- (a) Briefly explain why goodwill should be paid under the following circumstances:

(i) By a partner on admission to a partnership.

(ii) To a partner on retirement...(Solved)

(a) Briefly explain why goodwill should be paid under the following circumstances:

(i) By a partner on admission to a partnership.

(ii) To a partner on retirement from a partnership.

(b) Abdi, Bob and Caleb are in partnership sharing profits and losses equally after allowing for interest on capital at 5% per annum to the partners and a salary to Bob of sh.30,000 per month.

The trial balance of the partnership as ta 31 September 2012 was as follows:

Sh. "000" Sh. "000"

Capital accounts: Abdi 3,500

Bob 3,000

Caleb 2,000

Current accounts: Abdi 300

Bob 400

Caleb 300

Drawings: Abdi 400

Bob 500

Caleb 300

Sales 30,000

Inventory (1 October 2011) 4,000

Purchases 20,300

Operating expenses 7,400

Loan: Bob (interest at 10% per annum) 2,000

Caleb (interest at 10% per annum) 3,000

Land 2,000

Buildings 6,000

Plant and Machinery (cost) 8,000

Accumulated depreciation (30 September 2012) 5,000

Accounts receivable/accounts payable 5,000 4,300

Cash at bank 100

53,900 53,900

Additional information:

1. Closing inventory as at 30th September 2012 was valued at sh.3,400,000

2. Interest on partner’s loan had not been paid.

3. Sales included credit sales of sh.700,000 in respect of two items sold on the basis of confirmation by the customer. The items had cost sh.200,000 each.

4. On 1 April 2012, the terms of the partnership agreement were changed. The new terms provided for:

• Profit sharing ratio of 5:3:2 for Abdi, Bob and Caleb respectively.

• Interest on capital at 5% per annum

• Salaries of sh.15,000 per month for Bob and Caleb.

5. For the purpose of the change, goodwill was valued at sh.1,200,000 and was to be written off

immediately while the land and buildings were valued at sh.3,000,000 and sh.7,400,000 respectively.

Required:

(i) Income statement and appropriation account for the year ended 30 September 2012.

(ii) Partner’s current accounts.

(iii) Statement of financial position as at 30 September 2012.

Date posted: September 30, 2022. Answers (1)

- (a) Explain the following terms as used in the context of public sector accounting:

(i) Public accounts committee (PAC).

(ii) Appropriation-In-Aid (AIA).

(iii) Public Investment committee (PIC).

(b) The...(Solved)

(a) Explain the following terms as used in the context of public sector accounting:

(i) Public accounts committee (PAC).

(ii) Appropriation-In-Aid (AIA).

(iii) Public Investment committee (PIC).

(b) The approved estimates and actual expenditure details for the ministry of Gender and Culture for the

financial year ended 30 June 2012 were as follows:

Vote no. Details Approved estimates Actual expenditure

Sh. "000" Sh. "000"

S001 Travelling and accommodation 32,100 31,200

S004 Commuter allowances 8,400 7,200

S010 Passage and leave expenses 80,120 75,600

S120 Communication expenses 6,110 5,880

S121 Staff development 10,120 8,440

S124 Vision 2030 flagship 7,150 7,850

S144 Purchase of computers 12,140 10,940

S300 Appropriation-In-Aid 6,000 14,500

S184 Personnel emoluments 241,800 212,300

S200 Miscellaneous expenses 34,480 32,150

S210 Transport expenses 8,300 7,900

S215 Housing allowance 41,300 37,200

The ministry made four equal withdrawals from the Exchequer of sh.110,000,000 each.

Required:

(i) Paymaster general account.

(ii) The Exchequer account.

(iii) General account of Vote

(iv) Statement of Assets and liabilities as at 30 June 2012

Date posted: September 30, 2022. Answers (1)

- The following is a receipt and payment account as reported by the treasurer of Mambula Sports Club for the year ended 31 December 2012.

Receipts ...(Solved)

The following is a receipt and payment account as reported by the treasurer of Mambula Sports Club for the year ended 31 December 2012.

Receipts Sh. "000"

Balance at 1 January 2012: Bank 3,000

Cash in hand 400

Subscription received 9,600

Canteen sales 2,700

Donation (for purchase of bus) 2,000

Dinner dance ticket sales 1,800

Bank interest 360

Investment income 600

20,460

Payments

Canteen purchases 2,010

Water and electricity 270

Sports Equipment 2,000

Canteen attendant wages 300

Canteen expenses 150

Secretary's honoraria 4,500

Training fee 1,500

Grounds man (field) wages 1,200

Field maintenance and repairs 540

Dinner dance expenses 900

Transport and travelling expenses 1,260

Closing balance (31 December 2012):

Bank 3,000

Cash in hand 2,830

20,460

The balances of assets and liabilities as at 31 December 2011 and 2012 were as follows:

2011 2012

Sh. "000" Sh. "000"

Sports equipment 2,400 ?

Club house at cost 9,200 9,200

Furniture and Fittings at cost 1,800 1,800

Canteen stock 600 750

Subscription in arrears 720 840

Subscription in advance 540 1,380

Water bills outstanding 90 220

Canteen creditors 270 360

Accumulated depreciation:

Sports equipment 840 ?

Furniture and Fittings 540 ?

Investment 2,400 2,400

Additional information:

1. Subscriptions money received related to the following periods:

Year Sh. "000"

2011 600

2012 7,620

2013 1,380

It is the policy of the club to write-off subscription in arrears after 12 months

2. Depreciation is to be charged on the cost of assets in existence at the end of the financial year as follows:

• Furniture and Fittings at 10% per annum

• Sports Equipment at 20% per annum

3. During the year, sports equipment was sold for sh.600,000 to club members on credit. These equipment had cost sh.1,200,000 and had been used for two years.

4. Cash sales for the canteen on the last day of the year amounting to sh.300,000 were omitted in the records as well as on the cash reported.

Required:

(a) Canteen income statement for the year ended 31 December 2012.

(b) The club’s income and expenditure account for the year ended 31 December 2012.

(c) Statement of financial position as at 31 December 2012.

Date posted: September 30, 2022. Answers (1)

- (a) Explain four ways in which the accounting profession is regulated. (8 marks)

(b) The authorized share capital of Mid-View Ltd. consists of 800,000 shares of...(Solved)

(a) Explain four ways in which the accounting profession is regulated. (8 marks)

(b) The authorized share capital of Mid-View Ltd. consists of 800,000 shares of sh.20 each and 250,000 8% redeemable preference shares of sh.20 each.

The following information was extracted from the books of the company as at 31 December 2012 after

preparing the income statement for the year:

Sh. "000"

Issued share capital

600,000 ordinary shares sh.20 each 12,000

250,000 redeemable preference shares sh.20 each 5,000

Share premium 400

Goodwill 1,200

Bank overdraft 540

Revaluation reserve 1,000

Net profit for the year 1,440

Retained earnings (1 January 2012) 4,460

General reserves 1,100

Allowance for doubtful debts 48

Interim dividends paid: Ordinary 600

Preference 200

Trade receivables 1,708

Land and Buildings at valuation (cost sh.4,400,000) 18,400

Capital redemption reserve fund 3,000

Fixtures and fittings at cost 3,000

Motor vehicles at cost 7,940

10% debentures 1,600

Accumulated depreciation: Motor vehicles 3,740

Fixtures and fittings 1,500

Trade payables and accruals 960

Short-term investments (market value sh.860,000) 780

Inventory (31 December 2012) 2,960

Additional information

The directors have approved the following:

1. Transfer of sh.500,000 to the general reserve.

2. A 5% final ordinary dividend and final preference dividend on shares issued and outstanding as at 31

December 2012.

3. A bonus issue of 100,000 fully paid ordinary shares from the retained earnings.

Required:

(i) Statement of changes in equity for the year ended 31 December 2012.

(ii) Statement of financial position as at 31 December 2012.

Date posted: September 30, 2022. Answers (1)

- QUESTION TWO

Kate and John formed a partnership business to sell Chinese motorbikes in Mombasa city sharing profits and losses in the ration of 3:1 respectively....(Solved)

QUESTION TWO

Kate and John formed a partnership business to sell Chinese motorbikes in Mombasa city sharing profits and losses in the ration of 3:1 respectively. On 1 April 2012, Kate contributed sh.15,000,000 and John sh.5,000,000 which was immediately deposited in a newly opened bank account of the partnership.

Additional information:

1. Sales proceeds banked during the year amounted to sh.109 million.

2. The cashier had paid the following expenses from sales proceeds before banking the balance:

• Rent of go downs and offices at sh.100,000 per month.

• Office running expenses at sh.10,000 per week.

• Casual wages at sh.4,000 per week.

• Local transport at sh.7,000 per week.

• Partners were allowed to draw salaries per month as follows: Kate sh.30,000 per month.

John sh.36,000 per month.

The partners made all their drawings for the year.

Assume there are 52 weeks in the financial year ended 31 March 2013.

3. The partnership paid the following amounts through the bank:

In Shillings:

Purchase of furniture and fittings 128,000

Purchase of computers 900,000

Staff salaries and wages per month 100,000

Purchases 96,000,000

Drawings (per month):

Kate 100,000

John 80,000

Licenses and clearing charges 1,920,000

Bank charges (per month) 3,000

Telephone per month 8,000

Freight charges 576,000

Electricity bill 10,000

4. Analysis of transactions revealed that:

• Accounts receivable amounting to sh.900,000 were outstanding at the year end.

• Inventory of motorbikes at the year end at cost was sh.8,700,000.

• Included in the inventory of motorbikes above are motorbikes which cost sh.1,100,000 but which can

now be sold for sh.800,000 only, because of impairment in value in the go down.

• The telephone and electricity bills for the month of March 2012 were paid on 3 May 2012.

• Accounts payable for purchases amounting to sh.600,000 were unpaid at the year end.

5. The partners are entitled to 10% interest on their fixed capitals per annum.

6. Depreciation is to be provided on furniture and fittings and computers at the rate of 12.5% and 20% per annum on cost respectively.

Required:

(a) Income statement and profit and loss appropriation account for the year ending 31 March 2013.

(b) Statement of financial position as at 31 March 2013.

Date posted: September 30, 2022. Answers (1)

- Mary Atieno, a sole proprietor, operates a business but does not observe the double entry rule of book-keeping.

The following balances were extracted from her books...(Solved)

Mary Atieno, a sole proprietor, operates a business but does not observe the double entry rule of book-keeping.

The following balances were extracted from her books as at 31 October 2011.

Sh. "000"

10% loan 6,000

Freehold property at cost 6,000

Motor Vehicles (net book value) 7,500

Furniture and Fittings (net book value) 2,400

Trade receivables 5,000

Allowance for doubtful debts 250

Accruals 150

Trade payables 3,800

Bank overdraft 600

Inventory 3,900

The following transactions relate to the financial year ended 31 October 2012

1. Discounts received and discount allowed amounted to sh.400,000 and sh.700,000 respectively.

2. Bad debts of sh.200,000 were written off. The allowance for doubtful debts is to be maintained at 5% of the trade receivables at the end of the financial year.

3. The following transactions were processed through the bank account.

Sh. "000"

• Cash sales 7,200

• Cash purchases 2,400

• Proceeds from the sale of a motor vehicle 1,200

• Collection from trade receivables 18,900

• Payment to suppliers 19,400

• Loan repayments (30 April 2012) 1,000

• Purchase of furniture 2,000

• Drawings 600

• Interest on loan 300

• General expenses 350

• Electricity expenses 650

• Salaries and wages 1,600

4. The business makes a normal gross profit margin of 25% on selling price.

5. Motor vehicles are depreciated at the rate of 20% per annum on a reducing balance basis. A full year’s

depreciation was provided on a motor vehicle which was disposed of in the course of the year. The motor

vehicle had been bought at sh.2,500,000 and had am accumulated depreciation of sh.1,220,000 at the time of

disposal.

6. Furniture is depreciated at the rate of 10% per annum on cost effective from the date of purchase. The

additional furniture was purchased on 1 May 2012 while the cost of the furniture at the beginning of the year

was sh.4,000,000.

7. Sales and purchases were all on credit and amounted to sh.20,800,000 and sh.19,000,000 respectively.

8. Accrued electricity expenses as at 31 October 2012 amounted to sh.190,000

Required:

(a) Income statement for the year ended 31 October 2012.

(b) Statement of financial position as at 31 October 2012.

Date posted: September 30, 2022. Answers (1)

- Explain four considerations that management should take into account in choosing the basis of cost apportionment.(Solved)

Explain four considerations that management should take into account in choosing the basis of cost apportionment.

Date posted: May 16, 2019. Answers (1)

- In relation to a manufacturing concern, Explain the term "cost apportionment".(Solved)

In relation to a manufacturing concern, Explain the term "cost apportionment".

Date posted: May 16, 2019. Answers (1)

- Outline two advantages of an income and expenditure account as compared to a receipts and

payments account.(Solved)

Outline two advantages of an income and expenditure account as compared to a receipts and

payments account.

Date posted: May 16, 2019. Answers (1)

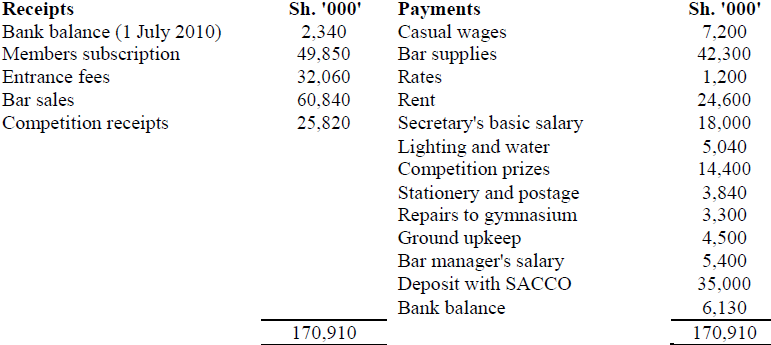

- The following is the summary of the cashbook of Mbedodo Football Club for the year ended 30 June

2011:

Additional information:

1. The assets of the club on...(Solved)

The following is the summary of the cashbook of Mbedodo Football Club for the year ended 30 June

2011:

Additional information:

1. The assets of the club on 1 July 2010 were as follows:

Sh. '000'

Land 650,000

Gymnasium and equipment 250,000

Bar inventory 10,800

Prizes in hand 4,800

2. Bar supplies owing amounted to Sh. 4,200,000 on 1 July 2010

3. On 30 June 2011 the bar inventory was Sh. 9,600,000, prizes in hand - Sh. 2,400,00 and

Sh. 5,640,000 was owing for bar supplies.

4. The secretary is to receive a leave allowance of 5% of his basic salary. It was also agreed that

the bar manager should receive aSh. 500,000 bonus for increased sales during the year.

5. From the register of members, it appeared that unpaid subscriptions as at 30 June 2011

totaled Sh. 5,100,000. Subscriptions received during the year included Sh. 2,550,000 in

respect of the previous year and Sh. 1,700,000 in respect of the year starting 1 July 2011.

6. Interest earned on the deposit with the SACCO for the year ended 30 June 2011 amounted to Sh.

1,750,000

7. The rent paid was for fifteen months up to 30th September 2011

8. The gymnasium and equipment are to be depreciated at the rate of 10% per annum on straight

line basis

Required;-

a) Income and expenditure account for the year ended 30 June 2011

b) Statement of financial position as at 30 June 2011

Date posted: May 16, 2019. Answers (1)

- Differentiate between "receipts and payments account" and "income and expenditure account".(Solved)

Differentiate between "receipts and payments account" and "income and expenditure account".

Date posted: May 16, 2019. Answers (1)

- Explain three reasons why in many organisations the cash flow for a given period differs from the

profit realised by the organisation in the same period.(Solved)

Explain three reasons why in many organisations the cash flow for a given period differs from the

profit realised by the organisation in the same period.

Date posted: May 16, 2019. Answers (1)

- Discuss three categories of financial ratios(Solved)

Discuss three categories of financial ratios

Date posted: May 16, 2019. Answers (1)

- Summarise three limitations of ratio analysis.(Solved)

Summarise three limitations of ratio analysis.

Date posted: May 16, 2019. Answers (1)

- Highlight six purposes of public sector accounting.(Solved)

Highlight six purposes of public sector accounting.

Date posted: May 16, 2019. Answers (1)

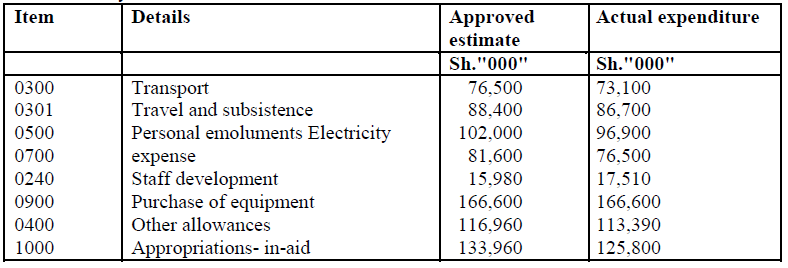

- The following were the approved estimates and actual expenditure for the Ministry of health for

the financial year ended 30 June 2013:

Drawings from the Exchequer during...(Solved)

The following were the approved estimates and actual expenditure for the Ministry of health for

the financial year ended 30 June 2013:

Drawings from the Exchequer during the financial year ended 30 June 2013 amounted to

Sh.127, 500,000.

Required:

(i) General account of vote.

(ii) Exchequer account.

(iii) Paymaster general account.

Date posted: May 16, 2019. Answers (1)

- Uzuri County Council authorised the construction of a city hall on 1 July 2012. The hall was

expected to cost Sh. 160,000,000. The project was to...(Solved)

Uzuri County Council authorised the construction of a city hall on 1 July 2012. The hall was

expected to cost Sh. 160,000,000. The project was to be financed as follows:

Sh. 80,000,000 from a 6.5% bond issue.

Sh. 64,000,000 from a government grant.

Sh. l6,000,000 from the general fund.

The following transactions and events took place during the year ended 30 June 2013:

1. The county council transferred Sh. 16,000,000 from the general fund to the city hall capital

fund. The capital project fund was for the purpose of construction of the city hall.

2. Planning and architects fees amounting to Sh.6,400,000 were paid.

3. The contract was awarded for Sh. 152, 000,000.

4. The 6.5% bonds were sold for Sh. 80,320,000 and the amount of the premium transferred to

the debt service fund.

5. The contract was certified 50% complete and an invoice for Sh.76,000,000 was received from

the contractor.

The contractor was paid the invoiced amount less 10% retention

Required:

i) Journal entries to record the above transactions.

ii) Statement of revenue and expenditure of the capital project fund for the year ended 30 June

2013.

iii) Statement of financial position of the capital project fund as at 30 June 2013.

Date posted: May 16, 2019. Answers (1)

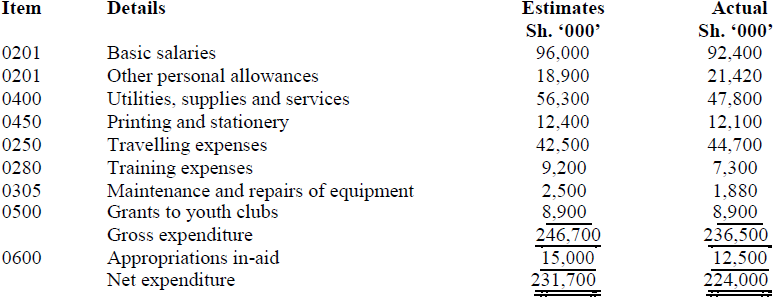

- The following were the estimates and actual expenditure of Barani Ministry of Youth and Sports for

the financial year ended 30 June 2012.

Drawings from the exchequer...(Solved)

The following were the estimates and actual expenditure of Barani Ministry of Youth and Sports for

the financial year ended 30 June 2012.

Drawings from the exchequer during the financial year ended 30 June 2012 amounted to

Sh.226,000,000

Required;

a) General account of vote

b) Exchequer account

c) Paymaster general (PMG) account

d) Appropriation account for the year ended 30 June 2012

e) Statement of assets and liabilities as at 30 June 2012

Date posted: May 16, 2019. Answers (1)

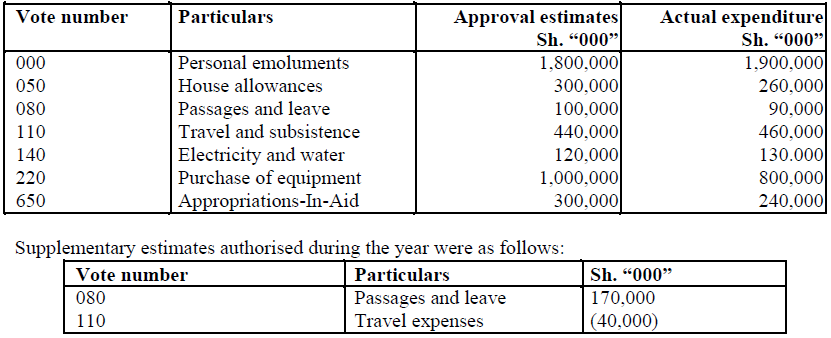

- The following details relate to the approved estimates and actual expenditure of a certain

government ministry for the financial year ended June 2012.

Required;-

Appropriation account for the...(Solved)

The following details relate to the approved estimates and actual expenditure of a certain

government ministry for the financial year ended June 2012.

Required;-

Appropriation account for the year ended 30 June 2012.

Date posted: May 16, 2019. Answers (1)

- Explain the following terms in the context of public sector accounting:

i) Commitment accounting

ii) Fund accounting(Solved)

Explain the following terms in the context of public sector accounting:

i) Commitment accounting

ii) Fund accounting

Date posted: May 16, 2019. Answers (1)