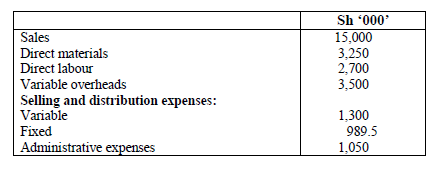

- Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:(Solved)

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

Date posted: February 21, 2019.

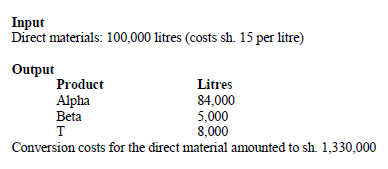

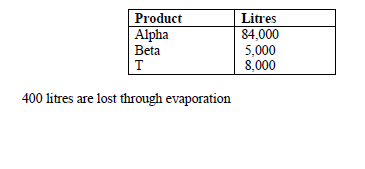

- Kenya Industrial Chemical limited (KICL) produces an industrial chemical branded Alpha. During the

production process a by-product Beta and a toxic waste T are also produced.

During...(Solved)

Kenya Industrial Chemical limited (KICL) produces an industrial chemical branded Alpha. During the

production process a by-product Beta and a toxic waste T are also produced.

During the month of October 2005, KICL recorded the following information in relation to the

production process.

Additional Information:

1. The toxic waste T is produced at the final production stage. KICL incurs sh. 80 to dispose of a

litre of T

2. Beta is transferred to a subsequent operation where it is packed at a cost of sh.25 per litre

This cost has not been included in the direct materials and conversion costs shown above.

During the month of October 2005, 300 litres of Deta were sold at a retail price of sh. 75 per litre

3. If is the company's policy to credit the account with the net realizable value of Beta produced

4. The normal output from the production process per 10,000 litres of direct materials is;

Additional Information:

1. The toxic waste T is produced at the final production stage. KICL incurs sh. 80 to dispose of a

litre of T

2. Beta is transferred to a subsequent operation where it is packed at a cost of sh.25 per litre

This cost has not been included in the direct materials and conversion costs shown above.

During the month of October 2005, 300 litres of Deta were sold at a retail price of sh. 75 per litre

3. If is the company's policy to credit the account with the net realizable value of Beta produced

4. The normal output from the production process per 10,000 litres of direct materials is;

Required:

a) Prepare the following accounts for the month of October 2005

i. Process account

ii. By-product

iii. Normal loss account (toxic waste)

iv. Abnormal loss account (toxic waste)

b) Determine the abnormal gain or loss products A,B

Required:

a) Prepare the following accounts for the month of October 2005

i. Process account

ii. By-product

iii. Normal loss account (toxic waste)

iv. Abnormal loss account (toxic waste)

b) Determine the abnormal gain or loss products A,B

Date posted: February 21, 2019.

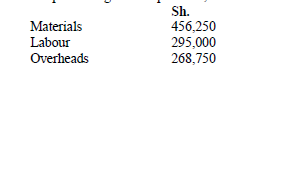

- Jitegemee limited company uses a process costing system in its operation. In one of the production processes, two joint products A and B and a...(Solved)

Jitegemee limited company uses a process costing system in its operation. In one of the

production processes, two joint products A and B and a by-product C are produced

The following additional information is provided:

1. Each processing run requires 12,500 kilograms of output.the costs incurred are as follow:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

Date posted: February 21, 2019.

- Go easy Limited crushes and refines mineral one into three products in a joint cost operation.

Costs and production for 1991 were as follows:-(Solved)

“Go easy” Limited crushes and refines mineral one into three products in a joint cost operation.

Costs and production for 1991 were as follows:-

Department X:

Initial joint costs sh. 2,100,000 producing 100,000 kilograms of Alco,

300,000 kilograms of Devo and 500,000 kilograms of Holo

Department Y: Processes Alco further at a cost of sh. 500,000

Department Z: Processes Devo further at a cost of sh. 1,000,000

Results 1991

Alco 180,000 kilograms completed; 95,000 kilograms sold for sh. 100 per

kilogram; Final inventory 5,000 kilograms

Devo: 300,000 kilograms completed; 295,000 kilograms sold for sh. 30 per

kilogram; final inventory 5,000 kilograms

Holo: 500,000 kilograms completed; 495,000 kilograms sold for sh. 5 per

kilograms; final inventory 5,000 kilograms; Holo required no further

processing

Required:

a) Use the net realizable –value method to allocate the joint costs of the three products

b) Compute the total costs and unit costs of ending inventories

Date posted: February 21, 2019.

- The West Africa Industries Limited buys crude vegetable oil: The refining of these oils results in four

products A, B and C which are liquids and...(Solved)

The West Africa Industries Limited buys crude vegetable oil: The refining of these oils results in four

products A, B and C which are liquids and D which is a heavy residue. The cost of the oil refined in

1992 was sh. 1,104,000 and the refining department had total processing costs of sh. 2,800,000. The

output and sales for the four products in 1992 were as follows:-

Required:

a) Assume that the next realizable value of allocating joint is used. What is the net income for

products A, B C and D? Joint cost total sh. 3,904,000

b) The company has been tempted to sell at split-off directly to other processors. If the alternative

had been selected, sales per litre would have been A, sh. 150, B sh. 5, C sh. 8 and D sh.30. What

would the net income be for each product under these alternatives?

Required:

a) Assume that the next realizable value of allocating joint is used. What is the net income for

products A, B C and D? Joint cost total sh. 3,904,000

b) The company has been tempted to sell at split-off directly to other processors. If the alternative

had been selected, sales per litre would have been A, sh. 150, B sh. 5, C sh. 8 and D sh.30. What

would the net income be for each product under these alternatives?

Date posted: February 21, 2019.

- The following information is obtained in respect of process 2 of the month of September;(Solved)

The following information is obtained in respect of process 2 of the month of September;

There was a normal loss in the process of 10% of production units' scrapped realized sh. 50 per unit,

use FIFO method

Required:

i. Statement of production

ii. Statement of cost and evaluation

iii. Process account

iv. Abnormal loss / gain account

There was a normal loss in the process of 10% of production units' scrapped realized sh. 50 per unit,

use FIFO method

Required:

i. Statement of production

ii. Statement of cost and evaluation

iii. Process account

iv. Abnormal loss / gain account

Date posted: February 21, 2019.

- a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account(Solved)

Required:

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

Required:

a) Calculate the cost of completed units transferred to process 3

b) Calculate the value of closing WIP

c) Show (i) Process 2 account

(ii) Abnormal Gain account

Date posted: February 21, 2019.

- The following data is shown in respect to month of August for process 3(Solved)

The following data is shown in respect to month of August for process 3

Required:

Using weighted average method show relevant accounts

Required:

Using weighted average method show relevant accounts

Date posted: February 21, 2019.

- Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information...(Solved)

Kenya chemical industries limited, process a range of products including bleaching detergent which

passes three processes before completion and transferred to finished goods store. The following

information was extracted from the books of the company for the month of October.

Date posted: February 21, 2019.

- Pakawa Ltd. employs five processes to manufacture a hybrid fertilizer branded 'Sunshine'.

The data below relates to process C for the month of October 2005:(Solved)

Pakawa Ltd. employs five processes to manufacture a hybrid fertilizer branded 'Sunshine.

The data below relates to process C for the month of October 2005:

Material costs are added to the product as the end of the process and conversion costs are assumed to

be incurred uniformly throughout the process. Manufacturing overhead is applied to the product on

the basis of 50 per cent of labour cost.

Additional information:

1. Units lost during processing are considered to be a normal occurrence unless the numbers of lost

units exceed 5 per cent of total units accounted for. The cost of normal loss is absorbed by the cost

of total units accounted for.

2. Lost units in excess of 5 per cent are considered abnormal. This cost is separately identified and

written off as a loss. The company cost accounts follow a policy of assigning only transferred-in

costs to abnormally lost units.

Required:

Using the FIFO method of valuing inventory, prepare process C statement for the month of October

2005 showing:

(i) Total cost assigned to good units and transferred to process D.

(ii) Total loss due to abnormal lost units.

(iii) Valuation of closing work-in-progress in total and by elements of cost

(d) Identify the causes of losses in process costing

Material costs are added to the product as the end of the process and conversion costs are assumed to

be incurred uniformly throughout the process. Manufacturing overhead is applied to the product on

the basis of 50 per cent of labour cost.

Additional information:

1. Units lost during processing are considered to be a normal occurrence unless the numbers of lost

units exceed 5 per cent of total units accounted for. The cost of normal loss is absorbed by the cost

of total units accounted for.

2. Lost units in excess of 5 per cent are considered abnormal. This cost is separately identified and

written off as a loss. The company cost accounts follow a policy of assigning only transferred-in

costs to abnormally lost units.

Required:

Using the FIFO method of valuing inventory, prepare process C statement for the month of October

2005 showing:

(i) Total cost assigned to good units and transferred to process D.

(ii) Total loss due to abnormal lost units.

(iii) Valuation of closing work-in-progress in total and by elements of cost

(d) Identify the causes of losses in process costing

Date posted: February 21, 2019.

- (a) In relation to process costing, explain the following terms:

(i) Direct material costs

(ii) Conversion costs

(b) Explain the features that are necessary for process costing to...(Solved)

(a) In relation to process costing, explain the following terms:

(i) Direct material costs

(ii) Conversion costs

(b) Explain the features that are necessary for process costing to be effectively applied in a

business entity?

Date posted: February 21, 2019.

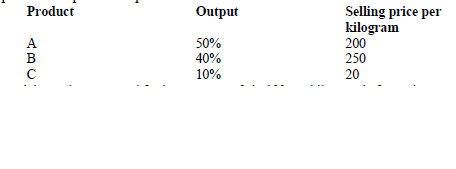

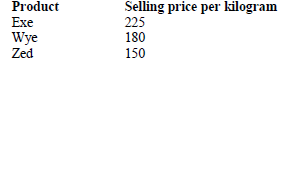

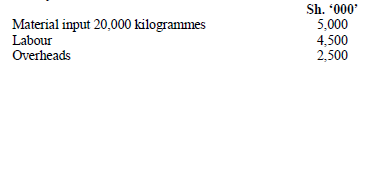

- Lenga Juu Limited produces three the products; Exe, Wye and Zed in a single process. For the

month of September 2006, the following budgeted figures were...(Solved)

Lenga Juu Limited produces three the products; Exe, Wye and Zed in a single process. For the

month of September 2006, the following budgeted figures were available:

Additional information

1. Fixed overheads were absorbed at 50% of labour cost

2. There was a normal loss of 10% of material input and no abnormal loss. The normal loss was

sold as scrap at sh. 15 per kilogram which was credited to the process account

3. Exe, Wye and Zed were produced in the ratio of 5:3:2 respectively

4. There was neither opening nor closing work in progress

5. The products were sold as follows:-

Additional information

1. Fixed overheads were absorbed at 50% of labour cost

2. There was a normal loss of 10% of material input and no abnormal loss. The normal loss was

sold as scrap at sh. 15 per kilogram which was credited to the process account

3. Exe, Wye and Zed were produced in the ratio of 5:3:2 respectively

4. There was neither opening nor closing work in progress

5. The products were sold as follows:-

Required:

Apportion the joint cost to the joint products, Exe, Wye and Zed using the following methods

i. Relative weight of output

ii. Sales value of output

b) On further processing, products Exe, Wye and Zed were converted to product A, B and C

respectively. The following prices per kilogramme were sh. 270, sh. 225 and sh. 180 for products

A, b and C respectively.

The further processing cost the company sh. 15 per kilogramme of material input. In addition the

normal loss was 10% of material input with no sales value.

Required:

Profit or loss on further processing of each of the products

Required:

Apportion the joint cost to the joint products, Exe, Wye and Zed using the following methods

i. Relative weight of output

ii. Sales value of output

b) On further processing, products Exe, Wye and Zed were converted to product A, B and C

respectively. The following prices per kilogramme were sh. 270, sh. 225 and sh. 180 for products

A, b and C respectively.

The further processing cost the company sh. 15 per kilogramme of material input. In addition the

normal loss was 10% of material input with no sales value.

Required:

Profit or loss on further processing of each of the products

Date posted: February 21, 2019.

- Usafi Limited operates a single process manufacturer soap. The process costs for the month of

February 2007 were as follows:-(Solved)

Usafi Limited operates a single process manufacturer soap. The process costs for the month of

February 2007 were as follows:-

Additional information:

1. The normal output of the process is 95% of material input. The loss from the process is sold for

sh. 60 per kilogram me

2. The output for the month of February 2007 was as follows:-

Finished goods 18,800 kilogram-mes

Closing work in progress 1,000 kilogram-mes

3. The degree of completion of closing work in progress was 50% for lab our and overheads and

overheads and 100% for materials.

Required:

i. Process account

ii. Abnormal gain account

Additional information:

1. The normal output of the process is 95% of material input. The loss from the process is sold for

sh. 60 per kilogram me

2. The output for the month of February 2007 was as follows:-

Finished goods 18,800 kilogram-mes

Closing work in progress 1,000 kilogram-mes

3. The degree of completion of closing work in progress was 50% for lab our and overheads and

overheads and 100% for materials.

Required:

i. Process account

ii. Abnormal gain account

Date posted: February 21, 2019.

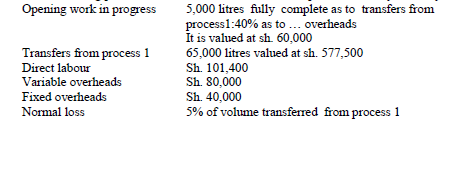

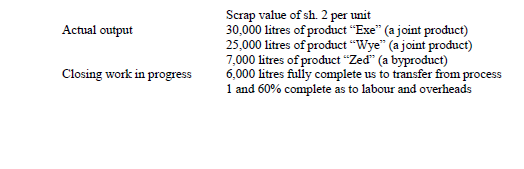

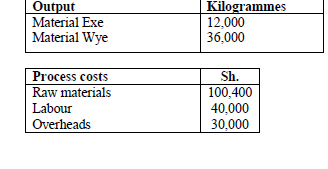

- The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed(Solved)

The manufacturing process of ABC limited results in three products namely Exe, Wye and Zed

Additional information;-

1. The final selling prices per litre of products Exe, Wye and Zed are shs.15, shs.18 and shs.4

respectively.

2. There are no further costs associated with by product Zed

3. Product Wye requires further processing at a cost of sh. 1.50 per litre

4. All the three products incur packaging costs of sh. 0.50 per litre before they are sold.

Required:

i) Calculate the number of equivalent units produced

ii) Calculate the costs of products Exe and Wye

iii) Apportion the common costs to joint products based on sales at the point of separation

iv) Prepare process II account for the month of January 2008

Additional information;-

1. The final selling prices per litre of products Exe, Wye and Zed are shs.15, shs.18 and shs.4

respectively.

2. There are no further costs associated with by product Zed

3. Product Wye requires further processing at a cost of sh. 1.50 per litre

4. All the three products incur packaging costs of sh. 0.50 per litre before they are sold.

Required:

i) Calculate the number of equivalent units produced

ii) Calculate the costs of products Exe and Wye

iii) Apportion the common costs to joint products based on sales at the point of separation

iv) Prepare process II account for the month of January 2008

Date posted: February 21, 2019.

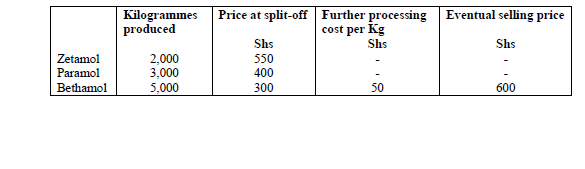

- Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material...(Solved)

Good Hope Pharmaceutical Company purchases raw material that is processed to yield three

chemicals namely;Zetamol,Paramol, and Bethamol.In January 2009,the company purchased 10,000

kilogrammes of the raw material nat a cost of sh.2,500,000 and incurred joint conversion costs of

sh.700,000.Sales and production information for the month of January wered as follows;

Zetamol and Paramol are sold to other pharmaceutical companies at the split off point. Bethamol can

be sold at the split off point or processed further and packaged for sale as an asthma medication.

Required

Allocate the joint costs to the three products using;

i) The physical units sold

ii) The sales value at split off method

iii) The net realizable value method

iv) Suppose that half the production of Paramol could be purified and mixed with all the

production of Zetamol to yield parazetamol.All further processing costs amount to

sh.350,000.The selling price for parazetamol is sh.1,120 per kilogramme.Advise the company

on whether to further process Zetamol into 2,000 kilogrammes of parazetamol.

Zetamol and Paramol are sold to other pharmaceutical companies at the split off point. Bethamol can

be sold at the split off point or processed further and packaged for sale as an asthma medication.

Required

Allocate the joint costs to the three products using;

i) The physical units sold

ii) The sales value at split off method

iii) The net realizable value method

iv) Suppose that half the production of Paramol could be purified and mixed with all the

production of Zetamol to yield parazetamol.All further processing costs amount to

sh.350,000.The selling price for parazetamol is sh.1,120 per kilogramme.Advise the company

on whether to further process Zetamol into 2,000 kilogrammes of parazetamol.

Date posted: February 21, 2019.

- Oxfam limited produces a product Jay in three processes. During the month of August 2009,

5,000 units were transferred from process one at a cost of...(Solved)

Oxfam limited produces a product Jay in three processes. During the month of August 2009,

5,000 units were transferred from process one at a cost of sh. 37 per unit

In addition the following costs were incurred in process two:-

Date posted: February 21, 2019.

- (i) Define the term 'uniform costing'.

(ii) Highlight four advantages of uniform costing'(Solved)

(i) Define the term 'uniform costing'.

(ii) Highlight four advantages of uniform costing'

Date posted: February 21, 2019.

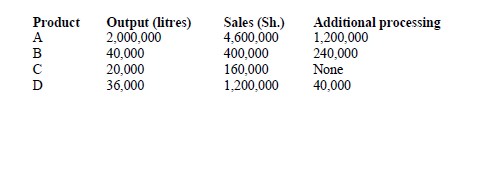

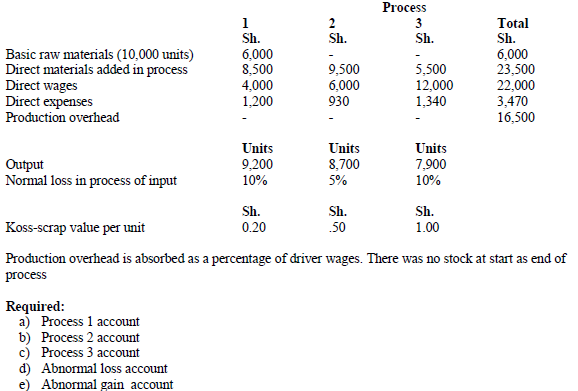

- ABC Company limited produces four products A, B, C and D

The following information is provided

1. The joint processing requires 10,000 kilograms of raw materials input,...(Solved)

ABC Company limited produces four products A, B, C and D

The following information is provided

1. The joint processing requires 10,000 kilograms of raw materials input, costing sh. 6 million

2. Joint process labour and material costs are sh. 5,920,000

3. Normal loss is 20% of raw material input, with product A's output being 2000 kilogram mes,

product B's output being 2,500 kilogram mes, product C's output being 2,500 kilogram mes and

the balance being from product D. No abnormal loss was reported.

4. Product A enters into process 2 incurring a further cost of sh. 1,255,000 , product B enters

process 3 incurring a further cost of sh. 1,493,750 product C enters into process 4 incurring a

further cost of sh. 1,118,750. Product D does not require additional processing. There are no

further processing costs.

5. The company‟s policy is to apportion joint costs on the basis of output

6. The selling price of each unit of products A, B C and D is sh. 1,500, sh. 3,460, sh. 2760 and sh.

1,000 respectively.

7. The company is in the process of analyzing the performance of each product in order to make

better decisions.

Required:

a) i) Cost per unit of product A

ii) Profit and loss statement for each individual product and for the company in a columnar

format

b) The company's management intends to start using the net realizable value method to allocate

joint costs. Show how this method would affect the profitability of individual products and that

of the company in (a) (ii) above.

Date posted: February 21, 2019.

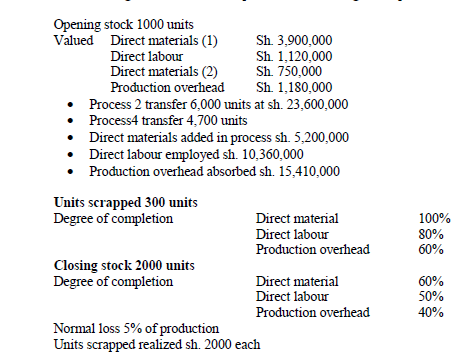

- Nyungu Limited is a manufacture of earthenware products. The undergo two processes; A and B(Solved)

Nyungu Limited is a manufacture of earthenware products. The undergo two processes; A and B

Additional information

1. Conversion costs are applied uniformly throughout the two processes.

2. Normal loss is 5% of throughput in both processes.

3. Scrap for normal loss is Sh. 250 per unit in process A and Sh. 500 per unit in process B.

4. Actual loss is 4,000 units in process A and 1,500 units in process B.

Required:

a) Statement of equivalent units for process A and B

b) For process A:

i) Total cost of production transferred to process B.

ii) Total cost of closing work-in-progress

c) For process B:

i) Total cost of production transferred to finished goods.

ii) Total cost of closing work-in-progress.

Additional information

1. Conversion costs are applied uniformly throughout the two processes.

2. Normal loss is 5% of throughput in both processes.

3. Scrap for normal loss is Sh. 250 per unit in process A and Sh. 500 per unit in process B.

4. Actual loss is 4,000 units in process A and 1,500 units in process B.

Required:

a) Statement of equivalent units for process A and B

b) For process A:

i) Total cost of production transferred to process B.

ii) Total cost of closing work-in-progress

c) For process B:

i) Total cost of production transferred to finished goods.

ii) Total cost of closing work-in-progress.

Date posted: February 21, 2019.

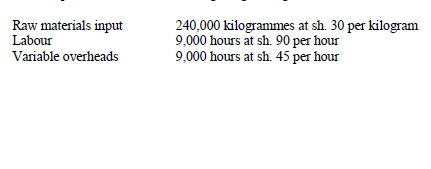

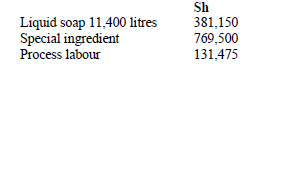

- Usafi Limited manufactures a brand of shampoo branded "Urembo". The company blends a liquid

soap with a special ingredient which has no significant volume. The resulting...(Solved)

Usafi Limited manufactures a brand of shampoo branded 'Urembo'. The company blends a liquid

soap with a special ingredient which has no significant volume. The resulting liquid is then put

into bottles costing Sh.5 each.

The following data relates to processing for the month of August 2011

Inputs into the blending process:

Additional information:

1. General overhead costs are absorbed on the basis of process labour costs at the rate of 100%.

2. The normal output of the blending process is 90% of input liquid soap.

3. The losses in the process take the form of a thicker soap which is sold for Sh.25 per litre.

4. The output from the process was 10,800 litres of Urembo which is equivalent to the monthly

budgeted output.

5. Each bottle of Urembo contains one third of a litre of shampoo and is sold for Sh.75.

Required:

(i) Process account for the blending in the month of August 2011.

(ii) Normal profit per bottle of shampoo.

c) The marketing department of Usafi Limited has made a proposal to rebrand Urembo as follows:

1. Change the name of the shampoo to "Urembo extra".

2. Use a different special ingredients costing 10% more than the existing one.

3. Use a different bottle design costing Sh.7.50 each but with the same capacity of one third of a

litre.

4. Undertake an advertising campaign costing Sh.4,374,000.

5. Maintain a maximum monthly budgeted output of 10,800 litres.

6. The production manager has forecasted the maximum shelf life of "Urembo extra" at 6

months.

7. Urembo extra has a potential of trading at a higher price than Urembo according to market

trend analysis.

Required:

Minimum price per bottle at which Urembo extra must be sold to maintain the company's current

profit level

Additional information:

1. General overhead costs are absorbed on the basis of process labour costs at the rate of 100%.

2. The normal output of the blending process is 90% of input liquid soap.

3. The losses in the process take the form of a thicker soap which is sold for Sh.25 per litre.

4. The output from the process was 10,800 litres of Urembo which is equivalent to the monthly

budgeted output.

5. Each bottle of Urembo contains one third of a litre of shampoo and is sold for Sh.75.

Required:

(i) Process account for the blending in the month of August 2011.

(ii) Normal profit per bottle of shampoo.

c) The marketing department of Usafi Limited has made a proposal to rebrand Urembo as follows:

1. Change the name of the shampoo to "Urembo extra".

2. Use a different special ingredients costing 10% more than the existing one.

3. Use a different bottle design costing Sh.7.50 each but with the same capacity of one third of a

litre.

4. Undertake an advertising campaign costing Sh.4,374,000.

5. Maintain a maximum monthly budgeted output of 10,800 litres.

6. The production manager has forecasted the maximum shelf life of "Urembo extra" at 6

months.

7. Urembo extra has a potential of trading at a higher price than Urembo according to market

trend analysis.

Required:

Minimum price per bottle at which Urembo extra must be sold to maintain the company's current

profit level

Date posted: February 21, 2019.

- Jasho Ltd. manufactures a product branded 'Vumilia'. The marketing department of Jasho Ltd. has

expressed concern that the product has not been profitable. The department has...(Solved)

Jasho Ltd. manufactures a product branded 'vumilia'. The marketing department of Jasho Ltd. has

expressed concern that the product has not been profitable. The department has therefore

recommended that appropriate action be taken to stem the losses.

Vumilia is produced from material Exe which is one of two materials jointly produced by passing

chemicals through a process. The other material is Wye.

During the month of February 2012, the following data was recorded for the process.

Additional information:

1. Joint costs are apportioned to the two materials, Exe and Wye according to the weight of output.

2. Production costs incurred in converting material Exe into finished product "Vumilia" are Sh.3 per

kilogramme of material used.

3. Normal loss for the process is 10% with no scrap value.

4. The selling price per kilogramme of "Vumilia" is Sh.7.

5. Material Wye is sold without further processing for Sh.8 per kilogramme.

Required;

a) Calculate the profit/loss per kilogramme of product 'Vumilia' and material 'Wye'.

b) Analyse the marketing department's recommendation and advise the company as appropriate.

c) Demonstrate an alternative joint cost apportionment for product 'Vumilia'. Comment briefly on

the alternative method of apportionment.

Additional information:

1. Joint costs are apportioned to the two materials, Exe and Wye according to the weight of output.

2. Production costs incurred in converting material Exe into finished product "Vumilia" are Sh.3 per

kilogramme of material used.

3. Normal loss for the process is 10% with no scrap value.

4. The selling price per kilogramme of "Vumilia" is Sh.7.

5. Material Wye is sold without further processing for Sh.8 per kilogramme.

Required;

a) Calculate the profit/loss per kilogramme of product 'Vumilia' and material 'Wye'.

b) Analyse the marketing department's recommendation and advise the company as appropriate.

c) Demonstrate an alternative joint cost apportionment for product 'Vumilia'. Comment briefly on

the alternative method of apportionment.

Date posted: February 21, 2019.

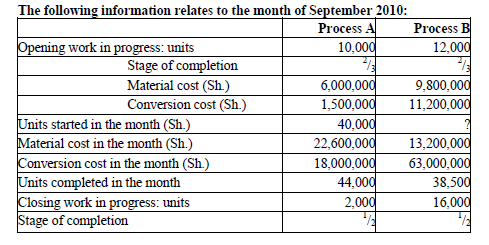

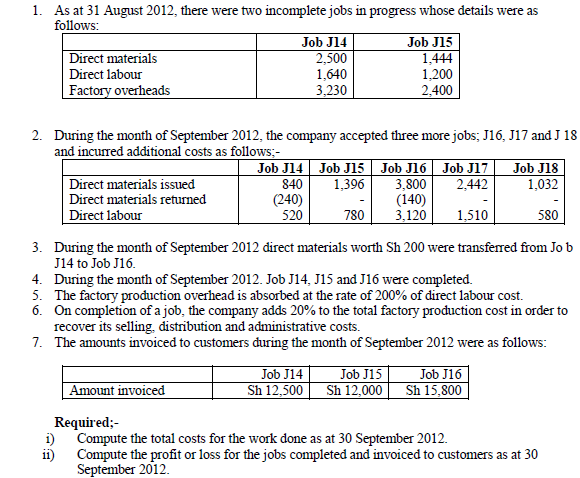

- Smarta Ltd. manufactures flower pots for sale. The company does not carry any stock of finished

goods as it manufactures specifically to customer's orders. However, the...(Solved)

Smarta Ltd. manufactures flower pots for sale. The company does not carry any stock of finished

goods as it manufactures specifically to customer's orders. However, the company holds a range

of raw materials in the stores.

The following information relates to the company's operations for the mouths of August and

September 2012:

Date posted: February 21, 2019.

- (i) Briefly explain the difference between job costing and batch costing.

(ii) Outline three features of job costing.(Solved)

(i) Briefly explain the difference between job costing' and batch costing'.

(ii) Outline three features of job costing.

Date posted: February 21, 2019.

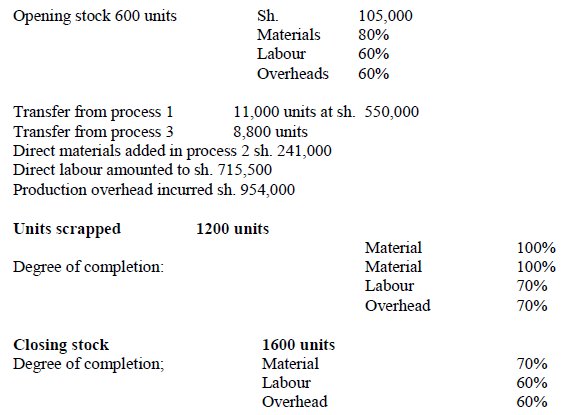

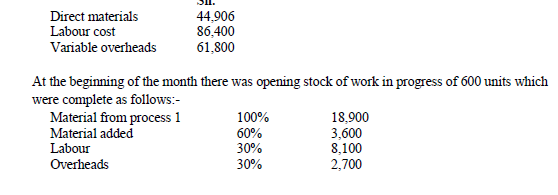

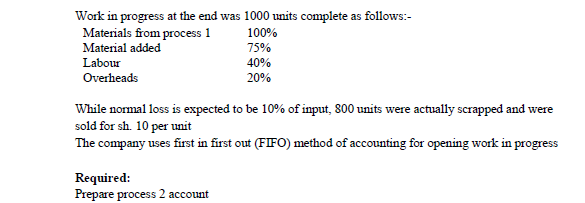

- a) Explain why it is necessary to distinguish between direct labour and indirect labour, with

particular reference to the effect on gross profit and net profit.

b)...(Solved)

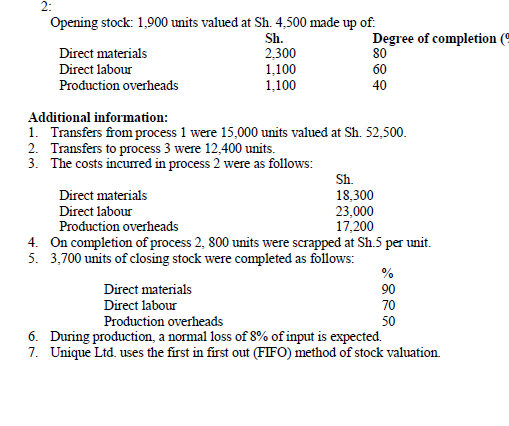

a) Explain why it is necessary to distinguish between direct labor and indirect labor, with

particular reference to the effect on gross profit and net profit.

b) Unique Ltd. manufactures a single product. The product passes through three processes before

completion. In the month of January 2013, the following data was recorded in respect to process

Required:

i) Statement of equivalent production.

ii) Statement of costs.

iii) Process 2 account

Required:

i) Statement of equivalent production.

ii) Statement of costs.

iii) Process 2 account

Date posted: February 21, 2019.

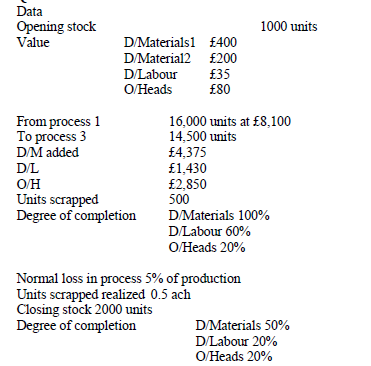

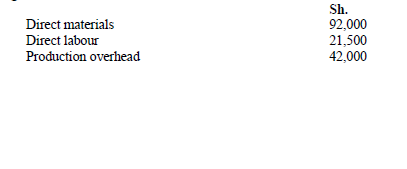

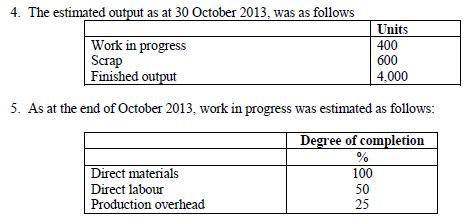

- Nald Ltd. manufactures a chemical product and uses process costing to account for its work in

progress. During the month of October 2013, 5,000 units...(Solved)

Nald Ltd. manufactures a chemical product and uses process costing to account for its work in

progress. During the month of October 2013, 5,000 units were introduced to process 1 and the

following costs were incurred:

Additional information:

1. The normal loss in process 1 was estimated at 10%.

2. The scrapped normal loss units were sold at Sh.4 per unit.

3. Inspection is usually done at the end of the process; therefore any units scrapped would have

passed through the entire process.

Additional information:

1. The normal loss in process 1 was estimated at 10%.

2. The scrapped normal loss units were sold at Sh.4 per unit.

3. Inspection is usually done at the end of the process; therefore any units scrapped would have

passed through the entire process.

Required

i) Statement of equivalent production

ii) Statement of cost

iii) Statement of evaluation of finished goods

iv) Process 1 account

Required

i) Statement of equivalent production

ii) Statement of cost

iii) Statement of evaluation of finished goods

iv) Process 1 account

Date posted: February 21, 2019.

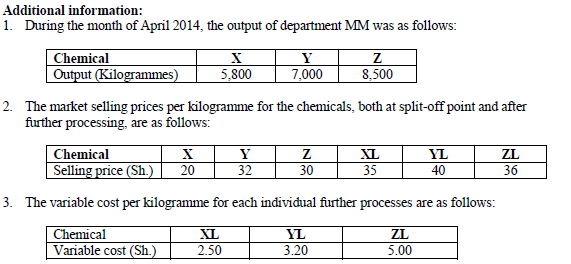

- Chemtex Ltd., a chemicals manufacturing company has two departments namely; MM and NN.

Department MM produces three types of chemicals; X, Y and Z using a...(Solved)

Chemtex Ltd., a chemicals manufacturing company has two departments namely; MM and NN.

Department MM produces three types of chemicals; X, Y and Z using a common process.

Each of the chemicals can either be sold by department MM to the external market at the split-off

point or can be transferred to department NN for individual further processing into products XL, YL

and ZL respectively.

4. Further processing leads to a normal loss of 5% at the beginning of the process for each of the

chemicals being manufactured.

Required:

Advise the management on which chemical(s), if any, should be subjected to further processing

4. Further processing leads to a normal loss of 5% at the beginning of the process for each of the

chemicals being manufactured.

Required:

Advise the management on which chemical(s), if any, should be subjected to further processing

Date posted: February 21, 2019.

- Explain the meaning of the following terms in regard to the cost and financial accounting

systems:

i) Integrated cost accounts

ii) Interlocking cost accounts

iii) Cost ledger control account

iv)...(Solved)

Explain the meaning of the following terms in regard to the cost and financial accounting

systems:

i) Integrated cost accounts

ii) Interlocking cost accounts

iii) Cost ledger control account

iv) Cost ledger contra account

Date posted: February 21, 2019.

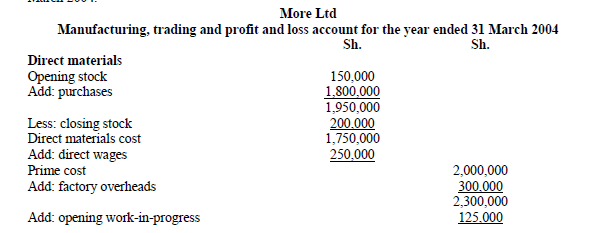

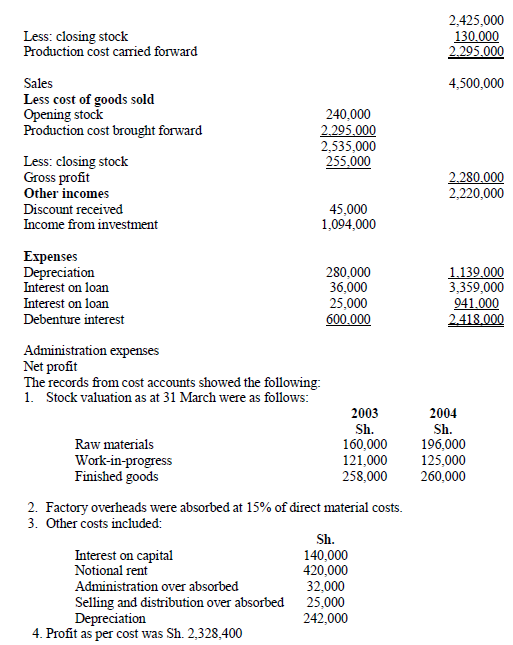

- More Ltd. is a medium size manufacturing company and it maintains separate cost and financialaccounting books. The financial accountant provided the following statement for the...(Solved)

More Ltd. is a medium size manufacturing company and it maintains separate cost and financial

accounting books. The financial accountant provided the following statement for the year ended 31

March 2004.

Required:

Prepare a profit reconciliation statement for the year ended 31 March 2004.

Required:

Prepare a profit reconciliation statement for the year ended 31 March 2004.

Date posted: February 19, 2019.

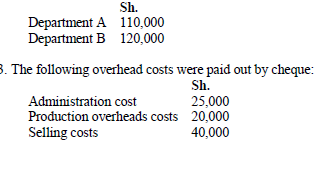

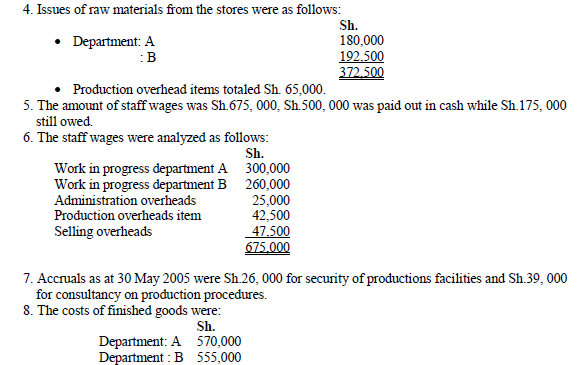

- Bora Ltd. Commenced its operations on 1 march 2005 with a fully paid up issued share capital of

Sh.500,000 represented by fixed assets of Sh.275,000 and...(Solved)

Bora Ltd. Commenced its operations on 1 march 2005 with a fully paid up issued share capital of

Sh.500,000 represented by fixed assets of Sh.275,000 and cash at bank of Sh.225,000.

The company has two departments; A and B.

As at 30 may 2005, the following transactions had taken place:

1. Credit purchases from suppliers amounted to Sh.573, 500 of which Sh.525, 000 were in respect

of raw materials and Sh.48, 500 were in respect of purchases classified in the ledger accounts

as production overhead items.

2. Production overhead costs absorbed in the period were:

9. Sales on credit amounted to Sh. 870,000 and the cost of these credit sales was Sh. 700,000.

10. Depreciation on production plant and equipment was Sh. 15,000.

11. Cash received from debtors totaled Sh. 520,000 and payments made to creditors totaled

Sh.150,000.

Required:

(i). Using integrated cost accounting system, record the above transactions for the three months

ended 30 May 2005.

(ii). Profit and loss account for the period ended 30 May 2005 and balance sheet as at 30 May

2005.

9. Sales on credit amounted to Sh. 870,000 and the cost of these credit sales was Sh. 700,000.

10. Depreciation on production plant and equipment was Sh. 15,000.

11. Cash received from debtors totaled Sh. 520,000 and payments made to creditors totaled

Sh.150,000.

Required:

(i). Using integrated cost accounting system, record the above transactions for the three months

ended 30 May 2005.

(ii). Profit and loss account for the period ended 30 May 2005 and balance sheet as at 30 May

2005.

Date posted: February 19, 2019.

- State possible causes of differences between reported profits in cost accounting and financial

accounting under the non-integrated cost accounting system.(Solved)

State possible causes of differences between reported profits in cost accounting and financial

accounting under the non-integrated cost accounting system.

Date posted: February 19, 2019.