1. Fair value adjustment:

The issues is whether fair value adjustment in the purchase method of accounting give rise to deferred tax where the full provision method is used, some feel that deferred tax should not be provided on fair value adjustments because these adjustments are made as a consolidation entry only. Rarely are they taxable or tax deductible and therefore do not affect the tax burden of the company. It is argued that providing for deferred tax on fair value adjustments is not an allocation of an expense but can be used as a smoothing device. Finally, the difference between the carrying amount of net assets acquired and their fair value is goodwill and therefore no deferred tax is required. The arguments in favour of deferred tax are conceptual by nature. If the net assets of the acquirer are shown in the group accounts, then this will affect the post acquisition earnings of the group and tax should be excluded. Additionally, since an acquisition gives rise to no tax effect, the effective tax rate in the profit and loss account should not be distorted as a result of the acquisition. Thus deferred tax should as an adjustment to reflect the reduction in the value of the asset

2. Revaluation of Fixed Assets:

Can be seen as creating a further temporary difference because it reflects an adjustment of depreciation which is itself a temporary difference. Alternative view is that is a permanent difference as it has no equivalent within the tax computation. The

revaluation is not a reversal of previous depreciation, simply that the remaining life of the asset will measure at a different amount. Deferred tax is a valuation adjustment and whilst a revaluation does not directly give rise to a tax liability, the tax status of the asset is inferior to an equivalent asset at historical cost and therefore provision or deferred tax should be made in order to reflect the true after tax cost of the asset. The revalued asset would not attract the same tax allowances as an asset purchased for the same amount and therefore if deferred tax was not provided it would distort the post revaluation effective tax rate.

Wilfykil answered the question on February 8, 2019 at 07:32

-

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms...

(Solved)

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms of the agreement, the machine is to be made available to Silversands Manufacturing Company Ltd. on 1 January 2005, when an immediate payment of Sh. 2,550,000 will be made, followed by seven semi-annual payments of an equivalent amount.

The fair market price of the machine on 1 January 2005 is expected to be Sh. 16,320,000. The estimated life of this type of machine is four years. The implicit rate of interest in the transaction is 6.94% payable semi-annually and the corporate tax rate is 30%. Silversands Manufacturing Company Ltd. has a policy of depreciating machines of this type over a four year period on the straight line basis.

Assume the lease is to be capitalized.

Show Balance sheet extracts of Silversands Manufacturing Company Ltd. as at 31 December 2005 and 2006.

(use the acturial method to allocate the interest charge)

Date posted:

February 8, 2019

.

Answers (1)

-

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms...

(Solved)

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms of the agreement, the machine is to be made available to Silversands Manufacturing Company Ltd. on 1 January 2005, when an immediate payment of Sh. 2,550,000 will be made, followed by seven semi-annual payments of an equivalent amount.

The fair market price of the machine on 1 January 2005 is expected to be Sh. 16,320,000. The estimated life of this type of machine is four years. The implicit rate of interest in the transaction is 6.94% payable semi-annually and the corporate tax rate is 30%. Silversands Manufacturing Company Ltd. has a policy of depreciating machines of this type over a four year period on the straight line basis.

Assume the lease is to be capitalized.

Show how the above transactions will be reflected in the profit and loss account of Silversands Manufacturing Company Ltd. for each of the four years ending 31 December 2005, 2006, 2007 and 2008

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 17 (Leases), briefly explain the meaning of the term Contingent rent.

(Solved)

In the context of IAS 17 (Leases), briefly explain the meaning of the term Contingent rent.

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 17 (Leases), briefly explain the meaning of the following term:Guaranteed residual value.

(Solved)

In the context of IAS 17 (Leases), briefly explain the meaning of the term: Guaranteed residual value.

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 17 (Leases), briefly explain the meaning of the term: Finance lease.

(Solved)

In the context of IAS 17 (Leases), briefly explain the meaning of the term: Finance lease.

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of the International Accounting Standards Board’s Framework for the Preparation and Presentation of financial statements, identify and briefly explain any four qualitative...

(Solved)

In the context of the International Accounting Standards Board’s Framework for the Preparation and Presentation of financial statements, identify and briefly explain any four qualitative characteristics of financial statements

Date posted:

February 8, 2019

.

Answers (1)

-

With reference to IAS 36 (Impairment of Assets), identify any four circumstances that may indicate that an asset has been impaired

(Solved)

With reference to IAS 36 (Impairment of Assets), identify any four circumstances that may indicate that an asset has been impaired

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Balance sheet extracts using two methods: Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life...

(Solved)

Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life of 4yrs and nil residual value. The expected profits of the co. before accounting for deprecation of the new machinery amounts to 50,000 p. a in each year of the machinery life

Determine Balance sheet extracts using two methods

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Profit and Loss Account Extract: Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life...

(Solved)

Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life of 4yrs and nil residual value. The expected profits of the co. before accounting for deprecation of the new machinery amounts to 50,000 p. a in each year of the machinery life

Determine Profit and Loss Account Extract

Date posted:

February 8, 2019

.

Answers (1)

-

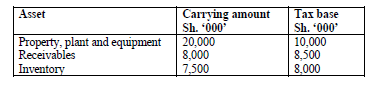

Jenga Ltd. had a deferred tax liability balance brought forward of Sh.2 million. As at 31 December 2008, the firm hand the following assets

(Solved)

Jenga Ltd. had a deferred tax liability balance brought forward of Sh.2 million. As at 31 December 2008, the firm hand the following assets

Temporary difference due to revaluation of buildings in the year was Sh. 1,000,000.

Compute the deferred tax liability as at 31 December 2008 and show the relevant journal

entry.

Date posted:

February 8, 2019

.

Answers (1)

-

Highlight four circumstances under which a legacy may fail

(Solved)

Highlight four circumstances under which a legacy may fail

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment,Outline any two disclosure requirement for items of property, plant and equipment which are stated at...

(Solved)

In the context of IAS 16 property, plant and equipment,Outline any two disclosure requirement for items of property, plant and equipment which are stated at revalued amounts

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment, Briefly describe the accounting treatment with respect to the increase in the carrying amount of...

(Solved)

In the context of IAS 16 property, plant and equipment,Briefly describe the accounting treatment with respect to the increase in the carrying amount of an asset as a result of revaluation

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment, Explain when the cost of an item of property ,plant and equipment should be recognized...

(Solved)

In the context of IAS 16 property, plant and equipment, Explain when the cost of an item of property ,plant and equipment should be recognized as an asset

Date posted:

February 8, 2019

.

Answers (1)

-

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets,Describe the accounting treatment of contingent liabilities in the financial statements

(Solved)

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets,Describe the accounting treatment of contingent liabilities in the financial statements

Date posted:

February 8, 2019

.

Answers (1)

-

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets,Identify the three circumstances under which a provision should be recognized in

the...

(Solved)

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets, Identify the three circumstances under which a provision should be recognized in the financial statements

Date posted:

February 8, 2019

.

Answers (1)

-

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets, Distinguish between “provisions” and “Contingent liabilities”

(Solved)

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets, Distinguish between “provisions” and “Contingent liabilities”

Date posted:

February 8, 2019

.

Answers (1)

-

Outline the four main categories of financial instruments in the context of International Accounting Standard (IAS) 39

(Solved)

Outline the four main categories of financial instruments in the context of International Accounting Standard (IAS) 39

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Extracts of the statement of financial position as at December 2009 and 2010

(Solved)

On 1 January 2009, Kamulu Limited leased a machine from General Machines Ltd. under a finance lease agreement. Kamulu Limited was to make installment lease payments of Sh. 14,000,000 every six months on 30 June and 31 December in arrears.The first payment was made on 30 June 2009.The fair value of the machine was Sh.60,000,000 with an estimated useful life of 3 years.The interest rate implicit in the lease was 10% per six months.

Determine Extracts of the statement of financial position as at December 2009 and 2010

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Extracts of the statement of comprehensive income for the years ended 31 December 2009 and 2010

(Solved)

On 1 January 2009, Kamulu Limited leased a machine from General Machines Ltd. under a finance lease agreement. Kamulu Limited was to make installment lease payments of Sh. 14,000,000 every six months on 30 June and 31 December in arrears.The first payment was made on 30 June 2009.The fair value of the machine was Sh.60,000,000 with an estimated useful life of 3 years.The interest rate implicit in the lease was 10% per six months.

Determine Extracts of the statement of comprehensive income for the years ended 31 December

2009 and 2010.

Date posted:

February 8, 2019

.

Answers (1)