Phase 1 - Pre Acquisition Review:

The first step is to assess your own situation and determine if a merger and acquisition strategy should be

implemented. If a company expects difficulty in the future when it comes to maintaining core competencies,

market share, return on capital, or other key performance drivers, then a merger and acquisition (M & A)

program may be necessary.

It is also useful to ascertain if the company is undervalued. If a company fails to protect its valuation, it may find

itself the target of a merger. Therefore, the pre-acquisition phase will often include a valuation of the company -

Are we undervalued? Would an M & A Program improve our valuations?

The primary focus within the Pre Acquisition Review is to determine if growth targets (such as 10% market

growth over the next 3 years) can be achieved internally. If not, an M & A Team should be formed to establish a

set of criteria whereby the company can grow through acquisition. A complete rough plan should be developed

on how growth will occur through M & A, including responsibilities within the company, how information will

be gathered, etc.

Phase 2 - Search & Screen Targets:

The second phase within the M & A Process is to search for possible takeover candidates. Target companies

must fulfill a set of criteria so that the Target Company is a good strategic fit with the acquiring company. For

example, the target's drivers of performance should compliment the acquiring company. Compatibility and fit

should be assessed across a range of criteria - relative size, type of business, capital structure, organizational

strengths, core competencies, market channels, etc.

It is worth noting that the search and screening process is performed in-house by the Acquiring Company.

Reliance on outside investment firms is kept to a minimum since the preliminary stages of M & A must be highly

guarded and independent.

Phase 3 - Investigate & Value the Target:

The third phase of M & A is to perform a more detail analysis of the target company. You want to confirm that

the Target Company is truly a good fit with the acquiring company. This will require a more thorough review of

operations, strategies, financials, and other aspects of the Target Company. This detail review is called "due

diligence." Specifically, Phase I Due Diligence is initiated once a target company has been selected. The main

objective is to identify various synergy values that can be realized through an M & A of the Target Company.

Investment Bankers now enter into the M & A process to assist with this evaluation.

A key part of due diligence is the valuation of the target company. In the preliminary phases of M & A, we will

calculate a total value for the combined company. We have already calculated a value for our company (acquiring

company). We now want to calculate a value for the target as well as all other costs associated with the M & A.

Phase 4 - Acquire through Negotiation:

Now that we have selected our target company, it's time to start the process of negotiating a M & A. We need to

develop a negotiation plan based on several key questions:

- How much resistance will we encounter from the Target Company?

- What are the benefits of the M & A for the Target Company?

- What will be our bidding strategy?

- How much do we offer in the first round of bidding?

The most common approach to acquiring another company is for both companies to reach agreement

concerning the M & A; i.e. a negotiated merger will take place. This negotiated arrangement is sometimes called a

"bear hug." The negotiated merger or bear hug is the preferred approach to a M & A since having both sides

agree to the deal will go a long way to making the M & A work. In cases where resistance is expected from the

target, the acquiring firm will acquire a partial interest in the target; sometimes referred to as a "toehold position."

This toehold position puts pressure on the target to negotiate without sending the target into panic mode.

In cases where the target is expected to strongly fight a takeover attempt, the acquiring company will make a

tender offer directly to the shareholders of the target, bypassing the target's management. Tender offers are

characterized by the following:

- The price offered is above the target's prevailing market price.

- The offer applies to a substantial, if not all, outstanding shares of stock.

- The offer is open for a limited period of time.

- The offer is made to the public shareholders of the target.

Another important element when two companies merge is Phase II Due Diligence. As you may recall, Phase I

Due Diligence started when we selected our target company. Once we start the negotiation process with the

target company, a much more intense level of due diligence (Phase II) will begin. Both companies, assuming we

have a negotiated merger, will launch a very detailed review to determine if the proposed merger will work. This

requires a very detail review of the target company - financials, operations, corporate culture, strategic issues, etc.

Phase 5 - Post Merger Integration:

If all goes well, the two companies will announce an agreement to merge the two companies. The deal is

finalized in a formal merger and acquisition agreement. This leads us to the fifth and final phase within the M &

A Process, the integration of the two companies.

Every company is different - differences in culture, differences in information systems, differences in strategies,

etc. As a result, the Post Merger Integration Phase is the most difficult phase within the M & A Process. Now all

of a sudden we have to bring these two companies together and make the whole thing work. This requires

extensive planning and design throughout the entire organization. The integration process can take place at three

levels:

Full: All functional areas (operations, marketing, finance, human resources, etc.) will be merged into one new

company. The new company will use the "best practices" between the two companies.

Moderate: Certain key functions or processes (such as production) will be merged together. Strategic decisions

will be centralized within one company, but day to day operating decisions will remain autonomous.

Minimal: Only selected personnel will be merged together in order to reduce redundancies. Both strategic and

operating decisions will remain decentralized and autonomous.

If post merger integration is successful, then we should generate synergy values. However, before we embark on

a formal merger and acquisition program, perhaps we need to understand the realities of mergers and

acquisitions.

Kavungya answered the question on April 14, 2021 at 11:29

-

State and explain the reasons of business mergers.

(Solved)

State and explain the reasons of business mergers.

Date posted:

April 14, 2021

.

Answers (1)

-

State and explain the types of mergers.

(Solved)

State and explain the types of mergers.

Date posted:

April 14, 2021

.

Answers (1)

-

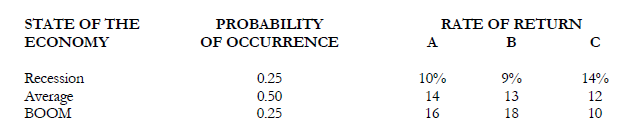

XYZ ltd. is considering three possible capital projects for next year. Each project has a 1 year life, and

project returns depend on next years state...

(Solved)

XYZ ltd. is considering three possible capital projects for next year. Each project has a 1 year life, and

project returns depend on next years state of the economy. The estimated rates of return are shown below.

a. Find each project expected rate of return, variance, standard deviation and coefficient of

variation.

b. Compute the correlation coefficient between

i. A and B

ii. A and C

iii. B and C

c. Compute the expected return on a portfolio if the firm invests equal wealth on each asset.

d. Compute the standard deviation of the portfolio.

Date posted:

April 13, 2021

.

Answers (1)

-

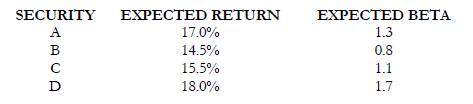

The risk free rate is 10% and the expected return on the market portfolio is 15%. The expected returns for 4

securities are listed below together...

(Solved)

The risk free rate is 10% and the expected return on the market portfolio is 15%. The expected returns for 4

securities are listed below together with their expected betas.

a. On the basis of these expectations, which securities are overvalued? Which are undervalued?

b. If the risk-free rate were to rise to 12% and the expected return on the market portfolio rose to 16%,

which securities would be overvalued? which would be under-valued? (Assume the expected returns

and the betas remain the same).

Date posted:

April 13, 2021

.

Answers (1)

-

Securities D, E and F have the following characteristics with respect to expected return, standard deviation

and correlation coefficients.

Compute the expected rate of return and standard...

(Solved)

Securities D, E and F have the following characteristics with respect to expected return, standard deviation

and correlation coefficients.

Compute the expected rate of return and standard deviation of a portfolio comprised of equal investment in

each security.

Date posted:

April 13, 2021

.

Answers (1)

-

Security returns depend on only three risk factors-inflation, industrial production and the aggregate degree of

risk aversion. The risk free rate is 8%, the required rate...

(Solved)

Security returns depend on only three risk factors-inflation, industrial production and the aggregate degree of

risk aversion. The risk free rate is 8%, the required rate of return on a portfolio with unit sensitivity to

inflation and zero-sensitivity to other factors is 13.0%, the required rate of return on a portfolio with unit

sensitivity to industrial production and zero sensitivity to inflation and other factors is 10% and the required

return on a portfolio with unit sensitivity to the degree of risk aversion and zero sensitivity to other factors is

6%. Security i has betas of 0.9 with the inflation portfolio, 1.2 with the industrial production and-0.7 with

risk bearing portfolio—(risk aversion)

Assume also that required rate of return on the market is 15% and stock i has CAPM beta of 1.1

Required:

Compute security i's required rate of return using

a. CAPM

b. APT

Date posted:

April 13, 2021

.

Answers (1)

-

Assume that the risk free rate of return is 8%, the market expected rate of return is 12%. The standard deviation of the market return...

(Solved)

Assume that the risk free rate of return is 8%, the market expected rate of return is 12%. The standard deviation of the market return is 2% while the covariance of return for security A and the market is 2%.

What is the required rate of return on Security A?

Date posted:

April 13, 2021

.

Answers (1)

-

What are efficient portfolios?

(Solved)

What are efficient portfolios?

Date posted:

April 13, 2021

.

Answers (1)

-

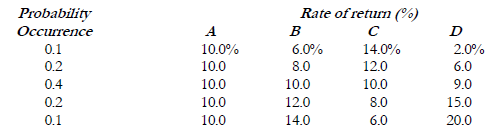

Four assets have the following distribution of returns.a. Compute the expected return and standard deviation of each asset.b. Compute the covariance of asseti. A and...

(Solved)

Four assets have the following distribution of returns.

Required.

a. Compute the expected return and standard deviation of each asset.

b. Compute the covariance of asset

i. A and B

ii. B and C

iii. B and D

c. Compute the correlation coefficient of the combination of assets in b above.

Date posted:

April 13, 2021

.

Answers (1)

-

Consider two investments A & B each having the following characteristics:

Compute the portfolio standard deviation if the correlation coefficient between the assets is

a. 1

b. 0

c....

(Solved)

Consider two investments A & B each having the following characteristics:

Investment Expected Return (%) Proportion

A 20 2/3

B 40 1/3

REQUIRED:

Compute the portfolio standard deviation if the correlation coefficient between the assets is

a. 1

b. 0

c. -1

Date posted:

April 13, 2021

.

Answers (1)

-

Consider two investments, A and B each having the following investment characteristics;

Compute the expected return of a portfolio of the two assets.

(Solved)

Consider two investments, A and B each having the following investment characteristics;

Investment Expected Return (%) Proportion

A 10 2/3

B 20 1/3

Required.

Compute the expected return of a portfolio of the two assets.

Date posted:

April 13, 2021

.

Answers (1)

-

A piece of equipment requiring the investment of 2.2 million is being considered by Charo Foods Ltd. The equipment has a ten-year useful life and...

(Solved)

A piece of equipment requiring the investment of 2.2 million is being considered by Charo Foods Ltd. The equipment has a ten-year useful life and an expected salvage value of Sh 200,000. The company uses the straight-line method of depreciation for analyzing investment decisions and faces a tax rate of 40%. For simplicity assume that the depreciation method is acceptable for tax purposes.

A pessimistic forecast projects cash earnings before depreciation and taxes at Sh 400,000 per year compared with an optimistic estimate of Sh 500,000 per year. The probability associated with the pessimistic estimate is 0.4 and 0.6 for the optimistic forecast. The company has a policy of using a hurdle rate of 10% for replacement investments, 12% (its cost of capital) for revenue expansion investments into existing product lines and 15% projects involving new areas or new product lines.

REQUIRED:

(a) Compute the expected annual cash flows associated with the proposed equipment investments.

(b) Would you recommend acceptance of this project if it involved expansion of sales for an existing product?

(c) Would it be acceptable if it was for the replacement of equipment with a book value of Sh 200,000 at the end of the tenth year but which could be sold at that time for only Sh 40,000?

(d) Discounted cash flow methods were developed for idealized settings of complete and perfect capital, factor and commodity markets. Explain what complications arise when an attempt is made to apply these methods in real life markets that are neither complete nor perfect.

Date posted:

April 13, 2021

.

Answers (1)

-

The Mentala Plastics Company has been dumping in the local council waste collection

centre some 30,000 Kg. of unusable chemicals each year. In addition to being...

(Solved)

The Mentala Plastics Company has been dumping in the local council waste collection

centre some 30,000 Kg. of unusable chemicals each year. In addition to being an

eyesore, the residents of a nearby estate have started complaining of bad odour

emanating from the dump and suspect that the company is to blame.

The company has received information that these chemicals can be recycled at relatively little

cost. The equipment to do it is however rather expensive and, in addition, the chemicals

recovered are of a relatively poor quality. Investigations have shown that these chemicals can

be sold to another firm at an average price of Sh.35 per Kg. The direct cost of recycling has

been calculated at Sh.15 per Kg. but this is before depreciation and taxes.

The equipment for this process has an expected life of 10 years and a current cost of Sh.2 million. At the

end of the ten years, it will be virtually worthless.

For financial analysis, the company uses the straight line method of depreciation and an average tax rate of

40%. It has a required rate of return of 15%.

REQUIRED:

i. Compute the project's net present value (N.P.V).

ii. Compute the payback period and the accounting rate of return.

iii. Compute the internal rate of return (IRR).

iv. Should this project be undertaken? Explain.

Are there any other important matters that the company should consider in evaluating this project?

Date posted:

April 13, 2021

.

Answers (1)

-

Explain the concept of "rate of interest" in the context of financial decisions.

(Solved)

Explain the concept of "rate of interest" in the context of financial decisions.

Date posted:

April 13, 2021

.

Answers (1)

-

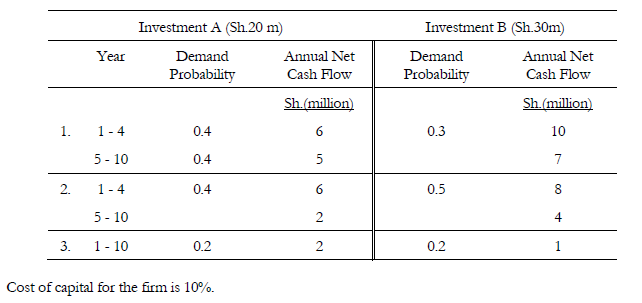

The Zeda Company Ltd. is considering a substantial investment in a new production process. From a

variety of sources, the total cost of the project has...

(Solved)

The Zeda Company Ltd. is considering a substantial investment in a new production process. From a

variety of sources, the total cost of the project has been estimated at Sh.20 million. However, if the

investment were to be increased to Sh.30 million, the productive capacity of the plant could be substantially

increased. Due to the nature of the process, it would be exorbitantly expensive to increase capacity once the

equipment is installed.

Once of the problems facing the company is that there is a considerable degree of uncertainty regarding

demand for the product. After some research which has been conducted jointly by the marketing and

finance departments, some data has been produced. These are shown below:

REQUIRED:

(a) Prepare a statement which clearly indicates the financial implications of each of the two alternative

investment scenarios.

(b) Comment on other matters which the management should take into account before reaching

the final decision.

PVIFA: 10% 5 years = 3.79

PVIFA: 10% 10 years = 6.14

PVIFA: 10% 10 years = 0.62

Date posted:

April 13, 2021

.

Answers (1)

-

State the disadvantages of utility approach.

(Solved)

State the disadvantages of utility approach.

Date posted:

April 13, 2021

.

Answers (1)

-

State the demerits of decision tree.

(Solved)

State the demerits of decision tree.

Date posted:

April 13, 2021

.

Answers (1)

-

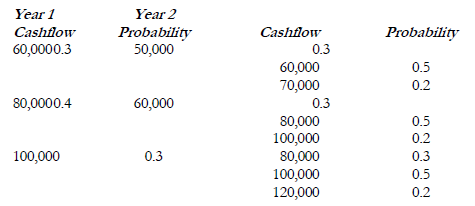

A project has the following cash flows

The projects initial cash outlay is Sh 100,000 with a cost of capital of 12%.

Required:

Determine:

(a) The projects expected monetary...

(Solved)

A project has the following cash flows

The projects initial cash outlay is Sh 100,000 with a cost of capital of 12%.

Required:

Determine:

(a) The projects expected monetary value (EMV)

(b) The projects NPV

Date posted:

April 13, 2021

.

Answers (1)

-

Outline the factors affecting the projects net present value.

(Solved)

Outline the factors affecting the projects net present value.

Date posted:

April 13, 2021

.

Answers (1)

-

State the advantages of sensitivity analysis.

(Solved)

State the advantages of sensitivity analysis.

Date posted:

April 13, 2021

.

Answers (1)