-

Disadvantages of scheme of work

Date posted:

December 15, 2021

-

Advantages of scheme of work

Date posted:

December 15, 2021

-

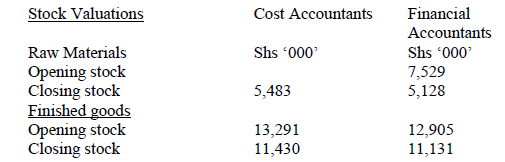

The profit shown in the financial accounts of MRM Co Ltd for the year ended 31st December 2002 is Shs 18,592,000. The cost accounts for the same period reflected a profit of Shs 20,496,000. Comparison of the two set of accounts revealed the following:

Dividends and interests received of Shs 500,000 and Shs 52,000 respectively were reflected in the

financial accounts. The company disposed a production machine costing Shs 5 million for Shs 0.25

million. It had been depreciated to the extent of Shs 3 million.

Required;

Prepare reconciliation for the cost and financial profits for the period.

Dividends and interests received of Shs 500,000 and Shs 52,000 respectively were reflected in the

financial accounts. The company disposed a production machine costing Shs 5 million for Shs 0.25

million. It had been depreciated to the extent of Shs 3 million.

Required;

Prepare reconciliation for the cost and financial profits for the period.

Date posted:

December 15, 2021

-

Distinguish between valuation of assets based on current cost and historical cost.

Date posted:

December 15, 2021

-

Explain the financial and non-financial performances measures used by business organizations.

Date posted:

December 15, 2021

-

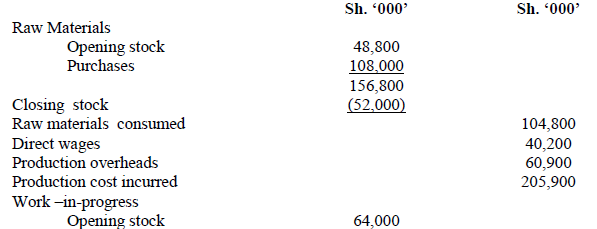

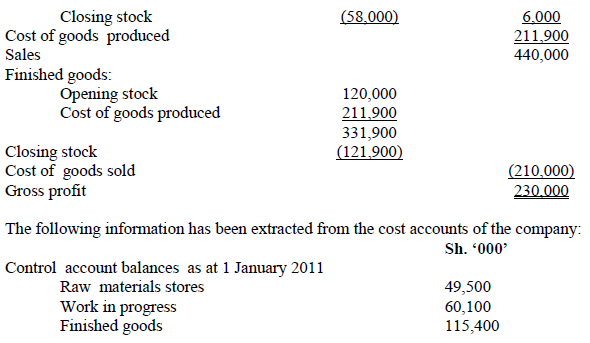

Takers Limited operates separate cost accounting and financial accounting systems. The following manufacturing and trading statement has been extracted from the company's financial accounts for the quarter ended 31 march 2011

Additional information:

1. The cost accounts indicated that raw materials issued during the quarter ended 31 March 2011

amounted to sh. 104,800,000

2. As per the cost accounts cost of goods produced and cost of goods sold amounted to sh.

222,500,000 and sh. 212,100,000 respectively

3. Raw materials lost through floods amounted to sh, 2,400,000 Insurance claim for these raw

materials is pending

This claim was reflected in the cost accounts

4. A notional rent of sh. 4,000,000 per month has been charged in the cost accounts

5. Production overheads were absorbed at the rate of 185% of direct wages

Required:

a) Prepare the following control accounts in the cost ledger

i. Raw materials stores

ii. Work in progress

iii. Finished goods

iv. Production overhead

b) A statement reconciling the gross profit as per the cost accounts and the gross profit as per the

financial accounts

Additional information:

1. The cost accounts indicated that raw materials issued during the quarter ended 31 March 2011

amounted to sh. 104,800,000

2. As per the cost accounts cost of goods produced and cost of goods sold amounted to sh.

222,500,000 and sh. 212,100,000 respectively

3. Raw materials lost through floods amounted to sh, 2,400,000 Insurance claim for these raw

materials is pending

This claim was reflected in the cost accounts

4. A notional rent of sh. 4,000,000 per month has been charged in the cost accounts

5. Production overheads were absorbed at the rate of 185% of direct wages

Required:

a) Prepare the following control accounts in the cost ledger

i. Raw materials stores

ii. Work in progress

iii. Finished goods

iv. Production overhead

b) A statement reconciling the gross profit as per the cost accounts and the gross profit as per the

financial accounts

Date posted:

December 15, 2021

-

Ushindi Limited manufactures ornaments for export trade. Jobs are allocated to two operators.

Mbotela and Juma with bonus paid for hours saved.

In the month of February 2005, Mbotela made 186 units and Juma made 210 units for which the

time allowed of 30 standard minutes and 25 minutes per unit respectively was credited.

The basic wage rate was Sh.18 per hour for both employees. For every hour saved, a bonus was

paid at 20% of the basic wage rate. Hours worked in excess were paid at the basic wage rate plus

two thirds.

Mbotela completed his job in 44 hours and Juma completed his job in 39 hours.

A basic working week has 40 hours.

Required:

For each operator:

(i). The amount of bonus payable.

(ii). The total gross wage payable.

(iii). The wages cost per unit.

Date posted:

December 15, 2021

-

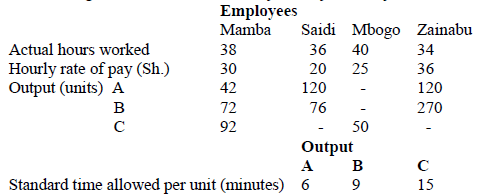

Ardhi company Ltd. Is considering the type of remuneration scheme to adopt for its employees.

The following information is availed to you for your analysis:

For the calculation of piecework earnings the company values each minute at a rate of Sh.0.5

Required:

Calculate the earnings for each employee using

(i). Basic guaranteed hourly rates

(ii). Piece work rates.

(iii). Premium bonus, given that an employee earns the premium bonus at the rate of two thirds of the time saved.

For the calculation of piecework earnings the company values each minute at a rate of Sh.0.5

Required:

Calculate the earnings for each employee using

(i). Basic guaranteed hourly rates

(ii). Piece work rates.

(iii). Premium bonus, given that an employee earns the premium bonus at the rate of two thirds of the time saved.

Date posted:

December 15, 2021

-

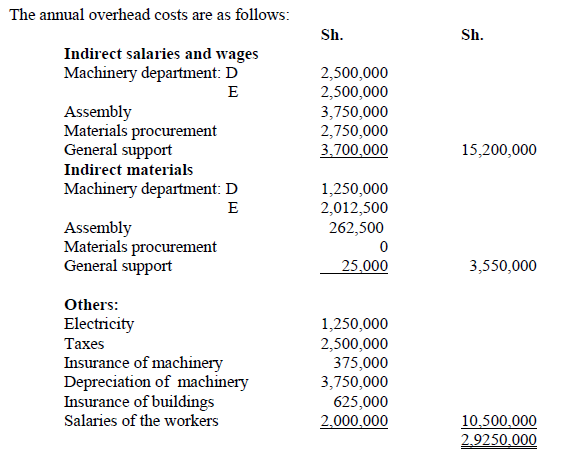

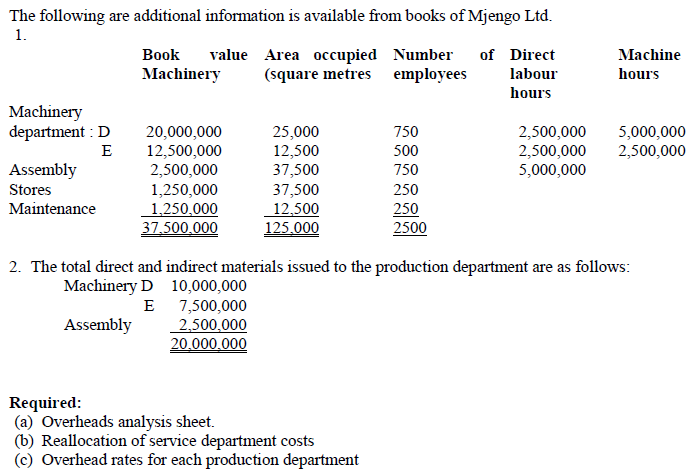

Mjengo Ltd. Is a medium sized company which operates three production departments and two service departments. The three production departments are: Machinery department D, machinery department E and Assembly department.

The two service departments are materials procurement and general support department.

Date posted:

December 15, 2021

-

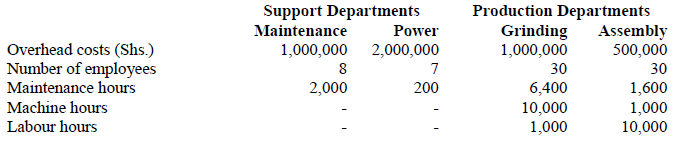

MMC Ltd. produces machine parts on a job-order basis. Majority of the business contracts are obtained through bidding. Business firms competing with MMC Ltd. bid full cost plus 20 per cent mark up. Recently, with the expectation of increase in sales, MMC Ltd. reduced its mark up from 25 per cent to 20 per cent.

The company operates two support departments and two production departments. The budgeted costs and the normal activity levels for each department are given below:

Additional information:

1. The direct costs of the maintenance department are allocated on the basis of employees while

those of power department are allocated on the basis of maintenance hours.

2. Departmental overhead rates are used to assign costs to products. Grinding department uses

machine hours and assembly department uses labour hours.

MMC Ltd. is preparing to bid for a contract, job K, that requires three machine hours per unit

produced in grinding and zero hours in assembly department. The expected prime costs per unit are Shs. 670.

Required:

a) Allocate the support service costs to the production departments using the direct allocation method

b) What will be the bid for job K if the direct allocation method is used?

c) Allocate the service costs to the production departments using the sequential allocation method

d) What will be the bid for job K if the sequential allocation method is used?

e) Briefly explain the problems encountered in setting overhead cost standards.

f) Distinguish between cost allocation and cost apportionment.

Additional information:

1. The direct costs of the maintenance department are allocated on the basis of employees while

those of power department are allocated on the basis of maintenance hours.

2. Departmental overhead rates are used to assign costs to products. Grinding department uses

machine hours and assembly department uses labour hours.

MMC Ltd. is preparing to bid for a contract, job K, that requires three machine hours per unit

produced in grinding and zero hours in assembly department. The expected prime costs per unit are Shs. 670.

Required:

a) Allocate the support service costs to the production departments using the direct allocation method

b) What will be the bid for job K if the direct allocation method is used?

c) Allocate the service costs to the production departments using the sequential allocation method

d) What will be the bid for job K if the sequential allocation method is used?

e) Briefly explain the problems encountered in setting overhead cost standards.

f) Distinguish between cost allocation and cost apportionment.

Date posted:

December 15, 2021

-

Describe the Historical Background of Business Education

Date posted:

December 15, 2021

-

Gopher Ltd has issued 300,000 ordinary shares of £1 each, which are at present selling for £4 per share. The company plans to issue rights to purchase one new equity share at a price of £3.20 per share for every 3 shares held. A shareholder who owns 900 shares thinks that he will suffer a loss in his personal wealth because the new shares are being offered at a price lower than market value. On the assumption that the actual market value of shares will be equal to the theoretical ex-rights price, what would be the effect on the shareholder's wealth if:

(a) He sells all the rights;

(b) He exercises one half of the rights and sells the other half;

(c) He does nothing at all?

Date posted:

December 15, 2021

-

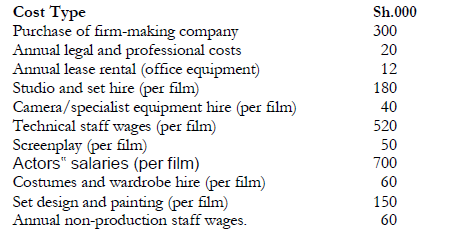

The Independent Film Company plc is a film company which purchases distribution rights on films from small independent producers, and sells the films on to cinema chains for national and international screening. In recent years the company has found it difficult to source sufficient films to maintain profitability. In response to the problem, the Independent Film Company has decided to invest in commissioning and producing films in its own right. In order to gain the expertise for this venture, the Independent Film Company is considering purchasing an existing

filmmaking concern, at a cost of Sh.400,000. The main difficult that is anticipated for the business is the increasing uncertainty as to the potential success/failure rate of independently produced films. Many cinema chains are adopting a policy of only buying films from large international film companies, as they believe that the market for independent films is very limited and specialist in nature. The Independent Film Company is prepared for the fact that they are likely to have more films that fail than that succeed, but believe that the proposed film

production business will nonetheless be profitable.

Using data collection from the existing distribution business and discussions with industry

experts, they have produced cost and revenue forecasts for the five years of operation of the

proposed investment. The company aims to complete the production of three films per year.

The after tax cost of capital for the company is estimated to be 14%.

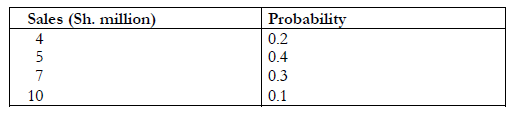

Year 1 sales for the new business are uncertain, but expected to be in the range of Sh.4-10

million. Probability estimates for different forecast values are as follows:

Sales are expected to grow at an annual rate of 5%.

Anticipated costs related to the new business are as follows:

Sales are expected to grow at an annual rate of 5%.

Anticipated costs related to the new business are as follows:

Additional Information

(i) No capital allowances are available.

(ii) Tax is payable one year in arrears, at a rate of 33% and full use can be made of tax

refunds as they fall due.

(iii) Staff wages (technical and non-production staff) and actors‟ salaries, are

expected to rise by 10% per annum.

(iv) Studio hire costs will be subject to an increase of 30% in Year 3.

(v) Screenplay costs per film are expected to rise by 15% per annum due to a shortage of

skilled writers.

(vi) The new business will occupy office accommodation which has to date been let out for

an annual rent of Sh.20,000. Demand for such accommodation is buoyant and the

company anticipates in finding future tenants at the same annual rent.

(vii) A market research survey into the potential for the film production business cost Sh.25,000.

Required:

Using DCF analysis, calculate the expected Net Present Value of the proposed investment.

(Workings should be rounded to the nearest Sh.‟000‟)

Additional Information

(i) No capital allowances are available.

(ii) Tax is payable one year in arrears, at a rate of 33% and full use can be made of tax

refunds as they fall due.

(iii) Staff wages (technical and non-production staff) and actors‟ salaries, are

expected to rise by 10% per annum.

(iv) Studio hire costs will be subject to an increase of 30% in Year 3.

(v) Screenplay costs per film are expected to rise by 15% per annum due to a shortage of

skilled writers.

(vi) The new business will occupy office accommodation which has to date been let out for

an annual rent of Sh.20,000. Demand for such accommodation is buoyant and the

company anticipates in finding future tenants at the same annual rent.

(vii) A market research survey into the potential for the film production business cost Sh.25,000.

Required:

Using DCF analysis, calculate the expected Net Present Value of the proposed investment.

(Workings should be rounded to the nearest Sh.‟000‟)

Date posted:

December 15, 2021

-

Write notes on the following cash management models:

(i) The Baumol model.

(ii) The Miller – Orr model.

Date posted:

December 15, 2021

-

List three advantages to the management of a company for knowing who their shareholders are.

Date posted:

December 15, 2021

-

Describe four non-financial objectives that a company might pursue that have the effect of limiting the achievement of the financial objectives.

Date posted:

December 15, 2021

-

W White’s business has a rate of turnover of 7 times. Average stock is sh12,600. Trade discount (i.e. margin allowed) is 33¼% off all selling prices. Expenses are 66 ¾% of gross profit.

You are to calculate:

(a)Cost of goods sold.

(b)Gross profit margin.

(c)Turnover.

(d)Total expenses.

(e)Net profit.

Date posted:

December 14, 2021

-

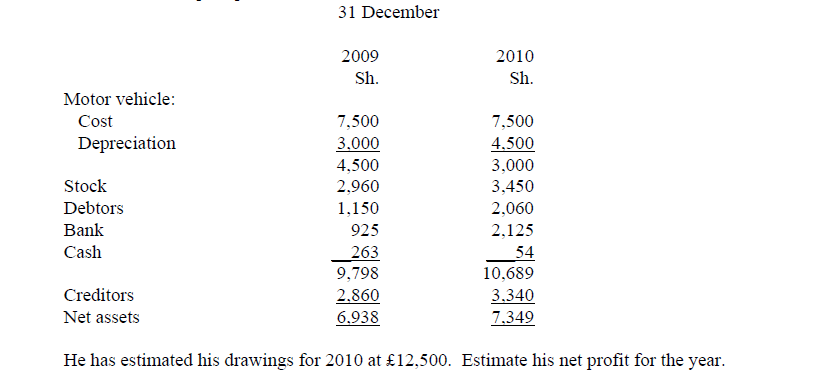

A sole trader’s capital position is as follows

Date posted:

December 14, 2021

-

Approaches in preparing final accounts where there are insufficient records

Date posted:

December 14, 2021

-

Give two reasons for incomplete records in accounting records

Date posted:

December 14, 2021

-

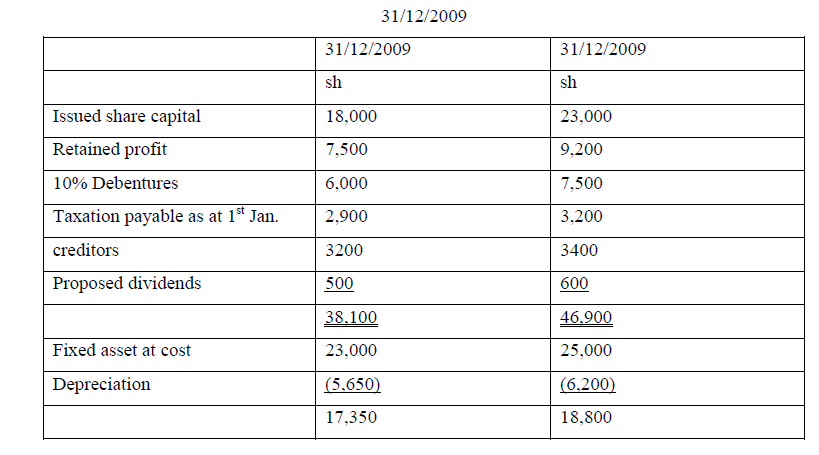

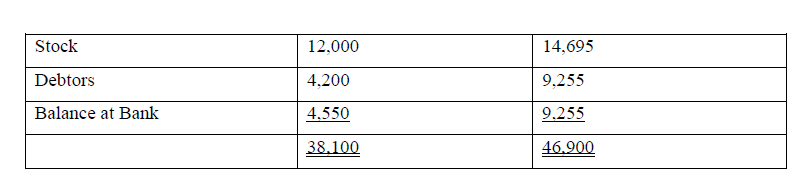

From the following balance sheet, prepare cash flow statement of Abc Ltd for the ended 31/12/2009

Date posted:

December 14, 2021

-

In a company, an agency problem may exist between management and shareholders on one hand and the debt holders (creditors and lenders) on the other because management and shareholders, who own and control the company have the incentive to enter into transactions that may transfer wealth from debt holders to shareholders. Hence the need for agreements by debt holders in lending contracts.

Required:

(a) State and explain any four actions or transactions by management and shareholders that could be harmful to the interests of debt holders (sources of conflict).

(b) Write short notes on any four restrictive covenants that debt holders may use to protect their wealth from management and shareholder raids.

Date posted:

December 14, 2021

-

List and explain five factors that should be taken into account by a businessman in making the choice between financing by short-term and long-term sources.

Date posted:

December 14, 2021

-

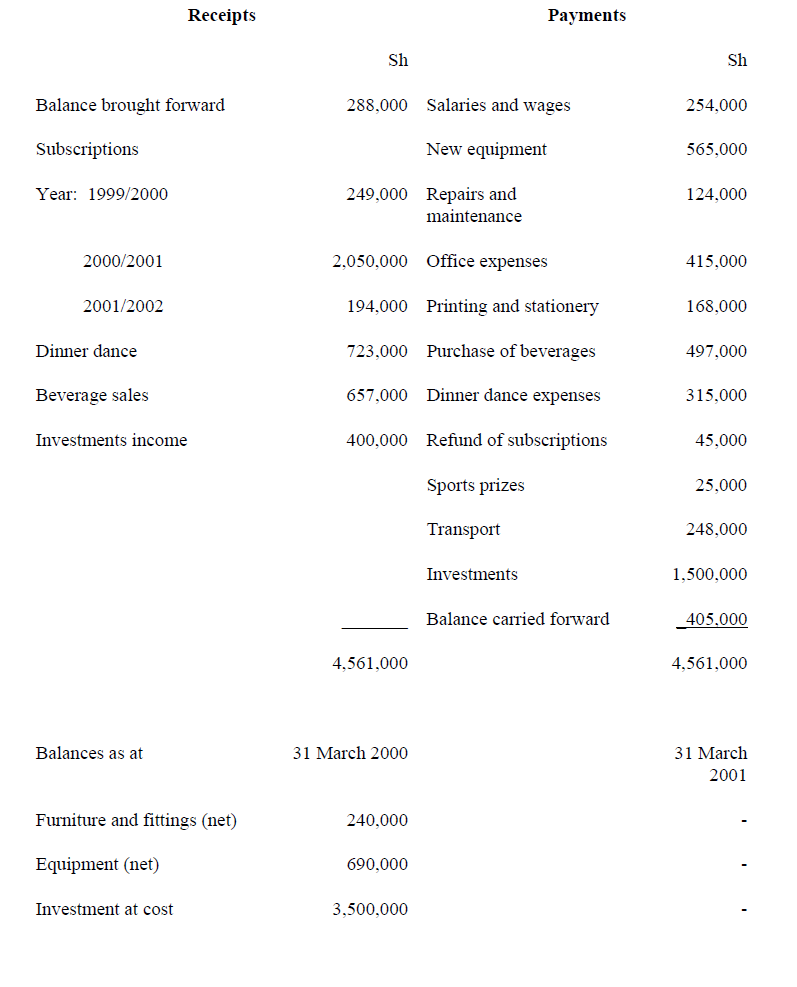

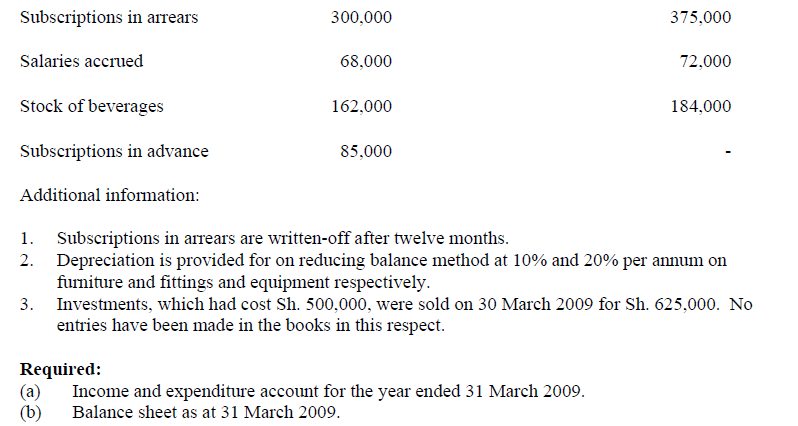

The accountant of Mamba Sports Club has extracted the following information from the books of account for the year ended 31 March 2009

Date posted:

December 14, 2021

-

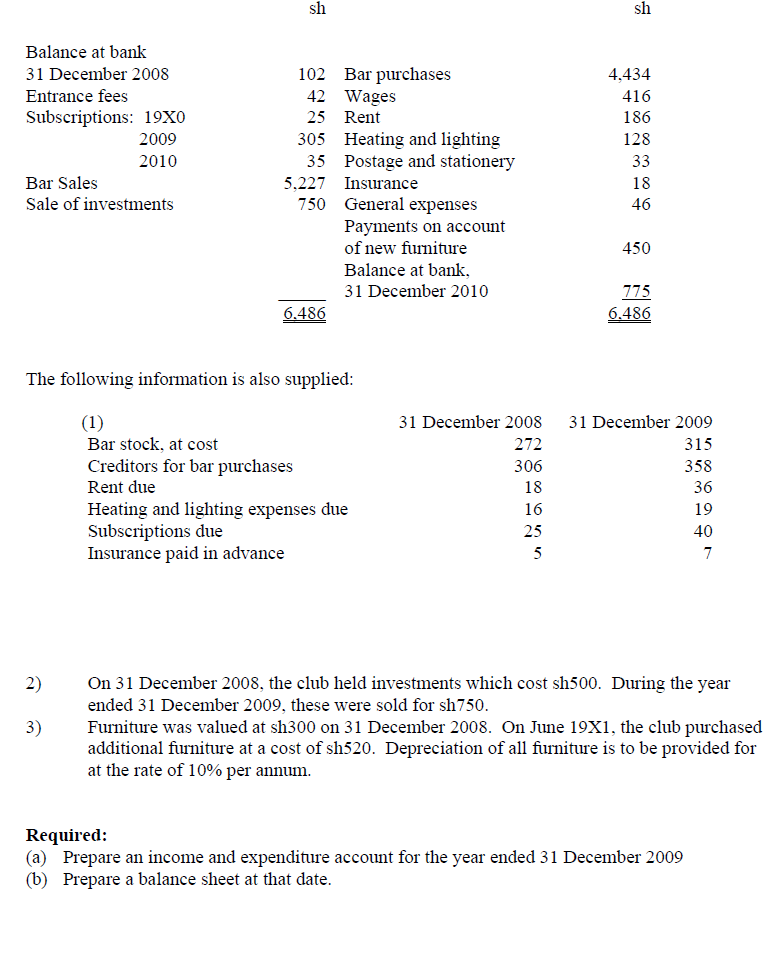

The following is the receipts and payments account of the Friendship Club for the year ended 31 December 2010

a)Prepare an income and expenditure account for the year ended 31 December 2009

(b)Prepare a balance sheet at that date

Date posted:

December 14, 2021

-

Explain the benefits that are enjoyed by investors because of the existence of organized security exchanges.

Date posted:

December 14, 2021

-

The CMA (Capital Markets Authority) has put in place several tax incentives to encourage investments in capital markets.

Highlight some of the tax incentives by the Capital Markets Authority.

Date posted:

December 14, 2021

-

Millennium Investments Ltd. wishes to raise funds amounting to Sh.10 million to finance a project in the following manner:

Sh.6 million from debt; and Sh.4 million from floating new ordinary shares.

The present capital structure of the company is made up as follows:

1. 600,000 fully paid ordinary shares of Sh.10 each

2. Retained earnings of Sh.4 million

3. 200,000, 10% preference shares of Sh.20 each.

4. 40,000 6% long term debentures of Sh.150 each.

The current market value of the company's ordinary shares is Sh.60 per share.

The expected ordinary share dividends in a year's time is Sh.2.40 per share.

The average growth rate in both dividends and earnings has been 10% over the past ten

years and this growth rate is expected to be maintained in the foreseeable future.

The company's long term debentures currently change hands for Sh.100

each. The debentures will mature in 100 years. The preference shares were issued four

years ago and still change hands at face value.

Required:

(i) Compute the component cost of:

- Ordinary share capital;

- Debt capital

- Preference share capital.

(ii) Compute the company's current weighted average cost of capital. (5 marks)

(iii) Compute the company's marginal cost of capital if it raised the additional Sh.10

million as envisaged. (Assume a tax rate of 30%).

Date posted:

December 14, 2021

-

Format for the financial account of a non profit making organisation

Date posted:

December 14, 2021

-

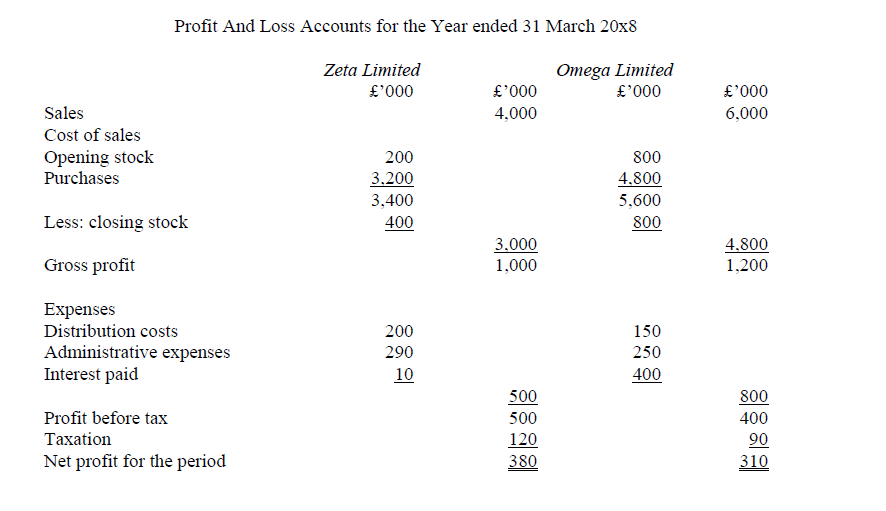

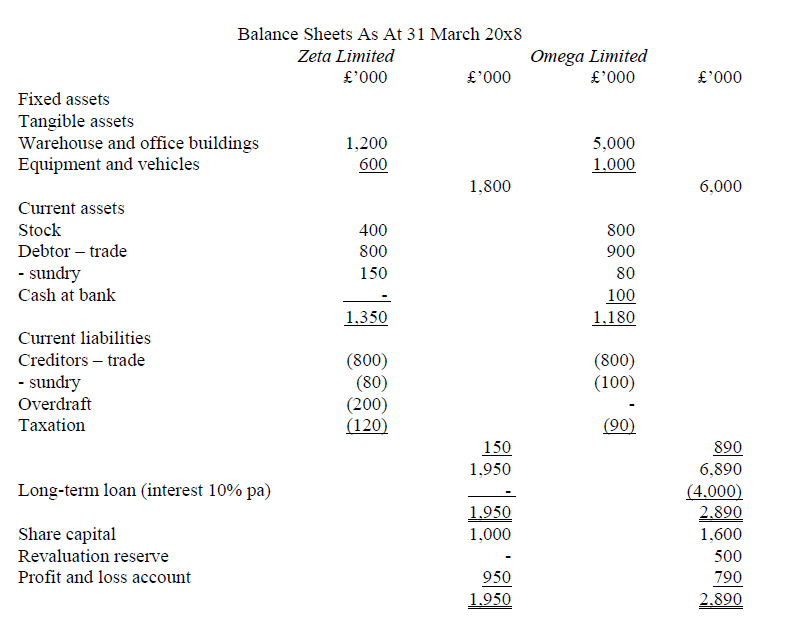

Beta Ltd is reviewing the financial statements of two companies, Zeta Ltd and Omega Ltd. The companies trade as wholesalers, selling electrical goods to retailers on credit. Their most recent financial statements appear below.

Required:

a)Calculate for each company a total of eight ratios which will assist in measuring the three aspects of profitability, liquidity and management of the elements of working capital. Show all workings.

b)Based on the ratios you have calculated in (a), compare the two companies as regards their profitability, liquidity and working capital management.

c)Omega Ltd is much more highly geared than Zera Ltd. What are the implications of this for the two companies?

Required:

a)Calculate for each company a total of eight ratios which will assist in measuring the three aspects of profitability, liquidity and management of the elements of working capital. Show all workings.

b)Based on the ratios you have calculated in (a), compare the two companies as regards their profitability, liquidity and working capital management.

c)Omega Ltd is much more highly geared than Zera Ltd. What are the implications of this for the two companies?

Date posted:

December 14, 2021