1. Benefits of IFRs for SMEs

- Improved access to capital.

- Improved quality and comparability or reporting.

- Facilitates cross-border trading.

- Focus on the needs of users of SME financial statement.

- Audit efficiencies.

- Stability - initial 2 year comprehensive review followed by 3-year omnibus updates.

- Eases burden where full IFRS has previously been required.

- Stepping stone to full IFRS for private entities aiming for initial offering (IPO).

2. Challenges facing implementation of IFRS

- Learning new technologies and accounting techniques.

- Making changes to information systems and accounting software may be needed.

- Collecting additional data for some transactions

- Dealing with new concepts.

- Dealing with valuation issues

Wilfykil answered the question on February 13, 2019 at 07:02

-

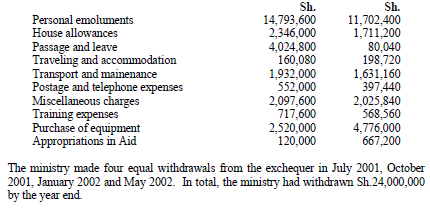

The approved estimates and actual expenditure details for the Ministry of Planning and Development for the year 2001/2002 were as follows:

Prepare:

(i) The General Account of...

(Solved)

The approved estimates and actual expenditure details for the Ministry of Planning and Development for the year 2001/2002 were as follows:

Prepare:

(i) The General Account of Vote.

(ii) The Exchequer Account

(iii) The Paymaster General Account.

(iv) Statement of assets and liabilities as at 30 June 2002.

Date posted:

February 13, 2019

.

Answers (1)

-

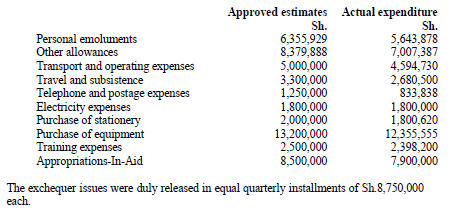

The following are details relating to approved estimates and actual expenditure for a certain government department for the financial year ended 30 June 2003

Prepare:

i) Paymaster...

(Solved)

The following are details relating to approved estimates and actual expenditure for a certain government department for the financial year ended 30 June 2003

Prepare:

i) Paymaster general account.

ii) Exchequer account.

iii) General account of vote

iv) Statement of assets and liabilities as at 30 June 2003.

Date posted:

February 13, 2019

.

Answers (1)

-

Briefly explain the following terms in relation to government accounting:

(i) Exchequer over issues.

(ii) Paymaster General

(iii) Vote on account.

(iv) Commitment accounting.

(Solved)

Briefly explain the following terms in relation to government accounting:

(i) Exchequer over issues.

(ii) Paymaster General

(iii) Vote on account.

(iv) Commitment accounting.

Date posted:

February 13, 2019

.

Answers (1)

-

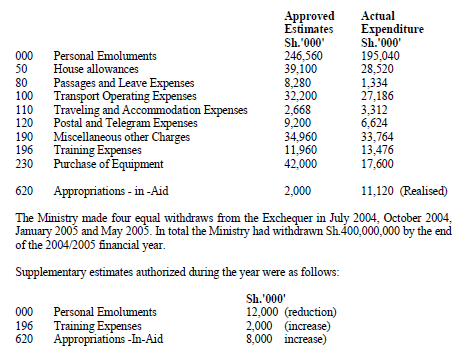

The approved Estimates and Actual Expenditure details for vote E45 of ministry ABC for the financial year 2004/2005 were as follows:

Required:

a) Appropriation account for the...

(Solved)

The approved Estimates and Actual Expenditure details for vote E45 of ministry ABC for the financial year 2004/2005 were as follows:

Required:

a) Appropriation account for the year ended 30 June 2005

b) General Account of vote for the year ended 30 June 2005.

c) Exchequer Account for the year ended 30 June 2005

d) Paymaster General (PMG) account for the year ended 30 June 2005

e) Statement of assets and liabilities as at 30 June 2005.

Date posted:

February 13, 2019

.

Answers (1)

-

Outline the powers of the Auditor General in the exercise of his duties

(Solved)

Outline the powers of the Auditor General in the exercise of his duties

Date posted:

February 13, 2019

.

Answers (1)

-

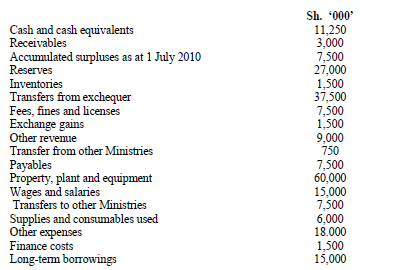

The following information was extracted from the books of the Ministry of Commerce and Industrialization for the fiscal year ended 30 June 2011:

Prepare:

(i) Statement of...

(Solved)

The following information was extracted from the books of the Ministry of Commerce and Industrialization for the fiscal year ended 30 June 2011:

Prepare:

(i) Statement of financial performance for the year ended 30 June 2011.

(ii) Statement of financial position as at 30 June 2011.

Date posted:

February 13, 2019

.

Answers (1)

-

Explain two requirements that should be met for government grants to be recognized in the financial statements in the context of International Accounting Standard (IAS)...

(Solved)

Explain two requirements that should be met for government grants to be recognized in the financial statements in the context of International Accounting Standard (IAS) 20.

Date posted:

February 13, 2019

.

Answers (1)

-

In the context of International Accounting Standard (1AS) 21, distinguish between the accounting treatment for foreign currency transactions "on initial recognition" and "at the end...

(Solved)

In the context of International Accounting Standard (1AS) 21, distinguish between the accounting treatment for foreign currency transactions "on initial recognition" and "at the end of subsequent reporting periods".

Date posted:

February 13, 2019

.

Answers (1)

-

List the circumstances under which a subsidiary should be excluded from the consolidated financial statement

(Solved)

List the circumstances under which a subsidiary should be excluded from the consolidated financial statement

Date posted:

February 12, 2019

.

Answers (1)

-

Explain four circumstances in which a parent company is exempted from consolidating investments in subsidiaries in accordance with International Accounting Standards (IAS)27- Consolidated and separate...

(Solved)

Explain four circumstances in which a parent company is exempted from consolidating investments in subsidiaries in accordance with International Accounting Standards (IAS)27- Consolidated and separate financial statements

Date posted:

February 12, 2019

.

Answers (1)

-

Auma Ltd. acquired 80% of the ordinary shares of Sakwa Ltd. on 31 October 2009 for Sh. 117 million. At this date, the net assets...

(Solved)

Auma Ltd. acquired 80% of the ordinary shares of Sakwa Ltd. on 31 October 2009 for Sh. 117 million. At this date, the net assets of Sakwa Ltd. were Sh. 127.5 million. The fair value of the non-controlling interest on the acquisition date was Sh.28.5 million.

Calculate the value of goodwill using the two methods

Date posted:

February 12, 2019

.

Answers (1)

-

Distinguish between the full method and the partial method of determining goodwill arising on acquisition of a subsidiary company

(Solved)

Distinguish between the full method and the partial method of determining goodwill arising on acquisition of a subsidiary company

Date posted:

February 12, 2019

.

Answers (1)

-

Briefly explain three circumstances in which a parent company need not present consolidated financial statements in accordance with International Accounting Standard (IAS ) 27 ,Consolidated...

(Solved)

Briefly explain three circumstances in which a parent company need not present consolidated financial statements in accordance with International Accounting Standard (IAS ) 27 ,Consolidated and Separate financial Statements

Date posted:

February 12, 2019

.

Answers (1)

-

Differentiate between full consolidation and equity method of accounting for subsidiaries and associate companies

(Solved)

Differentiate between full consolidation and equity method of accounting for subsidiaries and associate companies

Date posted:

February 12, 2019

.

Answers (1)

-

International Accounting Standard (IAS) 28, Investment in Associates prescribes the use of the equity method of accounting for investments in associates over which the investor...

(Solved)

International Accounting Standard (IAS) 28, Investment in Associates prescribes the use of the equity method of accounting for investments in associates over which the investor has significant influence.

Required:

i) Describe the term "significant influence" in the context of IAS 28.

ii) Explain four circumstances under which the investor is exempted from use of the equity method.

Date posted:

February 12, 2019

.

Answers (1)

-

Explain the circumstances in which an entity is permitted to change its accounting policies.

(Solved)

Explain the circumstances in which an entity is permitted to change its accounting policies.

Date posted:

February 12, 2019

.

Answers (1)

-

What meetings of creditors must be held and for what purpose in the course of a creditors’ voluntary winding up?

(Solved)

What meetings of creditors must be held and for what purpose in the course of a creditors’ voluntary winding up?

Date posted:

February 12, 2019

.

Answers (1)

-

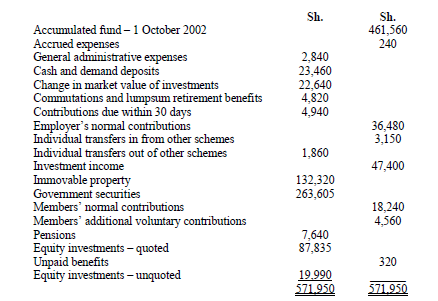

The following trial balance was extracted from the books of ABC Retirement Benefits Scheme for the year ended 30 September 2003:

Prepare:

(i) Statement of changes in...

(Solved)

The following trial balance was extracted from the books of ABC Retirement Benefits Scheme for the year ended 30 September 2003:

Date posted:

February 12, 2019

.

Answers (1)

-

Briefly explain the meaning of the term “abatement”

(Solved)

Briefly explain the meaning of the term “abatement”

Date posted:

February 12, 2019

.

Answers (1)

-

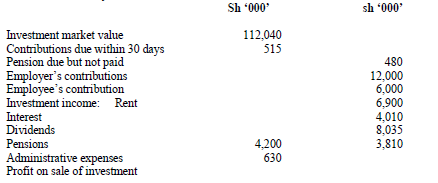

The following trial balance was extracted by the trustees of XYZ Retirement Benefit Scheme as at 31 May 2007

Prepare:

(i) Statement of changes in net assets...

(Solved)

The following trial balance was extracted by the trustees of XYZ Retirement Benefit Scheme as at 31 May 2007

Date posted:

February 12, 2019

.

Answers (1)