State objectives of budgetary planning and control systems

- To ensure that management plans ahead so that long term goals are achieved.

- To establish a basis for internal audit regularly evaluating departmental results

- To allow people to participate in setting of budgets thereby have a motivational impact on

the workforce

- To provide a yardstick against which the performance of the firm can be evaluated

- To make people more responsible for items of cost and revenue

- To identify areas of efficiency and inefficiency. Variance analysis will prompt remedial

action where necessary.

- To ensure communication is increased throughout the firm and co-ordination improved.

marto answered the question on February 26, 2019 at 05:58

-

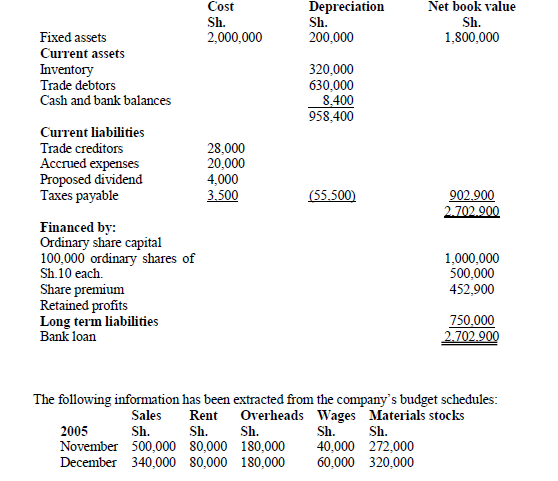

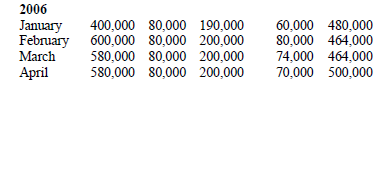

Mavuno Ltd. is a small scale company that specializes in the production of farm tools.

The company uses budgets for planning and controlling its activities. Currently...

(Solved)

Mavuno Ltd. is a small scale company that specializes in the production of farm tools.

The company uses budgets for planning and controlling its activities. Currently the management are

preparing budgets for the three months ending 31 March 2006.

The projected balance sheet as at 31 December 2005 is shown below:

Additional information:

1. The company sells the farm tools at a mark up of 25 %.

2. Purchase of materials stocks is on credit and it is paid for in the month of receipt by the

company

3. Employees are paid wages at the end of every week with the earnings of the last week of the

month being settled in the following month (Assume one month has 4 weeks).

4. Sales commission is paid on month in arrears at the rate of 1% of sales.

5. Overheads include a monthly depreciation charge of Sh. 25,000.

6. 25% of the sales are on cash basis. The other 75% is receivable two months after the sale.

7. The company will receive a loan of Sh.2, 500,000 in the month of March 2006 from Wakulima

Bank.

8. Old equipment will be sold for sh.250, 000 in February 2006 and new equipment will be

purchased at Sh.1, 200,000 to replace the old equipment sold. The new equipment will be paid

for in month of March 2006.

9. Rent is paid for quarterly in advance in the months of January, April, July and October

Required:

(a) Cash budget for the three months ending 31 March 2006.

(b) Budgeted trading profit and loss account for the three months ending 31 March 2006

(c) Budgeted balance sheet as at 31 March 2006.

Date posted:

February 26, 2019

.

Answers (1)

-

Distinguish between the following sets of terms:-

i) Budgetary slack an principal budget factor

ii) Pudding the budget and rolling budget

(Solved)

Distinguish between the following sets of terms:-

i) Budgetary slack an principal budget factor

ii) Pudding the budget and rolling budget

Date posted:

February 26, 2019

.

Answers (1)

-

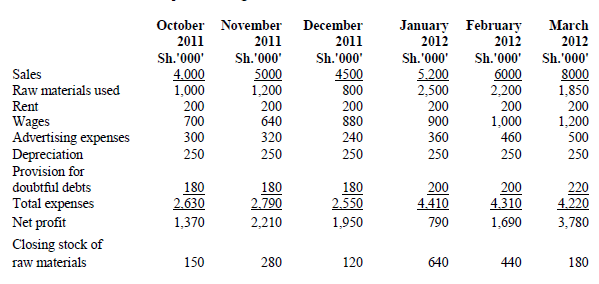

Bright Retailers Ltd. operates a budgetary control system. The following is the company's profit

forecast for the six months period ending 31 March 2012:

(Solved)

Bright Retailers Ltd. operates a budgetary control system. The following is the company's profit

forecast for the six months period ending 31 March 2012:

Additional information:

1. 25%, of the sales are on cash basis. The balance is receivable three months after the month of

sale.

2. A generator worth Sh.600,000 was procured in September 2011. The supplier would install and

test the generator for three months whereas the payment will be made in January 2012.

3. Payment for raw materials is made to suppliers two months after delivery.

4. A dividend of Sh.900,000 will be paid in December 2011.

5. Rent for three months is payable in advance on the first day of each quarter.

6. Advertising expenses are paid three months in arrears.

7. 75% of the wages are paid in the month they are incurred with the balance being paid in the

following month.

8. The company's cost accountant estimates the closing cash balance for the quarter ending

December 2011 to be Sh.1 million.

Required:

A cash budget for the quarter ending 31 March 2012

Date posted:

February 25, 2019

.

Answers (1)

-

Explain five factors to consider when preparing a sales forecast for a cash budget.

(Solved)

Explain five factors to consider when preparing a sales forecast for a cash budget.

Date posted:

February 22, 2019

.

Answers (1)

-

Outline three differences between budgets and standards.

(Solved)

Outline three differences between budgets and standards.

Date posted:

February 22, 2019

.

Answers (1)

-

Differentiate between the following types of budgets

i) Functional budget and master budget.

ii) Rolling budget and incremental budget.

(Solved)

Differentiate between the following types of budgets

i) Functional budget and master budget.

ii) Rolling budget and incremental budget.

Date posted:

February 22, 2019

.

Answers (1)

-

XYZ Ltd. Carries on its business in Nairobi. The company has been reporting its profits using

absorption costing system. During the financial year ended 30 September...

(Solved)

XYZ Ltd. Carries on its business in Nairobi. The company has been reporting its profits using

absorption costing system. During the financial year ended 30 September 2005, the following

summary statement was provided:

Date posted:

February 22, 2019

.

Answers (1)

-

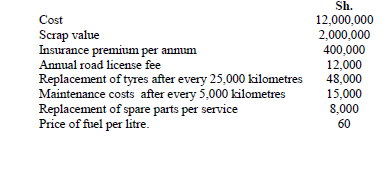

Jogi Transporters operate in the transport industry. On 1 December 2005, the management

acquired a new lorry to meet customer needs and cater for the increase...

(Solved)

Jogi Transporters operate in the transport industry. On 1 December 2005, the management

acquired a new lorry to meet customer needs and cater for the increase in business volume.

The following information relates to the initial and maintenance cost of the lorry.

Additional information:

1. The lorry has an economic life of 4 years.

2. The lorry has 6 tyres after each costing Sh.8000

3. Service is carried out after every 5,000 kilometres.

4. On average the lorry covers 20 kilometres per litre of fuel consumed.

5. The lorry is projected to cover 100,000 kilometres in January 2006, 25,000 kilometres in

Required:

Prepare a schedule for the three months showing

i. Variable costs per kilometer

ii. Fixed costs per kilometer

iii. Total costs per kilometer

c) Fixed costs are actually variable cost

With reference to (b) above explain whether you agree or disagree with the statement.

February 2006 and 50,000 kilometres in March 2006.

Date posted:

February 22, 2019

.

Answers (1)

-

State the limitations of break – even analysis.

(Solved)

State the limitations of break – even analysis.

Date posted:

February 22, 2019

.

Answers (1)

-

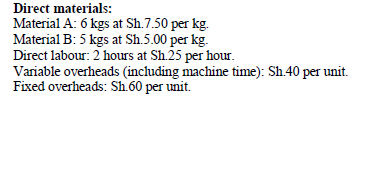

ABC limited manufactures and sells a single product branded “Zed”. The following data has been

extracted from the budgets and standard costs to product “Zed”.

(Solved)

ABC limited manufactures and sells a single product branded 'Zed'. The following data has been

extracted from the budgets and standard costs to product 'Zed'.

Date posted:

February 22, 2019

.

Answers (1)

-

Highlight six limitations of cost-volume-profit analysis.

(Solved)

Highlight six limitations of cost-volume-profit analysis.

Date posted:

February 22, 2019

.

Answers (1)

-

Describe the difference between the accountant's and the economist's model of cost-volume profit

analysis.

(Solved)

Describe the difference between the accountant's and the economist's model of cost-volume profit

analysis.

Date posted:

February 22, 2019

.

Answers (1)

-

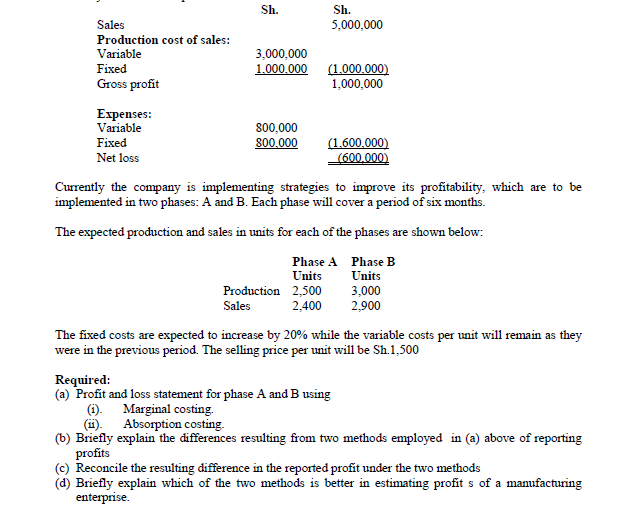

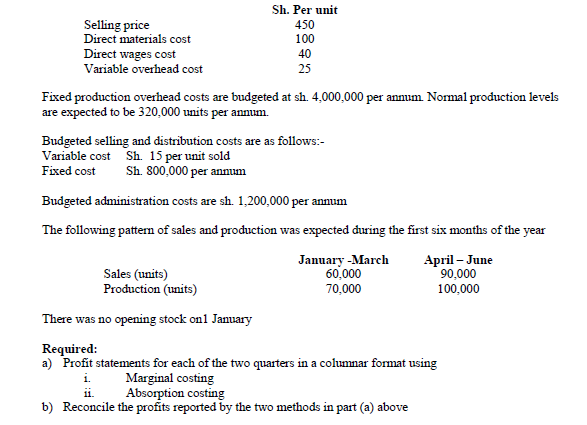

Tec Ltd. manufactures a single product branded 'Zed' for sale on the local and international

market.

The cost structure per unit of product 'Zed' is as follows:

(Solved)

Tec Ltd. manufactures a single product branded 'Zed' for sale on the local and international

market.

The cost structure per unit of product "'zed' is as follows:

Additional information:

1. The current sales level for the company amounts to Sh. 800,000.

2. The fixed overheads per unit have been calculated based on the current sales level of 4,000

units.

Required:

i) Sales price per unit.

ii) Current profit or loss.

iii) Break even point in units and shillings.

iv) Suggest four measures that could be taken to improve the current profit position

Date posted:

February 21, 2019

.

Answers (1)

-

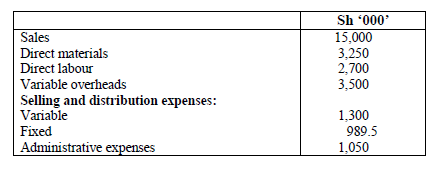

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

(Solved)

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

Date posted:

February 21, 2019

.

Answers (1)

-

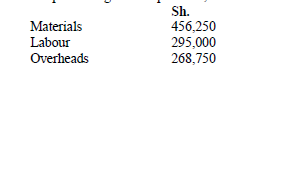

Jitegemee limited company uses a process costing system in its operation. In one of the production processes, two joint products A and B and a...

(Solved)

Jitegemee limited company uses a process costing system in its operation. In one of the

production processes, two joint products A and B and a by-product C are produced

The following additional information is provided:

1. Each processing run requires 12,500 kilograms of output.the costs incurred are as follow:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

Date posted:

February 21, 2019

.

Answers (1)

-

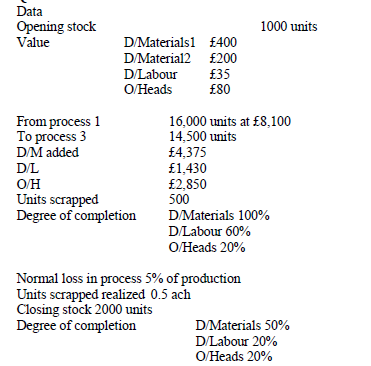

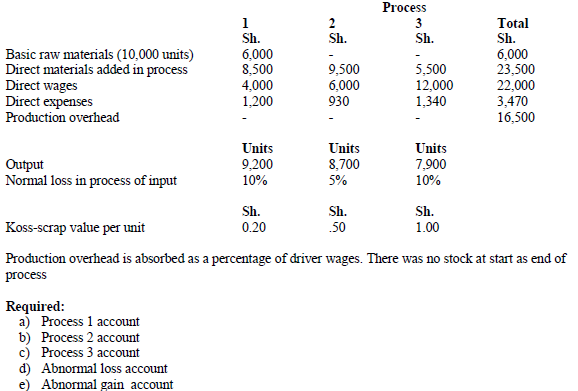

The following information is obtained in respect of process 2 of the month of September;

(Solved)

The following information is obtained in respect of process 2 of the month of September;

There was a normal loss in the process of 10% of production units' scrapped realized sh. 50 per unit,

use FIFO method

Required:

i. Statement of production

ii. Statement of cost and evaluation

iii. Process account

iv. Abnormal loss / gain account

Date posted:

February 21, 2019

.

Answers (1)

-

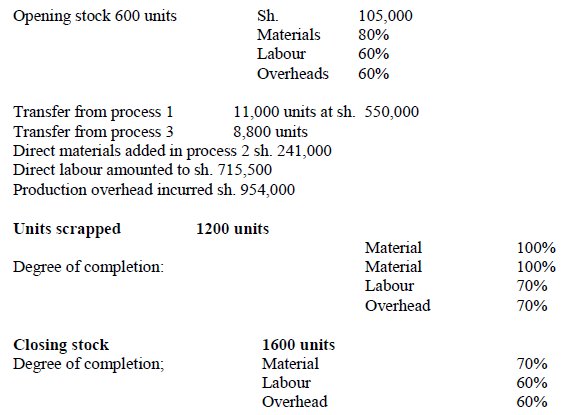

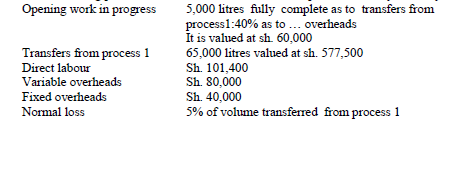

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

(Solved)

Required:

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

Date posted:

February 21, 2019

.

Answers (1)

-

Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information...

(Solved)

Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information was extracted from the books of the company for the month of October.

Date posted:

February 21, 2019

.

Answers (1)

-

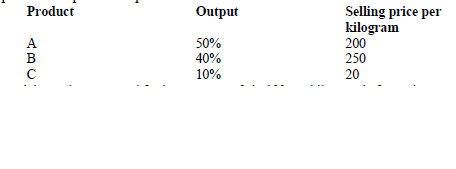

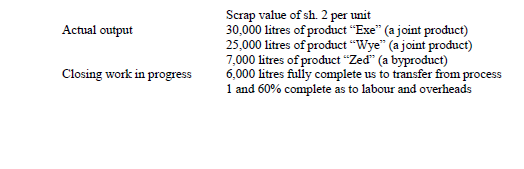

The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed

(Solved)

The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed

Additional information;-

1. The final selling prices per litre of products Exe, Wye and Zed are shs.15, shs.18 and shs.4

respectively.

2. There are no further costs associated with by product Zed

3. Product Wye requires further processing at a cost of sh. 1.50 per litre

4. All the three products incur packaging costs of sh. 0.50 per litre before they are sold.

Required:

i) Calculate the number of equivalent units produced

ii) Calculate the costs of products Exe and Wye

iii) Apportion the common costs to joint products based on sales at the point of separation

iv) Prepare process II account for the month of January 2008

Date posted:

February 21, 2019

.

Answers (1)

-

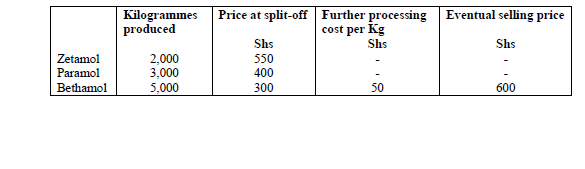

Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material...

(Solved)

Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material nat a cost of sh.2,500,000 and incurred joint conversion costs of

sh.700,000.Sales and production information for the month of January wered as follows;

Zetamol and Paramol are sold to other pharmaceutical companies at the split off point. Bethamol can

be sold at the split off point or processed further and packaged for sale as an asthma medication.

Required

Allocate the joint costs to the three products using;

i) The physical units sold

ii) The sales value at split off method

iii) The net realizable value method

iv) Suppose that half the production of Paramol could be purified and mixed with all the

production of Zetamol to yield parazetamol.All further processing costs amount to

sh.350,000.The selling price for parazetamol is sh.1,120 per kilogramme.Advise the company

on whether to further process Zetamol into 2,000 kilogrammes of parazetamol.

Date posted:

February 21, 2019

.

Answers (1)