-

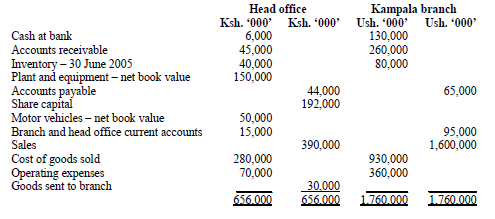

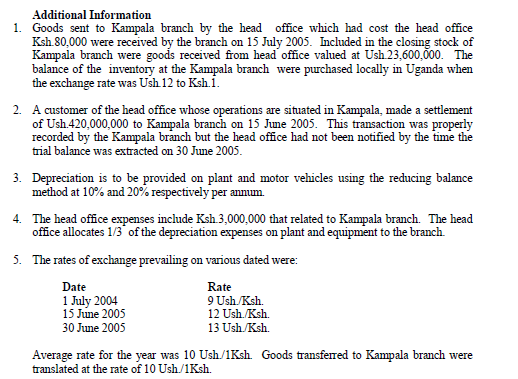

Beta East Africa Ltd. manufactures tubeless tyres at its head office plant located in Nairobi. It operates an overseas outlet at Kampala which maintains its own books of account. The tyres are transferred to the branch at head office cost plus 25% mark-up. All sales are at a uniform margin of 50%.

The trial balances extracted from the books o both the head office and the Kampala branch

as at 30 June 2005 were as follows:

Date posted:

February 11, 2019

-

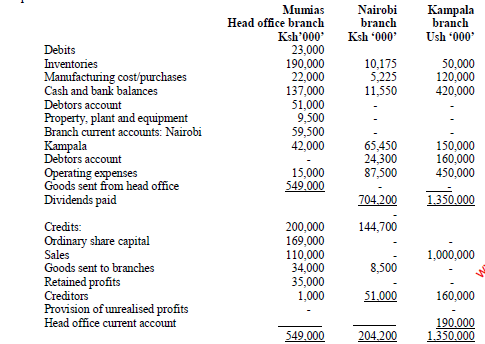

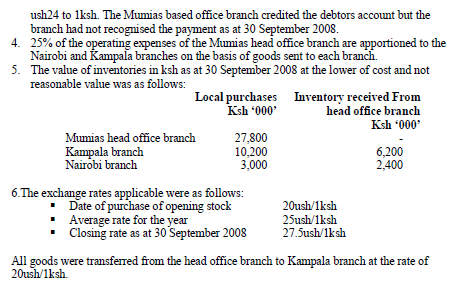

Impact Triangle ltd is a manufacturer of industrial ethanol. The head office of the company is in Mumias Kenya. The company has two other branches; one in Nairobi, Kenya and a foreign branch in Kampala Uganda. The reporting currency of the Kenya Branches is in Kenya shillings(Ksh) while the reporting currency of the Kampala branch is the Uganda Shilling(Ush)

The Nairobi and Kampala branches mainly deal with goods sent from Mumias branch. The goods are transferred from Mumias branch at a mark-up of 25% on cost to Nairobi and a margin of 25% to Kampala

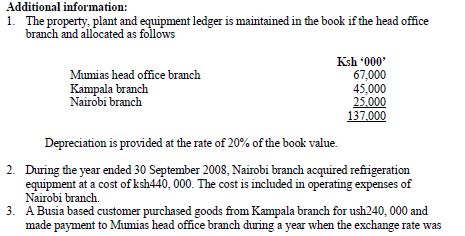

The following trial balances were extracted from the books of the company as at 30 September 2008

Determine:Trading profit and loss accounts for the head office, the two branches and combined business for the year ended 30 September 2008

Determine:Trading profit and loss accounts for the head office, the two branches and combined business for the year ended 30 September 2008

Date posted:

February 11, 2019

-

List four factors that should be considered in establishing an effective credit policy.

Date posted:

February 11, 2019

-

Identify and briefly explain the three main forms of agency relationship in a firm.

Date posted:

February 11, 2019

-

Dawamu Ltd, which operates in the retail sector selling a single product, is considering

a change of credit policy which will result in an increase in the average collection period

of debts from one to two months. The relaxation of the credit policy is expected to

produce an increase in sales in each year, amounting to 25% of the current sales

volume. The following information is available.

1. Selling price per unit of product – Sh.1,000

2. Variable cost per unit of product – Sh.850

3. Current annual sales of product – Sh.240,000,000

4. Dawamu Ltd.'s required rate of return on investments is 20%.

5. It is expected that increase in sales would result in additional stock of

Sh.10,000,000 and additional creditors of Sh.2,000,000.

Required:

Advise Dawamu Ltd. on whether or not to extend the credit period offered to

customers, if

(i) All customers take the longer credit period of two months.

(ii) Existing customers do not change their payment habits and only the new

customers will take a full two months' credit.

Date posted:

February 11, 2019

-

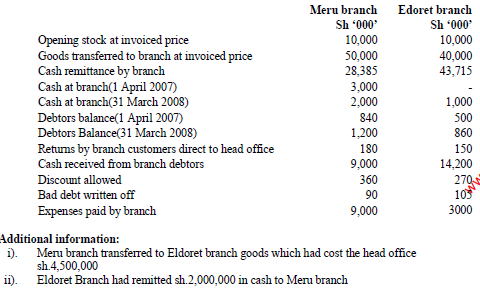

Sellwell Ltd operates a supermarket chain with a head office in Nairobi and branches in Meru and Eldoret.

Goods are transferred from the head office to Meru Branch at a mark-up of 25% and to Eldoret branch at a gross profit margin of 25%. The branches do not maintain separate books of accounts.

The following information relates to the transaction at both branches during the year ended 31 March 2008

Date posted:

February 11, 2019

-

Briefly explain how the Miller-Orr cash management model operates.

Date posted:

February 11, 2019

-

Briefly explain four purposes of the branch accounts to an organisation which sells goods through various outlets

Date posted:

February 11, 2019

-

Identify and briefly explain three conditions which have to be satisfied before the use of

the weighted average cost of capital (WACC) can be justified.

Date posted:

February 11, 2019

-

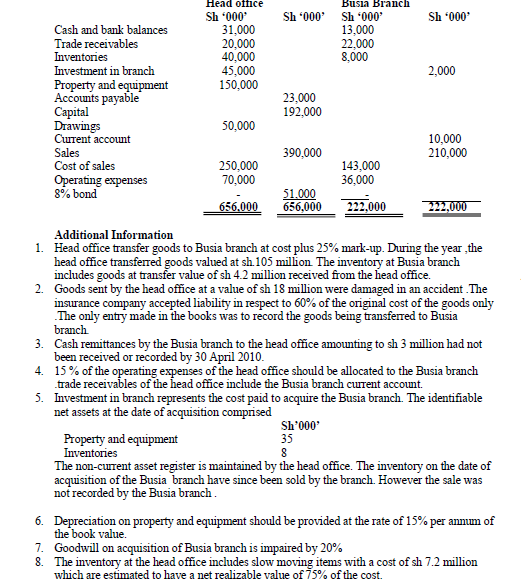

The trial balances below were extracted from the books of Shakers Enterprises with respect to its operations at the head office in Nakuru and Busia branch as at 30 April 2010.

Date posted:

February 11, 2019

-

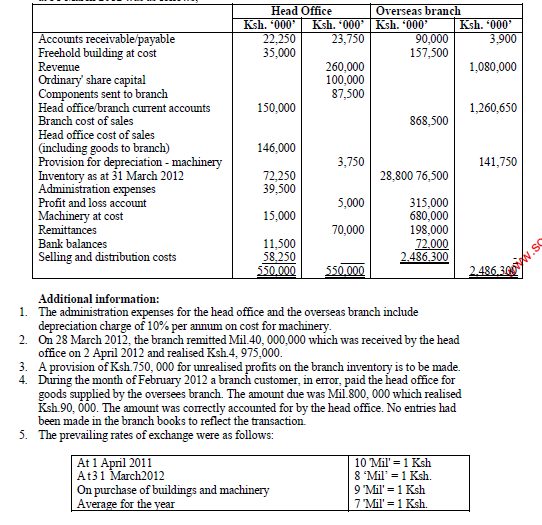

Elgon Ltd., a manufacturing concern, exports some of its products through an overseas branch whose currency is the "Mil". The reporting currency of Elgon Ltd. is the Kenya Shilling (Ksh.). The overseas branch carries out the final assembly for the products before the goods are sold to customers. The trial balances of the head office and overseas branch as at 31 March 2012 was as follows;-

Date posted:

February 11, 2019

-

In the context of non-autonomous branches, describe the accounting treatment in the books of the head office of the following items.

(i) Goods stolen in transit

(ii) Mark-ups and mark-downs in prices.

Date posted:

February 11, 2019

-

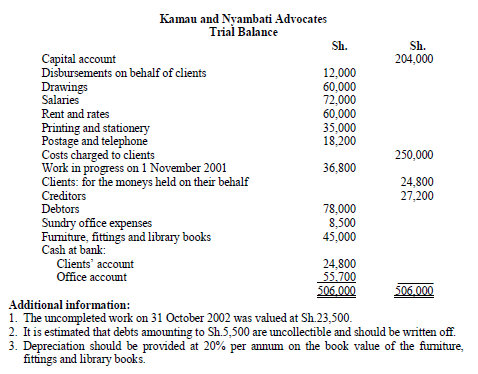

Given below is a trial balance extracted from the books of Kamau and Nyambati, a firm of practicing advocates as at 31 October 2002:

Date posted:

February 11, 2019

-

Briefly explain the following terms as used in the accounts of professional practitioners:

(i) Office account

(ii) Client account

(iii) Costs charged to clients

(iv) Work-in-progress.

Date posted:

February 11, 2019

-

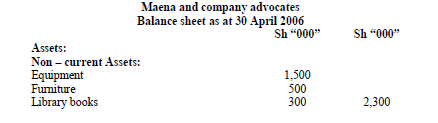

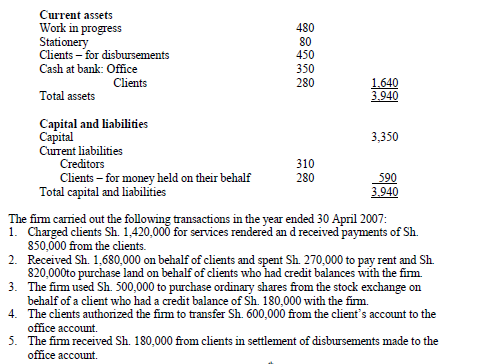

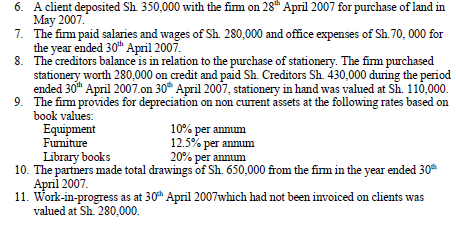

The following is the balance sheet of Maena and Company Advoactes, a small size law firm, as at 30 April 2006:

Date posted:

February 11, 2019

-

Magma Ltd. wishes to make a choice between two mutually exclusive projects. Each of

these projects requires Sh.400,000,000 in initial cash outlay. The details of the two

projects are as follows:

Project A

This project is made up of two sub-projects. The first sub-project will require an initial

outlay of Sh.100,000,000 and will generate Sh.25,600,000 per annum in perpetuity. The

second sub-project will require an initial outlay of Sh.300,000,000 and will generate

Sh.85,200,000 per annum for the 8 years of its useful life. This sub-project does not

have a residual value at the end of the 8 years. Both sub-projects are to commence

immediately.

Project B

This project will generate Sh.87,000,000 per annum in

perpetuity. The company has a cost of capital of 16%.

Required:

(i) Determine the net present value (NPV) of each project.

(ii) Compute the internal rate of return (IRR) for each project.

(iii) Advise Magma Ltd. on which project to invest in, and justify your choice

Date posted:

February 11, 2019

-

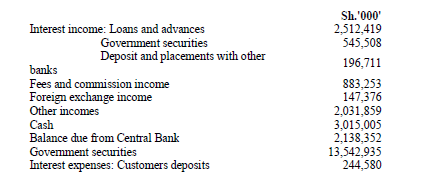

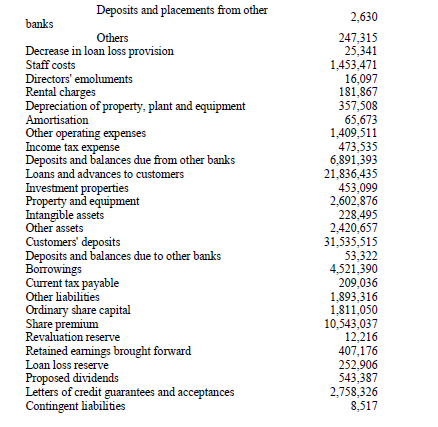

The following list of balances was extracted from the books of Mwananchi Bank Ltd as at 31 December 2008.

Date posted:

February 11, 2019

-

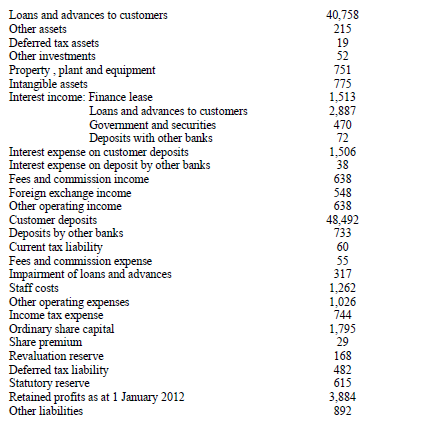

The following financial information was extracted from the books of Zuraya commercial Bank Ltd. as at 31 December 2012.

Date posted:

February 11, 2019

-

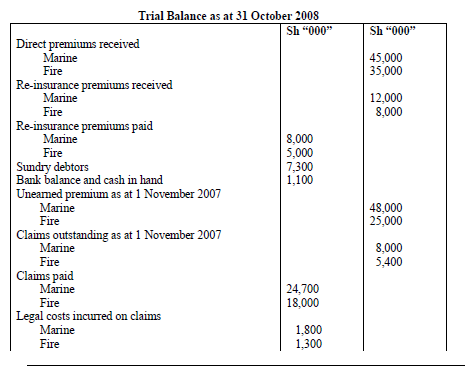

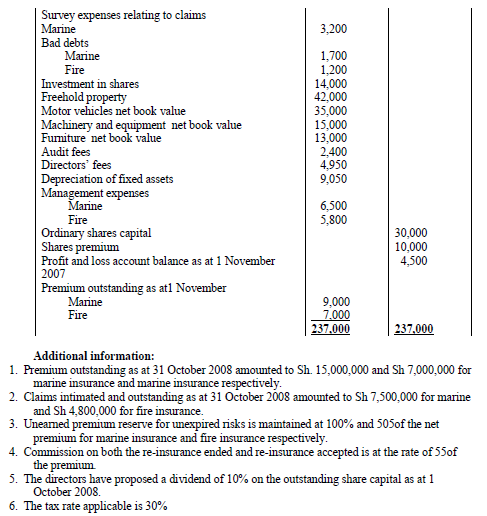

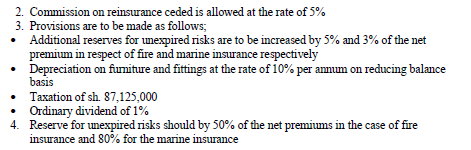

Bima Insurance Ltd specializes in general insurance business. The following trial balance was extracted from the books of the company as at 31 October 2008.

Date posted:

February 11, 2019

-

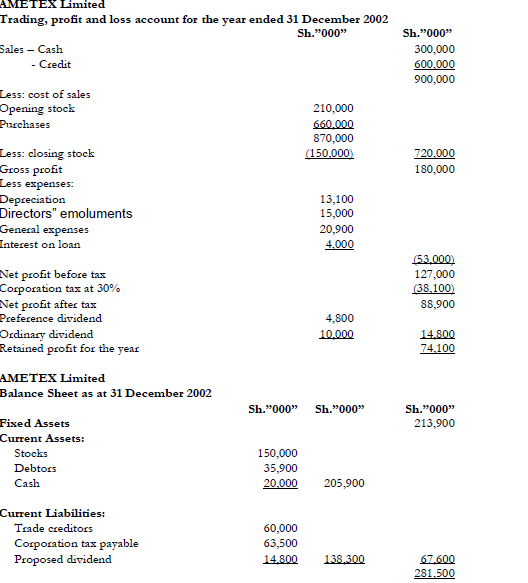

The following information represents the financial position and financial results of

AMETEX Limited for the year ended 31 December 2002.

Required:

Determine the following financial ratios:

(i) Acid test ratio.

(ii) Operating ratio

(iii) Return on total capital employed

(iv) Price earnings ratio.

(v) Interest coverage ratio

(vi) Total assets turnover

(c) Determine the working capital cycle for the company.

Required:

Determine the following financial ratios:

(i) Acid test ratio.

(ii) Operating ratio

(iii) Return on total capital employed

(iv) Price earnings ratio.

(v) Interest coverage ratio

(vi) Total assets turnover

(c) Determine the working capital cycle for the company.

Date posted:

February 11, 2019

-

Explain the meaning of the following terms as used in insurance business

i) Bonus in reduction of premium.

ii) Surrender value

Date posted:

February 11, 2019

-

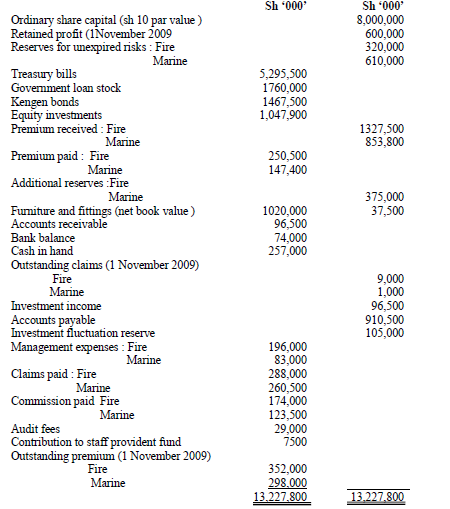

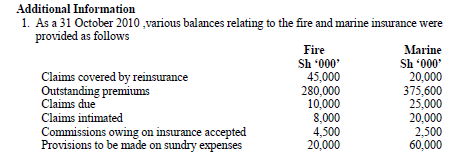

The following trial balance was extracted from the books of Umoja Insurance Company limited as at 31 October 2010

Date posted:

February 11, 2019

-

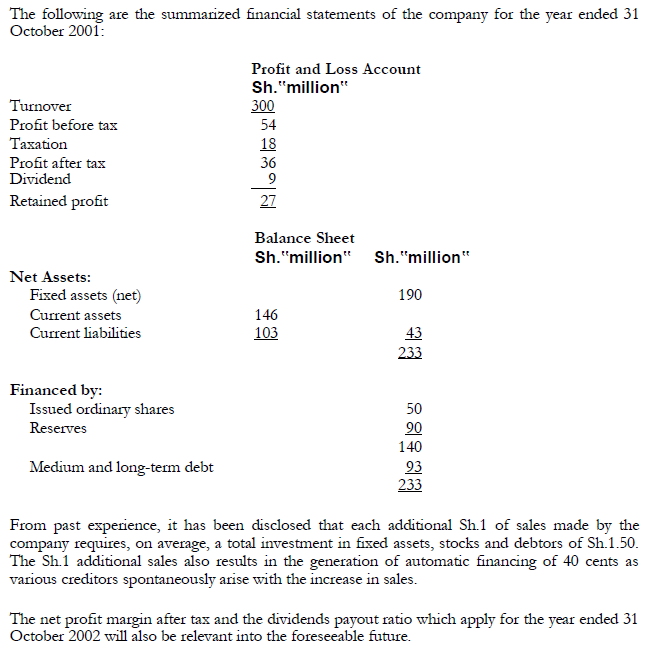

Madawa Chemicals Ltd. is in the process of forecasting its financial needs for the coming year ending 31 October 2003. The company attained a turnover of Sh.300 million for the current year ended 31 October 2002.

Required:

(a) The amount of external finance that will be needed during the year ending 31 October 2003 if sales are expected to increase by 15% in the year.

(b) The maximum expected sales growth that can be achieved in the year ending 31 October 2003 if only internally generated funds are used.

(c) The maximum growth in sales that can be achieved in the year ending 31 October 2003 if the company wishes to maintain its current level of financial gearing.

(d) Briefly comment upon the weaknesses of the method of forecasting used above.

Required:

(a) The amount of external finance that will be needed during the year ending 31 October 2003 if sales are expected to increase by 15% in the year.

(b) The maximum expected sales growth that can be achieved in the year ending 31 October 2003 if only internally generated funds are used.

(c) The maximum growth in sales that can be achieved in the year ending 31 October 2003 if the company wishes to maintain its current level of financial gearing.

(d) Briefly comment upon the weaknesses of the method of forecasting used above.

Date posted:

February 11, 2019

-

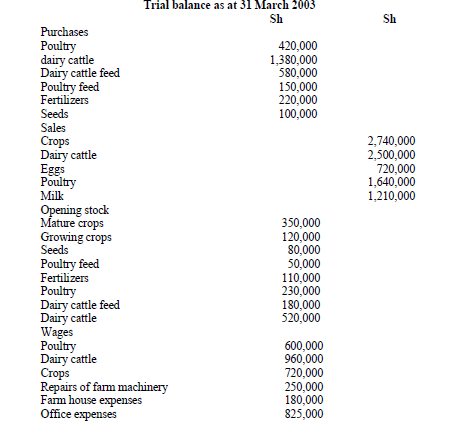

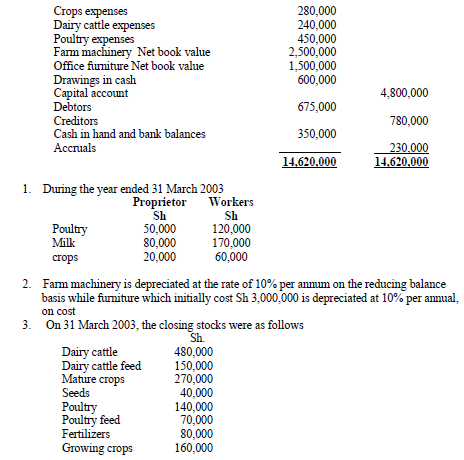

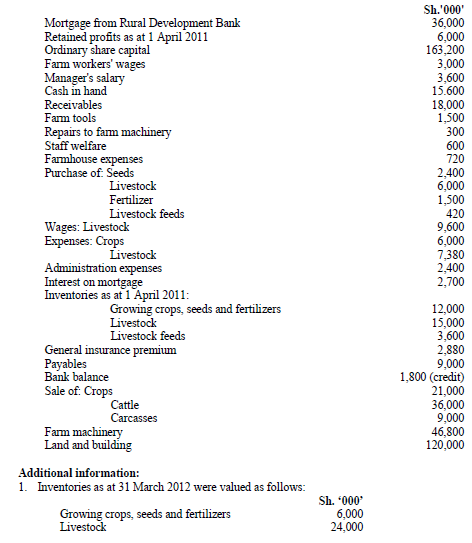

The following information was extracted from the books of Moses Kiprono, a farmer, for the year ended 31 March 2003.

Date posted:

February 11, 2019

-

Mwamba Limited is considering replacing a production machinery at its Mtwapa plant.

The existing machinery at the plant was bought 3 years ago at a cost of Sh.50 million. It

is expected to have a useful life of 5 more years with no scrap value at the end of this

period. The machinery could be disposed of immediately with net proceeds of Sh.35

million after tax.

The new machinery will cost Sh.80 million, with a useful life of 5 years and expected

terminal value of Sh.5 million. With the introduction of the new machinery, sales are

expected to increase by Sh.25 million per annum over the next 5 years. Variable costs

are 60 per cent of sales and the corporate tax rate is at 30 per cent per annum.

The operation of the new machinery will also require an immediate investment of Sh.8

million in working capital which will be recovered at the end of its useful life.

Installation costs of the new machinery will amount to Sh.6 million.

Assume that capital allowances are to be provided for on a straight-line basis and

Mwamba Limited's cost of capital is 12 per cent per annum.

Required:

(i) The initial cash outflow for the replacement decision.

(ii) The annual incremental after tax operating cash flows.

(iii) The NPV of the replacement decision and advise Mwamba Limited on whether

to replace the machinery.

(iv) The minimum after tax annual operating cash flows that will make the

replacement feasible

Date posted:

February 11, 2019

-

The following balances were extracted from the books of Shamba Ltd. as at 31 March 2012:

Date posted:

February 11, 2019

-

Explain the circumstances under which an entity should recognize a biological asset or agricultural produce in the context of International Accounting Standard (IAS) 41, Agriculture.

Date posted:

February 11, 2019

-

Discuss the main factors which a company should consider when determining the appropriate mix of long-term and short-term debt in its capital structure.

Date posted:

February 11, 2019

-

In the context of accounting for long-term construction contracts, briefly explain the following terms:

(i) Retention money

(ii) Escalation clause

Date posted:

February 11, 2019

-

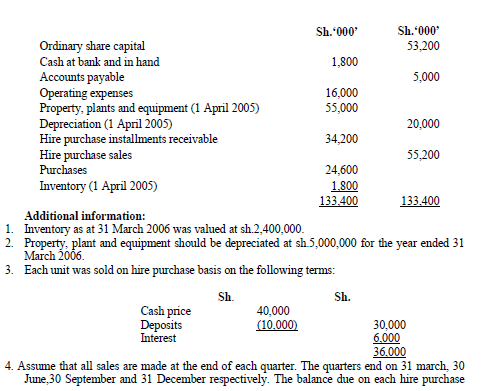

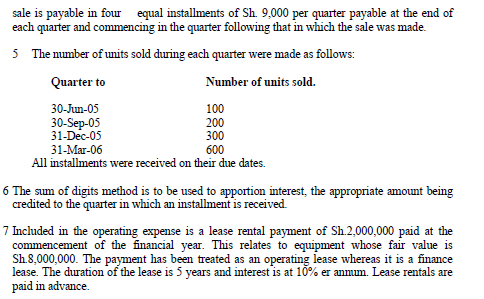

Kopesha Limited has been in business for several years dealing in electronic goods. All the firm’s goods are sold on hire purchase terms. The following trial balance extracted from the books of the firm as at 31 March 2006:

Date posted:

February 11, 2019