- The standards in respect of selling price and production costs are set. Standard costs are ascertained for each elements of cost and the main procedures involved in setting standards are explained as under:

1. Direct Material StandardDirect materials price (rate) Standard:

- The unit price of Direct Material purchased should be contingent upon sales forecast. Suppliers need to know an estimate of total quantity to determine amount of discount. Also, need quality and delivery standards before a standard price per unit can be set.

- Material prices and materials usage are set for each product. The quantity of material required for one unit of any product is obtained from technical and engineering specifications. The standard quantity of raw material includes an allowance for normal loss in production due to evaporation or other technical reasons. The material prices are provided by the purchasing department. These prices are set in view of anticipated changes, carriage, quantity and cash discount and any other factors which will influence material costs.

- Price changes must be considered in determining the standards. Can use weighted average of prices, or preferred alternative is to change the standard when prices change.

- A separate standard must be established for each material. It is determined by the cost accounting and/or the purchasing departments. A separate department is established as established standards is a time consuming process.

- Direct materials efficiency (usage) standard predetermined specification of the quantity of direct materials that should go into the production of one finished product. Individual standards must be established for each direct material.

2. Direct labourDirect Labour Standard classified as:

- Direct labour price (rate) standards are predetermined rates of pay for a period usually established by union contract or by management and/or personnel if non union influenced by type of job and experience. Any personnel if non union influenced by type of job and experience. Any pay rate increases during the year must be considered in determining the standards. It can use weighted average of pay rates, or preferred alternative is to change the standard when pay rates increase.

- Direct labour efficiency standards are set in respect of direct labour cost. There are different grades of labour and wage rates payable to different grades of labour are set by the personnel department. These rates are taken as standard rates per hour. The number of labour hours required to produce one unit of any product are set in conjunction with technical experts.

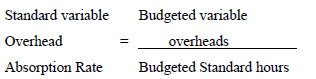

3. OverheadsThe overheads standards are set separately for variable overheads and fixed overheads. The variable overheads are set mostly in terms of labour hours. Variable overhead absorption rate per labour hour is calculated as under:-

- This overhead absorption rate is multiplied by the number of standard hours required for the production of a specific number of units of any product in order to find out the standard variable overhead cost.

- Fixed overheads relate to time and these are constant for a specific year irrespective of fluctuations in the level of output.

- The standard fixed overheads are determined on the basis of the following considerations:-

a) The total cost of fixed overheads for a specific period.

b) The budgeted promotion for a specific period

c) The number of hours expected to be worked during a specific period.

- Fixed overhead absorption rate is calculated as under:-

4. Factory overhead standards

4. Factory overhead standards- Factory OH cost pool includes Indirect Materials, Indirect labour, factory rent, factory depreciation, factory equipment depreciation etc. to prepare the standard usually involves input from many department and managers. Standard costing establishes a single standard cost / unit which is applied despite fluctuations in activity.

- Budgets are commonly used in controlling factory overhead costs. Fixed budgets show anticipated costs at one level of activity. Factory Budget show anticipated costs at different levels of activities.

Wilfykil answered the question on

August 6, 2019 at 09:49