osman is a sole trader who operates a retail business. His balance sheet as at 30 April 2004 was as

follows:

Although the trial balance did not agree, the above balance sheet was prepared and a suspense account

opened to which the difference was posted. At a later date, an inspection of the books revealed the

following:

1. The salaries day book had been overcast by Sh.3,000,000.

1. A payment of Sh. 1,560,000 received from a debtor had been recorded in the cashbook but had

not been posted to the personal account.

2. A discount received 0 Sh.150,000 had been posted to the wrong side of the personal account.

3. The stock book had been undercast by Sh.! 0,000,000 as at 30 April 2004.

4. Bank charges of Sh.850,000 had not been entered into the books.

5. A cash balance of Sh.500,000 had not been included in the trial balance.

6. An invoice for Sh.850,000 for private work commissioned by Ali Osman had been paid by the

business and posted to sundry expenses account.

Required:

a) Suspense account to clear the difference.

b) Statement showing the correct net profit or the year ended 30 April 2004

Date posted:

May 16, 2019

.

Answers (1)

-

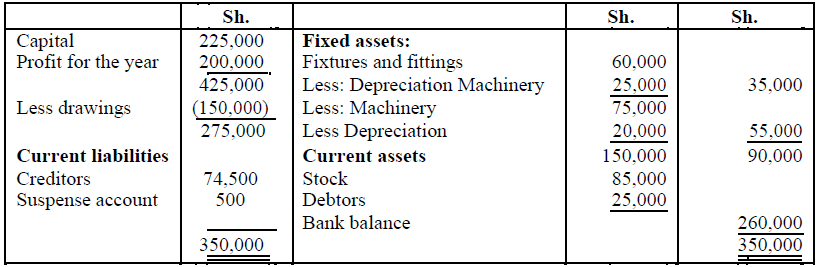

a) Explain any four purposes of journal entries in the accounting process

b) Walter Muita, a sole trader, presented the following balance sheet of his business...

(Solved)

a) Explain any four purposes of journal entries in the accounting process

b) Walter Muita, a sole trader, presented the following balance sheet of his business as at 30 June

2005. He asked you to investigate the causes of errors giving rise to the amount in the

suspense account:

You subsequently discovered the following errors:

1. The purchases day book was undercast by Sh.4,000.

2. A telephone head costing Sh.3,000 was bought and the amount was debited to the repairs account.

3. The telephone head is to be depreciated at the rate of 15% per annum as pari of fixtures

and fittings.

4. An amount of Sh.2,000 was omitted from total debtors.

5. Returns outwards of Sh.500 were erroneously entered in the sales book.

6. A payment of Sh.1,250 to a creditor was correctly entered in the cash book but credited to his

account.

7. Goods valued at Sh.l 0,000 were taken by Walter Muita for his own use and no entry has

been made to this effect.

8. A bad debt of Sh 1,250 had been written off

9. A discount received of Sh4,500 had been correctly recorded in the cash book but had been posted

to the wrong side of the discount received account.

Required:

i) Show the necessary journal entries to correct the errors listed above.

ii) Prepare a statement of adjusted profit (or loss) for the year ended 30 June 2005.

iii) Prepare the corrected balance sheet as at 30 June 2005.

Date posted:

May 16, 2019

.

Answers (1)

-

(a) Briefly explain the following types of errors:

i. Error of commission

ii. Error of principle

iii. Complete reversal of entries

iv. Compensating errors

(b) The trial balance of Amanda...

(Solved)

(a) Briefly explain the following types of errors:

i. Error of commission

ii. Error of principle

iii. Complete reversal of entries

iv. Compensating errors

(b) The trial balance of Amanda Ltd as at 30 April 2004 did not balance. On investigation, the

following errors were discovered:

1. A loan of Sh.2,000,000 from one of the directors has been correctly entered in the cashbook

but posted to the wrong side of the loan account.

2. The purchase of a motor vehicle on credit fro Sh.2,860,000 had been recorded by debiting the

supplier’s account and crediting the motor expenses account.

3. A cheque for Sh.80,000 from Ogola, a customer to whom goods are regularly supplied on

credit, was correctly entered in the cashbook but was posted to the credit of bad debts

recovered account in the mistaken belief that it was a receipt from Agola, a customer whose

debt had been written off three years earlier.

4. In reconciling the company’s cash book with the bank statement, it was found that bank

charges of Sh.38,000 had not been entered in the company’s records.

5. The totals of the cash discount columns in the cashbook for the month of April 2004 had not

been posted to the respective discount accounts.

The figures were:

Sh.

Discounts allowed 184,000

Discounts received 397,000

6. The company had purchased some plant on 1 March 2003 for Sh.1,600,000. The payment was

correctly entered in the cashbook but was debited to the plant repairs account. Depreciation on

such plant is provided for at the rate of 20% per annum on cost.

Required:

(i) Journal entries with narrations to correct the above errors.

(ii) Suspense accounts showing the original difference

Date posted:

May 16, 2019

.

Answers (1)

-

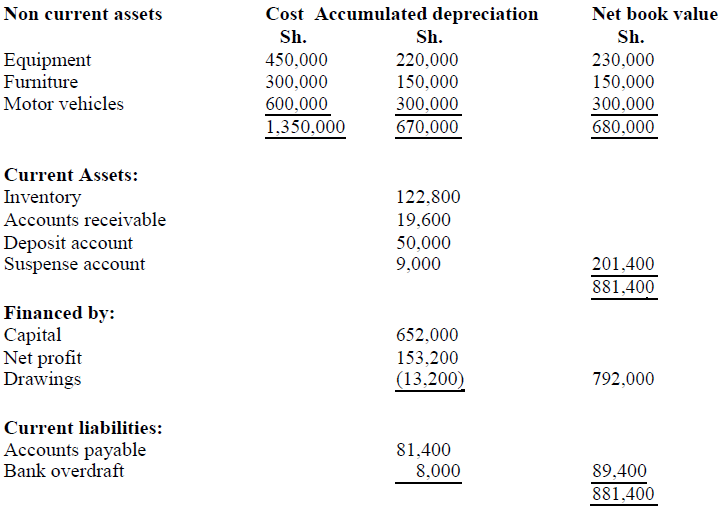

Ben Mogaka prepared the following draft balance sheet for BM Enterprises as at 31 December 2005:

Additional information:

On further investigation, the suspense account was discovered to...

(Solved)

Ben Mogaka prepared the following draft balance sheet for BM Enterprises as at 31 December 2005:

Additional information:

On further investigation, the suspense account was discovered to have resulted from the following

errors:

1. The sales of goods on credit to Alex Otis amounting to Sh.19,000had been recorded in the sales

journal as sh.9,000.

2. A receipt of Sh.20,000 from sale of an item of equipment had been credited to sales account. The

equipment was shown in the books of account at costs of account of Sh.90,000 and accumulated

depreciation of Sh.72,000.

3. A credit note from a supplier, Simon Masound for Sh.15,000 had been omitted from the books.

4. A bank overdraft for Sh.7,000 reflected in the cash book as at 31 December 2005 was omitted In

the trial balance.

5. A payment of Sh. 9,700 to Tom Wambugu, a creditor, was correctly entered in the cahs book but

posted to his personal account as Sh.7,900.

6. The debit side of rent expense account had been undercast by Sh.1,000.

7. A provision of Sh.2,000 for sundry expenses outstanding as at 31 December 2004 and debited to

sundry expenses at that dated had not been brought forward to the credit of the account in the

following period. No credit entry had been made in any other account in respect to this account in

respect to this item.

8. Discount received from the supplier of Sh.8,200 had been entered on the wrong side of purchases

ledger control account.

9. On 31 December, goods valued at Sh.9,600 (selling price) were returned by Jane Kerubo (a

debtor). No entry had been made in the books to reflect this transaction. These goods were not

included in the closing stock.

10. Discounts allowed were overcast by Sh.1,200.

Required:

(a) Journal entries to correct the above errors (Narration not required)

(b) Suspense account.

(c) Statement of corrected net profit for the year ended 31 December 2005

(d) Corrected balance sheet as 31 December 2005.

Date posted:

May 16, 2019

.

Answers (1)

-

The trial balance extracted from the books of Benard Masita as at 30 September 2010 failed to

agree. The debit difference of Sh. 442,000 was posted...

(Solved)

The trial balance extracted from the books of Benard Masita as at 30 September 2010 failed to

agree. The debit difference of Sh. 442,000 was posted to a suspense account. An income

statement was prepared which showed a gross profit and a net profit of Sh. 1,985,000 and

Sh.1,229,000 respectively. Upon investigations, the following errors were discovered:

1. A purchase of Sh 150,000 on credit was correctly posted to the suppliers account but was

completely omitted from the purchases day book.

2. Sales amounting to Sh. 250,000 to Samuel Njuguna were erroneously credited to his account.

The sales account had been correctly posted.

3. Salaries paid for the month of September 2010 amounting to Sh. 230,000 were recorded in

the salaries account as Sh 320,000.

4. Purchases of office stationery for Sh. 125,000 were erroneously debited to purchases account.

5. A payment of Sh.45,000 to Daniel Olunya, a creditor, was erroneously debited to the account of

Alois Olunya, another creditor.

6. An entry of Sh.21,000 for returns outwards was made in error in the sales day book instead of

in the purchases return day book.

7. A bad debt of Sh 22,500 is yet to be written off.

8. Goods valued at Sh220,000 were taken for personal use but no entry had been made in the

books.

9. A discount received of Sh.59,000 was correctly entered in the cashbook but posted to the

discounts allowed account.

Required:

i) A fully balanced suspense account.

ii) Statement of corrected gross profit.

iii) Statement of corrected net profit.

Date posted:

May 16, 2019

.

Answers (1)

-

Pata Transport Limited (PTL) was incorporated on 1 June 2006 and on the same day bought its first

lorry; KB099S for Sh. 9,000,000.

On 1 April 2007,...

(Solved)

Pata Transport Limited (PTL) was incorporated on 1 June 2006 and on the same day bought its first

lorry; KB099S for Sh. 9,000,000.

On 1 April 2007, the company bought its second lorry KB 120T FOR Sh 12,000,000.

On 1 June 2008, the company bought a third lorry KB 340X for Sh. 6,000,000.

On 1 October 2008, lorry KB 099S was involved in an accident and was written off. The

insurance compensation paid to PTL by the insurers was Sh. 2,600,000.

On 31 December 2009,lorry KB 340X broke down and was traded in with a new lorry registration KB

419Y valued at Sh. 8,000,000.PTL; paid cash amounting to Sh. 5,400,000 for the lorry.

On 1 Apri12010, a van KB 890B was purchased for Sh 4,800,000.

Depreciation on motor vehicles is to be provided at the rate of 10% per annum on a straight line basis.

The policy of the company is to provide depreciation on a pro rata basis.

On 1 January 2009, the company decided to change its depreciation rate from 10% to 15% per annum.

The change was effected on motor vehicles that were in use retrospectively; that is from the year of

purchase. An adjusting entry was to be made in the accounts for the year ended 31 December 2009.

All lorries were comprehensively insured.

Assume the year end for PTL IS 31 December.

Required:

i) Motor vehicles account for the five years ended 31 December 2006,2007,2008,2009 and 2010.

ii) Provision for depreciation account for the same years stated in (b) (i) above

iii) Disposal of motor vehicles account

Date posted:

May 16, 2019

.

Answers (1)

-

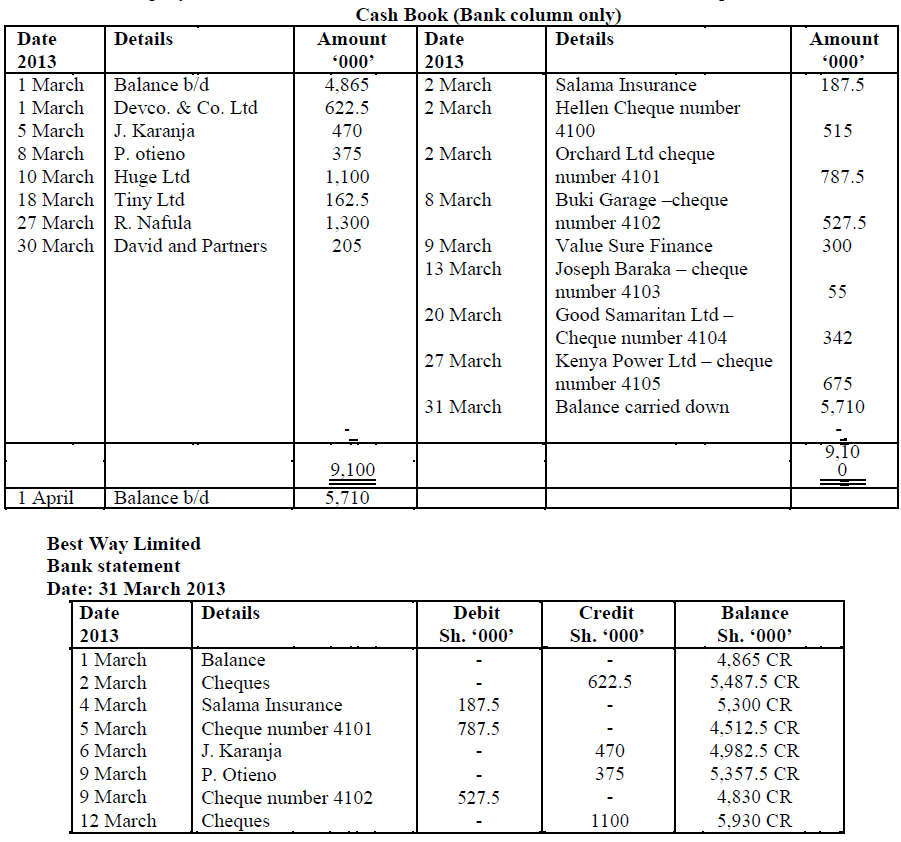

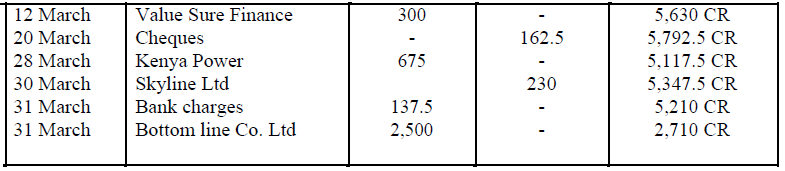

You have just been employed by Best Way Ltd as a trainee accountant. Your first exercise is to

check the transactions in the company’s cash book,...

(Solved)

You have just been employed by Best Way Ltd as a trainee accountant. Your first exercise is to

check the transactions in the company’s cash book, check entries in the bank statement, update

the cash book and make any amendments as necessary after which you will prepare a bank

reconciliation statement at the end of the month.

The company’s cash book and bank statement for the month of March 2013 are provided below;-

Required;

A bank reconciliation statement as at 31 March 2013

Date posted:

May 16, 2019

.

Answers (1)

-

Distinguish between ‘purchased goodwill’ and ‘non-purchased goodwill’

(Solved)

Distinguish between ‘purchased goodwill’ and ‘non-purchased goodwill’

Date posted:

May 16, 2019

.

Answers (1)

-

The following balances were extracted from the books of Furahia Enterprises for the month of

September 2013:

Sh.

Debit balance (1 September 2013): Sales ledger 14,280,000

Purchases ledger 1,920,000

Credit...

(Solved)

The following balances were extracted from the books of Furahia Enterprises for the month of

September 2013:

Sh.

Debit balance (1 September 2013): Sales ledger 14,280,000

Purchases ledger 1,920,000

Credit balance (1 September 2013): Sales ledger 1,680,000

Purchases ledger 6,720,000

Credit notes received from suppliers 1,860,000

Debt collection expenses 480,000

Interest charged on customers' overdue accounts 384,000

Customers dishonoured cheques 1,260,000

Bad debts written off 720,000

Receipts from customers 1,280,000

Interest charged by creditors on overdue accounts^ 588,000

Payment to creditors 7,680,000

Contra settlements 390,000

Credit notes issued to customers 270,000

Credit sales 17,340,000

Cash sales 3,240,000

Cash purchases 2,160,000

Credit purchases 7,440,000

Discounts, allowed 1,080,000

Discounts received 690,000

Balances as at 30 September 2013:

Sales ledger (credit) 1,110,000

Purchases ledger (debit) 1,050,000

Required;

i) Sales ledger control account for the month ended 30 September 2013.

ii) Purchases ledger control account for the month ended 30 September

Date posted:

May 16, 2019

.

Answers (1)

-

The following is a summary of the cash book of Azimio Ltd. for the year ended 31 May 2014:

Subsequent investigations reveal that:

1. A page of...

(Solved)

The following is a summary of the cash book of Azimio Ltd. for the year ended 31 May 2014:

Subsequent investigations reveal that:

1. A page of the receipt side of the cash book has been under cast by Sh.200, 000.

2. The following transactions appearing on the bank statement have not yet been entered in the cash

book:

- Dividend received on a trade investment Sh.1, 147,000.

- Hire purchase repayments for 12 months at Sh.55, 000 per month.

- Interest for the half year to 30 November 2014 on a loan of Sh.20, 000,000 at 11 percent per

annum.

3. Bank charges of Sh. 143,000 shown on the bank statement have not yet been entered in the cash

book.

4. A cheque received from a customer for Sh.180, 000 was returned by the bank unpaid and no entry

has been made in the cash book for this transaction.

5. The company owes Sh.430, 000 for electricity consumed in the month of May 2014.

6. A cheque for Sh.82, 000 has been debited to the company's account in error by the bank.

7. A cheque drawn for Sh.98, 000 has been entered in the cash book as Sh.89, 000 and another

one-drawn for Sh.230, 000 has been entered as a receipt.

8. A transposition error occurred in the opening balance of the cash book. The opening

balance should have been brought down as Sh.850, 000 instead of Sh.805, 000.

9. Cheques paid to suppliers totalling Sh.630, 000 have not yet been presented at the bank, while

deposits totaling Sh.580, 000 made on 31 May 2014 have not yet been credited to the company's

account.

10. The balance as per the bank statement is an overdraft of Sh.870, 000.

Required:

(i) Adjusted cash book balance.

(ii) Bank reconciliation statement as at 31 May 2014.

Date posted:

May 16, 2019

.

Answers (1)

-

Discuss five principles of the code of ethics that govern the professional conduct of accountants.

(Solved)

Discuss five principles of the code of ethics that govern the professional conduct of accountants.

Date posted:

May 15, 2019

.

Answers (1)