- There are four types of standards. These are explained as under:-

a) Basic Standards

- These are the standards which do not change from year to year. In these standards, prices level of efficiency and other factors remain the same over a period of time. A basic standard may be defined as “A standard established for use over a long period from which a current standard can be developed.”

These standards do not take into consideration the current situation so these are not realistic.

Ideal Standards: Usually this standard cannot be attained and leads to unfavourable variances as it assumes:

1. Minimum prices for all costs (Direct Material, Direct Labour and Factory OH).

2. Optimal usage of Direct Material, Direct Labour and Factory OH.

3. 100% manufacturing capacity.

- Thus, these are based on perfect operation conditions. It is assumed that the ideal level of efficiency is achieved. It means there are no breakdowns, no material wastages, no labour idle times and so on. An ideal standard can be defined as “A standard which can be attained under the most favourable conditions. Ideal standards are difficult to apply because the conditions, on which these standards are based, cannot be fulfilled.

b) Attainable Standard

Can be met because it recognizes:

1. Good overall price but not necessarily the lowest price for all costs.

2. Direct labour is not 100% efficient.

3. Normal spoilage will occur.

4. Manufacturers do not operate at 100% capacity.

- Most companies presently use attainable standards but a new manufacturing environment is development that emphasizes ideal standards.

c) Expected Standards

- These are also known as attainable standards. These are based on normal operating conditions and an allowance is made for average wastages and inefficiencies. In this caser, it is assumed that there will be some loss of production due to power failure, machinery breakdown or labour turnover etc. an expected or attainable standard unit of work is carried out efficiently, a machine property operated or material properly used.” These standards are more realistic and easy to apply. These can be used for product costing, for cost control, for stock valuation and as a basis for budgeting. These standards have some provisions for wastages and inefficiency but it does not mean that it should encourage employees for making excuses for not achieving their targets.

d) Current standards

- These standards are set for use over a limited period to reflect current conditions. These standards are normally used in the situations when the inflationary trends are very common. In this case, the standards are revised on monthly basis. A current standard may be defined as, “A standard established for use over a short period of time, related to current conditions.” These standards are not practicable in most of the circumstances.

Wilfykil answered the question on August 6, 2019 at 09:21

-

Show the difference between Historical cost and Standard cost

(Solved)

Show the difference between Historical cost and Standard cost

Date posted:

August 6, 2019

.

Answers (1)

-

Compare and contrast on Budgetary Control and Standard Costing

(Solved)

Compare and contrast on Budgetary Control and Standard Costing

Date posted:

August 6, 2019

.

Answers (1)

-

Define the term Standard costing

(Solved)

Define the term Standard costing

Date posted:

August 6, 2019

.

Answers (1)

-

What does Standard Costing involve?

(Solved)

What does Standard Costing involve?

Date posted:

August 6, 2019

.

Answers (1)

-

During a period 3000 units of a main product were produced at sh 60 per unit.

(Solved)

During a period 3000 units of a main product were produced at sh 60 per unit. Total production were sh 125000. A by product was produced together with main product. This by-product was 100 units and it was sold for sh 55 per unit post separation cost of this by product were sh 500. Calculate the production cost and profit of the main product.

Date posted:

August 6, 2019

.

Answers (1)

-

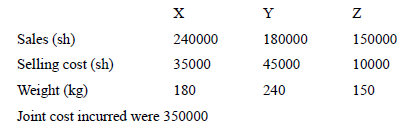

The following data relates to three products XYZ

(Solved)

The following data relates to three products XYZ

Required:

Calculate profit made by each product apportioning joint costs on;

i) Sales value bases

ii) Physical unit bases

Date posted:

August 6, 2019

.

Answers (1)

-

In a specific period production and cost data was as follows:

(Solved)

In a specific period production and cost data was as follows: Production was 1,600 full complete units and 400 partly complete units. The degree of completion of the 400 units WIP was as follows:

Required:

a) Calculate total equivalent unit

b) Cost per unit of complete units

c) Show the value of W.I.P

Date posted:

August 6, 2019

.

Answers (1)

-

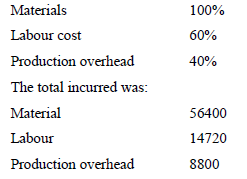

Using the data given below, show process 1 account where normal loss has a scrap value of sh1.8 per kilo.

(Solved)

Using the data given below, show process 1 account where normal loss has a scrap value of sh1.8 per kilo.

In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1. Labour cost amounted to sh 3,000 and production overheads sh 2,300, normal loss has been estimated at 10% . The actual product after process was 1750kg.

Date posted:

August 6, 2019

.

Answers (1)

-

In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1.

(Solved)

In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1. Labour cost amounted to sh 3,000 and production overheads sh 2,300, normal loss has been estimated at 10% . The actual product after process was 1750kg.

Required: Prepare process 1 account

Date posted:

August 6, 2019

.

Answers (1)

-

What is meant by Process loss scrap and waste?

(Solved)

What is meant by Process loss scrap and waste?

Date posted:

August 6, 2019

.

Answers (1)

-

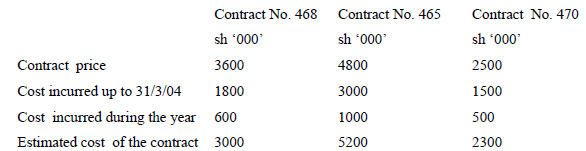

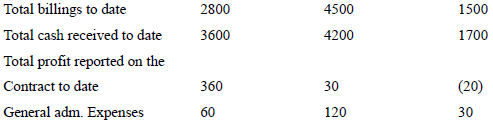

Njenga Limited is a construction Co. whose financial year end is 31st March.

(Solved)

Njenga Limited is a construction Co. whose financial year end is 31st March. The information provided was extracted from the books of the company in contraction with three construction contracts undertaken by the company during the financial year ended 31st March 2005

Required:

Using the percentage of completing method of accounting for long term construction contract:

1. Calculate profit/less realized on each contract for the year ended 31st March 2005.

2. Prepare profit and loss extract for each contract for year ended 31st March 2005.

3. Prepare balance sheet extract as at 31st March 2005.

Date posted:

August 6, 2019

.

Answers (1)

-

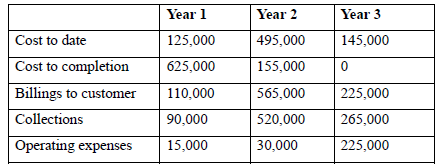

A small bridge is to be constructed by the beginning of the year at a fixed price of sh 900,000 with estimates contract cost of...

(Solved)

A small bridge is to be constructed by the beginning of the year at a fixed price of sh 900,000 with estimates contract cost of sh 750,000 in year one. The following summaries are presented:

Required:

a) Prepare a statement showing the profit recognized in each year.

b) Balance sheet extract.

c) Journal entries to account for the extraction

Date posted:

August 6, 2019

.

Answers (1)

-

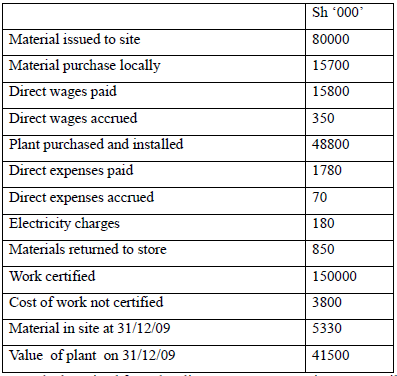

HZ Construction Company acquired a contact for the construction of a dual carriage way from Nairobi at cost of 200 million.

(Solved)

HZ Construction Company acquired a contact for the construction of a dual carriage way from Nairobi at cost of 200 million. The data relating to the contract for year ended 31st December 2009 was as follows:

The company had received from the client payment amounting to 126 million.

Required:

(i) Contract account

(ii) Contractee account

(iii) Balance sheets extract showing work in progress.

Date posted:

August 6, 2019

.

Answers (1)

-

Give and explain cases where job costing is applied

(Solved)

Give and explain cases where job costing is applied

Date posted:

August 6, 2019

.

Answers (1)

-

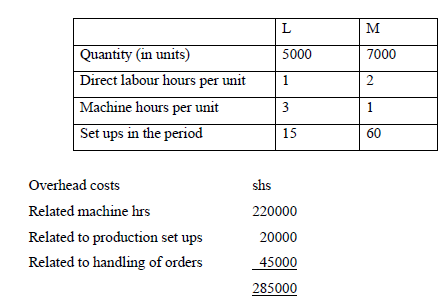

A company manufactures products L and M using the same equipment and similar processes. An extract of the production data for these products in one...

(Solved)

A company manufactures products L and M using the same equipment and similar processes. An extract of the production data for these products in one period is as follows.

Required:

Calculate the production overhead to be absorbed by one of each other product using the following costing methods.

(a) A traditional costing approach using direct labour hour rate to absorb overheat.

(b) An activity based costing approach using suitable cost drivers to trace overheads to products.

Date posted:

August 6, 2019

.

Answers (1)

-

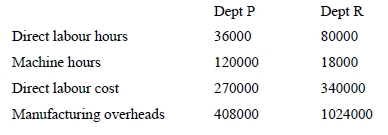

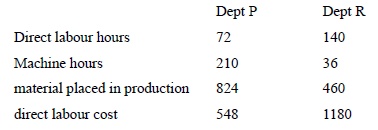

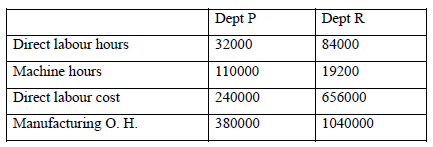

Gome Engineering Ltd. Employees job order cost system. The company use predetermined overheads rates in rime manufacturing overheads to jobs.

(Solved)

Gome Engineering Ltd. Employees job order cost system. The company use predetermined overheads rates in rime manufacturing overheads to jobs. The following additional information is presented by the company‟s cost accountant.

1. The company has two departments P and R. The predetermined overhead rates is based on machine hours for Dept P and direct labour cost for Dept R. As at 31st January 2003 the cost accountant made the following estimates for the year.

2. The companies cost records show the following information on job YJ 648.

Required:

a) Complete the predetermined overhead rates that should be used during the year in Dept P and R.

b) Compute the total overhead cost applied in job EFJ 648.

c) Calculate the cost of job FJ 648 and the cost per unit if the job containers 120 units.

d) As at 31st Dec 2003 the company records revealed the following information in relation to each department.

Calculate the amount of under / over applied overheads in each department and for the company as a whole.

Date posted:

August 6, 2019

.

Answers (1)

-

Discuss the Overhead Absorption

(Solved)

Discuss the Overhead Absorption

Date posted:

August 6, 2019

.

Answers (1)

-

Explain the purposes of overhead cost analysis

(Solved)

Explain the purposes of overhead cost analysis

Date posted:

August 5, 2019

.

Answers (1)

-

Define the following terms:

(Solved)

Define the following terms:

1. Allocation

2. Apportionment

3. Reapportionment

4. A reciprocal service charge

5. Absorption

Date posted:

August 5, 2019

.

Answers (1)

-

Discuss the topic Overhead Analysis

(Solved)

Discuss the topic Overhead Analysis

Date posted:

August 5, 2019

.

Answers (1)