-

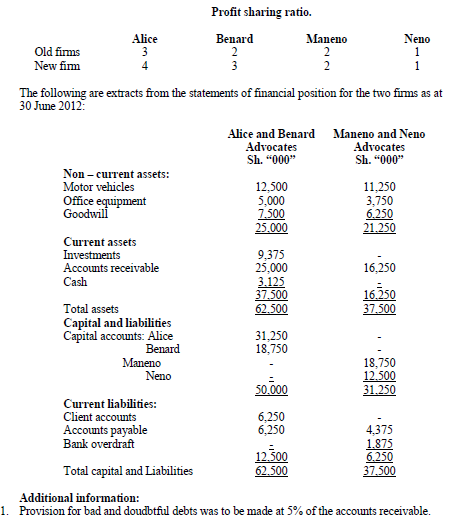

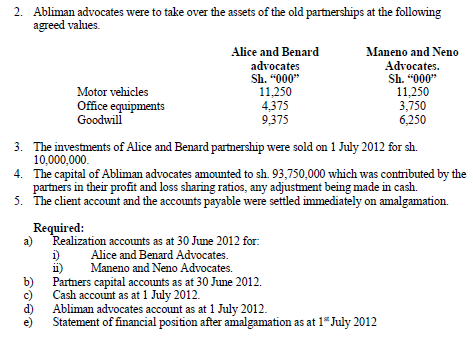

Alice and Benard Advocates and Maneno and Neno Advocates were practicing firms of Advocates. On 1 July 2012, they agreed to amalgamate their partnership businesses...

(Solved)

Alice and Benard Advocates and Maneno and Neno Advocates were practicing firms of Advocates. On 1 July 2012, they agreed to amalgamate their partnership businesses into one firm and called it Abliman advocates. The accounts of the separate partnerships have been prepared annually to 30 June 2012.

The agreed profit and loss sharing ratios in the old and new firms are as follows:

Date posted:

February 8, 2019

.

Answers (1)

-

Capps Ltd.., a manufacturing company, leased production equipment from Deux Ltd On 1st January 2008. The lease provided for an immediate rental payment of sh....

(Solved)

Capps Ltd.., a manufacturing company, leased production equipment from Deux Ltd On 1st January 2008. The lease provided for an immediate rental payment of sh. 10 million and three other annual rentals of shs. 10 million commencing 1 January 2009. The equipment has an estimated useful life of four years with a nil residual value. The cash selling price of equipment is shs.32.1 million. Interest rate implicit in the lease is 17 per cent per annum.

Required:-

For the years ended 31 December 2008, 2009, 2010 and 2011, show in the books of Capps Ltd:-

i) Extracts of the profit and loss account.

ii) Extracts of the balance sheet.

Date posted:

February 8, 2019

.

Answers (1)

-

A lessor leases out an asset on terms which constitute a finance lease. The primary period is five years commencing 1 July 2010 and the...

(Solved)

A lessor leases out an asset on terms which constitute a finance lease. The primary period is five years commencing 1 July 2010 and the rental payable is Sh.3, 000,000 per annum (in arrears). The lessee has the right to continue the lease after the five-year period referred to an indefinite period at a nominal rent. The cash price of the asset in question as at 1 July 2010 can be assumed to be Sh.11, 372,000. The rate of interest implicit in the lease is 10%.

Required:

Show the accounting entries in the leaser’s books (Apply the requirements of IAS 17- Leases).

Date posted:

February 8, 2019

.

Answers (1)

-

Madini Ltd. has entered into an agreement with a finance company to lease a machine for a four-year period. Under the terms of the agreement,...

(Solved)

Madini Ltd. has entered into an agreement with a finance company to lease a machine for a four-year period. Under the terms of the agreement, the machine is to be made available, to Madini Ltd. on 1 January 2012'; when an immediate payment of Sh.2,550,000 will be made, followed by seven semi-annual payments of an equal amount. The fair market price of the machine on 1 January 2012 is expected to be Sh. 16,320,000. The estimated useful life of this type of machine is 4 years. The implicit rate of interest in the transaction is 6.94% payable annually. The corporate tax rate is 30%. Madini Ltd.'s policy is to depreciate machines of this type over four-year period using the straight line basis.

Required:

Show how the above transaction would be reflected in the income statement of Madini Ltd for each of the four years ending 31 December 2012,2013,2014 and 2015.

(Assume that the lease is to be capitalised: Use the actuarial method to allocate the interest

charge)

Date posted:

February 8, 2019

.

Answers (1)

-

Discuss the reasons why IAS 12 (revised) requires enterprises to provide for deferred taxation on revaluations of assets and fair value adjustments on business combination.

(Solved)

IAS 12 (revised) “Income Taxes” requires an enterprise to provide for deferred tax in full for all deferred tax liabilities with only limited expectations. The original IAS 12, and the equivalent Kenyan Accounting Standard, allowed an enterprise not to recognize deferred tax assets and liabilities where there was reasonable evidence that timing differences would not reverse for some considerable period ahead; this was known as the partial provision method.

The original IAS 12 did not refer explicitly to fair value adjustments made on a business combination and did not require an enterprise to recognize a deferred tax liability in respect of asset revaluations. The revised IAS 12 now requires deferred tax adjustments for these items and classifies them as temporary differences.

Discuss the reasons why IAS 12 (revised) requires enterprises to provide for deferred taxation on revaluations of assets and fair value adjustments on business combination.

Date posted:

February 8, 2019

.

Answers (1)

-

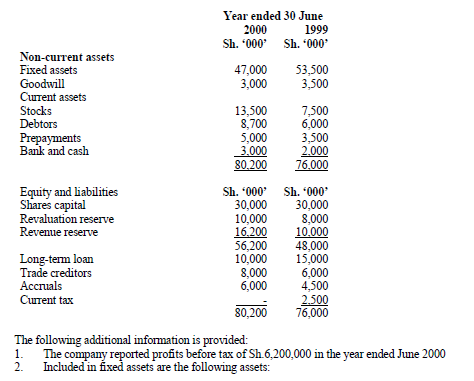

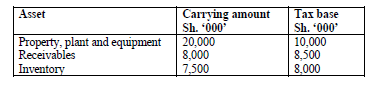

Calculate The current tax account, deferred tax account and revaluation account for the years 1999 and 2000

(Solved)

Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000, the company changed to deferred tax method and the new policy was to be applied retroactively to the accounts of the years ended 30 June 1999 and 2000.

The following are the balance sheets of the company for the two years ended 30 June 199 and 2000 before incorporating tax expense for the year 2000.

Calculate The current tax account, deferred tax account and revaluation account for the years 1999 and 2000

Date posted:

February 8, 2019

.

Answers (1)

-

Using the method recommended by the revised IAS 12, calculate deferred tax expense or income for the years 1999 and 2000

(Solved)

Jallam Co. Ltd. had been preparing its financial statements using actual taxes payable method for computing tax expense. In the year ended 30 June 2000, the company changed to deferred tax method and the new policy was to be applied retroactively to the accounts of the years ended 30 June 1999 and 2000.

The following are the balance sheets of the company for the two years ended 30 June 199 and 2000 before incorporating tax expense for the year 2000.

Using the method recommended by the revised IAS 12, calculate deferred tax expense or income for the years 1999 and 2000

Date posted:

February 8, 2019

.

Answers (1)

-

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms...

(Solved)

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms of the agreement, the machine is to be made available to Silversands Manufacturing Company Ltd. on 1 January 2005, when an immediate payment of Sh. 2,550,000 will be made, followed by seven semi-annual payments of an equivalent amount.

The fair market price of the machine on 1 January 2005 is expected to be Sh. 16,320,000. The estimated life of this type of machine is four years. The implicit rate of interest in the transaction is 6.94% payable semi-annually and the corporate tax rate is 30%. Silversands Manufacturing Company Ltd. has a policy of depreciating machines of this type over a four year period on the straight line basis.

Assume the lease is to be capitalized.

Show Balance sheet extracts of Silversands Manufacturing Company Ltd. as at 31 December 2005 and 2006.

(use the acturial method to allocate the interest charge)

Date posted:

February 8, 2019

.

Answers (1)

-

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms...

(Solved)

Silversands Manufacturing Company Ltd. has entered into an agreement with a finance company, to lease a machine for a four year period. Under the terms of the agreement, the machine is to be made available to Silversands Manufacturing Company Ltd. on 1 January 2005, when an immediate payment of Sh. 2,550,000 will be made, followed by seven semi-annual payments of an equivalent amount.

The fair market price of the machine on 1 January 2005 is expected to be Sh. 16,320,000. The estimated life of this type of machine is four years. The implicit rate of interest in the transaction is 6.94% payable semi-annually and the corporate tax rate is 30%. Silversands Manufacturing Company Ltd. has a policy of depreciating machines of this type over a four year period on the straight line basis.

Assume the lease is to be capitalized.

Show how the above transactions will be reflected in the profit and loss account of Silversands Manufacturing Company Ltd. for each of the four years ending 31 December 2005, 2006, 2007 and 2008

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of the International Accounting Standards Board’s Framework for the Preparation and Presentation of financial statements, identify and briefly explain any four qualitative...

(Solved)

In the context of the International Accounting Standards Board’s Framework for the Preparation and Presentation of financial statements, identify and briefly explain any four qualitative characteristics of financial statements

Date posted:

February 8, 2019

.

Answers (1)

-

With reference to IAS 36 (Impairment of Assets), identify any four circumstances that may indicate that an asset has been impaired

(Solved)

With reference to IAS 36 (Impairment of Assets), identify any four circumstances that may indicate that an asset has been impaired

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Balance sheet extracts using two methods: Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life...

(Solved)

Muniu Ltd received a 20 % grant towards the cost of new item of machinery that cost ksh. 100,000 kshs.The machinery her on expected life of 4yrs and nil residual value. The expected profits of the co. before accounting for deprecation of the new machinery amounts to 50,000 p. a in each year of the machinery life

Determine Balance sheet extracts using two methods

Date posted:

February 8, 2019

.

Answers (1)

-

Jenga Ltd. had a deferred tax liability balance brought forward of Sh.2 million. As at 31 December 2008, the firm hand the following assets

(Solved)

Jenga Ltd. had a deferred tax liability balance brought forward of Sh.2 million. As at 31 December 2008, the firm hand the following assets

Temporary difference due to revaluation of buildings in the year was Sh. 1,000,000.

Compute the deferred tax liability as at 31 December 2008 and show the relevant journal

entry.

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment,Outline any two disclosure requirement for items of property, plant and equipment which are stated at...

(Solved)

In the context of IAS 16 property, plant and equipment,Outline any two disclosure requirement for items of property, plant and equipment which are stated at revalued amounts

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment, Briefly describe the accounting treatment with respect to the increase in the carrying amount of...

(Solved)

In the context of IAS 16 property, plant and equipment,Briefly describe the accounting treatment with respect to the increase in the carrying amount of an asset as a result of revaluation

Date posted:

February 8, 2019

.

Answers (1)

-

In the context of IAS 16 property, plant and equipment, Explain when the cost of an item of property ,plant and equipment should be recognized...

(Solved)

In the context of IAS 16 property, plant and equipment, Explain when the cost of an item of property ,plant and equipment should be recognized as an asset

Date posted:

February 8, 2019

.

Answers (1)

-

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets,Describe the accounting treatment of contingent liabilities in the financial statements

(Solved)

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets,Describe the accounting treatment of contingent liabilities in the financial statements

Date posted:

February 8, 2019

.

Answers (1)

-

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets, Distinguish between “provisions” and “Contingent liabilities”

(Solved)

With respect to International Accounting Standard (IAS) 37 ,provisions ,contingent liabilities and contingent Assets, Distinguish between “provisions” and “Contingent liabilities”

Date posted:

February 8, 2019

.

Answers (1)

-

Outline the four main categories of financial instruments in the context of International Accounting Standard (IAS) 39

(Solved)

Outline the four main categories of financial instruments in the context of International Accounting Standard (IAS) 39

Date posted:

February 8, 2019

.

Answers (1)

-

Determine Extracts of the statement of financial position as at December 2009 and 2010

(Solved)

On 1 January 2009, Kamulu Limited leased a machine from General Machines Ltd. under a finance lease agreement. Kamulu Limited was to make installment lease payments of Sh. 14,000,000 every six months on 30 June and 31 December in arrears.The first payment was made on 30 June 2009.The fair value of the machine was Sh.60,000,000 with an estimated useful life of 3 years.The interest rate implicit in the lease was 10% per six months.

Determine Extracts of the statement of financial position as at December 2009 and 2010

Date posted:

February 8, 2019

.

Answers (1)