- Explain three roles of International Accounting Standards Board (IASB). (Solved)

Explain three roles of International Accounting Standards Board (IASB).

Date posted: October 3, 2022. Answers (1)

- Alloys Ltd. is a small enterprise with a turnover of sh.10million. The firm sells tyres and related products to various customers both on credit and...(Solved)

Alloys Ltd. is a small enterprise with a turnover of sh.10million. The firm sells tyres and related products to various customers both on credit and cash terms. Currently, the firms accounting systems are manual. The management of Alloys Ltd. is considering computerizing its accounting systems

Required:

(i) Advise Alloys Ltd. of six essential accounting information systems that could be implemented in the

computerized project.

(ii) Explain the benefits that would accrue to Alloys ltd. as a result of computerizing its accounting system.

(iii) Highlight the challenges Alloys Ltd. is likely to face in the computerization project

Date posted: October 3, 2022. Answers (1)

- The approved estimates and actual expenditure of the Ministry of Youth and Sports for the financial year ended 30 June 2009 were as follows;

Item ...(Solved)

The approved estimates and actual expenditure of the Ministry of Youth and Sports for the financial year ended 30 June 2009 were as follows;

Item Details Estimates Actual

Sh. Sh

2110100 Basic salaries 61,000,000 59,500,000

2110300 Other personal allowances 23,200,000 21,900,000

2210100 Utilities, supplies and services 73,100,000 66,450,000

2210300 Domestic travel and Subsistence 5,000,000 4,950,000

2210500 Printing and Stationary 4,500,000 4,050,000

2210700 Training expenses 6,400,000 6,390,000

2220200 Maintenance of Equipment 1,000,000 900,000

2230100 Grants to youth clubs 5,000,000 5,000,000

Gross expenditure 179,200,000 169,140,000

Appropriation-In-Aid

Receipts not classified

1450100 elsewhere 12,000,000 10,500,000

Net expenditure 167,200,000 158,640,000

Drawings from the exchequer during the financial year ended 30 June 2009 amounted to sh. 160,000,000

Required:

(a) Exchequer account

(b) General account of vote

(c) Paymaster general (PMG) account

(d) Appropriation account for the year ended 30 June 2009

(e) Statement of assets and liabilities as at 30 June 2009

Date posted: October 3, 2022. Answers (1)

- The following is the receipts and payments account of “The Professional club” for the year ended 30 September 2009:

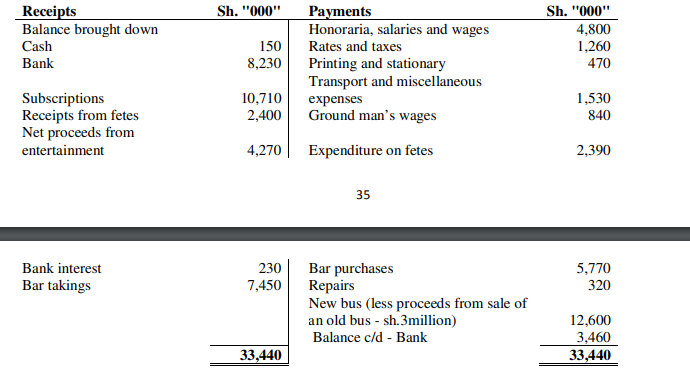

Additional information

1. The professional club premises...(Solved)

The following is the receipts and payments account of “The Professional club” for the year ended 30 September 2009:

Additional information

1. The professional club premises was acquired for sh.29,000,000. The provision for depreciation on the

premises as at 30 September 2008 amounted to sh.18,800,000. The old bus disposed of during the year cost

sh.12,190,000 and the accumulated depreciation as at 30 September 2008 was sh.10,290,000

2. Depreciation is to be provided as follows

Asset rate per annum

Club premises 5% on reducing balance basis

Bus 15% based on cost

3. The following balances as at 30 September 2008 and 2009 have been provided by the club

2008 2009

Sh. "000" Sh. "000"

Subscriptions due 1200 980

Accruals on printing 90 30

Bar inventory 710 870

Accruals on bar purchases 590 430

Required:

(a) Income statement for the year ended 30 September 2009

(b) Statement of financial position as at 30 September 2009

Date posted: October 3, 2022. Answers (1)

- The following information relates to Pambazuka ltd. for the month of August 2009:

...(Solved)

The following information relates to Pambazuka ltd. for the month of August 2009:

Sh.

Credit sales 3,800,000

Discount received 75,600

Return outwards 90,100

Interest charged to credit customers 200,500

Discount allowed 100,900

Receipts from credit customers 3,306,400

Payments to credit suppliers 3,800,000

Bad debts written off 80,700

Customers' cheques dishonoured (including

cheque over the counter by customers - sh.

380,000 965,000

Credit Purchases 3,950,000

Allowance for doubtful debts (established at the

end of the month) 640,000

Trade payables ledger (credits transferred to trade

receivables ledger 214,600

Trade receivables balances as at 1 August 2009 2,100,000

Trade payables balances as at 1 August 2009 800,000

Additional information

1. Estimated price adjustments and other allowances on outstanding trade receivables amounted to sh.180,000

2. Claims by Pambazuka Ltd. for price reductions on defective goods as agreed with suppliers was sh. 107,800 while the return inwards was sh.120,000

3. Ninety (90) percent of customers with outstanding accounts on 31 August 2009 took discounts in the first week of September 2009. The company offers a cash discount of 2% on sales

4. Amounts totaling sh.28,600 written off in the month of June 2009 were collected in the month of August 2009 and credited to suspense account

5. On 31 August 2009 customers’ accounts with credit balances amounted to sh.450,000 and suppliers’

accounts with debit balances amounted to sh.213,400

6. One invoice of sh.75,000 was posted to the trade receivables ledger as sh.57,000

7. A reconciliation of the trade receivables control account with the trade receivables ledger balances on 31 July 2009 revealed a difference of sh.60,000. In August 2009, this difference was discovered to have been caused by failure to add one invoice of the same amount to the July 2009 sales invoice total that was posted to the trade receivables control account. The invoice had been correctly posted to the trade receivables ledger.

8. The financial year end of pambazuka Ltd. is 31 August

Required:

(i) Trade receivables ledger control account

(ii) Trade payables ledger control account

(iii) A schedule showing how trade receivables would appear in the statement of financial position as at 31 August 2009

Date posted: October 3, 2022. Answers (1)

- Distinguish between bad debts and allowance for doubtful debts(Solved)

Distinguish between bad debts and allowance for doubtful debts

Date posted: October 3, 2022. Answers (1)

- Martin Stanley is a sole proprietor. He does not maintain a double entry system of accounting.

The following information was extracted from the books of the...(Solved)

Martin Stanley is a sole proprietor. He does not maintain a double entry system of accounting.

The following information was extracted from the books of the business as at 31 March 2008:

Sh.

Freehold property 900,000

Motor Vehicles 1,125,000

Inventory 585,000

Trade payables 570,000

Trade receivables 750,000

10% Bank Loan 600,000

Bank Overdraft 90,000

Other payables (electricity) 22,500

Prepayments (wages) 60,000

Allowance for doubtful debts 37,500

Additional information

1. Inventory as at 31 March 2009 was valued at sh. 645,000

2. The following transactions were carried out through the bank account during the year ended 31 March 2009:

Sh.

Receipts from trade receivables 2,835,000

Cash sales 1,080,000

Payments to trade payables 2,910,000

Cash purchases 360,000

Proceeds from sale of motor vehicle 180,000

Salaries and wages 240,000

General expenses 90,000

Electricity 60,000

Interest on loan 30,000

Drawings 105,000

3. Sales and purchases on credit amounted to sh. 3,120,000 and sh. 2,850,000 respectively

4. Interest on loan was paid on 30 September 2008

5. The discount received and discount allowed during the year amounted to sh.60,000 and sh.105,000

respectively.

6. Bad debts written off during the year amounted to sh.30,000. Allowance for doubtful debts is to be made at 5% of the trade receivables as at 31 March 2009

7. Accrued electricity was sh.28,000 while prepaid salaries amounted to sh.42,000 as at 31 March 2009

8. Motor vehicles are to be depreciated using reducing balance method at the rate of 20% per annum. A full year’s depreciation is provided in the year of purchase and non in the year of disposal. The Motor vehicle sold during the year had been purchases at sh.400,000 on 1 January 2006

Required:

(a) Income statement for the year ended 31 March 2009

(b) Statement of financial position as at 31 March 2009

Date posted: October 3, 2022. Answers (1)

- The following revenue information was obtained from the books of account of the Ministry of Local

Government for the year ended 30 June 2009

...(Solved)

The following revenue information was obtained from the books of account of the Ministry of Local

Government for the year ended 30 June 2009

Estimated revenue Actual receipts

Sh. "000" Sh. "000"

Rent from buildings and Equipment 850,000 870,000

Fees from trading licenses 430,000 400,000

Fees from import and export licenses 470,000 480,000

Other receipts 235,000 210,000

Additional information

1. The balances at hand on 30 June 2008 amounted to sh. 247,000,000

2. The balances at hand on 30 June 2009 amounted to sh. 160,000,000

Required:

Revenue account for the ended 30 June 2009

Date posted: October 3, 2022. Answers (1)

- In the context of public sector accounting, explain the following terms

(i) Budgetary accounting

(ii) Cash accounting

(iii) Accruals accounting

(iv) Commitment accounting

(v) Fund accounting(Solved)

In the context of public sector accounting, explain the following terms

(i) Budgetary accounting

(ii) Cash accounting

(iii) Accruals accounting

(iv) Commitment accounting

(v) Fund accounting

Date posted: October 3, 2022. Answers (1)

- The financial statements of Savannah Ltd. for the year ended 30 April 2009 and 30 April 2010 are given below:

Income Statement for the years ended...(Solved)

The financial statements of Savannah Ltd. for the year ended 30 April 2009 and 30 April 2010 are given below:

Income Statement for the years ended 30 April

2010 2009

Sh. "000" Sh. "000"

Revenue 396,900 378,000

Cost of sales (217,140) (219,240)

Gross profits 179,760 158,760

Administrative expenses (31,563) (29,589)

Distribution expenses (35,070) (32,865)

Profit from Operations 113,127 96,306

Finance cost (17,115) (14,784)

Profit before tax 96,012 81,522

Income tax expense (42,000) (28,980)

Net profit for the year 54,012 52,542

Extract of the statement of changes in equity (retained earnings) for the year ended 30 April:

2010 2009

Sh. "000" Sh. "000'

Opening balance 135,114 116,172

Net profit for the year 54,012 52,542

Ordinary dividends paid (35,553) (33,600)

Balance as at 30 April 153,573 135,114

Statement of financial position as at 30 April

Assets: 2010 2009

Non-Current Assets Sh. "000" Sh. "000"

Property, Plant and Equipment 443,961 427,476

Current Assets

Inventory 55,923 37,275

Trade receivables 47,460 30,240

Bank balances 1,113 1,050

104,496 68,565

Total assets 548,457 496,041

Equity and Liabilities

Equity and Reserves

Called up share capital 168,000 168,000

Retained profits 153,573 135,114

321,573 303,114

Non-Current Liabilities

12% Loan notes 105,000 105,000

Current Liabilities

Trade payables 8,148 8,190

Bank overdraft 48,800 27,300

Tax payable 64,936 52,437

121,884 87,927

Equity and Liabilities 548,457 496,041

Required:

(a) For each year, compute the following ratios

(i) Gross profit margin

(ii) Profit margin

(iii) Return on capital employed

(iv) Current ratio

(v) Acid test ratio

(vi) Inventory turnover

(vii) Trade receivables collections period

(b) Citing relevant ratios computed in (a) above, briefly comment on the performance of savannah Ltd. using the following criteria

(i) Profitability

(ii) Liquidity

(iii) Efficiency

Date posted: October 3, 2022. Answers (1)

- Explain four benefits that would accrue to a country from adopting International Financial Reporting

Standards (IFRSs)(Solved)

Explain four benefits that would accrue to a country from adopting International Financial Reporting

Standards (IFRSs)

Date posted: October 3, 2022. Answers (1)

- Abdi and Barasa were partners in a Wholesale business sharing profits and losses in the ratio of 3:2 respectively after allowing for interest on capital...(Solved)

Abdi and Barasa were partners in a Wholesale business sharing profits and losses in the ratio of 3:2 respectively after allowing for interest on capital at the rate of 10% per annum. On 1 October 2009, they admitted Chale into the partnership. Chale paid his capital and goodwill contributions of sh. 400,000 and sh. 200,000 respectively in cash.

The partners agreed to allow interest on capital at the rate of 10% per annum and to write off the goodwill paid on admission of Chale. Chale was to share ¼ of the profit and losses of the partnership.

Abdi and Barasa were to share the balance of the profits and losses in the ratio 3:2 respectively. For purposes of admission of Chale into the partnership, Land and Buildings were valued as sh. 2,000,000 on 1 October 2009.

The trial balance extracted from the books of the partnership as at 31 March 2010 was as follows:

Sh. "000' Sh. "000"

Capital accounts

Abdi 900

Barasa 600

Capital introduced by Chale 400

Cash premium paid by Chale 200

Current accounts

Abdi 300

Barasa 200

Drawings

Abdi 100

Barasa 80

Chale 60

Inventory (1 April 2009) 200

Purchase/Sales 5,000 9,000

Administrative expenses 1,600

Selling and distribution costs 1,050

Allowance for doubtful debts 100

Trade receivables /payables 600 500

Land and Buildings 1,400

Equipment at cost 2,000

Provision for depreciation 800

Bank balance 910

13,000 13,000

Additional information

1. Inventory as at 31 March 2010 was valued at sh. 400,000

2. As at 31 March 2010, accrued administrative expenses amounted to sh. 150,000 while prepaid selling and distribution costs amounted to sh. 50,000

3. Depreciation is to be provided on equipment at the rate of 20% per annum based on cost

4. Allowance for doubtful debts is to be increased to sh. 150,000 of which sh. 30,000 relates to the period 1 April 2009 to 30 September 2009

5. Assume sales , gross profit and expenses accrue evenly throughout the year

Required:

(a) Income statement for the year ended 31 March 2010

(b) Statement of financial position as at 31 March 2010

Date posted: October 3, 2022. Answers (1)

- Sabuni Ltd is a medium-sized factory producing a soap branded “malaika”. The following trial balance was

extracted from the books of the company as at 31...(Solved)

Sabuni Ltd is a medium-sized factory producing a soap branded “malaika”. The following trial balance was

extracted from the books of the company as at 31 December 2009.

Sh. “000” Sh. “000”

Ordinary share capital 100,000

10% preference share capital 40,000

15% debentures 20,000

Share premium 2,000

General reserves 6,000

Retained profits 900

Sales 116,400

Purchases of raw materials 24,800

Inventory (1 January 2009)

Raw materials 1,300

Work-in-progress 4,770

Finished goods (90,000units) 8,100

Land 100,000

Buildings (cost) 60,000

Provision for depreciation 6,000

Plant and Machinery at Net book value 4,600

Interest on debentures 1,500

Direct labour 10,800

Carriage inwards 100

Purchase returns 200

General factory costs 1,600

General administrative expenses 20,000

Electricity and water expenses 2,000

Insurance 1,800

Royalty expenses 2,300

Selling and distribution costs 8,200

provision for unrealized profits 1,350

Bank balance 24,000

Motor vehicles at cost (for sales men) 8,000

Provision for depreciation 2,000

Interim dividends paid to preference shareholders 2,000

Trade payables 5,150

Trade receivables 14,130

300,000 300,000

Additional information

1. Inventories as at 31 December 2009 were valued as follows

Sh. "000'

Raw materials 1,500

Work-in-progress 3,100

2. Depreciation is to be provided annually as follows

Buildings at 10% based on cost

Motor Vehicles at 25% based on cost

Plant and Machinery at 30% using reducing method

3. The company apportions expenses between factory and administration in the following ratios;

Factory Administration

Depreciation on buildings 80% 20%

Electricity and water 60% 40%

Insurance 75% 25%

4. Sabuni Ltd. produced 600,000 units and sold 582,000 units during the year. Assume finished goods were

sold on a first-in-first-out basis

5. Finished goods are transferred to the warehouse at cost plus a mark-up of 20%

6. As at 31 December 2009, six month’s interest on the 15% debentures was outstanding while accrued labour costs amounted to sh. 400,000

7. The directors propose to pay the preference shareholders a final dividend. In addition, the directors propose to pay the ordinary shareholders a dividend of 15% per share after the transfer of sh. 4,000,000 to the general reserve.

8. Corporation tax is estimated at sh. 9,900,000

Required:

(a) Manufacturing account and Income statement for the year ended 31 December 2009.

(b) Explain four benefits that would accrue to a country from adopting International Financial Reporting

Standards (IFRSs)

Date posted: October 3, 2022. Answers (1)

- Nguvumali, a Sole Trader who operates a small business in Mombasa, does not keep proper books of account. He had instructed his shop assistant, who...(Solved)

Nguvumali, a Sole Trader who operates a small business in Mombasa, does not keep proper books of account. He had instructed his shop assistant, who absconded duty on 30 March 2010 with an unknown amount of cash, to collect trade receivables and to bank the cash intact.

Given below are the balances extracted from the records of the firm as at 31 March

2009 2010

Sh. "000" Sh. "000'

Buildings 20,000 20,000

Equipment at cost 8,000 8,000

Accumulated depreciation 800 ?

Motor vehicles at cost 8,000 8,000

Accumulated depreciation 2,000 ?

Inventory 7,000 ?

Trade receivables 5,000 4,000

Bank overdraft 4,200 ?

Cash in hand 100 100

Prepaid electricity 100 60

Accrued salaries and wages 600 400

Trade payables 2,000 3,000

Additional information

1. The following transactions were made during the year ended 31 March 2010

Sh. "000"

Cheques paid to trade creditors 41,000

Cash banked during the year 59,940

Cash paid for electricity and water expenses 160

salaries and wages paid through the bank 5,700

Cash withdrawn from the bank for office use 5,000

Cheques paid for selling and distribution costs 1,600

Cash drawings for personal use 3,000

Cash paid for general expenses 1,400

Returns inwards 9,000

Discount allowed 600

Bad debts written off 400

Cash from trade debtors 60,000

Discount received 1,000

2. The firm applied a uniform mark-up of ¾

3. Depreciation on motor vehicles and equipment is to be provided based on cost and annual rates of 25% and 10% respectively. Ignore depreciation on buildings

4. Nguvumali did not have an insurance policy to cover theft by servants

Required:

(a) Determine the amount of cash stolen by the shop assistant

(b) Income statement for the year ended 31 March 2010

(c) Statement of financial position as at 31 March 2010

Date posted: October 3, 2022. Answers (1)

- With reference to the International Public Sector Accounting Standard (IPSASs), explain the following

bases of accounting;

(i) Cash basis

(ii) Accrual basis(Solved)

With reference to the International Public Sector Accounting Standard (IPSASs), explain the following

bases of accounting;

(i) Cash basis

(ii) Accrual basis

Date posted: October 3, 2022. Answers (1)

- Explain the role of the “Paymaster General”(Solved)

Explain the role of the “Paymaster General”

Date posted: October 3, 2022. Answers (1)

- The following balances of the non-current assets were extracted from the books of Charaka Ltd. as at 1 May

2009

...(Solved)

The following balances of the non-current assets were extracted from the books of Charaka Ltd. as at 1 May

2009

Cost Accumulated depreciation

Sh. "000" Sh. "000"

Land 4,162,500 -

Buildings 4,387,500 438,750

Furniture and fittings 1,350,000 450,000

Plant and Machinery 11,081,250 6,693,750

Motor Vehicles 5,287,500 2,205,000

The following relates to the year ended 30 April 2010

1. The depreciation policy of Charaka Ltd is as follows

Non-current Asset Basis of depreciation Rate per annum (%)

Land - -

Buildings Straight-line method 2.50

Plant and machinery Straight-line method 10.0

Motor vehicles Straight-line method 25.0

Furniture and fittings Reducing balance method 12.5

A full year’s depreciation is provided in the year of acquisition. No depreciation is provided in the year of disposal

2. An item of plant acquired on 1 November 2004 for sh. 2,562,500 was disposed of during the year for sh. 1,250,000

3. New machinery was acquired during the year. The following were the cost of acquisition;

Sh.

Invoice price paid 5,215,000

Import duty 724,500

Freight charges 126,740

Annual insurance premium 146,000

Installation cost 178,500

Value added tax 810,500

Input VAT is recoverable from output VAT

4. A delivery Van which was purchased in April 2009 for sh. 2,145,000 was stolen during the year. The

insurers agreed to compensate the company by paying 85% of the cost

5. Land and Buildings were revalued by JLC valuers on 2 May 2009 at sh. 5,675,000 and sh. 4,860,000

respectively.

Required:

Property, Plant and Equipment movement schedule for the year ended 30 April 2010

Date posted: October 3, 2022. Answers (1)

- Briefly explain two types of accounting packages that may be used by an organization and the main features

of these packages.(Solved)

Briefly explain two types of accounting packages that may be used by an organization and the main features

of these packages.

Date posted: October 3, 2022. Answers (1)

- Explain any four roles of the Institute of Certified Public Accountants of Kenya (ICPAK) or the equivalent

body in your country (Solved)

Explain any four roles of the Institute of Certified Public Accountants of Kenya (ICPAK) or the equivalent

body in your country

Date posted: October 3, 2022. Answers (1)

- Salama Ltd. offered 5 million ordinary shares of sh.20 par each payable as follows:

...(Solved)

Salama Ltd. offered 5 million ordinary shares of sh.20 par each payable as follows:

Sh.

• On application 3

• On allotment 8 (including premium)

• On 1st Call 7

• On 2nd and final call 4

The following is a sequence of transactions relating to the issue

Date

May 2010

5: Applications were received for 7,200,000 ordinary shares

18: Applications for 1,200,000 ordinary shares were rejected and the application monies refunded to the

applicants

20: Allotment letters were issued to 6,000,000 applicants. 5 shares were allotted for every 6 shares applied

for. Excess application monies were to be transferred to the allotment account

28: All allotment monies due were received in cash

June 2010

4: First call was made

10: Monies due on first call were received except for 5 shareholders who had been allotted a total of

200,000 shares.

July 2010

20: Second call was made.

28: Monies due on second and final call were received except for sh. 300,000 shares (including 200,000

shares on which first call monies were also not received.

August 2010

6: Shares were forfeited for applicants who had failed to pay monies due on both the first call and second and final call. Those who had not paid the monies due on the second and final call only were issued with notices.

13: The forfeited shares were re-issued at sh.14 per share, the money due being received on the same date.

The following information as at 4th May 2010 is provided

1. The authorized share capital of Salama Ltd is 20 million ordinary shares of sh.20 par value of which

10million ordinary shares had been issued and fully paid

2. The share premium account amounted to sh.12million while cash at bank was sh. 52million

Required:

(a) Journal entries to record the above transactions

(b) Extract from the statement of financial position of Salama Ltd. immediately after the issue

Date posted: October 3, 2022. Answers (1)