-

Uzuri County Council authorised the construction of a city hall on 1 July 2012. The hall was

expected to cost Sh. 160,000,000. The project was to...

(Solved)

Uzuri County Council authorised the construction of a city hall on 1 July 2012. The hall was

expected to cost Sh. 160,000,000. The project was to be financed as follows:

Sh. 80,000,000 from a 6.5% bond issue.

Sh. 64,000,000 from a government grant.

Sh. l6,000,000 from the general fund.

The following transactions and events took place during the year ended 30 June 2013:

1. The county council transferred Sh. 16,000,000 from the general fund to the city hall capital

fund. The capital project fund was for the purpose of construction of the city hall.

2. Planning and architects fees amounting to Sh.6,400,000 were paid.

3. The contract was awarded for Sh. 152, 000,000.

4. The 6.5% bonds were sold for Sh. 80,320,000 and the amount of the premium transferred to

the debt service fund.

5. The contract was certified 50% complete and an invoice for Sh.76,000,000 was received from

the contractor.

The contractor was paid the invoiced amount less 10% retention

Required:

i) Journal entries to record the above transactions.

ii) Statement of revenue and expenditure of the capital project fund for the year ended 30 June

2013.

iii) Statement of financial position of the capital project fund as at 30 June 2013.

Date posted:

May 16, 2019

.

Answers (1)

-

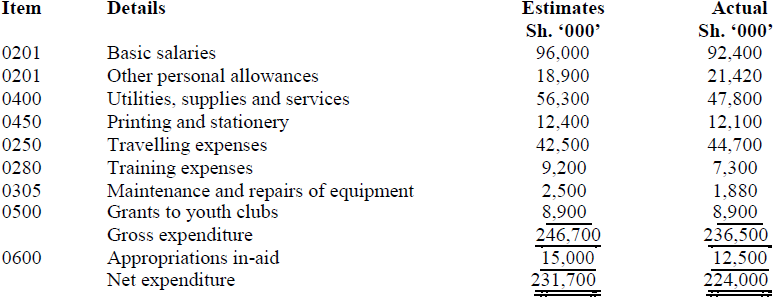

The following were the estimates and actual expenditure of Barani Ministry of Youth and Sports for

the financial year ended 30 June 2012.

Drawings from the exchequer...

(Solved)

The following were the estimates and actual expenditure of Barani Ministry of Youth and Sports for

the financial year ended 30 June 2012.

Drawings from the exchequer during the financial year ended 30 June 2012 amounted to

Sh.226,000,000

Required;

a) General account of vote

b) Exchequer account

c) Paymaster general (PMG) account

d) Appropriation account for the year ended 30 June 2012

e) Statement of assets and liabilities as at 30 June 2012

Date posted:

May 16, 2019

.

Answers (1)

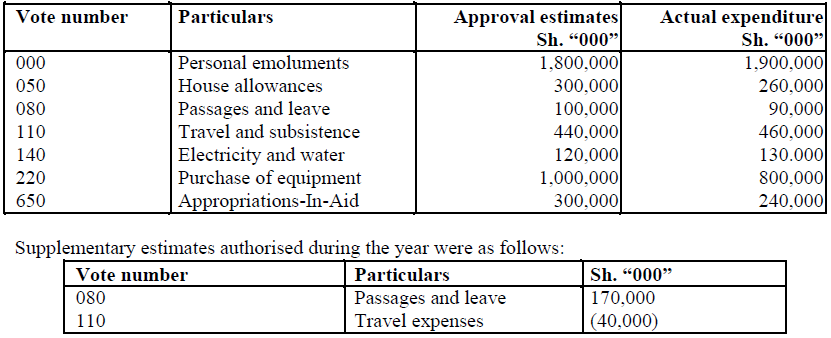

-

The following details relate to the approved estimates and actual expenditure of a certain

government ministry for the financial year ended June 2012.

Required;-

Appropriation account for the...

(Solved)

The following details relate to the approved estimates and actual expenditure of a certain

government ministry for the financial year ended June 2012.

Required;-

Appropriation account for the year ended 30 June 2012.

Date posted:

May 16, 2019

.

Answers (1)

-

Explain the following terms in the context of public sector accounting:

i) Commitment accounting

ii) Fund accounting

(Solved)

Explain the following terms in the context of public sector accounting:

i) Commitment accounting

ii) Fund accounting

Date posted:

May 16, 2019

.

Answers (1)

-

Explain three roles of the International Public Sector Accounting Standards Board (IPSASB).

(Solved)

Explain three roles of the International Public Sector Accounting Standards Board (IPSASB).

Date posted:

May 16, 2019

.

Answers (1)

-

Explain the meaning of the following terms in relation to Public Sector Accounting:

i) Appropriation-In-Aid

ii) Paymaster general

iii) General Account of Vote

iv) Exchequer Account

(Solved)

Explain the meaning of the following terms in relation to Public Sector Accounting:

i) Appropriation-In-Aid

ii) Paymaster general

iii) General Account of Vote

iv) Exchequer Account

Date posted:

May 16, 2019

.

Answers (1)

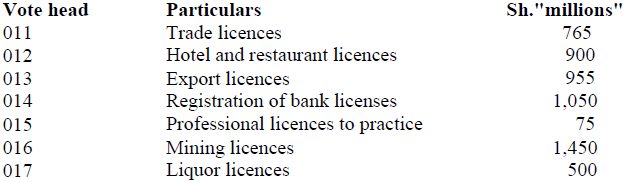

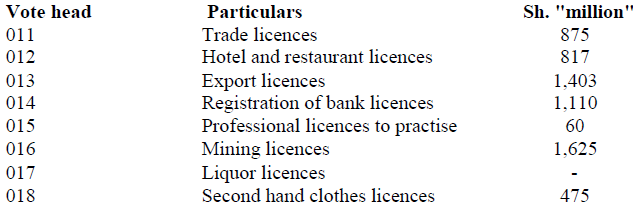

-

The Ministry of Finance estimated the revenue from licences for the year ended 30 June 2010 to be

follows:

During the year, the treasury introduced a new...

(Solved)

The Ministry of Finance estimated the revenue from licences for the year ended 30 June 2010 to be

follows:

During the year, the treasury introduced a new vote head 018, second hand clothes licences

under supplement estimate number 1.The estimated revenue from this vote head was Sh450

million. The actual revenue during the year was as follows:

Additional information:

1. The balance of revenue from licences as at 1 July 2009 was Sh. 325 million.

2. As at 30 June 2010, the amount of revenue from licences due to the Exchequer was Sh124 million

Required:

Statement of revenue for the year ended 30 June 2010.

Date posted:

May 16, 2019

.

Answers (1)

-

Highlight the importance of using accounting standards as the basis for preparing financial

statements.

(Solved)

Highlight the importance of using accounting standards as the basis for preparing financial

statements.

Date posted:

May 16, 2019

.

Answers (1)

-

The International Public Sector Accounting Standards (IPSASs) recommend the use of accrual

basis of accounting for public sector entities.

Discuss the case for and against the use...

(Solved)

The International Public Sector Accounting Standards (IPSASs) recommend the use of accrual

basis of accounting for public sector entities.

Discuss the case for and against the use of accrual basis of accounting in the public sector.

Date posted:

May 16, 2019

.

Answers (1)

-

Government expenditure is classified into recurrent expenditure and development

expenditure. Citing two examples, explain the two categories of expenditure.

(Solved)

Government expenditure is classified into recurrent expenditure and development

expenditure. Citing two examples, explain the two categories of expenditure.

Date posted:

May 16, 2019

.

Answers (1)

-

Sunny Side Ltd. began its operations on 1 July 2012 by raising Sh.52 million ordinary share

capital and issuing 18% per annum debentures.

The following information was...

(Solved)

Sunny Side Ltd. began its operations on 1 July 2012 by raising Sh.52 million ordinary share

capital and issuing 18% per annum debentures.

The following information was extracted from the books of the company for the year ended 30

June 2013:

1.

Item Sh. ‘000’

Dividends paid 3,376

Cash and bank balance 2,500

Operating costs (excluding finance cost) 31,320

Total non-current assets at net book value 60,000

2. The total current assets as at 30 June 2013 consisted

of: Σ Trade receivables.

Σ Inventory.

Σ Cash and bank balance.

3. The total current liabilities as at 30 June 2013 consisted of:

Σ Trade payables.

Σ Taxation charge for the year.

4. Taxation is to be provided for at the rate of 30% per annum.

5. 20% of the total sales for the year were made in cash.

6. Credit purchases during the year amounted to Sh. 28,800,000.

7. The accountant provided the following ratios which were determined from the financial

statements of the company:

Σ Inventory turnover 4.4 times

Σ Non-current asset turnover 1.8 times

Σ Gross profit margin 45%

Σ Average debt collection period 84 days

Σ Interest cover 4 times

Σ Average credit repayment period 90 days

Required:

i) Income statement for the year ended 30 June 2013.

ii) Statement of financial position as at 30 June 2013.

Note: Assume a year has 360 days.

Date posted:

May 16, 2019

.

Answers (1)

-

Explain the following terms as used in company accounts.

i) Cumulative preference shares.

ii) Public offer.

iii) Mortgaged debenture

(Solved)

Explain the following terms as used in company accounts.

i) Cumulative preference shares.

ii) Public offer.

iii) Mortgaged debenture

Date posted:

May 16, 2019

.

Answers (1)

-

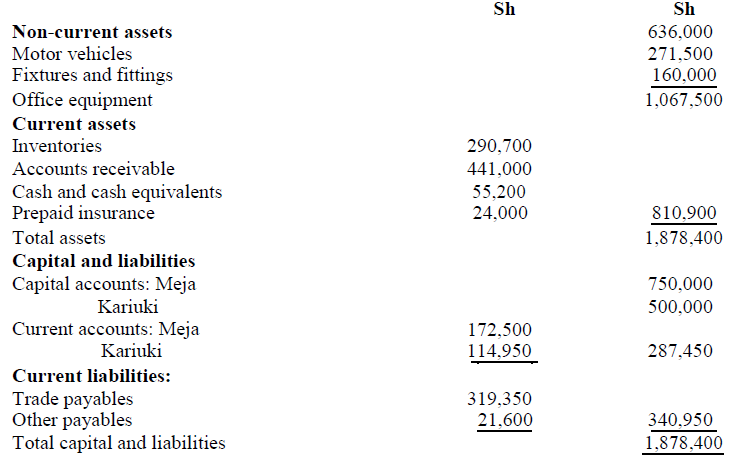

Meja and Kariuki have been trading as partners sharing profits and losses in the ratio of their fixed

capitals. The statement of financial position of the...

(Solved)

Meja and Kariuki have been trading as partners sharing profits and losses in the ratio of their fixed

capitals. The statement of financial position of the partnership as at 31 March 2011 was as follows:

The partners have been having some disagreements on the following issues:

1. The historical cost of the assets did not reflect the fair value of the assets.

2. Although the partners contributed different amounts as fixed capital, the partnership agreement

did not provide for payment of interest on capital.

3. Kariuki devoted his entire working time to the business of the partnership but the partnership

agreement did not provide for any salaries for active partners.

4. Kariuki strongly believed that the present profits and losses sharing ratio was inequitable.

At a meeting convened to resolve the above issues, the partners agreed as follows:

i) The non-current assets as at 31 March 2011 were to be revalued as follows:

Sh.

Motor vehicles 600,000

Fixtures and fittings 262,500

Office equipment 225,000

ii) Inventories as at 31 March 2011 were to be written down to Sh. 275,000 and Sh 16,000 was

to be written off as bad debts. An allowance for doubtful debts of 5% was to be provided on

the remaining accounts receivable.

iii) Interest on capital was to be allowed at 5% per annum for the years ended 31 March 2010 and

31 March 2011.

iv) Kariuki was to be paid a salary of Sh 90,000 per annum for the years ended 31 March 2010

and 31 March 2011.

v) Profits and losses were to be shared equally with effect from 1 April 2009

vi) Meja was to be compensated for his loss arising from the new profit sharing agreement by

allowing him goodwill of Sh. 200,000.The goodwill would not be retained in the books of the

partnership. The net profits for the year ended 31 March 2009,2010 and 2011 were Sh.

425,000,Sh. 525000 and Sh. 412,500 respectively.

Required:

a) Adjusted income statement and appropriation 2011 account for the years ended 31 March 2010

and 31March 2011

b) Partners' current accounts.

c) Statement of financial position as at 31 March 2011.

Date posted:

May 16, 2019

.

Answers (1)

-

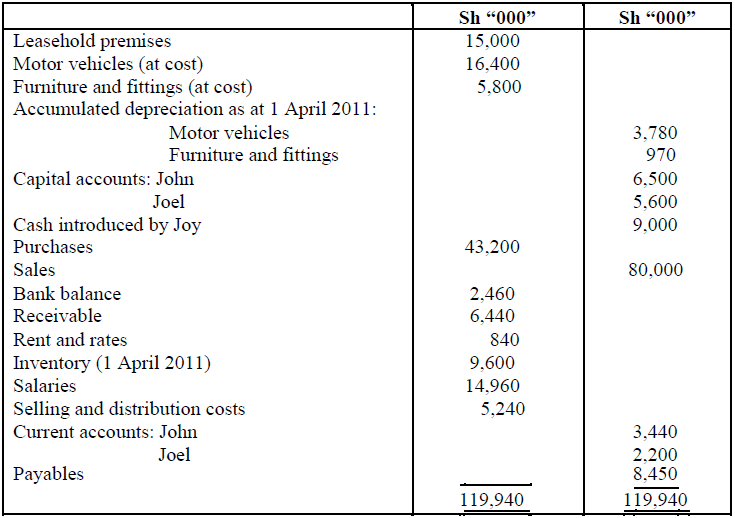

John and Joel were partners in a business sharing profits and losses in the ratio of 2:1. Interest on

fixed capital was allowed at the rate...

(Solved)

John and Joel were partners in a business sharing profits and losses in the ratio of 2:1. Interest on

fixed capital was allowed at the rate of 10% per annum. No interest was charged on current accounts.

On 30 September 2011 Joy was admitted as a partner and from that date profits and losses were to be

shared in the ratio of 2:2:1 for John, Joel and Joy respectively. Goodwill was not to be retained in the

books with adjusting entries being made in the current accounts.

The following trial balance was extracted from the partnership's books of account as at 31 March

2012:

Additional information:

1. No entries have been made to record the admission of Joy. Goodwill was agreed at Sh.10.5

million. Sh.6 million of the cash introduced by Joy was the fixed capital.

2. Salaries include the following partners' drawings:

Sh ‘000’

John 2,580

Joel 2,040

Joy 680

3. Depreciation is to be provided as follows:

Asset Rate per annum

Motor vehicles 20% on cost

Furniture and fittings 10% on cost

4. The sales during the six month period from 1 October 2011 to 31 March 2012 were 50% more

than the sales during the six month period from 1 April 2011 to 30 September 2011. The selling

and distribution expenses varied with the sales.

All other expenses accrued evenly.

5. Inventory as at 31 March 2012 was valued at Sh.11 million.

6. Allowance for doubtful debts was Sh.229,000 as at 30 September 2011 and Sh.309,000 as at 31

March 2012.

7. The leasehold premises is to be amortised over 30 years from 31 March 2011

Required:

a) Income statement for the year ended 31 March 2012.

b) Statement of financial position as at 3 I March 2012.

c) Partners' current accounts.

Date posted:

May 16, 2019

.

Answers (1)

-

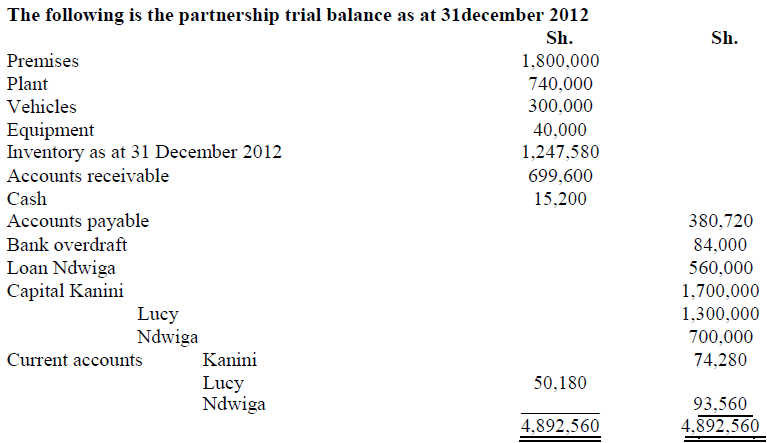

Kanini, Lucy and Ndwiga are in partnership sharing profits and losses in the ratio 3:2:1 respectively. Ndwiga decided to retire on 31 December 2012 and Gitonga...

(Solved)

Kanini, Lucy and Ndwiga are in partnership sharing profits and losses in the ratio 3:2:1 respectively.

Ndwiga decided to retire on 31 December 2012 and Gitonga was admitted as a partner on that date.

Additional information

1. Revaluation premises Sh. 2,400,000 plant Sh. 700,000 and inventory Sh. 1,083,580

2. Allowance for doubtful debts amounting to sh. 60,000 is to be provided

3. Goodwill amounting to sh. 840,000 is to be recorded in the books on the day Ndwiga retires. The

partners in the new partnership do not wish to maintain goodwill.

4. Kanini and Lucy are to share profits in the same ratio as before. Gitonga will have the same

share of profits as Lucy.

5. Ndwiga is to take his car at book value of sh. 78,000 in part payment and the balance of all he is

owned by the firm in cash except sh. 400,000 which he is willing to leave as a loan account.

6. The partners in the new firm are to start on equal footing so far as capital and current accounts are

concerned. Gitonga is to contribute cash to bring his capital and current accounts to the same

amount as the original partner from the old firm who has the lower investment in the business

7. The original partner in the old firm who has the higher investment will draw cash so that capital

and current account balances equal those of his new partners

Required;-

a) Partners capital account

b) Partners current account

c) Statement of financial position for the partnership of Kanini, Lucy and Gitonga as at 31

December 2012

Date posted:

May 16, 2019

.

Answers (1)

-

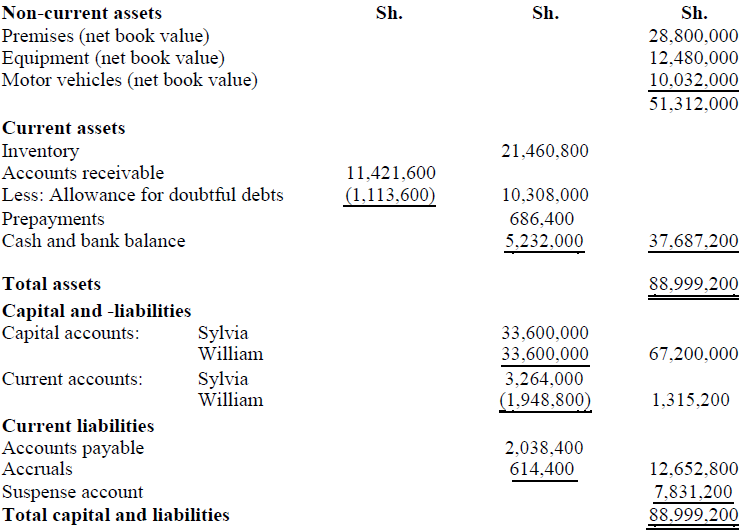

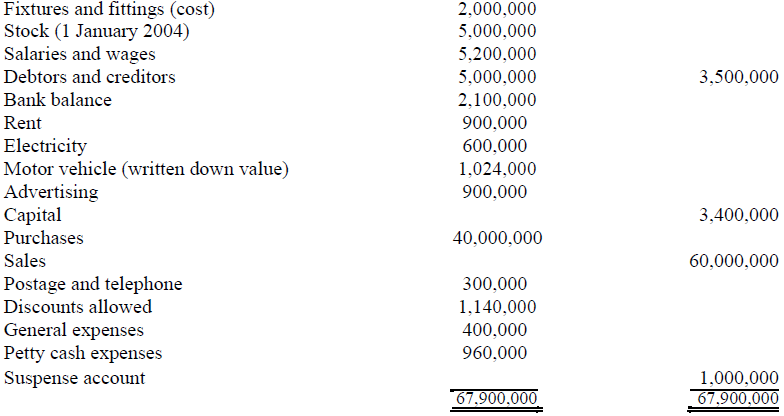

Sylivia and William are in a partnership business trading under the name Slywill Enterprises. Their

statement of financial position as at 31 October 2013 failed to...

(Solved)

Sylivia and William are in a partnership business trading under the name Slywill Enterprises. Their

statement of financial position as at 31 October 2013 failed to agree. The difference was-posted to a

suspense account pending investigations as shown below:

Additional information:

After checking all the entries, the following errors were discovered:

1. Discounts received of Sh. 633,600 had been debited to discounts allowed account.

2. The sales account had been undercast by Sh. 4,800,000.

3. The purchase returns day book had been correctly entered and totalled at Sh. 2,956,800 but had

not been posted to the ledger.

4. A credit sale of Sh. 705,600 had been debited to the customer's account as Sh. l,029,600.

5. A motor vehicle originally bought for Sh.3,360,000 four years ago and depreciated at 20% using

the straight-line method had a residual value of Sh.480,000. The motor vehicle was disposed of at

Sh.1,440,000

No entries, other than bank account, had been passed through the books.

6. An accrual of Sh. 268,800 for electricity charges had been omitted from the books.

7. A bad debt of Sh. 748,800 had not been written off.

8. Allowance for doubtful debts should be maintained at 10% of accounts receivable.

9. Sylvia's current account had been credited with a partnership salary of Sh. 1,440,000 which

should have been credited to William’s current account.

10. Sylvia had withdrawn goods worth Sh.940,800 for personal use. No entry had been made in the

partnership books.

11. The partners share profits as follows:

Sylvia - 60%

William - 40%

Required:

a) Suspense account, duly balanced, for the year ended 31 October 2013

b) Statement of adjustments to show the correct net profit for the year ended 31 October 2013

c) Partners' current accounts.

d) Statement of financial position as at 31 October 2013.

Date posted:

May 16, 2019

.

Answers (1)

-

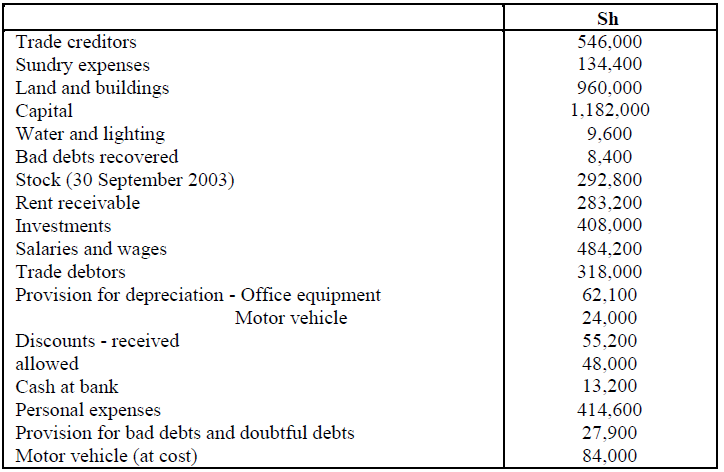

The following balances were extracted from the boob of Chuma Enterprises as at 30 September 2003.

Additional information:

1. Provision for depreciation on the motor vehicle and...

(Solved)

The following balances were extracted from the boob of Chuma Enterprises as at 30 September 2003.

Additional information:

1. Provision for depreciation on the motor vehicle and office equipment is to be provided so as to

reflect two years depreciation at the rate of 20% per annum on cost.

2. Rent received amounting to Sh.6,000 has not been recorded ill the accounts. The

proprietor converted this money to personal use.

3. The sales day book had been overcast by Sh.9,000.

4. Discounts allowed amounting to Sh.7,200 had been posted to the discounts allowed account but

not to the debtors account.

5. The sales returns day book had been overcast by Sh1,800.

6. Stock at 30 September 2003 included an item valued at Sh.60,000 which had been sold and

invoiced to a customer on 30 September 2003.

Required:

a) Profit and loss account for the year ended 30 September 2003

b) Balance sheet as a. 30 September 2003

Date posted:

May 16, 2019

.

Answers (1)

-

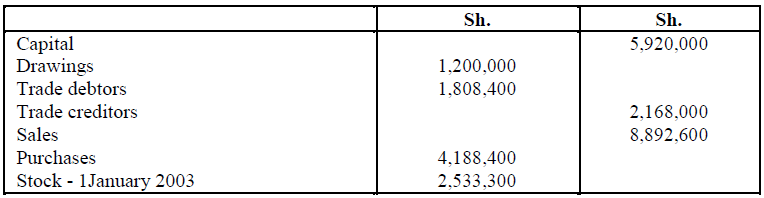

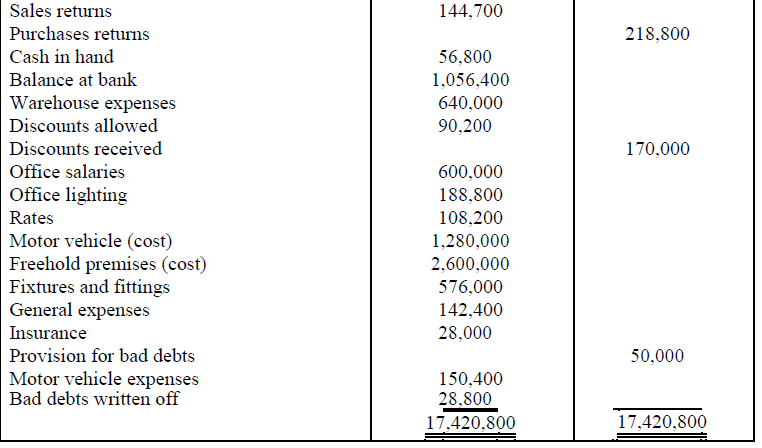

The following trial balance was extracted from the books of T. Onyancha a sole trader,

Additional information:

1. Stock as at 31 December 2003 was valued at...

(Solved)

The following trial balance was extracted from the books of T. Onyancha a sole trader,

Additional information:

1. Stock as at 31 December 2003 was valued at Sh. 1,760,000

2. Depreciation on fixtures and fittings and the motor vehicle is to be provided at the rate of 5% and

10% per annum on cost respectively.

3. Rates prepaid as at 31 December 2003 amounted to Sh.25,600.

4. Unexpired insurance as at 31 December 2003 is to be made at 2 1/2 of the trade debtors,

Required:

a) Trading and profit and loss account for the year ended 31 December 2003.

b) Balances sheet as at 31 December 2003.

Date posted:

May 16, 2019

.

Answers (1)

-

The following trial balance was extracted from the books of Hari Singh as at 31December 2004:

Additional information:

1. Closing stock as at 31 December 2004 was...

(Solved)

The following trial balance was extracted from the books of Hari Singh as at 31December 2004:

Sh. Sh

Drawings 1,600,000

Cash 676,000

Petty cash 100,000

Additional information:

1. Closing stock as at 31 December 2004 was valued at Sh.7,500,000

2. Petty cash balance represents the month end imprest amount. As at 31 December 2004, the petty

cashier had vouchers amounting to Sh40,000 which had not been reimbursed by the main

cashier.

3. Discounts allowed amounting to Sh.100,000 had been posted to the debit of the debtors account.

4. Sales had been undercast by Sh400,000.

5. The motor vehicle, which had been purchased on 1 January 2002, was being depreciated at

20% per annum on the reducing balance basis. The original cost of the motor vehicle was

Sh.2,000,000. It has been decided that the motor vehicle be depreciated at 6% per annum on the

straight line basis and to make the change effective from the date of purchase.

6. Cash withdrawn from the bank for business use amounting to Sh400,000 had not been entered

in the bank column of the cash book.

7. No entry bas been made for stock valued at Sh1,000,000 taken by the proprietor for personal

use.

8. Telephone bills amounting to Sh.100,000 were unpaid as at 31 December 2004.

9. Advertising expenses include the cost of a sales campaign conducted during the year of

Sh.600,000. It is expected that the benefits of this campaign will be enjoyed or the next three

years.

10. Fixtures and fittings are to be depreciated at 20%. per annum on cost.

Required:

a) Trading, profit and loss account or the year ended 31 December 2004.

b) Balance sheet as at 31 December 2004.

Date posted:

May 16, 2019

.

Answers (1)

-

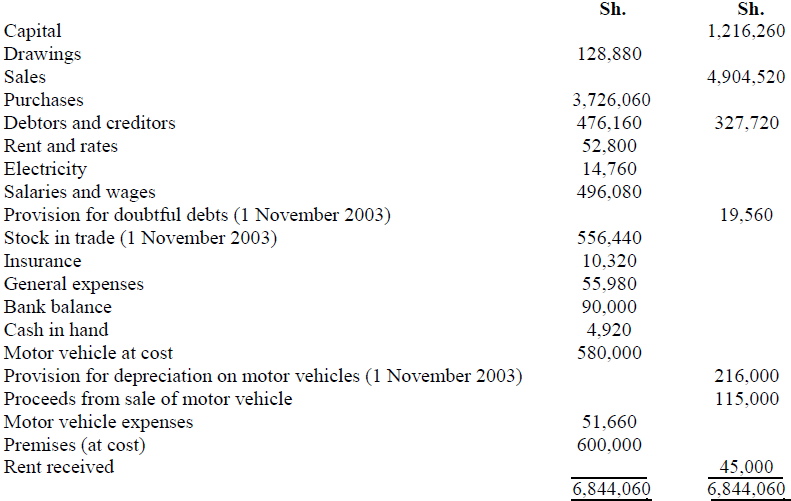

The following trial balance was extracted from the books of Mohammed Kagame, a sole trader, as at

31 October 2004:

1. Stock in trade a s at...

(Solved)

The following trial balance was extracted from the books of Mohammed Kagame, a sole trader, as at

31 October 2004:

1. Stock in trade a s at 31 October 2004 was valued at Sh593,040.

2. Rates and insurance were prepaid to the extent ofSh.2,400 and Sh.2,820 respectively, as at 3 J

October 2004,

3. Electricity due as at 31 October 2004 amounted to Sh.6,000.

4. The provision for doubtful debts is to be adjusted to S% of the debtors remaining after taking into

account that Sh.20, 1 60 of the debtors were to be regarded as bad.

5. Rent receivable as at 31 October 2004 was Sh. 15,000

6. Depreciation has been and is to be charged on motor vehicles at the rate of 20% per annum on the

straight line basis. No depreciation is to be charged on premises.

7. In November 2003, a motor vehicle which had been purchased or Sh.160,000 on I November

2000, was sold for Sh.115,000. The only record of this disposal is the entry in the proceeds from

sale of motor vehicle account.

Required:

a) Trading and profit and loss account or the year ended 31 October 2004

b) Balance sheet as at 3 I October 2004.

Date posted:

May 16, 2019

.

Answers (1)