-

Malikia Guyo borrowed Sh.1, 000,000 from Huduma Bank at an annual compound interest of 14% on the reducing balance. The loan was repayable in annual instalments over a period of four years. The installments were payable at end of the year.

Required:

A loan amortisation schedule.

Date posted:

March 30, 2022

-

Shadrack Chando borrowed Sh.80,000 from XYZ commercial bank at an interest rate of 1.25% compounded monthly. The loan is to be amortized using the reducing balance method and be repaid in 12 equal monthly installments payable at the end of each month.

Required:

A loan amortization schedule.

Date posted:

March 30, 2022

-

John Matata has just borrowed Sh.220,000 from a bank payable at 12% per annum compounded annually to be repaid in six equal annual instalments.

These payments are to be sufficient to repay the principal amount together with interest.

Required;-

The loan amortization schedule.

Date posted:

March 30, 2022

-

Explain four reasons that may drive a company to raise equity finance rather than debt finance.

Date posted:

March 30, 2022

-

In relation to the financial objectives of a business entity, distinguish between the terms “maximizing” and “satisficing”.

Date posted:

March 30, 2022

-

Explain three causes of conflict of interest between shareholders and debt holders.

Date posted:

March 30, 2022

-

Executive compensation plans hinder value creation in a company. Citing three reasons, justify the above statement.

Date posted:

March 30, 2022

-

Gopher Ltd has issued 300,000 ordinary shares of £1 each, which are at present selling for £4 per share. The company plans to issue rights to purchase one new equity share at a price of £3.20 per share for every 3 shares held. A shareholder who owns 900 shares thinks that he will suffer a loss in his personal wealth because the new shares are being offered at a price lower than market value. On the assumption that the actual market value of shares will be equal to the theoretical ex-rights price, what would be the effect on the shareholder's wealth if:

(a) He sells all the rights;

(b) He exercises one half of the rights and sells the other half;

(c) He does nothing at all?

Date posted:

December 15, 2021

-

The Independent Film Company plc is a film company which purchases distribution rights on films from small independent producers, and sells the films on to cinema chains for national and international screening. In recent years the company has found it difficult to source sufficient films to maintain profitability. In response to the problem, the Independent Film Company has decided to invest in commissioning and producing films in its own right. In order to gain the expertise for this venture, the Independent Film Company is considering purchasing an existing

filmmaking concern, at a cost of Sh.400,000. The main difficult that is anticipated for the business is the increasing uncertainty as to the potential success/failure rate of independently produced films. Many cinema chains are adopting a policy of only buying films from large international film companies, as they believe that the market for independent films is very limited and specialist in nature. The Independent Film Company is prepared for the fact that they are likely to have more films that fail than that succeed, but believe that the proposed film

production business will nonetheless be profitable.

Using data collection from the existing distribution business and discussions with industry

experts, they have produced cost and revenue forecasts for the five years of operation of the

proposed investment. The company aims to complete the production of three films per year.

The after tax cost of capital for the company is estimated to be 14%.

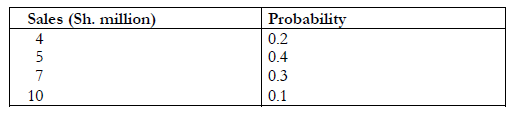

Year 1 sales for the new business are uncertain, but expected to be in the range of Sh.4-10

million. Probability estimates for different forecast values are as follows:

Sales are expected to grow at an annual rate of 5%.

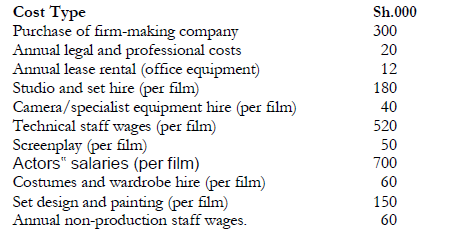

Anticipated costs related to the new business are as follows:

Sales are expected to grow at an annual rate of 5%.

Anticipated costs related to the new business are as follows:

Additional Information

(i) No capital allowances are available.

(ii) Tax is payable one year in arrears, at a rate of 33% and full use can be made of tax

refunds as they fall due.

(iii) Staff wages (technical and non-production staff) and actors‟ salaries, are

expected to rise by 10% per annum.

(iv) Studio hire costs will be subject to an increase of 30% in Year 3.

(v) Screenplay costs per film are expected to rise by 15% per annum due to a shortage of

skilled writers.

(vi) The new business will occupy office accommodation which has to date been let out for

an annual rent of Sh.20,000. Demand for such accommodation is buoyant and the

company anticipates in finding future tenants at the same annual rent.

(vii) A market research survey into the potential for the film production business cost Sh.25,000.

Required:

Using DCF analysis, calculate the expected Net Present Value of the proposed investment.

(Workings should be rounded to the nearest Sh.‟000‟)

Additional Information

(i) No capital allowances are available.

(ii) Tax is payable one year in arrears, at a rate of 33% and full use can be made of tax

refunds as they fall due.

(iii) Staff wages (technical and non-production staff) and actors‟ salaries, are

expected to rise by 10% per annum.

(iv) Studio hire costs will be subject to an increase of 30% in Year 3.

(v) Screenplay costs per film are expected to rise by 15% per annum due to a shortage of

skilled writers.

(vi) The new business will occupy office accommodation which has to date been let out for

an annual rent of Sh.20,000. Demand for such accommodation is buoyant and the

company anticipates in finding future tenants at the same annual rent.

(vii) A market research survey into the potential for the film production business cost Sh.25,000.

Required:

Using DCF analysis, calculate the expected Net Present Value of the proposed investment.

(Workings should be rounded to the nearest Sh.‟000‟)

Date posted:

December 15, 2021

-

Write notes on the following cash management models:

(i) The Baumol model.

(ii) The Miller – Orr model.

Date posted:

December 15, 2021

-

List three advantages to the management of a company for knowing who their shareholders are.

Date posted:

December 15, 2021

-

Describe four non-financial objectives that a company might pursue that have the effect of limiting the achievement of the financial objectives.

Date posted:

December 15, 2021

-

In a company, an agency problem may exist between management and shareholders on one hand and the debt holders (creditors and lenders) on the other because management and shareholders, who own and control the company have the incentive to enter into transactions that may transfer wealth from debt holders to shareholders. Hence the need for agreements by debt holders in lending contracts.

Required:

(a) State and explain any four actions or transactions by management and shareholders that could be harmful to the interests of debt holders (sources of conflict).

(b) Write short notes on any four restrictive covenants that debt holders may use to protect their wealth from management and shareholder raids.

Date posted:

December 14, 2021

-

List and explain five factors that should be taken into account by a businessman in making the choice between financing by short-term and long-term sources.

Date posted:

December 14, 2021

-

Explain the benefits that are enjoyed by investors because of the existence of organized security exchanges.

Date posted:

December 14, 2021

-

State and explain the types of euro-currency loans.

Date posted:

April 15, 2021

-

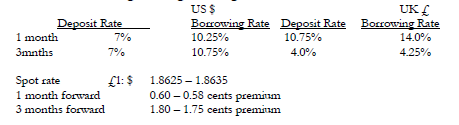

XYZ Ltd, a UK firm has bought goods from a US supplier and must pay USD 4 million in 3 months time.

The company finance director wishes to hedge against the foreign exchange risk and is considering 3

methods:

- Using the forward exchange contract

- Using the money market hedge

- Using a lead payments

Annual interest rate and foreign exchange rate are given below:

Required

Advise the company on the best method to use.

Required

Advise the company on the best method to use.

Date posted:

April 15, 2021

-

Assume that the foreign currency (F) has been quoted against the £ as follows :

Spot rate £1: F2156 – 2166

3 months forward rate £1: F2207 – 2222

Required:

1. Determine the amount required in sterling pound to buy 2 million foreign currencies

• At the spot

• In 3 months time under the forward exchange contract.

2. Compute the amount a customer would get if he were to sell 2 million foreign currency.

• At the spot rate

• In 3 months time under forward exchange contract

Date posted:

April 15, 2021

-

Assume that the direct quote is deuchemark is DM 1 - USD 0.5 while the general interest rate in US is

6% and general interest rate in Germany is 3%.

Required:

Compute the percentage change in direct quote and the new exchange rate.

Date posted:

April 15, 2021

-

XYZ Ltd has an issued share capital of 10 million ordinary shares with a par value of £1, on which it pays a

constant dividend of £0.4 per share. The market value per share was £2 ex-dividend.

The company then proposed a 1 for 4 rights issue with an issue price of £1.50. The money raised would be

used to finance a major new project, which was expected to increase annual profits after taxation by

£950,000. This information is released together with the announcement of rights issue.

Required:

(a) Compute the cum-right price at the eve-of the rights issue

(b) Compute the theoretical ex-rights price

(c) Calculate the market price per share at the time of the rights issue if the money raised was to be used

to redeem £3,750,000 of 8% debentures. The tax rate is 50%.

Date posted:

April 15, 2021

-

Assume that the following information has been obtained:

P = Sh 20

X = Sh 20

t = 3 months (0.25 years)

KRF = 12%

δ² = 0.16

Determine the value of the option.

Date posted:

April 14, 2021

-

ABC Ltd has decided to acquire a piece of equipment costing Shs 240 000 of five years. The

equipment is expected to have no salvage value ate the end and the company uses straight-line

depreciation method on all it Fixed Assets. The company has two financing alternative methods

available, leasing or borrowing.

The loan has an interest rate of 15% requiring equal-year-end installments to be paid. The lease

would be set at a level that would amortize the cost of equipment over the lease period and would

provide the lessor with a 14% return on capital. The company’s tax rate is 40%.

Required:

a. Compute the annual lease payments.

b. Compute the PV of the cash out flow under lease financing

c. Calculate the annual loan installment payment

d. For each of the 5 years, calculate the interest and the principal component of the loan

repayment.

e. Calculate the PV of after tax cash flow under the loan alternative

f. Which alternative is better and why?

Date posted:

April 14, 2021

-

A company negotiates a Sh 30 million loan for eight years from a financial institution. The interest rate is 14% per annum on the outstanding balance of the loan. The principal and interest will be repaid in eight equal year-end instalments.

Required

Prepare a loan repayment schedule

Date posted:

April 14, 2021

-

A company currently has Shs 20 000 000, 12% debenture issue outstanding which has 20 years remaining to maturity. The company can now sell a Shs 20 million 20 year bond or debenture with a normal or coupon rate of 20% that will net Shs 19.6 million, after the underwriting expenses of the old bond. The core premium and the unamortized discount of the old bond

are deductible as expenses in the year of refunding. The old issue has Shs 200 000 unamortized

discounts outstanding and unamortized legal fee of Shs 100 000. The core right of old bond is

Shs 109 and the issuing expenses on the new bond are Shs 150, 000 and there is a 30 day period

of interest overlap. Assume that the effective income tax is 50%.

Required:

Advice the company on whether to replace the old issue with the new bonds.

Date posted:

April 14, 2021

-

XYZ Ltd has 900,000 shares outstanding at current market price of Sh 130 per share. The company

needs Sh 22,500,000 to finance its proposed expansion. The board of directors has decided to issue

rights for raising the required funds. The subscription price has been fixed at Sh 75 per share.

Required:

(a) How many rights are required to purchase one new share?

(b) What is the price of one share after the rights issue (Ex-right price)?

(c) Compute the theoretical value of each right

(d) Consider the effect of the rights issue on the shareholders' wealth under the three options

available to the shareholders (Assume he owns 3 shares and has Sh 75 cash on hand).

Date posted:

April 14, 2021

-

Companies U and L are identical in every respect except that U is unlevered while L has Sh 10 million of 5% bonds outstanding. Assume

(a) That all of the MM assumptions are met

(b) That there are no corporate or personal taxes

(c) That EBIT is Sh 2 million

(d) That the cost of equity to company U is 10%

Required:

i. Determine the value MM would estimate for each firm

ii. Determine the cost of equity for both firms

iii. What is the overall cost of capital for both firms

iv. Suppose the value of U is Sh 20 million and that of L is Sh 22 million. Explain the arbitrage process for a shareholder who owns 10% of company L's shares.

Date posted:

April 14, 2021

-

Company A and B are in the same risk class and are identical in every respect except that Company A is

geared while B is not. Company A has Sh 6 million in 5% bonds outstanding. Both companies earn 10%

before interest and taxes on their Sh 10 million total assets. Assume perfect capital markets, rational

investors, a tax rate of 60% and a capitalization rate of 10% for an all equity company.

Required:

(a) Compute the value of firms A and B using the net income (NI) approach and Net operating income

(NOI) approach.

(b) Using the NOI approach, calculate the after tax weighted average cost of capital for firms A and B.

Which of these firms has the optimal capital structure according to NOI approach? Why?

(c) According to the NOI approach, the values of firms A and B computed in (a) are not in equilibrium.

Assuming that you own 10% of A's shares, show the process which will give you the same amount of

income but at less cost. At what point would this process stop?

Date posted:

April 14, 2021

-

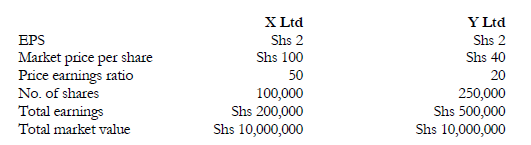

X Ltd intends to take-over Y Ltd by offering two of its share for every five shares in Y Company Ltd.

Relevant financial data is as follows:

Required.

a. Compute the combined EPS & MPS

b. Has wealth been created for shareholders?

Required.

a. Compute the combined EPS & MPS

b. Has wealth been created for shareholders?

Date posted:

April 14, 2021

-

The following data are pertinent for companies A and B.

a. If the two companies were to merge and the exchange ratio were one share of Company A for each share of Company B, what would be the initial impact on earnings per share of the two companies? what is the market value exchange ratio? Is the merger likely to take place?

b. If the exchange ratio were two shares of Company A for each share of Company B what would happen with respect to the above?

c. If the exchange ratio were 1.5 shares of Company A for each share of Company B, what would happen?

d. What exchange ratio would you recommend?

a. If the two companies were to merge and the exchange ratio were one share of Company A for each share of Company B, what would be the initial impact on earnings per share of the two companies? what is the market value exchange ratio? Is the merger likely to take place?

b. If the exchange ratio were two shares of Company A for each share of Company B what would happen with respect to the above?

c. If the exchange ratio were 1.5 shares of Company A for each share of Company B, what would happen?

d. What exchange ratio would you recommend?

Date posted:

April 14, 2021

-

XYZ Ltd. is considered acquiring ABC Ltd. The following information relates to ABC Ltd. for the next five years. The projected financial data are for the post-merger period. The corporate tax rate is 40% for both companies.

Other information

a. After the fifth year the cashflows available to XYZ from ABC is expected to grow by 10% per

annum in perpetuity.

b. ABC will retain Shs 40,000 for internal expansion every year.

c. The cost of capital can be assumed to be 18%.

REQUIRED:

i. Estimate the annual cash flows.

ii. Determine the maximum amount XYZ would be willing to acquire ABC at.

Other information

a. After the fifth year the cashflows available to XYZ from ABC is expected to grow by 10% per

annum in perpetuity.

b. ABC will retain Shs 40,000 for internal expansion every year.

c. The cost of capital can be assumed to be 18%.

REQUIRED:

i. Estimate the annual cash flows.

ii. Determine the maximum amount XYZ would be willing to acquire ABC at.

Date posted:

April 14, 2021