Get premium membership

Get premium membership and access questions with answers, video lessons as well as revision papers.

1. Variable Overhead Variances

- This is the difference between the standard variable overhead cost for the production achieved and the actual variable overhead incurred. In other words, this is the difference between the actual variable overheads incurred and the variable overheads absorbed. This variance is simply the over or under absorption of overheads. This is the sum of variable overhead expenditure variance and variable overhead efficiency variance.

(a) Variable Overhead Expenditure Variance

This is the difference between the actual overheads incurred and the allowed variable overheads based on the actual hours worked. It is calculated as under:-

Actual variable overhead – V.O.A.R x Actual labour hours

Where: V.O.A.R = Variable overhead absorption rate. This variance may arise due to rise or fall in overhead expenditure as a result of some unexpected changes.

(b) Variable Overhead Efficiency Variance

This is the difference between the allowed variable overheads and the absorbed variable overhead. It is calculated as under:-

V.O.A.R (Actual hours – Standard hours)

The main cause of this variance is the difference between actual hours and standard hours

2. Fixed Overhead Variances

- This is the difference between the standard cost of fixed overhead absorbed in the production achieved, whether completed or not and the fixed overhead attributed and charged to that period. This simply represents under or over absorption. This is the sum of fixed overhead expenditure variance and fixed overhead volume variance.

(a) Fixed overhead expenditure variance

- This is the difference between the budget cost allowances for production for a specified control period and the actual fixed expenditure attributed and charged to that period. It is calculated as under:

Actual expenditure – Budgeted expenditure

(b) Fixed overhead volume variance

- This is that portion of the fixed production overhead variance which is the difference between the standard cost absorbed in the production achieved, whether completed or not, and the budget cost allowance for a specified control period. This is the sum of fixed overhead efficiency variance and fixed overhead capacity variance. It is calculated as under:-

Standard cost (Actual production – Budget production) per unit.

- The main cause of this variance is the difference between actual level of production and budgeted production.

(c) Fixed overhead efficiency variance

This is that portion of the fixed production overhead volume variance which is the difference between the standard cost absorbed in the production achieved, whether completed or not, and the actual labour hours worked, valued at the standard hourly absorption rate. It is calculated as under.

=F.O.A.R. (Actual hours – Standard hours) Or

=Standard cost per unit (Actual quantity – Standard quantity)

Where: F.O.A.R. = Fixed overhead absorption rate.

(d) Fixed Overhead Capacity Variance

- This is that portion of the fixed production overhead volume variance which is due to working ad higher or lower capacity than standard. Capacity is often expressed in terms of average direct labour hours per day, and the variance is the difference between the budget cost allowance and the actual labour hours worked, valued at the standard hourly absorption rate. It is calculated as under:-

= F.O.A.R. (Actual hours – budgeted hours) or

= Standard cost per unit(Budgeted production-Standard production)

3. Sales Margin Variance

The standard sales margin is the difference between the standard selling price of a product and its standard cost. It is also known as the standard profit for the product. Total sales margin variance is the difference between the budgeted margin from sales and the actual margin when the cost of sales is valued at the standard cost of production. This is the sum of sales margin price variance and sales margin quantity variance.

(a) Sales margin price variance

This is that portion of the total sales margin variance which the difference between the standard margin per unit and the actual margin per unit fo te number of units sold in the period. It is calculated as under:-

Actual sales – (Standard selling price x Actual sales quantity)

(b) Sales Margin Quantity Variance

This is that portion of the total sales margin variance which is the difference between the budgeted number of units sold and the actual number sold valued at the standard margin per unit. It is calculated as under:-

=Standard sales margin(Actual sales quantity-Budgeted sales quantity)

Or profit

Wilfykil answered the question on August 7, 2019 at 05:30

- Discuss on Labour Cost Variances(Solved)

Discuss on Labour Cost Variances

Date posted: August 6, 2019. Answers (1)

- Explain Material Cost Variance(Solved)

Explain Material Cost Variance

Date posted: August 6, 2019. Answers (1)

- Illustrate the Structure of variances(Solved)

Illustrate the Structure of variances

Date posted: August 6, 2019. Answers (1)

- Explain the establishment of standards or Setting standards(Solved)

Explain the establishment of standards or Setting standards

Date posted: August 6, 2019. Answers (1)

- Which factors must be considered in standard costing?(Solved)

Which factors must be considered in standard costing?

Date posted: August 6, 2019. Answers (1)

- Discuss the Types of standards in the cost accounting context(Solved)

Discuss the Types of standards in the cost accounting context

Date posted: August 6, 2019. Answers (1)

- Show the difference between Historical cost and Standard cost(Solved)

Show the difference between Historical cost and Standard cost

Date posted: August 6, 2019. Answers (1)

- Compare and contrast on Budgetary Control and Standard Costing(Solved)

Compare and contrast on Budgetary Control and Standard Costing

Date posted: August 6, 2019. Answers (1)

- Define the term Standard costing(Solved)

Define the term Standard costing

Date posted: August 6, 2019. Answers (1)

- What does Standard Costing involve?(Solved)

What does Standard Costing involve?

Date posted: August 6, 2019. Answers (1)

- During a period 3000 units of a main product were produced at sh 60 per unit. (Solved)

During a period 3000 units of a main product were produced at sh 60 per unit. Total production were sh 125000. A by product was produced together with main product. This by-product was 100 units and it was sold for sh 55 per unit post separation cost of this by product were sh 500. Calculate the production cost and profit of the main product.

Date posted: August 6, 2019. Answers (1)

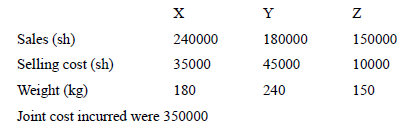

- The following data relates to three products XYZ(Solved)

The following data relates to three products XYZ

Required:

Calculate profit made by each product apportioning joint costs on;

i) Sales value bases

ii) Physical unit bases

Date posted: August 6, 2019. Answers (1)

- In a specific period production and cost data was as follows:(Solved)

In a specific period production and cost data was as follows: Production was 1,600 full complete units and 400 partly complete units. The degree of completion of the 400 units WIP was as follows:

Required:

a) Calculate total equivalent unit

b) Cost per unit of complete units

c) Show the value of W.I.P

Date posted: August 6, 2019. Answers (1)

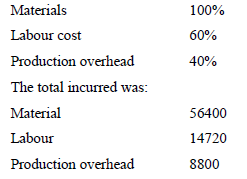

- Using the data given below, show process 1 account where normal loss has a scrap value of sh1.8 per kilo.(Solved)

Using the data given below, show process 1 account where normal loss has a scrap value of sh1.8 per kilo.

In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1. Labour cost amounted to sh 3,000 and production overheads sh 2,300, normal loss has been estimated at 10% . The actual product after process was 1750kg.

Date posted: August 6, 2019. Answers (1)

- In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1.(Solved)

In the manufacture of product vitality 2000 kgs of material at kshs 5kg were supplied to process 1. Labour cost amounted to sh 3,000 and production overheads sh 2,300, normal loss has been estimated at 10% . The actual product after process was 1750kg.

Required: Prepare process 1 account

Date posted: August 6, 2019. Answers (1)

- What is meant by Process loss scrap and waste?(Solved)

What is meant by Process loss scrap and waste?

Date posted: August 6, 2019. Answers (1)

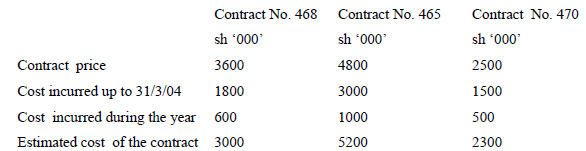

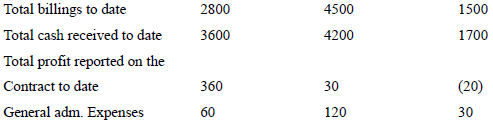

- Njenga Limited is a construction Co. whose financial year end is 31st March.(Solved)

Njenga Limited is a construction Co. whose financial year end is 31st March. The information provided was extracted from the books of the company in contraction with three construction contracts undertaken by the company during the financial year ended 31st March 2005

Required:

Using the percentage of completing method of accounting for long term construction contract:

1. Calculate profit/less realized on each contract for the year ended 31st March 2005.

2. Prepare profit and loss extract for each contract for year ended 31st March 2005.

3. Prepare balance sheet extract as at 31st March 2005.

Date posted: August 6, 2019. Answers (1)

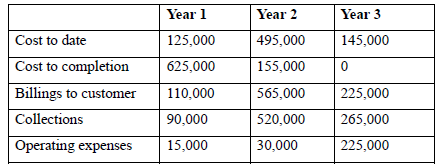

- A small bridge is to be constructed by the beginning of the year at a fixed price of sh 900,000 with estimates contract cost of...(Solved)

A small bridge is to be constructed by the beginning of the year at a fixed price of sh 900,000 with estimates contract cost of sh 750,000 in year one. The following summaries are presented:

Required:

a) Prepare a statement showing the profit recognized in each year.

b) Balance sheet extract.

c) Journal entries to account for the extraction

Date posted: August 6, 2019. Answers (1)

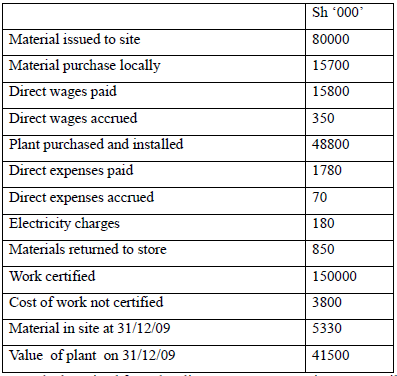

- HZ Construction Company acquired a contact for the construction of a dual carriage way from Nairobi at cost of 200 million.(Solved)

HZ Construction Company acquired a contact for the construction of a dual carriage way from Nairobi at cost of 200 million. The data relating to the contract for year ended 31st December 2009 was as follows:

The company had received from the client payment amounting to 126 million.

Required:

(i) Contract account

(ii) Contractee account

(iii) Balance sheets extract showing work in progress.

Date posted: August 6, 2019. Answers (1)

- Give and explain cases where job costing is applied(Solved)

Give and explain cases where job costing is applied

Date posted: August 6, 2019. Answers (1)