-

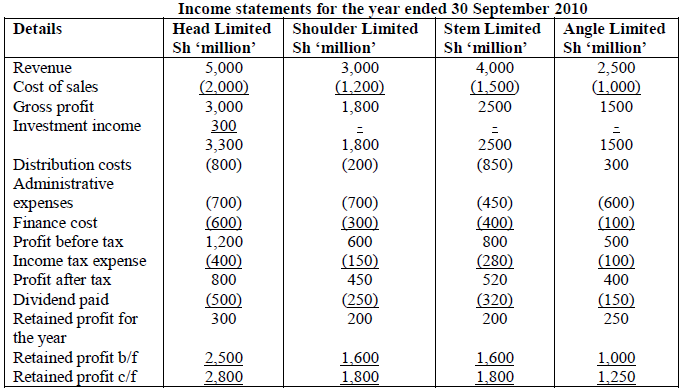

Head Limited sold off its entire shareholding of 80% in Shoulder Limited and acquired 75% of the shares of Stem Limited during the year ended...

(Solved)

Head Limited sold off its entire shareholding of 80% in Shoulder Limited and acquired 75% of the shares of Stem Limited during the year ended 30 September 2010. Head Limited also acquired 40% of the shares of Angle Limited.

The following income statements relate to the four companies:

Additional information:

1. Head Limited had acquired it s shareholding in Shoulder Limited at a cost of Sh 2200 million on 1 October 2007 when the retained earnings of Shoulder Limited were Sh.500 million. The ordinary share capital of Shoulder Limited was Sh. 2,000 million and there were no other reserves. The fair value of the non-controlling interest in Shoulder Limited on the same date was Sh.550 million.

2. During the year ended 30 September 2010, Head Limited acquired the investment in Stem Limited and Angle Limited. The details of the acquisitions are as follows:

On the date of its acquisition, Stem Limited had an item of plant that was Sh.270 million below its fair value. Plant is depreciated at 20% per annum with a full year’s charge in the year of purchase or revaluation.

3. On 1 July 2010, Head Limited sold its investment in Shoulder Limited at a price of Sh.3,430 million. This disposal has not been reflected in the income statement of Head Limited.

4. During the year, the companies traded as follows:

5. Goodwill of Shoulder Limited had been impaired by half as at 1 October 2009. Any goodwill arising in Stem Limited and Angle Limited is impaired by 20%.

6. All dividends were paid on 31 August 2010.

Required:

a) The group income statement for the year ended 30 September 2010.

b) The statement of changes in equity showing only the retained profits column.

Date posted:

December 10, 2021

.

Answers (1)

-

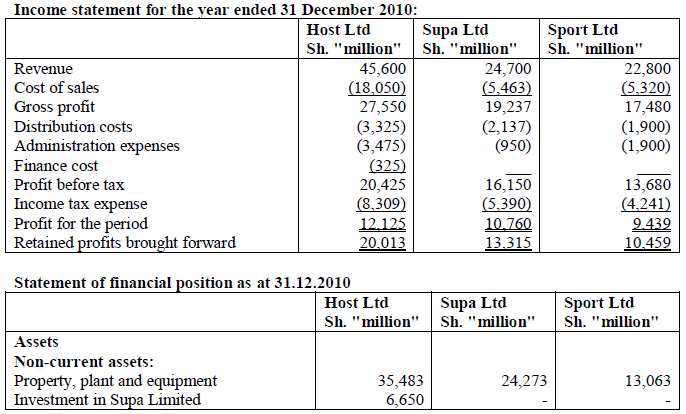

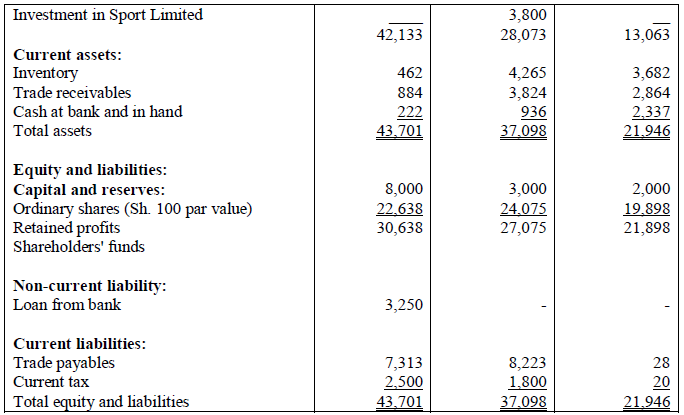

Host Limited, its subsidiary Supa Limited and sub-subsidiary Sport Limited operate in the media industry.

The following financial statements relate to the three companies for the...

(Solved)

Host Limited, its subsidiary Supa Limited and sub-subsidiary Sport Limited operate in the media industry.

The following financial statements relate to the three companies for the year ended 31 December 2010:

Additional information:

1. Host Limited acquired 90% of the ordinary share capital of Supa Limited on 1 January 2005 when the retained profit, of Supa Limited were Sh. 1,425 million. Subsequently, Supa Limited acquired 80% of the ordinary share capital of Sport Limited on 1 January 2007 when the retained profits of Sport Limited were Sh.950 million.

2. During the year 2010, Sport Limited sold goods to Supa Limited at a selling price of Sh.480 million making a profit of 25% on cost. Sh.75 million -worth of these goods were still in the inventory of Supa Limited at the end of the year Supa Limited still owed Sport Limited Sh. 100 million as at 31 December 2010.

3. During the year 2010, Supa Limited sold goods to Host Limited at a selling price of Sh.260 million making a profit of /) on cost. Sh.60 million worth of these goods were still in the inventory of Host Limited as at the end of the year. Host Limited still owed Supa Limited Sh.50 million as at 31 December 2010.

4. During the year, Host Limited sold an item of plant to Supa Limited at a selling price of Sh.240 million reporting a profit of 20% on cost. The group charges depreciation at the rate of 20% on cost and this is included as part of the cost of sales.

5. The entire goodwill of Supa Limited has been impaired and by 31 December 2009, 60% of the goodwill of Sport Limited was impaired. An additional half of the balance of goodwill in Sport Limited is considered impaired. The group uses the partial goodwill method.

Required:

a) Consolidated income statement for the year ended 31 December 2010.

b) Consolidated statement of changes in equity (retained profits only) as at 31 December 2010.

c) Consolidated statement of financial position as at 31 December 2010.

Date posted:

December 10, 2021

.

Answers (1)

-

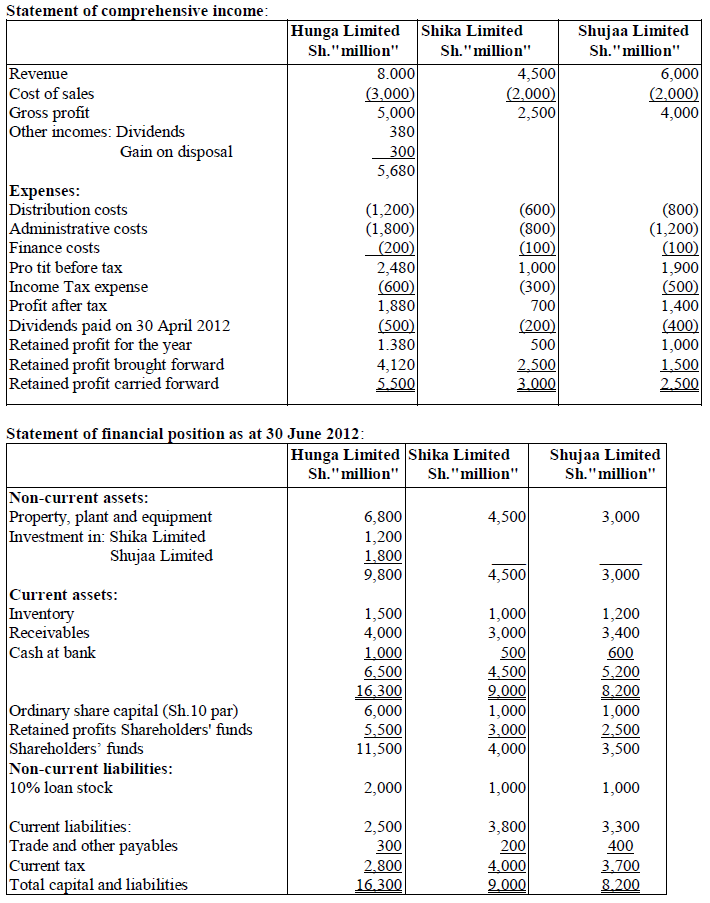

Hunga Limited, a company quoted on the securities exchange, acquired 80% of Shika Limited several years ago. On 1 January 2012 Hunga limited sold half...

(Solved)

Hunga Limited, a company quoted on the securities exchange, acquired 80% of Shika Limited several years ago. On 1 January 2012 Hunga limited sold half of its investment in Shika Limited and acquired 75% of the equity shares of Shujaa Limited.

The financial statements for the year ended 30 June 2012 for the three companies are as given below.

Additional information:

1. Hunga Limited had acquired its shareholding in Shika Limited for Sh.2,400 million when the retained profits of Shika Limited amounted to Sh. 1,500 million. There was no fair value adjustment at the time of this acquisition.

2. Hunga Limited sold half of the investment in Shika Limited for Sh.1.500 million. This disposal has already been accounted for by Hunga Limited but not by the group. The fair value of the remaining investment in Shika Limited was Sh.1, 300 million on the date of disposal.

3. Between 1 January 2012 and 30 June 2012. Hunga Limited sold to Shujaa Limited goods worth Sh.500 million reporting, a profit of Sh. 100 million. Half of the goods were still in the inventory of Shujaa Limited as at 30 June 2012.

4. Intercompany receivables and payables were as follows as at 30 June 2012:

5. As at 1 July 2011, half of the goodwill of Shika Limited had been impaired. The goodwills of the companies were not impaired in the current year to 30 June 2012. The group uses the partial goodwill method when preparing the consolidated financial statements.

Required;-

a) Group statement of comprehensive income for the year ended 30 June 2012.

b) Group statement of financial position as at 30 June 2012.

Date posted:

December 10, 2021

.

Answers (1)

-

Describe four shortcomings of cost accounting.

(Solved)

Describe four shortcomings of cost accounting.

Date posted:

February 15, 2019

.

Answers (1)

-

Explain what 'integrated reporting' entails.

(Solved)

Explain what 'integrated reporting' entails.

Date posted:

February 15, 2019

.

Answers (1)

-

In the context of integrated reporting:

i. Discuss any two components of an integrated report.

ii. Explain four guiding principles that underpin the preparation of an integrated...

(Solved)

In the context of integrated reporting:

i. Discuss any two components of an integrated report.

ii. Explain four guiding principles that underpin the preparation of an integrated report.

Date posted:

February 15, 2019

.

Answers (1)

-

Explain the benefits that would accrue from the adoption of international public sector accounting standards (IPSASs) by governments and public entities.

(Solved)

Explain the benefits that would accrue from the adoption of international public sector accounting standards (IPSASs) by governments and public entities.

Date posted:

February 15, 2019

.

Answers (1)

-

The following information has been compiled by the Ministry of Finance for the fiscal year ended 30 June 2009:

(Solved)

The following information has been compiled by the Ministry of Finance for the fiscal year ended 30 June 2009:

Date posted:

February 15, 2019

.

Answers (1)

-

The International Public Sector Accounting Standards (IPSASs) are developed by the International Public Sector Accounting Standards Board (IPSASB) to enhance uniformity in the way...

(Solved)

The International Public Sector Accounting Standards (IPSASs) are developed by the International Public Sector Accounting Standards Board (IPSASB) to enhance uniformity in the way public sector organizations prepare their financial statements. The Board (IPSASB) is promoting the international adoption and application of these standards.

Required:

Highlight four challenges that the Board is facing in promoting the use of IPSASs.

Date posted:

February 15, 2019

.

Answers (1)

-

The following data has been collected from the Ministry of Trade and Commerce for the fiscal year ended 30 June 2010:

(Solved)

The following data has been collected from the Ministry of Trade and Commerce for the fiscal year ended 30 June 2010:

Required:

The following statements in accordance with IPSAS 1 (Presentation of Financial Statements):

i) Statement of financial performance for the year ended 30 June 2010.

ii) Statement of financial position as at 30 June 2010.

Date posted:

February 15, 2019

.

Answers (1)

-

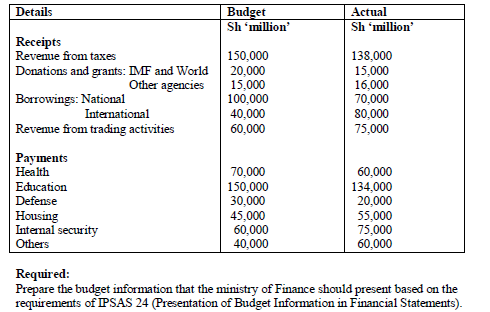

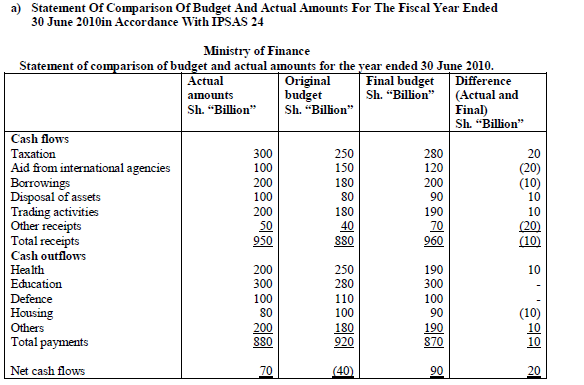

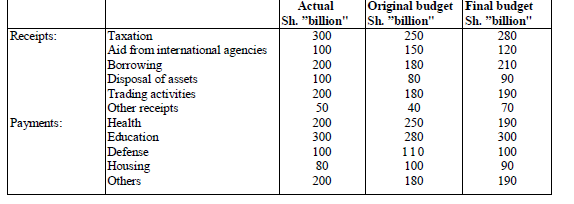

The following summary of receipts and payments was extracted from the records of the Ministry of Finance for the fiscal year ended 30 June 2010.

(Solved)

The following summary of receipts and payments was extracted from the records of the Ministry of Finance for the fiscal year ended 30 June 2010.

Required:

The statement of comparison of budget and actual amounts for the fiscal year ended 30 June 2010 in accordance with International Public Sector Accounting Standard (IPSAS) 24 (Presentation of Budget Information in Financial Statements

Date posted:

February 15, 2019

.

Answers (1)

-

i. A certain government agency has a widely published environmental policy in which it undertakes to clean up all contamination arising from its operations. The...

(Solved)

i. A certain government agency has a widely published environmental policy in which it undertakes to clean up all contamination arising from its operations. The government agency has a record of honoring agency operates. During the course of a naval exercise, a vessel was damaged and a substantial amount of oil leaked. The government agency agreed to pay for the costs of the immediate clean-up and the costs of monitoring and assisting marine animals and birds.

Required:

In the context of International Public Sector Accounting Standard Number 19 (Provisions, Contingent Liabilities, and Contingent Assets}, evaluate how the costs in the above, scenario would be accounted for.

ii. Mashinani City Council constructed a 20 storey office building for use by the council at a cost of Sh.800 million. This building came into use on 1 January 1996 and it was expected to have a useful life of 40 years. During the year 2010, National Safety Regulations required that owing to security concerns, the top 4 storeys of high-rise buildings should be left unoccupied for the foreseeable future. These regulations were to come into force on 31 December 2010. As at 31 December 2010, the building had a fair value less costs to sell of Sh.450 million. As at the same date, the replacement cost of a similar 20 storey building was Sh.850 million.

Required:

Using the service units approach, evaluate whether there is any impairment loss as at 31 December 2010 in accordance with the requirements of International Public Sector Accounting Standard Number 21 (Impairment of Non-Cash-Generating Assets).

Date posted:

February 15, 2019

.

Answers (1)

-

In relation to-International Public Sector Accounting Standards (IPSASs).

i) Explain any three benefits that would accrue to a government as a result of the adoption of...

(Solved)

In relation to-International Public Sector Accounting Standards (IPSASs).

i) Explain any three benefits that would accrue to a government as a result of the adoption of IPSASs.

ii) Analyze, any two limitations that, state (or. county) governments in your country are likely to face in implementing IPSASs.

Date posted:

February 15, 2019

.

Answers (1)

-

In the context of IPSAS 19 (Provisions, Contingent Liabilities and Contingent Assets), explain the meaning of the term 'constructive obligation'.

(Solved)

In the context of IPSAS 19 (Provisions, Contingent Liabilities and Contingent Assets), explain the meaning of the term 'constructive obligation'.

Date posted:

February 15, 2019

.

Answers (1)

-

With reference to IPSAS 9 (Revenue from Exchange Transactions):

(i) Evaluate the objectives of the standard.

(ii) Analyse the difference between 'exchange transactions' and 'non-exchange transactions'.

(Solved)

With reference to IPSAS 9 (Revenue from Exchange Transactions):

(i) Evaluate the objectives of the standard.

(ii) Analyse the difference between 'exchange transactions' and 'non-exchange transactions'.

Date posted:

February 15, 2019

.

Answers (1)

-

In the context of IPSAS 23 (Revenue from Non-exchange Transactions), summarize five sources of revenue from non-exchange transactions recognized by this standard.

(Solved)

In the context of IPSAS 23 (Revenue from Non-exchange Transactions), summarize five sources of revenue from non-exchange transactions recognized by this standard.

Date posted:

February 15, 2019

.

Answers (1)

-

On 1 January 2008, Mashambani County Education Department purchased a printing machine at a cost of Sh.40 million. The department estimated that the useful life...

(Solved)

On 1 January 2008, Mashambani County Education Department purchased a printing machine at a cost of Sh.40 million. The department estimated that the useful life of the machine would be ten years. On 31 December 2012, it was reported that an automated feature on the machine's function did not operate as expected, resulting in a 25% reduction in the machine's annual output over the remaining five years of its useful life. The cost of a new printing machine was Sh.45 million as at 3 1 December 2012.

Required:

The impairment loss as at 31 December 2012 using the service units approach

Date posted:

February 15, 2019

.

Answers (1)

-

With reference to IPSAS 26 (Impairment of Cash Generating Assets), explain the meaning of the following terms

i) Value in use.

ii) Recoverable amount.

(Solved)

With reference to IPSAS 26 (Impairment of Cash Generating Assets), explain the meaning of the following terms

i) Value in use.

ii) Recoverable amount.

Date posted:

February 15, 2019

.

Answers (1)

-

In 1993, the Nairobi County Government constructed a public primary school at a cost of Sh.25 million. It was estimated that the school would be...

(Solved)

In 1993, the Nairobi County Government constructed a public primary school at a cost of Sh.25 million. It was estimated that the school would be used for 40 years. By the end of 2013, the school population had declined from 1,500 students to 400 students as a result of a population shift caused by the bankruptcy of a major employer in the area. The management decided to close the two top floors of the three storey school building. The management has no expectation that enrollment will increase in future such that the upper storeys would be reopened. The current replacement cost of the school is estimated at Sh.13 million.Required:

Calculate the impairment loss to be recognized using the depreciated replacement cost approach.

(b) International Public Sector Accounting Standard (IPSAS) 22 (Disclosure of Financial Information about the General Government Sector (GGS)), defines a general government sector as "comprising all organizational entities of the general government as defined in statistical bases of financial reporting".

With regard to this standard, outline eight items that should be disclosed in respect of a GGS.

(c) IPSAS 20 (Related Party Disclosures) defines a related party as 'any party that has the ability to control the other party or exercise significant influence over the other party in making financial and operating decisions or if the related party entity and another entity are subject to common control'.

With respect to the above statement:

i) Explain the meaning of 'significant influence'.

ii) Outline four ways in which significant influence might be exercised.

Date posted:

February 15, 2019

.

Answers (1)

-

With reference to IPSAS 9 (Revenue from Exchange Transactions), summarize five conditions that must be satisfied before revenue from the sale of goods can be...

(Solved)

With reference to IPSAS 9 (Revenue from Exchange Transactions), summarize five conditions that must be satisfied before revenue from the sale of goods can be recognized.

Date posted:

February 15, 2019

.

Answers (1)