-

The Uganda Bank (E.A.) Ltd has only two-branches. The head office branch is in the center

of Kampala and the Kagera branch outside Kampala. The head...

(Solved)

The Uganda Bank (E.A.) Ltd has only two-branches. The head office branch is in the center

of Kampala and the Kagera branch outside Kampala. The head office staff consists of the

managing director and finance manager. With minor exceptions, the branch managers are

permitted to conduct their affairs like the heads of two independent banks. The planning

and control system centers on branch income statements prepared by the Finance Manager.

The Kagera branch, on the other hand, is located outside Kampala in a large and growing

retirement community and as primary retail branch. Mr. Obok, the manager, is in his first

year with the Uganda Bank. In his attempts to sell the bank‟s services to the

Kagera residents, he has found that his only success is the area of foreign deposits. Loan

business, on the other hand, is both competitive and scarce.

The interest rate he can charge is constrained by the fact that the manager of the local

competing branch of the other bank while not actively soliciting loan business is apparently

charging rates below the prevailing Kampala prime rate. Additionally, there seems to be

fundamental resistance in the part of the Kagera residents to the idea of borrowing even at

the 12% rate Obok has been offering.

The Kampala branch located in the growing central business district, serves primarily

commercial customers. The manger, Mr. Kamau, has found in recent years that while he

faces a number of vigorous competitors the principal constraint on his ability to generate

new loan business is lack of supporting deposits. The only alternative source of lending

funds is the purchase of Euro currency, which are foreign deposits held in a bank outside

Africa.

This opinion is considered less than acceptable by Kamau, as the 22% interest he would

have to pay for such funds is higher than the rate he is able to charge loan customers

currently at 20%.

In spite of his frequent lectures on the merits of leverage, the best Obok has been able to do

is to generate a few goll-carat installment and social security cheque receivable loans. As a

result, he finds himself with substantial excess savings deposits, which he has to keep in the

vault to satisfy the government‟s 20% cash reserve requirement, the vault

additionally contains excess lendable funds equal to almost 70% of total savings deposits.

The finance manager has suggested that he lends these funds to Kamau at the Kampala

branch. This was acceptable to both managers, although some disagreement arose as to the

interest rate appropriate for such a loan. The argument was finally settled by the finance

manger, who indicated that the theoretically correct rate was the rate Obok was paying on

savings deposits, 10%. It has been further agreed that if Obok could find additional loans,

any or all of the funds lent to Kamau would be returned.

Required:

a) Evaluate the 10% interbranch loan rate and suggest appropriate changes in relation to

the following criteria:

i Motivating managers to act in a manner consistent with the best interests of the

bank as a whole.

ii Evaluating the performance of individual branches.

b) Would your answer change if the Kagera branch loan rate were to rise to 14%, while all

other rates as well as the level of loan demand at Kampala b ranch, remained the same?

c) Would your answer change if all rates were the same as in (a) above except that he cost

of Euro currency dropped to 18%.

d) Based on your answers to the above, what general statements can you make about the

interbranch loan rate appropriate for evaluation of individual managers?

Date posted:

May 8, 2021

.

Answers (1)

-

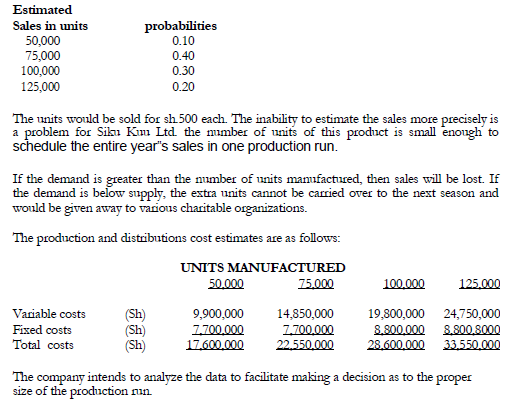

Siku Kuu Ltd. Manufactures and distributes a line of Christmas gifts. The company had

neglected to keep its gifts line current. As a result, sales have...

(Solved)

Siku Kuu Ltd. Manufactures and distributes a line of Christmas gifts. The company had

neglected to keep its gifts line current. As a result, sales have decreased to approximately 25,000

units per year fro a previous high of 125,000 units. The gifts have been redesigned recently and

is considered by company officials to be comparable to its competitors‟ models.

The company plans to redesign the gifts each year in order to compete effectively. Kama

Kawaida, the Sales Manager, is not sure how many units can be sold next year, but she is willing

to place probabilities on her estimates. Kama Kawaida's estimates of the number of

units that can be sold during the next year and the related probabilities are as follows:

Required:

a) Prepare a payoff table for the different sizes of production runs required to meet the four

sales estimates prepared by Kama Kawaida for Siku Kuu Ltd.

If Siku Kuu Ltd. relied solely on the expected monetary value approach to make

decisions, what size of production run would be selected?

b) Identify the seven basic steps that are taken in any decision process. Explain each step by

reference to the situation presented by Siku Kuu Ltd. and your answer to requirement (a)

Date posted:

May 8, 2021

.

Answers (1)

-

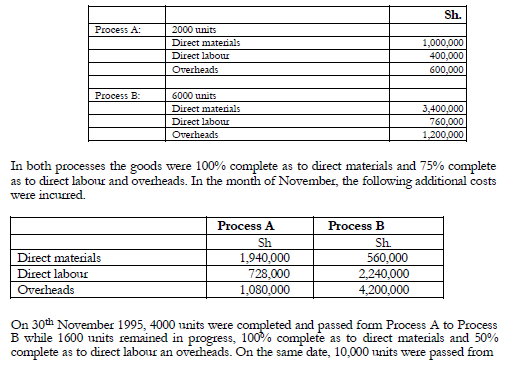

A company makes a lotion that is manufactured through two processes, A and B. on the 1 November 1995, work in process consisted of the...

(Solved)

A company makes a lotion that is manufactured through two processes, A and B. on the 1 November 1995, work in process consisted of the following:

Process B into finished goods while 4000 units remained in progress, 100% complete as to

direct materials and 50% complete as to direct labour and overheads.

All inventories are valued on the weighted average cost basis and transfers from process A

to Process B are treated as part of direct material cost.

Required:

The cost accounts for both processes for the month of November 1995.

Show all supporting computations including the inventory flow through each process.

Date posted:

May 8, 2021

.

Answers (1)

-

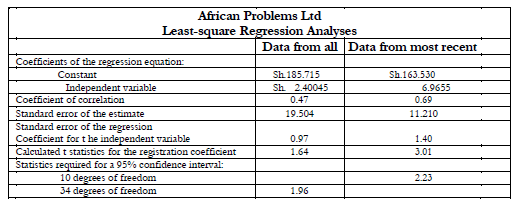

The Finance Director of Africa Problems Ltd. is considering developing a flexible-budget

formula for the manufacturing overhead costs.

The accounting staffs have suggested that simple linear regression...

(Solved)

The Finance Director of Africa Problems Ltd. is considering developing a flexible-budget

formula for the manufacturing overhead costs.

The accounting staffs have suggested that simple linear regression be used to determine the

cost behaviour pattern of the overhead cost. They consider that this method would provide

a good and quick estimate of the costs that can be expected to be incurred each month. The

actual direct-labour hours and corresponding manufacturing overhead costs for each month

between 1996 and 1999 were used in the linear-regression analysis.

The following occurrences during the period are considered unusual:

1. Production was reduced in one month during 1997 due to wildcat strikes related to

political changes in one of the countries.

2. In 1998, production was reduced in one month because of material shortages and

materially increased (overtime scheduled) during two-months to meet the units

required for one-time sales order.

3. Employee benefits were raised significantly in December 1998 as a result of a labour

agreement.

4. Production during 1999 was not affected by any special circumstances.

The accounting staff raised the following issues:

Some members question whether historical data should be used at all to form the basis

for a flexible-budget formula.

Some members believe that he use of data from all 48 months would provide a more

accurate portrayal of the cost behaviour. While they recognized that any of the monthly

data could include efficiencies, they believed these would tend to balance out over a

long period of time.

Still other members felt that only the most recent 12 months should be used because

they were the most current.

Other members of the accounting staff suggested that only those months that were

considered normal should be used so that the regression would not be distorted.

The accounting department ran two regression analyses of the data, one using the data from

all 48 months and the other using only the data from the last 12 months.

The results were as follows:

a)

i Formulate the flexible-budget equation that can be employed to estimate monthly

manufacturing-overhead costs.

ii Calculate the estimate of overhead costs for a month when 37.500 direct labour

hours are worked.

b) Using only the results of the two regression analysis above, explain which of the two

results is more appropriate as a basis for the flexible-budget formula.

c) Evaluate and explain how each of the four issues raised by the accounting department

staff influence our willingness to use the results of the statistical analyses as the basis for

the flexible-budget formula.

Date posted:

May 8, 2021

.

Answers (1)

-

Samaki Ltd., a company based in Mombasa, exports vital fishing hooks to Madagascar.

The demand for the hooks is constant and Samaki Ltd., is able to...

(Solved)

Samaki Ltd., a company based in Mombasa, exports vital fishing hooks to Madagascar.

The demand for the hooks is constant and Samaki Ltd., is able to predict the annual

demand with considerable accuracy. The predicted demand for the next couple of year is

200,000 hooks per year.

Samaki Ltd. purchases its hooks from a manufacturer in Mombasa at a price of Sh.400

per hook. In order to transport the purchases from Mombasa to Madagascar, Samaki Ltd.

must charter a ship. The charter services usually charge Sh.20,000 per trip plus Sh.40 per

hook (this includes the cost of loading the ship). The ships have a capacity of 10,000

hooks. The placing of each order including arranging for the ship requires 5 h ours of

employee time. It takes about a week for an order to arrive at the Samaki Ltd. warehouse

in Madagascar. The warehouse has a capacity of 15,000 hooks.

When a ship arrives at the Samaki warehouse, the hooks can be unloaded at a rate of 25

hooks per hour per employee. The unloading equipment used by each employee is rented

from a local supplier at a rate equivalent to Sh.100 per hour. Supervisory time for each

shipload is about 4 hours. The employees working in the warehouse have several tasks:

i Placing the hooks into storage, after they are unloaded which can be done at the

rate of about 40 per hour.

ii Checking, cleaning etc. of the hooks in inventory requires about one-half hour

per hook per year.

iii Removing a hook from inventory and preparing it for shipments to a customer

requires about one-eighth of an hour.

iv Security guards general maintenance, etc. require about 10,000 hours per year.

The average cost per hour of labour is equivalent to Sh.200 (including fringe benefits).

Samaki Ltd. has developed the following prediction equation for its general overhead

(excluding shipping materials, fringe benefits, and equipment rental):

Predicted overhead for the year = Sh.20,000,000 + (Sh.160 x Total labour hours)

The materials used to ship one hook to a customer costs Sh.20 and the delivery costs

average out to about Sh.40 per hook.

The company requires a before-tax rate of return of 20 per cent on its investment.

The ordering policy from the manufacturers by Samaki Ltd., is based on an EOQ. Model,

which is determined by the demand for hooks in Madagascar.

Required

a) Determine the quantity that should be ordered each time and the re-order level

b) If the true overhead prediction equation is:

Sh.16,000,000 + (Sh.240 x Total labour hours), what is the cost of the prediction error?

Date posted:

May 8, 2021

.

Answers (1)

-

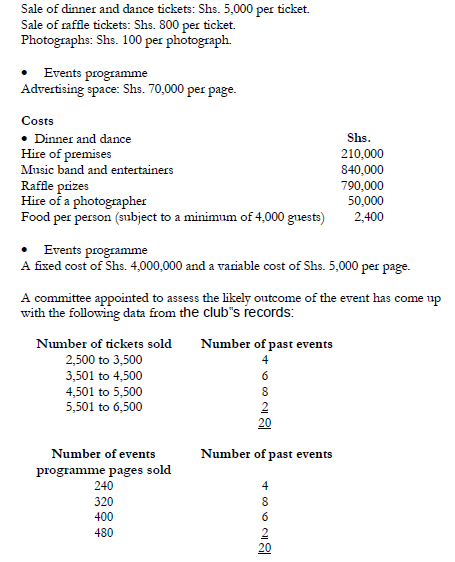

Mwito Club is a charitable organization based in Nairobi. For the last 20 years, the

club has held an annual dinner and dance event with the...

(Solved)

Mwito Club is a charitable organization based in Nairobi. For the last 20 years, the

club has held an annual dinner and dance event with the primary aim of raising

funds to help the less fortune members of the society.

This year, there is concern that an economic recession may adversely affect the

success of the event with a fall in the number of guests attending and sale of

advertising space in the published events programme.

A study of past experience, current prices and quotations shows that the following

costs and revenues will apply for the event:

Revenue

Dinner and dance

Required:

(i) The expected profit from the event. (Assume one raffle ticket and one

photograph per attendant).

(ii) Describe how cost-volume-profit (C-V-P) analysis can be applied in

absorption costing.

Date posted:

May 7, 2021

.

Answers (1)

-

Angels of Mercy Mission Hospital operates on charity basis. The hospital?s board

of directors has recently complained about the increasing size of the cost budget insisting...

(Solved)

Angels of Mercy Mission Hospital operates on charity basis. The hospital‟s board

of directors has recently complained about the increasing size of the cost budget insisting that

the management should cut down on costs.

The major concern of the board is the cost of maintaining patients at the intensive care unit

(ICU).

The following information is available on the operations of the hospital:

1. The average cost of maintaining a patient at the ICU per week is Shs. 200,000 compared

to Shs. 100,000 per week incurred in maintaining a patient at the high dependency unit

(HDU) and Shs. 50,000 per week of maintaining a patient at the general ward (GW).

2. Past information on patients indicates that:

(i) 50% of the patients in ICU at the beginning of the week will remain in ICU

at the end of the week and 50% will be transferred to HDU by the end of the

week.

(ii) 10% of the patients in HDU at the beginning of the week will be transferred

to ICU, 50% will remain in HDU, and 40% will be transferred to GW.

(iii) 85% of the patients in the GW at the beginning of the week will remain in

GW at the end of the week, 10% will be transferred to HDU and 5% to ICU.

3. The board of directors believe that the criteria for maintaining patients in the ICU is too

strict and should be relaxed so that only 40% of the patients in ICU at the beginning of

the week remain there at the end of the week while 60% are transferred to HDU.

4. The staff at the hospital insist that if the proposed criterion is adopted:

(i) 20% of patients in HDU at the beginning of the week will be transferred to

ICU, 50% will remain in HDU while only 30% will be transferred to GW.

(ii) No changes will be expected in the GW.

5. Past hospital records indicate that the hospital serves an average of 4,000 patients

weekly.

Required:

(a) The steady state weekly costs under the current policy.

(b) The steady state weekly costs under the proposed policy.

(c) Advise the board on the best policy.

(d) State the assumptions of the quantitative technique used in solving problems (a) and

(b) above.

Date posted:

May 7, 2021

.

Answers (1)

-

Pwani Marine Ltd., a boat construction company, has developed a new type

of speed boat called “Speed Surf.”

The following information has been availed to you:

1. Boat...

(Solved)

Pwani Marine Ltd., a boat construction company, has developed a new type

of speed boat called “Speed Surf.”

The following information has been availed to you:

1. Boat construction is a continuous assembling process carried out at

the company‟s yard.

2. Boat assembling is labour intensive involving the use of two classes of

labour namely:

Skilled labour at a standard rate of Shs. 1,250 per hour.

Semi-skilled labour at a standard rate of Shs. 950 per hour.

3. Experience on boat construction from other models indicates that the use of

skilled labour is associated with an 80% learning curve effect whereas use of

semi-skilled labour is associated with a 90% learning curve effect.

4. Labour usage for the first speed boat assembled was as follows:

Skilled labour – 952 hours.

Semi-skilled labour – 650 hours.

5. In October 2005, the sixth and the seventh speed boats were assembled

from start to finish. During the month, the following labour usage and costs

were recorded:

Skilled labour – 680 hours at a total cost of Shs. 800,400.

Semi-skilled labour – 1,256 hours at a total cost of Shs. 1,281,200.

The management of Pwani Marine Ltd. is concerned about the cost variances and

would like to learn more on the composition of the variances.

Required:

(i) Calculate the standard labour cost of the month of October 2005.

(ii) Reconcile the standard cost with the actual cost for the month of October

2005 showing the labour rate and labour efficiency variances.

(iii) Express the labour efficiency variance in terms of labour mix and labour

output variances. (Value the labour mix variances using standard rates).

Date posted:

May 7, 2021

.

Answers (1)

-

Explain the applications of the learning curve.

(Solved)

Explain the applications of the learning curve.

Date posted:

May 7, 2021

.

Answers (1)

-

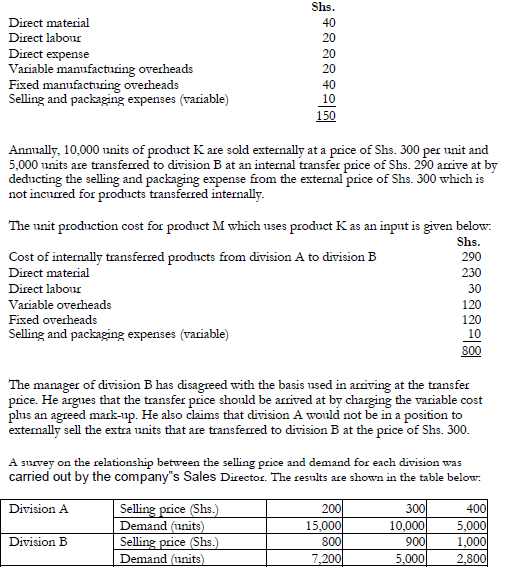

Kutwa Ltd. is a manufacturing company with two divisions; A and B. Division A

manufactures a single standard product K, some of which is sold externally...

(Solved)

Kutwa Ltd. is a manufacturing company with two divisions; A and B. Division A

manufactures a single standard product K, some of which is sold externally and the

remainder used as an input in division B in the manufacture of product M.

The unit production costs of product K are given below:

The manager of division B suggests that based on the above results, a transfer price of Shs.

120 would offer division A a reasonable contribution towards its fixed cost and earn

division B a reasonable profit. This would lead to an increase in the output and overall

profitability of the company.

Required:

( a) Calculate the effect of the existing transfer pricing system on the company‟s profits.

( b) Calculate the effect of adopting the transfer price of Shs. 120 on the company‟s

profits.

Date posted:

May 7, 2021

.

Answers (1)

-

Nairobi Manufacturers Ltd. produces component X on machine Y at a rate of 4,000

units per month. Machine Z uses component X at the rate of...

(Solved)

Nairobi Manufacturers Ltd. produces component X on machine Y at a rate of 4,000

units per month. Machine Z uses component X at the rate of 1,000 units per month,

the remainder being put into stock. It costs Shs. 2,000 to set up machine Y while the

stock holding cost is estimated at Shs. 2.50 per unit per annum plus a 20% opportunity

cost of capital per annum. Each component costs Shs. 25 to produce.

Required:

(i) Compute the optimal batch size that should be produced using machine Y.

(ii) Assume that the actual set-up cost of machine Y is Shs. 1,000 instead of

Shs. 2,000. Calculate the cost of prediction error.

Date posted:

May 7, 2021

.

Answers (1)

-

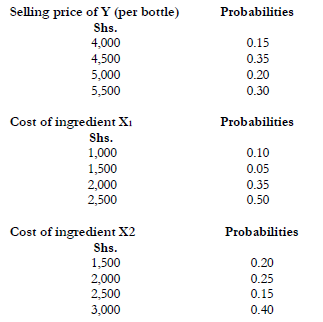

Manukato Ltd. produces a designer perfume called “Hint of Elegance.”

Production of the perfume involves the use of two ingredients, X1 and X2

represented by the production...

(Solved)

Manukato Ltd. produces a designer perfume called “Hint of Elegance.”

Production of the perfume involves the use of two ingredients, X1 and X2

represented by the production function given below:

Required:

(i) Calculate the daily expected profit of the company.

(ii) Simulate the company‟s profit for 10 days using the following

random numbers:

58, 71, 96, 30, 24, 18, 46, 23, 34, 27, 85, 13, 99, 24, 44, 49,

18, 09, 79, 49, 74, 16, 32, 23, 02, 56, 88, 87, 59, 41, 06

Date posted:

May 7, 2021

.

Answers (1)

-

Shadow prices may be used in the setting of transfer prices between divisions in a

company, where the intermediate products being transferred are in short supply.

Required:

Explain...

(Solved)

Shadow prices may be used in the setting of transfer prices between divisions in a

company, where the intermediate products being transferred are in short supply.

Required:

Explain why the transfer prices thus calculated are more likely to be favoured by the

management of the divisions supplying the intermediate products rather than the

management of the divisions receiving the intermediate products.

Date posted:

May 7, 2021

.

Answers (1)

-

Transfer pricing of products between processes in a manufacturing company can be done at:

1. Cost or

2. Sales value at the point of transfer.

Required:

Discuss how each...

(Solved)

Transfer pricing of products between processes in a manufacturing company can be done at:

1. Cost or

2. Sales value at the point of transfer.

Required:

Discuss how each of the above methods could be used effectively in the operations

of a responsibility accounting system.

Date posted:

May 7, 2021

.

Answers (1)

-

State four objectives of a transfer pricing system.

(Solved)

State four objectives of a transfer pricing system.

Date posted:

May 7, 2021

.

Answers (1)

-

State the limitations of the use of fame theory in decision making.

(Solved)

State the limitations of the use of fame theory in decision making.

Date posted:

May 7, 2021

.

Answers (1)

-

Topcom Kenya International Limited (TKIL) is a telecommunications company

situated in Nakuru. Recently, the company was faced with a workers strike which

necessitated a renegotiation of the...

(Solved)

Topcom Kenya International Limited (TKIL) is a telecommunications company

situated in Nakuru. Recently, the company was faced with a workers strike which

necessitated a renegotiation of the workers‟ salaries through their union.

The management with the help of a consultant, has prepared the pay-off matrix

shown below:

A positive sign represents a wage increase while a negative sign represents a wage decrease.

Required:

(i) Advise the management on the best strategies.

(ii) The value of the game

Date posted:

May 7, 2021

.

Answers (1)

-

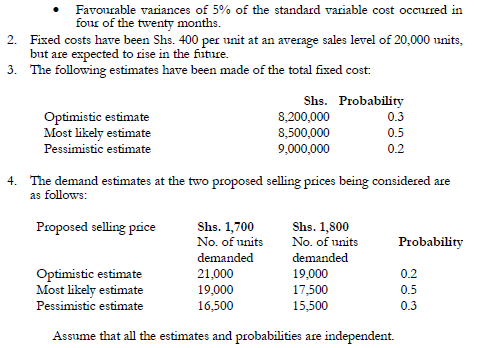

Makazi Ltd. manufactures a hedge-trimming tool which has been selling at Shs.

1,600 per unit for a number of years. The selling price is to be...

(Solved)

Makazi Ltd. manufactures a hedge-trimming tool which has been selling at Shs.

1,600 per unit for a number of years. The selling price is to be reviewed and the

following information is available on costs and the likely demand:

1. The standard variable cost of manufacturing the tool is Shs. 1,000 per unit and

an analysis of the cost variances in the past 20 months shows the following

pattern which the production manager expects to continue in the future.

Adverse variances of 10% of the standard variables cost occurred in ten

of the twenty months.

Nil variances occurred in six of the twenty months.

Required:

(i) Based on the information given above, advise the management of Makazi Ltd.

on whether they should change the selling price. Indicate the price you would

recommend.

(ii) The expected profit at the price you have recommended in (i) above and the

resulting margin of safety expressed as a percentage of expected sales

(iii) Comment on the method of analysis you have used to deal with the

probabilities given in the question.

(iv) Explain briefly how the use of a computer program would improve your

analysis.

Date posted:

May 7, 2021

.

Answers (1)

-

Equi -solutions Ltd. was formed ten years ago to provide business equipment solutions tolocal business. It has separate divisions for research, marketing, product design, technologyand...

(Solved)

Equi -solutions Ltd. was formed ten years ago to provide business equipment solutions to

local business. It has separate divisions for research, marketing, product design, technology

and communication services, and now manufactures and supplies a wide range of business

equipment. To date the company has evaluated its performance using monthly financial

reports that analyze profitability by type of equipment. The managing director of Equi solutions

Ltd. has recently returned from a course in which it has been suggested that the

“Balanced Scorecard” could be a useful way of measuring performance.

Required:

a) Explain the “Balanced Scorecard” and how it could be used by Equi-solutions Ltd. to

measure its performance.

b) The managing director of Equi-solutions Ltd. also overheard someone mention how the

performance of their company had improved after they introduced “Bench marking.”

Required:

Explain “Bench-marking” and how it could be used to improve the performance of

Equi -solutions Ltd.

Date posted:

May 7, 2021

.

Answers (1)

-

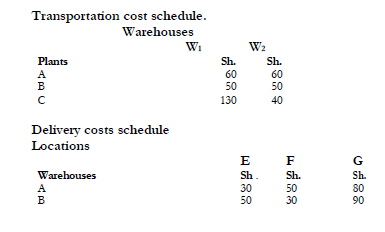

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may...

(Solved)

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may be distributed through any combination of the two

company warehouses W1 and W2.

2. The available monthly production capabilities for the new products are:

1000 units at plant A

2000 units at plant B

1000 units at plant C

3. Three major concentration points of customer demand are at locations E, F

and G which are estimated to have a monthly demand of:

900 units at E

800 units at F

900 units at G

4. The unit production costs amount to Sh.30, Sh.40, Sh.10 at A, B and C

respectively.

5. The unit handling costs at the warehouses amount to Sh.20 and Sh.30 at W1

and W2.

6. The unit transportation costs from plant to warehouse and unit delivery cost

from warehouse to customers are as shown below:

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Date posted:

May 7, 2021

.

Answers (1)