-

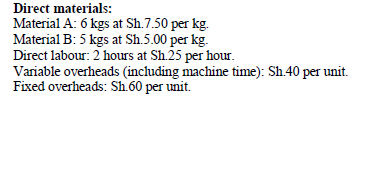

Tec Ltd. manufactures a single product branded 'Zed' for sale on the local and international

market.

The cost structure per unit of product 'Zed' is as follows:

(Solved)

Tec Ltd. manufactures a single product branded 'Zed' for sale on the local and international

market.

The cost structure per unit of product "'zed' is as follows:

Additional information:

1. The current sales level for the company amounts to Sh. 800,000.

2. The fixed overheads per unit have been calculated based on the current sales level of 4,000

units.

Required:

i) Sales price per unit.

ii) Current profit or loss.

iii) Break even point in units and shillings.

iv) Suggest four measures that could be taken to improve the current profit position

Date posted:

February 21, 2019

.

Answers (1)

-

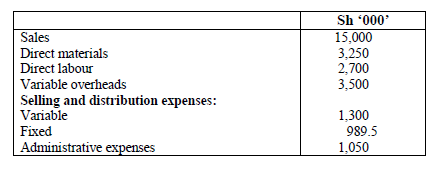

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

(Solved)

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

Date posted:

February 21, 2019

.

Answers (1)

-

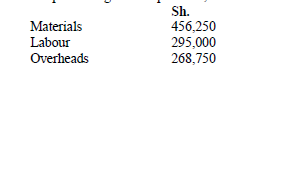

Jitegemee limited company uses a process costing system in its operation. In one of the production processes, two joint products A and B and a...

(Solved)

Jitegemee limited company uses a process costing system in its operation. In one of the

production processes, two joint products A and B and a by-product C are produced

The following additional information is provided:

1. Each processing run requires 12,500 kilograms of output.the costs incurred are as follow:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

Date posted:

February 21, 2019

.

Answers (1)

-

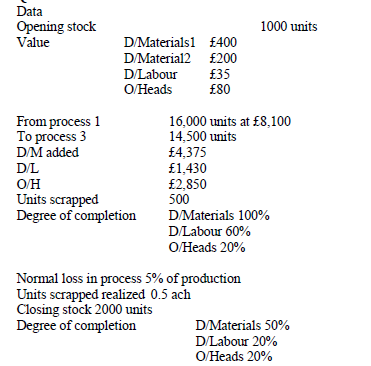

The following information is obtained in respect of process 2 of the month of September;

(Solved)

The following information is obtained in respect of process 2 of the month of September;

There was a normal loss in the process of 10% of production units' scrapped realized sh. 50 per unit,

use FIFO method

Required:

i. Statement of production

ii. Statement of cost and evaluation

iii. Process account

iv. Abnormal loss / gain account

Date posted:

February 21, 2019

.

Answers (1)

-

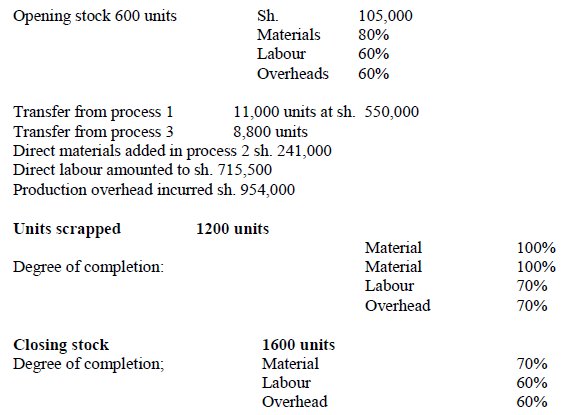

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

(Solved)

Required:

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

Date posted:

February 21, 2019

.

Answers (1)

-

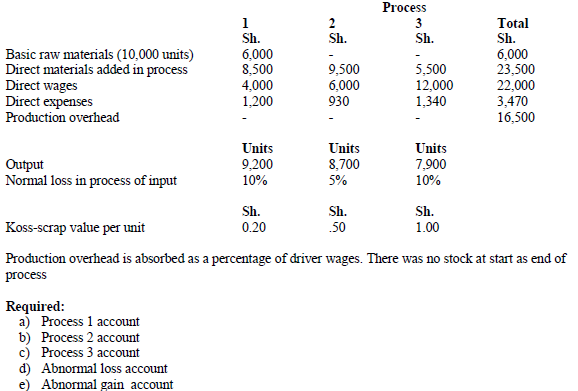

Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information...

(Solved)

Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information was extracted from the books of the company for the month of October.

Date posted:

February 21, 2019

.

Answers (1)

-

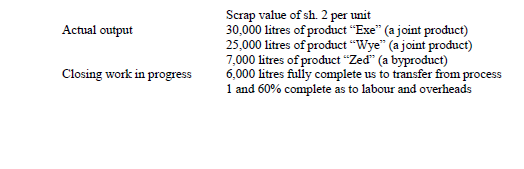

The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed

(Solved)

The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed

Additional information;-

1. The final selling prices per litre of products Exe, Wye and Zed are shs.15, shs.18 and shs.4

respectively.

2. There are no further costs associated with by product Zed

3. Product Wye requires further processing at a cost of sh. 1.50 per litre

4. All the three products incur packaging costs of sh. 0.50 per litre before they are sold.

Required:

i) Calculate the number of equivalent units produced

ii) Calculate the costs of products Exe and Wye

iii) Apportion the common costs to joint products based on sales at the point of separation

iv) Prepare process II account for the month of January 2008

Date posted:

February 21, 2019

.

Answers (1)

-

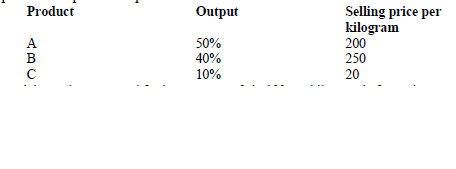

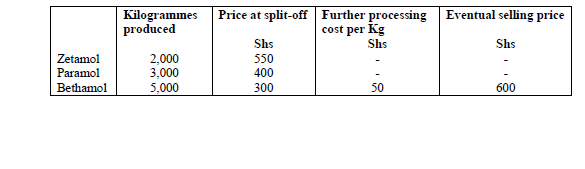

Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material...

(Solved)

Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material nat a cost of sh.2,500,000 and incurred joint conversion costs of

sh.700,000.Sales and production information for the month of January wered as follows;

Zetamol and Paramol are sold to other pharmaceutical companies at the split off point. Bethamol can

be sold at the split off point or processed further and packaged for sale as an asthma medication.

Required

Allocate the joint costs to the three products using;

i) The physical units sold

ii) The sales value at split off method

iii) The net realizable value method

iv) Suppose that half the production of Paramol could be purified and mixed with all the

production of Zetamol to yield parazetamol.All further processing costs amount to

sh.350,000.The selling price for parazetamol is sh.1,120 per kilogramme.Advise the company

on whether to further process Zetamol into 2,000 kilogrammes of parazetamol.

Date posted:

February 21, 2019

.

Answers (1)

-

ABC Company limited produces four products A, B, C and D

The following information is provided

1. The joint processing requires 10,000 kilograms of raw materials input,...

(Solved)

ABC Company limited produces four products A, B, C and D

The following information is provided

1. The joint processing requires 10,000 kilograms of raw materials input, costing sh. 6 million

2. Joint process labour and material costs are sh. 5,920,000

3. Normal loss is 20% of raw material input, with product A's output being 2000 kilogram mes,

product B's output being 2,500 kilogram mes, product C's output being 2,500 kilogram mes and

the balance being from product D. No abnormal loss was reported.

4. Product A enters into process 2 incurring a further cost of sh. 1,255,000 , product B enters

process 3 incurring a further cost of sh. 1,493,750 product C enters into process 4 incurring a

further cost of sh. 1,118,750. Product D does not require additional processing. There are no

further processing costs.

5. The company‟s policy is to apportion joint costs on the basis of output

6. The selling price of each unit of products A, B C and D is sh. 1,500, sh. 3,460, sh. 2760 and sh.

1,000 respectively.

7. The company is in the process of analyzing the performance of each product in order to make

better decisions.

Required:

a) i) Cost per unit of product A

ii) Profit and loss statement for each individual product and for the company in a columnar

format

b) The company's management intends to start using the net realizable value method to allocate

joint costs. Show how this method would affect the profitability of individual products and that

of the company in (a) (ii) above.

Date posted:

February 21, 2019

.

Answers (1)

-

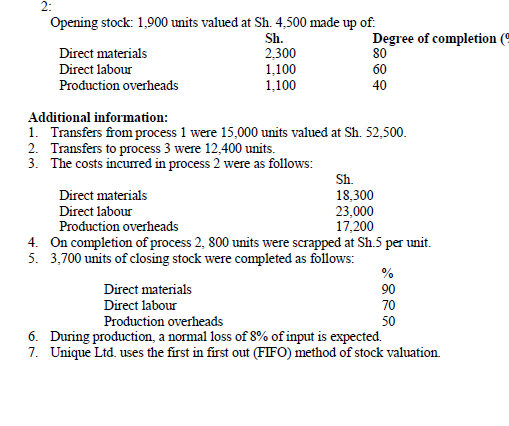

a) Explain why it is necessary to distinguish between direct labour and indirect labour, with

particular reference to the effect on gross profit and net profit.

b)...

(Solved)

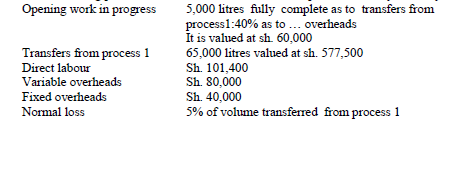

a) Explain why it is necessary to distinguish between direct labor and indirect labor, with

particular reference to the effect on gross profit and net profit.

b) Unique Ltd. manufactures a single product. The product passes through three processes before

completion. In the month of January 2013, the following data was recorded in respect to process

Required:

i) Statement of equivalent production.

ii) Statement of costs.

iii) Process 2 account

Date posted:

February 21, 2019

.

Answers (1)

-

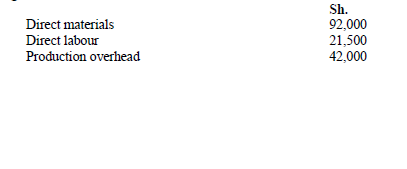

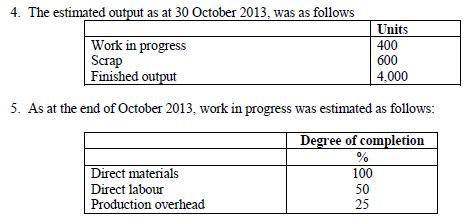

Nald Ltd. manufactures a chemical product and uses process costing to account for its work in

progress. During the month of October 2013, 5,000 units...

(Solved)

Nald Ltd. manufactures a chemical product and uses process costing to account for its work in

progress. During the month of October 2013, 5,000 units were introduced to process 1 and the

following costs were incurred:

Additional information:

1. The normal loss in process 1 was estimated at 10%.

2. The scrapped normal loss units were sold at Sh.4 per unit.

3. Inspection is usually done at the end of the process; therefore any units scrapped would have

passed through the entire process.

Required

i) Statement of equivalent production

ii) Statement of cost

iii) Statement of evaluation of finished goods

iv) Process 1 account

Date posted:

February 21, 2019

.

Answers (1)

-

Explain the meaning of the following terms in regard to the cost and financial accounting

systems:

i) Integrated cost accounts

ii) Interlocking cost accounts

iii) Cost ledger control account

iv)...

(Solved)

Explain the meaning of the following terms in regard to the cost and financial accounting

systems:

i) Integrated cost accounts

ii) Interlocking cost accounts

iii) Cost ledger control account

iv) Cost ledger contra account

Date posted:

February 21, 2019

.

Answers (1)

-

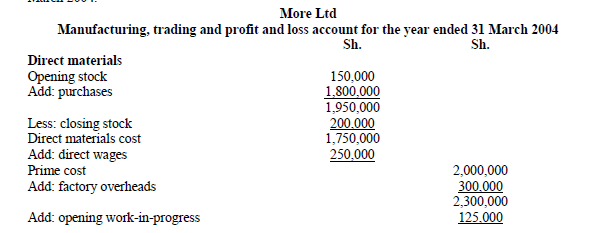

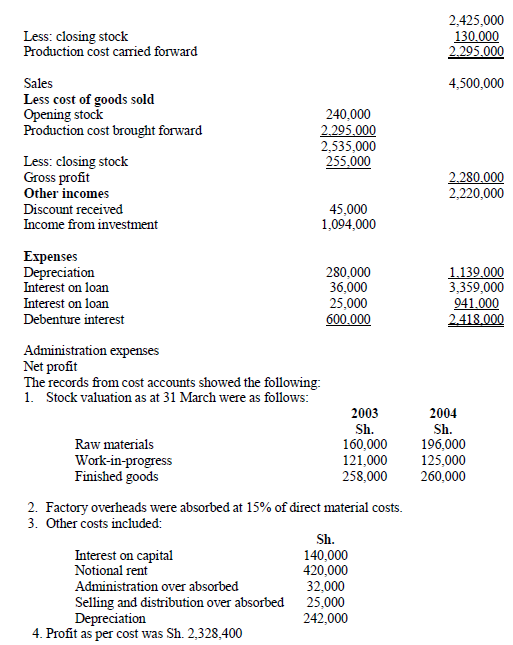

More Ltd. is a medium size manufacturing company and it maintains separate cost and financialaccounting books. The financial accountant provided the following statement for the...

(Solved)

More Ltd. is a medium size manufacturing company and it maintains separate cost and financial

accounting books. The financial accountant provided the following statement for the year ended 31

March 2004.

Required:

Prepare a profit reconciliation statement for the year ended 31 March 2004.

Date posted:

February 19, 2019

.

Answers (1)

-

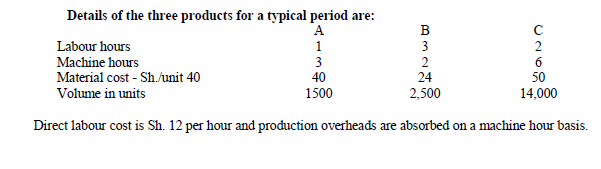

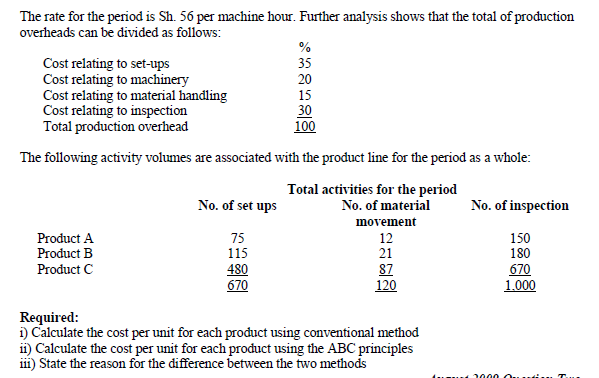

Tengeneza Ltd makes three main products using broadly the same production methods and

equipment for each. A conventional product costing system is used at present, although...

(Solved)

Tengeneza Ltd makes three main products using broadly the same production methods and

equipment for each. A conventional product costing system is used at present, although an

Activity Based Costing (ABC) system is being considered.

Date posted:

February 15, 2019

.

Answers (1)

-

Briefly explain bases of apportionment of overheads.

(Solved)

Briefly explain bases of apportionment of overheads.

Date posted:

February 15, 2019

.

Answers (1)

-

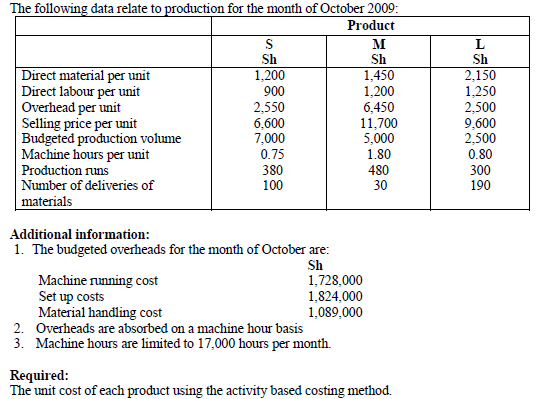

Apex Furniture Ltd. manufactures three products: S, M and L.

(Solved)

Apex Furniture Ltd. manufactures three products: S, M and L.

Date posted:

February 15, 2019

.

Answers (1)

-

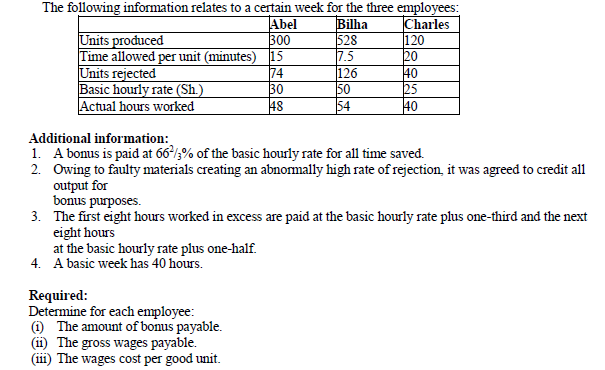

BabyCom Limited manufactures different types of toys. The company engages three employees.

Abel, Bilha and Charles.

(Solved)

BabyCom Limited manufactures different types of toys. The company engages three employees.

Abel, Bilha and Charles.

Date posted:

February 15, 2019

.

Answers (1)

-

Explain the reasons why an organisation might use overheads allocation and apportionment in

allocating costs among cost centres.

(Solved)

Explain the reasons why an organisation might use overheads allocation and apportionment in

allocating costs among cost centres.

Date posted:

February 15, 2019

.

Answers (1)

-

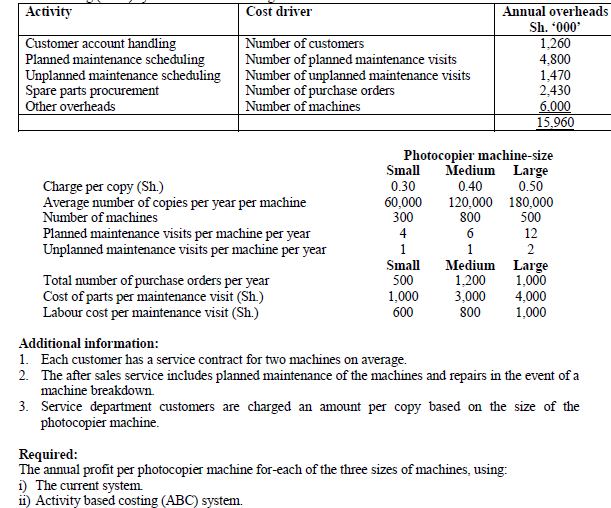

Copytech Ltd. sells and services photocopying machines. The company's sales department sells

the photocopying machines and consumables while the service department provides an after sale

service to...

(Solved)

Copytech Ltd. sells and services photocopying machines. The company's sales department sells

the photocopying machines and consumables while the service department provides an after sale

service to customers.

Currently, Copytech Ltd. uses a single overhead absorption rate to charge overheads based on total

sales revenue from copy charges. However, the service manager has proposed to change to activity

based costing (ABC) system and the following information has been obtained

Date posted:

February 15, 2019

.

Answers (1)

-

Distinguish between 'cost allocation' and 'cost absorption

(Solved)

Distinguish between 'cost allocation and 'cost absorption

Date posted:

February 15, 2019

.

Answers (1)