(a) Large – scale service organizations have a number of features that have been identified as

being necessary to drive significant benefits from the introduction of ABC:

i. They operate in a highly competitive environment

ii. They incur a large proportion of indirect costs that cannot be directly assigned to

specific cost objects.

iii. Products and consumers differ significantly in terms of consuming overhead resources.

iv. They market many different products and services.

Furthermore, many of the constraints imposed on manufacturing organizations, such as also having

to meet financial accounting stock valuation requirements, or a reluctance to change or scrap existing

systems, do not apply. Many services organizations have only recently implemented cost systems for

the first time. This has occurred at the same time as when the weaknesses of existing systems and the

benefits of ABC systems were being widely publicized. These conditions have provided a strong

measure for introducing ABC systems.

(b) The following may create problems for the application of ABC.

i. Facility sustaining costs (such as property rents etc) represent a significant

proportion of total costs and may only be avoidable if the organization ceases

business. It may be impossible to establish appropriate cost drivers

ii. It?s often difficult to define products where they are of an intangible

nature. Cost objects can therefore be difficult to specify;

iii. Many service organizations have not previously had a costing system and much of

the information required to set up an ABC system will be non-existent. Therefore

introducing ABC is likely to be expensive.

(c) The uses for ABC information for service industries are similar to those for manufacturing

organizations:

i. It leads to more accurate product costs as a basis for pricing decisions when cost plus

pricing methods are used;

ii. It results in more accurate product and customer profitability analysis

statements that provide a more appropriate basis for decision-making.

iii. ABC attaches costs to activities and identifies the cost drivers that cause the costs.

Thus ABC provides a better understanding of what causes costs and highlights

ways of performing activities more effectively by reducing cost driver transactions.

Costs can therefore be managed more effectively in the long term. Activities can be

analyzed into value added and non-value added activities alteration is drawn to areas

where there is a potential for cost reduction without reducing the products

service potentials to customers.

Kavungya answered the question on May 5, 2021 at 18:13

-

Explain the advantages and disadvantages of the Just-In-Tie (JIT) inventory system.

(Solved)

Explain the advantages and disadvantages of the Just-In-Tie (JIT) inventory system.

Date posted:

May 4, 2021

.

Answers (1)

-

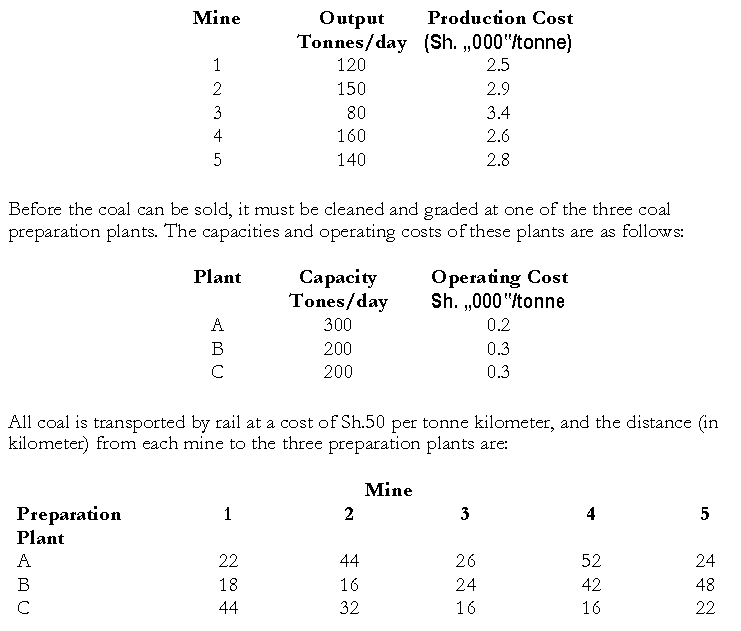

In all the Republic of Ramuka there are five coal mines, which have the following outputs and production costs:

Required:

a) Determine how the output of each...

(Solved)

In all the Republic of Ramuka there are five coal mines, which have the following outputs and production costs:

Required:

a) Determine how the output of each mine should be allocated to the three preparation plants.

b) Following the installation of a new equipment at coal mine No.3, the production

cost is expected to fall to Sh.3,000 per tonne.

What effect, if any, will have on the allocation of coal to the preparation plant?

c) It is planned to increase the output of coal mine No.5 to 180 tonnes per day, which

can be achieved without any increase in production cost per tonne.

How will this affect the allocation of coal to the preparation plants?

Date posted:

May 4, 2021

.

Answers (1)

-

“If a manager searches for a system that will provide the „true costs? of each service produced by his firm he is attempting the impossible”....

(Solved)

“If a manager searches for a system that will provide the „true costs‟ of each service produced by his firm he is attempting the impossible”. Discuss.

Date posted:

May 4, 2021

.

Answers (1)

-

State the major characteristics of modern businesses that necessitate the introduction of a strategic cost management system

(Solved)

State the major characteristics of modern businesses that necessitate the introduction of a strategic cost management system

Date posted:

May 4, 2021

.

Answers (1)

-

Kisumu Municipal council operates a mini-bus service to take shoppers and tourist from the bus and the railway stations to various locations in the Municipality....

(Solved)

Kisumu Municipal council operates a mini-bus service to take shoppers and tourist from the bus and the railway stations to various locations in the Municipality. The following data have been collected for the arrival of passengers at the bus stop outside the railway station:

Time between successive arrivals 0 1 2 3 4 5 6

(minutes)

Probability 0.04 0.16 0.24 0.28 0.16 0.10 0.02

The mini-buses are scheduled to run every 10 minutes but variation in traffic conditions

results in the following distribution.

Time between successive buses 8 10 12 14 16

(minutes)

Probability 0.10 0.38 0.28 0.15 0.09

The number of empty seats on the bus is found to follow the distribution below:

Number of empty seats 0 1 2 3 4 5 6

Probability 0.06 0.18 0.27 0.34 0.11 0.03 0.01

Required:

i. Simulate the arrival of to passengers at the bus stop assuming that the simulation clock

begins at time zero. Use the following random numbers:

18262318624207384092976446757444417165809

i i. Estimate the average time a passenger must wait for a bus and the average length of queue

Date posted:

May 4, 2021

.

Answers (1)

-

Kamau and Njoroge are two cousins specializing in hawking business along River

road. Kamau specializes in second hand shirts while Njoroge specializes in cheap

electronic goods. However,...

(Solved)

Kamau and Njoroge are two cousins specializing in hawking business along River

road. Kamau specializes in second hand shirts while Njoroge specializes in cheap

electronic goods. However, sales have been decreasing partly due to the harsh

economic condition in Kenya and partly due to restrictions by the City Council.

Each of the cousins is considering expanding to include in their lines of business,

items on which their rivals now have a monopoly. Each knows that the other is

considering this expansion and this influences each of their decisions.

Kamau figures out that if he does not expand his business and his cousin does, it will

hurt his trade by Sh.500 of profit per day. If neither of them expands inventory to

include the extra product, Kamau thinks it will boost his net profit by Sh.500 per day

due to his superior location. If he expands and his cousin does also, he believes the

combination of location and expanded inventory will increase his profits by Sh.1,000

per day. However, if he alone expands and his cousin does not, this will result in no

net increase in business.

Required:

i Prepare a game matrix and show that a pure strategy does not exist.

ii Solve the above game to determine the average winnings (or losses) each of the cousins would expect.

Date posted:

May 4, 2021

.

Answers (1)

-

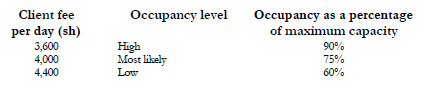

Mount Sinai Health Centre specializes in the provision of sports/exercise and

medical/dietary advice to clients. The service is provided on a residential basis and

clients reside for...

(Solved)

Mount Sinai Health Centre specializes in the provision of sports/exercise and

medical/dietary advice to clients. The service is provided on a residential basis and

clients reside for whatever number of days that suit their needs.

Budgeted estimates for the year ending 300 June 2002 are as follows:

1. The maximum capacity of the center is 50 clients per day for 350 days in the year.

2. Clients will be invoiced at a fee per day. The budgeted occupancy level will vary with

the client fee level per day and is estimated at different percentages of maximum

capacity as follows:

3. Variable costs are also estimated at one of the three levels per client day. The high

most likely and low levels per client per day are Sh.1,900, Sh.1,700 ad Sh.1,400

respectively.

4. The range of cost levels reflects only the possible effect of the purchase prices of

goods and services.

Required:

i. A summary which shows the budgeted contribution to be earned by Mount Sinai Health

Centre for the year ended 30 June 2002 for each of the nine possible outcomes.

ii. State the client fee strategy for the year to end 30 June 20002 which will result from the use

of each of the following decision rules.

(a) Maximax;

(b) Maximin;

(c) Minimax regret.

Date posted:

May 4, 2021

.

Answers (1)

-

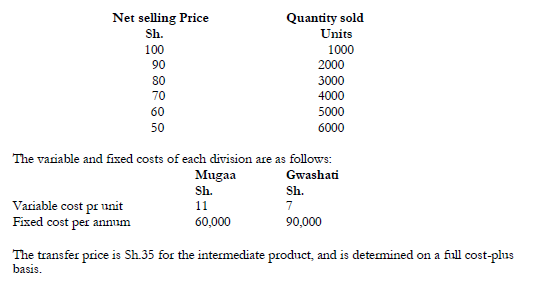

Kanorer Enterprises Ltd has two divisions Mugaa and Gwashati. Mugaa division manufactures an intermediate product for which there is no external market. Gwashati division incorporates...

(Solved)

Kanorer Enterprises Ltd has two divisions Mugaa and Gwashati. Mugaa division manufactures an intermediate product for which there is no external market. Gwashati division incorporates the intermediate product into a final product, which it sells. One unit of the intermediate product is used in the production of the final product. The expected units of the final product which Gwashati division estimates it can sell at various selling

prices are as follows:

Required:

a) Profit statements for each division and the company as a whole for the various selling

prices.

b) Which selling prices maximize the profits of Gwashati division and the company as a

whole? Comment on why the selling price (which is selected by the company) is not

selected by Gwashati division.

c) It has been argued that full cost is an inappropriate basis for selling transfer prices.

Outline the objections which can be raised against this basis.

Date posted:

May 3, 2021

.

Answers (1)

-

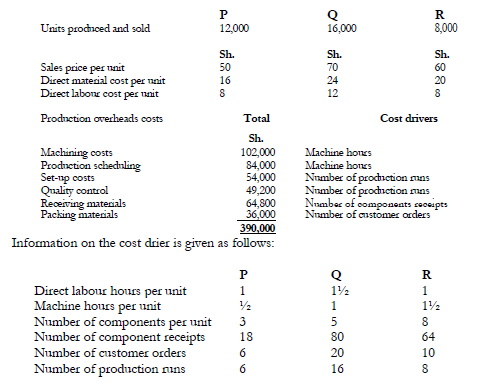

ABC Lt. Is a manufacturing company that makes only three products P, Q, and R. Data for the period ended last month are as follows:

Required:

Using...

(Solved)

ABC Lt. Is a manufacturing company that makes only three products P, Q, and R. Data for the period ended last month are as follows:

Required:

Using activity based costing (ABC) show the cost and gross profit per unit for each product during the period.

Date posted:

May 3, 2021

.

Answers (1)

-

Explain the advantages of using Value Added Statements (VAS) for interdivision for comparisons in decentralized firm.

(Solved)

Explain the advantages of using Value Added Statements (VAS) for interdivision for comparisons in decentralized firm.

Date posted:

May 3, 2021

.

Answers (1)

-

Some businesses which supply two or more separate markets from a single source may decide to charge a higher price for sales to home markets...

(Solved)

Some businesses which supply two or more separate markets from a single source may decide to charge a higher price for sales to home markets than for export sales. The businesses may justify their pricing policy by stating that they need to earn foreign exchange from foreign markets and recover their research and development costs, plus production overheads against home demand.

Required:

i Critically explain briefly the rationale for such a differential pricing policy.

ii Should earning of foreign exchange be a factor in a firm's pricing policy.

Date posted:

May 3, 2021

.

Answers (1)

-

Alvis Kiptoo has budgeted that output and sales of his single product will be 100,000

units in the coming year. At this level of activity, his...

(Solved)

Alvis Kiptoo has budgeted that output and sales of his single product will be 100,000

units in the coming year. At this level of activity, his unit variable costs are budgeted at

Sh.50 and his unit fixed costs at Sh.25. His sales manager estimates that the demand for

the product would increases by 1000 units for every decreased of Sh.1 in unit selling

price (and vice versa) and that at a unit selling price of Sh.200 demand would be nil.

Information about two price increases has just been received from suppliers: one is for

materials (which are included in Alvis Kiptoo‟s variable costs) and one is for

fuel (which included in his fixed costs). Their effect will be to increase both the variable

and fixed costs by 20% each over the budgeted figures.

Alvis Kiptoo aims at maximizing profits from his business.

Required:

a. Calculate before the cost increases the budgeted contribution and profit at the budgeted levels of 100,000 units.

b. Calculate the level of sales at which profits would be maximized and the amounts of these maximum profits before the cost increases.

c. Show whether and by how much Alvis Kiptoo should adjust his selling price in respect to increases in:

- Fuel costs.

- Material costs.

Date posted:

May 3, 2021

.

Answers (1)

-

A critic has suggested that budgets should be abolished because they introduce rigidity and hamper creativity. Discuss.

(Solved)

A critic has suggested that budgets should be abolished because they introduce rigidity and hamper creativity. Discuss.

Date posted:

May 3, 2021

.

Answers (1)

-

In his study of: “the impact of budgets on people” C Argyris reported the following

comment by a financial controller on the practice of participation in...

(Solved)

In his study of: “the impact of budgets on people” C Argyris reported the following

comment by a financial controller on the practice of participation in setting budgets in

his company:

“We bring in the supervisors of budget areas, we tell them that we want their frank

opinion, but most of them just sit there and nod their heads. We know they are not

coming out with exactly what they feel. I guess budget scares them”.

Explain why managers may be reluctant to participate fully in setting budgets, indicating

the negative side effects, which may arise from the imposition of budgets by senior management.

Date posted:

May 3, 2021

.

Answers (1)

-

Watt Lovell Ltd. (WLL) is trying to decide whether or not to drill for oil on a particular site

in North Eastern Kenya. The Chief Engineer...

(Solved)

Watt Lovell Ltd. (WLL) is trying to decide whether or not to drill for oil on a particular site

in North Eastern Kenya. The Chief Engineer has assessed the probabilities that there will be

oil as follow, based on past experience.

Oil 0.2

No oil 0.8

It is possible for WLL to hire a firm of international consultants to carry out a complete

survey of the site. WLL has used the firm many times before and has made the following

estimates:

1. If there really is oil, then there is a 95% chance that the report will be favourable.

2. If there is no oil then there is only a 10% chance that the report will indicate that there is oil.

The following additional information is also provided:

The cost of drilling is Sh.10 million.

The value of the benefits if oil is found is Sh.70 million

The cost of obtaining information is Sh.3 million.

Required:

a) Advise the company on whether to acquire additional information from the consultants

b) Compute the value of imperfect information.

Date posted:

May 3, 2021

.

Answers (1)

-

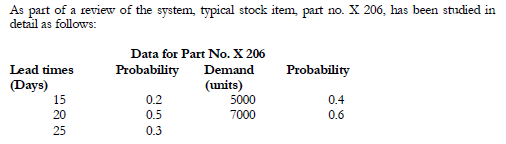

Muthothi Ltd. Operates a conventional stock control system based on re-order levels and

Economic Order Quantities (EOQ). The various control levels were set originally based on

estimates...

(Solved)

Muthothi Ltd. Operates a conventional stock control system based on re-order levels and

Economic Order Quantities (EOQ). The various control levels were set originally based on

estimates which did not allow for any uncertainty and this has caused difficulties because, in

practice, lead times, demands and other factors to vary.

The company works for 360 days per year and it costs Sh.1,000 to place an order. The

holding cost is estimated at Sh.0.025 for storage plus 10% opportunity cost of capital. Each

unit is purchased at Sh.2. The re-order level for this part is currently 150,000 units and it can

be assumed that the demands would apply for the whole of the appropriate lead-time.

Required:

a) Calculate the level of buffer stock implicit in a re-order level of 150,000 units.

b) Calculate the probability of stock-outs.

c) Calculate the expected annual stock-outs in units.

d) Compute the stock-out costs per unit at which it would be worthwhile raising the reorder

level to 175,000 units.

e) Discuss the possible alternatives to a re-order level EOQ inventory system and their

advantages and disadvantages.

Date posted:

May 3, 2021

.

Answers (1)

-

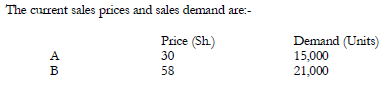

A manufacturer produces and sells two products, A and B. The unit variable cost is sh.12

and sh.8 for A and B respectively. A review of...

(Solved)

A manufacturer produces and sells two products, A and B. The unit variable cost is sh.12

and sh.8 for A and B respectively. A review of selling prices is in progress and it has

been estimated that, for each product and increase in the selling price would result in a

fall in demand of Sh.500 units per every Sh.1 increase in price and similarly a decrease of

Sh.1 in price would result in an increase in demand of 500 units.

Required:

Calculate the profit-maximizing price for reach product.

Date posted:

May 3, 2021

.

Answers (1)

-

The Z division of XYZ Ltd., produces a component which it sells externally, and can also

be transferred to other divisions within the organization. The division...

(Solved)

The Z division of XYZ Ltd., produces a component which it sells externally, and can also

be transferred to other divisions within the organization. The division has set a

performance target for the coming financial year of residual income of Shs. 5,000,000.

The following budgeted information relating to Z division has been prepared for the

coming financial year.

1. Maximum production/sales capacity 800,000 units.

2. Sales to external customers: 500,000 units at Sh.37.

3. Variable cost per component Sh.25.

4. Fixed costs directly attributable to the division Sh.1,400,000.

5. Capital employed: Sh.20,000,000 with cost of capital of 13%

The X division of XYZ Ltd has asked Z division to quote a transfer price for units of the

component.

Required:

i Calculate the transfer price per component which Z division should quote to X

division so that its residual income target is achieved.

ii Explain why the transfer price calculated in (i) above may lead to sub -optimal

decision making from the point of view of XYZ Ltd taken as a whole.

Date posted:

May 3, 2021

.

Answers (1)