-

Andika visawe viwili vya nahau:

Fanya inda.

Date posted:

September 21, 2019

-

The initial velocity of a particle was 1 m/s and its acceleration is given by 2-t m/s2 every second after the start.

(i)determine the equation representing its velocity.

(ii)Find the velocity of the particle during the third second

Date posted:

September 21, 2019

-

A and B are two points on the latitude 400N. The two points lie on the longitude 800W and 1000E respectively. ( take r= 6370 km & π= 22/7)

( a ) Calculate:

(i)The distance from A to B along the parallel of latitude

(ii)The shortest distance from A to B

( b )Two planes P and Q left A for B at 400 knots and 600 knots respectively. If P flew along the great circle and q along the parallel of latitude, which one arrived earlier and by how long? Give your answer to

the nearest minute

Date posted:

September 21, 2019

-

Changanua sentensi ifuatayo kwa kielelezo cha jedwali:

Ule mkongojo ulioletewa babu utauzwa na fundi maarufu.

Date posted:

September 21, 2019

-

Ainisha virai katika sentensi ifuatayo.

Amenijibu kwa hasira.

Date posted:

September 21, 2019

-

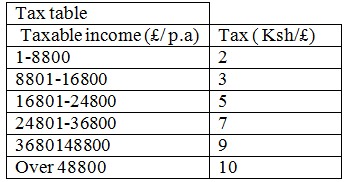

Mrs. Langat, a primary school head teacher, earns a basic salary of sh.38,300, house allowance of sh 12000 and medical allowance of sh 3600 every month. She claims a family relief of sh.1172 and insurance relief of 3% of the premium paid. Using tax rates table below:

(a)Calculate Mrs. Langat’s annual taxable income in Kenya pound per annum

(b)Tax due every month from Mrs. Langat

(c) If further deductions are made every month from her salary:

•WCPS of 2% of basic salary

•Life insuarance premium of sh4600

•Sacco loan repayment of sh 14,200

Calculate: (i) the total deductions

( ii ) her net pay for every month

(a)Calculate Mrs. Langat’s annual taxable income in Kenya pound per annum

(b)Tax due every month from Mrs. Langat

(c) If further deductions are made every month from her salary:

•WCPS of 2% of basic salary

•Life insuarance premium of sh4600

•Sacco loan repayment of sh 14,200

Calculate: (i) the total deductions

( ii ) her net pay for every month

Date posted:

September 21, 2019

-

Tumia mzizi- enye katika sentensi kama kihusishi.

Date posted:

September 21, 2019

-

Ainisha maneno katika sentensi ifuatayo:-

Shehena ya dawa ilikuwa bandarini

Date posted:

September 21, 2019

-

Onyesha muundo wa silabi katika neno wachanjwao

Date posted:

September 21, 2019

-

Andika neno lenye mfumo ufuatao wa vitamkwa. Nazali ya ufizi + kipasuo cha kaakaa gumu + irabu ya juu nyuma + kizuiwa ghuna cha kaakaa laini + irabu ya chini wastani.

Date posted:

September 21, 2019

-

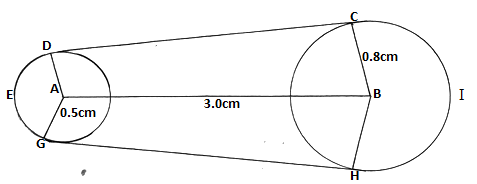

The diagram below shows a design model of a race course drawn to scale of 1:5000,000. It consists of two circles centre A and B radii 0.5cm and 0.8cm respectively and the distance between their centres is 3.0cm

Calculate in km:

(i) The length of leg CD

(ii) The length of the leg DEG (π=3.142)

(iii) The length of the leg HIC (π=3.142)

(iv) During a race, the course is manned by race officials placed 500m apart and each is paid Kshs.2300/= per day. How much is needed to pay race officials for one day event

Calculate in km:

(i) The length of leg CD

(ii) The length of the leg DEG (π=3.142)

(iii) The length of the leg HIC (π=3.142)

(iv) During a race, the course is manned by race officials placed 500m apart and each is paid Kshs.2300/= per day. How much is needed to pay race officials for one day event

Date posted:

September 20, 2019

-

In a certain country, the probability of a school A topping in county exams is 1/3. If it tops the probability of it topping in KCSE is 5/7 otherwise the probability of it topping in KCSE is 2/9. If the school tops in KCSE the probability of its appearing in the newspaper is 2/5, otherwise the probability of its appearing in newspaper is 4/11

(a) Draw a tree diagram to represent the above information

(b) Use the tree diagram to find the probability that:

(i) The school tops in the two exams and appears in the newspaper

(ii) The school did not appear in the newspaper

(iii) The school topped in at least one exam and did not appear in the newspaper

(iv) The school appeared in the newspaper

Date posted:

September 20, 2019

-

A passenger plane takes off from airport A(60oN,5oE) and flies directly to another airport B(60oN,17oE) and then flies due North for 600 nautical miles (nm) another airport C

(a) Find the position of airport C

(b) Find the distance between airport A and B in nautical miles

(c) If the plane at an average speed of 300knots, find total flight time

(d)Given that the plane left air port A at 9.20am. Find the local time of arrival at airport C

Date posted:

September 20, 2019

-

A solution whose volume is 120 litres is made up of 35% water and the rest alcohol. When y litres of alcohol is added the percentage of water drops to 15%

(a) Find the value of y

(b) The new solution is diluted further by addition of seventy litres of water. Calculate the percentage of alcohol in the resulting solution

(c) A blend is made by mixing 10 litres of the solution in (b) above with 20 liters of the original solution.

Calculate in the simplest form, the ratio of water to that of alcohol in the blend

Date posted:

September 20, 2019

-

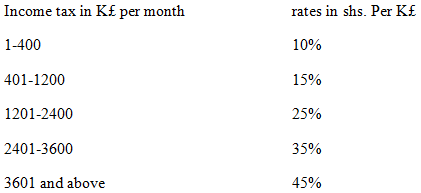

Mr. Alvin George, a civil servant gets a monthly salary of Shs. 48,000. He lives in a government house where he pays nominal rent of Shs.2500. Besides this he gets an automatic house allowance of Shs.12000 and medical allowance of shs.8000 per month. He gets a family relief of sh.1065 per month. The rates of income tax are shown below

Calculate:

(a) His taxable income per month in Kenya pounds

(b) Net tax per month in Kshs.

(c) Net salary

Calculate:

(a) His taxable income per month in Kenya pounds

(b) Net tax per month in Kshs.

(c) Net salary

Date posted:

September 20, 2019

-

A rectangle ABCD is such that AB=6cm, and BC=5cm. A variable point P moves inside the rectangle such that AP ≤ PB and AP >2.5cm. Show the region where P lies

Date posted:

September 20, 2019

-

(a) Expand and simplify the binomial expression (2x-y)5

(b) Use the first four terms of the expansion above to approximate the value of (3.8)5

Date posted:

September 20, 2019

-

An arithmetic progression of 41 terms in such that the sum of the first five terms is 560 and sum of the last five terms is -250. Find the first term

Date posted:

September 20, 2019

-

Miss Jaber bought a motor cycle at Shs.160,000. The depreciation rate was 6% per annum determined semi annually. How long will it take the motor cycle to be valued at a quarter of its original cost.

Date posted:

September 20, 2019

-

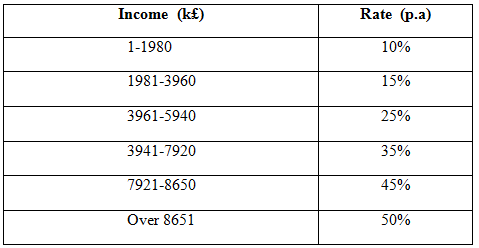

The table below gives the income tax rates.

a)Calculate income tax of Wanga’s taxable income of kshs.50,400 per month allowing a family relief of kshs. 520 per month.

b)Calculate the total tax as a percentage of taxable income

a)Calculate income tax of Wanga’s taxable income of kshs.50,400 per month allowing a family relief of kshs. 520 per month.

b)Calculate the total tax as a percentage of taxable income

Date posted:

September 20, 2019

-

Write the expression of (2 – 1/5 x)6 up to the term in x4. Hence use the expansion to find the value of (1.96)6 correct to 3 decimal places.

Date posted:

September 20, 2019

-

The position vectors of points A and B are a = 2i + j – 8k and b = 3i +2j – 2k respectively. Find the magnitude of AB.

Date posted:

September 20, 2019

-

A quantity P varies partly as t and partly as the square of t.When t = 20, p = 45 , and when t = 24 , p = 60.

a)Express p in terms of t.

b)Find p when t = 32.

Date posted:

September 20, 2019

-

Express the recurring decimal below as a fraction; 4.372 leaving your answer in the form of a/b where a and b are integers.

Date posted:

September 20, 2019

-

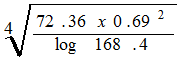

Use logarithms only to evaluate,

Correct to four significant figures.

Correct to four significant figures.

Date posted:

September 20, 2019

-

(a) Complete the table below for the function:

(b) Use the mid-ordinate rule with six ordinates to estimate the area enclosed by the curve of the functions y = x2 – 3x + 5, x – axis and the lines x = 2 and x = 8.

(c) Find the exact area of the region described in (b) above.

(d) If the mid-ordinates rule is used to estimate the area under the curve between x = 2 and x = 8, what will be the percentage error in the estimation?

(b) Use the mid-ordinate rule with six ordinates to estimate the area enclosed by the curve of the functions y = x2 – 3x + 5, x – axis and the lines x = 2 and x = 8.

(c) Find the exact area of the region described in (b) above.

(d) If the mid-ordinates rule is used to estimate the area under the curve between x = 2 and x = 8, what will be the percentage error in the estimation?

Date posted:

September 20, 2019

-

A farmer has at least 50 acres of land on which he plans to plant potatoes and cabbages.

Each acre of potatoes requires 6 men and each acre of cabbages requires 2 men. The farmer has 240 men available and he must plant at least 10 acres of potatoes. The profit on potatoes is Ksh. 1000 per acre and on cabbages is Ksh. 1200 per acre. If he plants x acres of potatoes and y acres of cabbages:

(a)Write down three inequalities in x and y to describe this information.

(b)Represent these inequalities graphically.

Date posted:

September 20, 2019

-

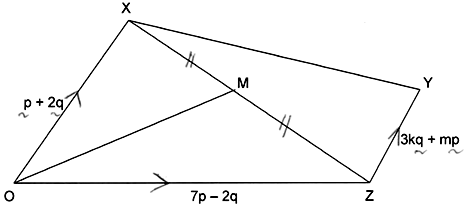

In the diagram M is the midpoint of XZ. OX = p + 2q. Oz = 7p – 2q and ZY = 3Kq + Mp where

k, and m are constants.

(a)Express the following in terms of p and q.

(i) XZ

(ii) XM

(iii) OM

(b)Express OY in terms of p, q, k and m.

(c)If y lies on OM produced with OY:OM = 3:2. Find the values of k and m.

(a)Express the following in terms of p and q.

(i) XZ

(ii) XM

(iii) OM

(b)Express OY in terms of p, q, k and m.

(c)If y lies on OM produced with OY:OM = 3:2. Find the values of k and m.

Date posted:

September 20, 2019

-

A blender mixes two brands of Juice A and B to obtain 70mls of the mixture worth Ksh. 165 per litre. If brand A is valued at Ksh. 168 per 1 litre bottle and brand B at Ksh. 153 per 1 litre bottle, calculate the ratio in which the bands A and B are mixed.

Date posted:

September 20, 2019

-

A circle whose equation is (x – 1)2 + (y – k)2 = 10 passes through point (2,5). Find the coordinates of the two possible centres of the circle.

Date posted:

September 20, 2019