-

Outline four roles of professional ethics in tax practice

Date posted:

February 13, 2019

-

Alex Karama is employed by Ziada Ltd. as a sales manager. He has provided the following information relating to his income for the year ended 31 December 2010

1. His monthly basic salary was Sh.50,000 (pay as you earn (PAYE) Sh.14,800 per month).

2. He was also entitled to a commission of 5% based on average monthly sales made in a year. The average sales per month during the year amounted to Sh.l04,400 inclusive of value added tax (VAT) at the rate of 16%.

3. He lived in a company house until 30 September 2010 and paid a nominal rent of Sh.5,000 for the house. The market rental value of houses in the estate was Sh.50,000 per month.

4. He was provided with a company car of 2400 cc whose cost at the time of purchase was Sh.800,000. The car was purchased in year 2008. Depreciation on motor vehicles is at the rate of 20% per annum on cost

5. The education fees for his two daughters amounting to Sh360,000 were paid by the company The company had not debited the fees in the statement of comprehensive income for the year ended 31 December 2010

6. He purchased a house and moved in on 1 October 2010, through a mortgage loan of Sh.5,000,000 at an interest rate of 12% per annum. The initial deposit of Sh.1,400,000 was advanced to him by the company at an interest rate of 8% per annum. The market interest rate during the period was 10% per annum.

7. He is a member of a home ownership savings plan, and contributed Sh.5,000 per month up to the acquired the mortgage loan.

8. He has a life assurance policy where the company paid Sh.10,000 for him per month.

9. He holds 12% of the share capital of Ziada Ltd. while his wife controls 6% of the share capital in the company

10. Both Mr Alex Karama and the wife contributed to a registered pension scheme Sh.36,000 per month while the employer contributed an equal amount.

11. He received dividends from Chai Co-operative Society Ltd. of Sh.34,000 (net) and interest on 30 year infrastructure bonds of Sh.36,000 (gross) during the year.

12. He received a monthly pension ofSh.25,000 from a previous employer.

13. His other income during the year included:

- Professional loss for the year Sh.64,000 (part-time consultancy).

- Rental income Sh.420,000 excluding cost of purchase of furniture Sh.90,000.

- Farming loss Sh.124,000.

Compute for Mr Alex Karama for the year ended 31 December 2010:

(i) Taxable income.

(ii) Tax liability.

Date posted:

February 13, 2019

-

The use of materials of lead in roofing and in water pipes is being discouraged.

State

(i)Two reasons why these materials have been used in the past.

(ii)One reason why their use is being discouraged.

Date posted:

February 13, 2019

-

State the cardinal rule in taxation of employment income in your country

Date posted:

February 13, 2019

-

Comment on the treatment of the following items for tax purposes

i) Education fees paid by an educational institution for income employees‘ dependents attending the institution

ii) Income received for disabled persons

iii) Non-cash benefits

iv) Medical benefits provided to non-whole time service director

v) Registered employee share ownership plans

Date posted:

February 13, 2019

-

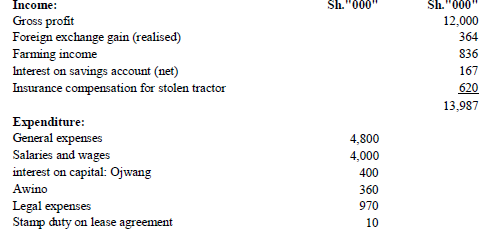

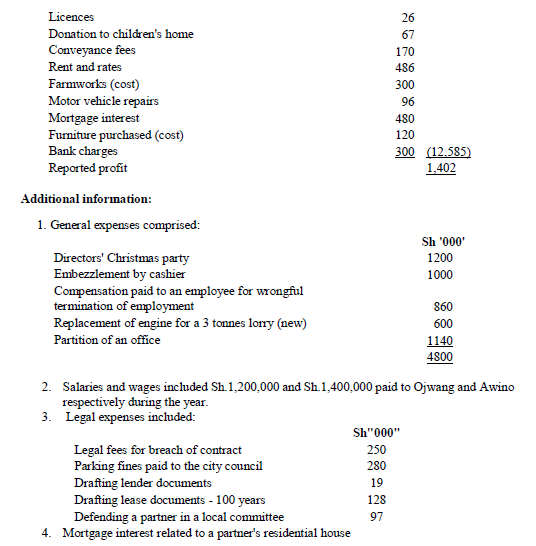

Ojwang, Awino and Ochieng are partners trading as Okode Enterprises. Ojwang and Awino are active partners while Ochieng is a sleeping partner. The partnership agreement was silent on the profit and loss sharing ratio.

The partners have presented the following statement of comprehensive income for the year ended

Required:

(i) The adjusted partnership profit or loss for the year ended 31 December 2011

(ii) Distribution schedule of the profit or loss calculated in (i) above

Required:

(i) The adjusted partnership profit or loss for the year ended 31 December 2011

(ii) Distribution schedule of the profit or loss calculated in (i) above

Date posted:

February 13, 2019

-

Abiud Kageni is an employee of Tala Ltd. He has provided the following details relating to his employment income and other benefits for the year ended 31 December 2011.

1. Monthly salary Sh 124,000 (PAYE tax Sh34,100)

2. School fees for his daughter amounting to Sh.64,000 was paid by the employer and deducted as an expense

3. His monthly salary was increased on 1 December 2011, by Sh.20,000 and backdated to 1 September 2011.

4. The company provided him with airtime worth Sh.5,000 per month. It was estimated that 50% of his calls were non-business related.

5. Passages to facilitate his family to move from South Africa to Kenya amounted to Sh.150,000

6. A fully furnished house whose cost of furniture was Sh.240,000.

7. A life insurance cover whose annual Insurance premium amounted to Sh.72,000.

8. A motor vehicle (2000 cc) whose cost was Sh.600,000 at the time of purchase on 1 January 2008.

9. AbiudKageni controls 15% of the share capital of the company. The company gave the wife free gifts valued at Sh.25,000 during the end of year party.

10. He is a member of the company's registered pension scheme where he contributes 20% of his basic salary. The employer contributes an equal amount.

11. The company gave AbiudKageni a loan of Sh.5,000,000 at an interest rate of 4% per annum. The market interest rate is 9% per annum.

12. The company paid medical bills amounting to Sh.1,200,000 following hospitalization of his son.

13. AbiudKageni's other incomes included: Farming loss Sh.194,000

Rental income Sh.240,000

Compute the following for the year ended 31 December 20 I I:

(i) Taxable income for Abiud Kageni.

(ii) Tax liability (if any) on the income in (i) above.

(iii) Fringe benefit tax.

Date posted:

February 13, 2019

-

The management of Ndimu Ltd. has presented the following statement of comprehensive income for the year ended 31 December 2011

Required:

(i) Adjusted taxable profit or loss for Ndimu Ltd. for the year ended 31 December

(ii) The tax thereon (if any).

Required:

(i) Adjusted taxable profit or loss for Ndimu Ltd. for the year ended 31 December

(ii) The tax thereon (if any).

Date posted:

February 13, 2019

-

Outline four conditions which must be fulfilled for passage to be excluded from taxation of an employee's income.

Date posted:

February 13, 2019

-

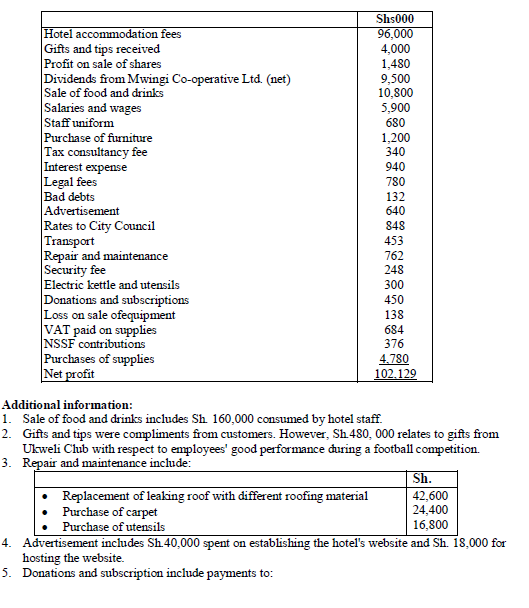

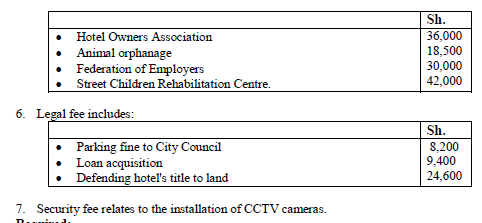

Limuru Enterprises Ltd. operates a hotel complex in Nairobi. The hotel presented the following set of data from the accounting records for the year ended 31 December 2011:

Prepare A statement of adjusted taxable profit or loss for Limuru Enterprises Ltd for the year ended 31 December 2011.

Prepare A statement of adjusted taxable profit or loss for Limuru Enterprises Ltd for the year ended 31 December 2011.

Date posted:

February 13, 2019

-

Highlight three circumstances under which:

i) The income of a taxable person is assessed on another person.

ii) A married woman might be called upon to bear a tax burden.

Date posted:

February 13, 2019

-

Pearson Morry is a non-citizen, who was recruited in 2010 by a company incorporated in your country.

He reported on duty on 1 January 2011. During the year of income 2011, he provided the following details to assist him file his individual income tax return for the year of income 2011.

Required:

i) Total taxable income for Pearson Morry for the year ended 31 December 201 I.

ii) Tax payable by Pearson Morry for the year ended 31 December 2011.

Required:

i) Total taxable income for Pearson Morry for the year ended 31 December 201 I.

ii) Tax payable by Pearson Morry for the year ended 31 December 2011.

Date posted:

February 13, 2019

-

Discuss two benefits of withholding tax.

Date posted:

February 13, 2019

-

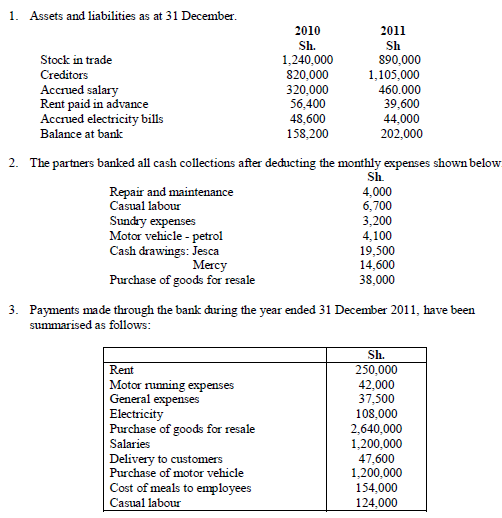

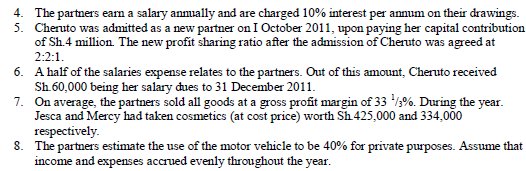

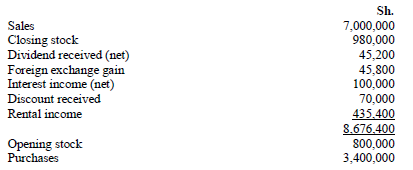

Jessica and Mercy have been operating a cosmetics retail business and sharing profits and losses equally. They have not maintained proper books of account. They have engaged you as a qualified accountant at an agreed fee of Sh.210, 000 to prepare their books and annual tax returns.

The following information was presented to you relating to the business operations for the year ended 31 December 2011

Required:

i) Taxable income for the year ended 31December 2011 in respect of each partner.

ii) Using the taxable income computed in (b) (i) above, compute the tax payable by each partner.

Required:

i) Taxable income for the year ended 31December 2011 in respect of each partner.

ii) Using the taxable income computed in (b) (i) above, compute the tax payable by each partner.

Date posted:

February 13, 2019

-

a) In the context of International Accounting Standard (IAS) 21 (The Effects of Changes in Foreign Exchange Rates), explain two factors that should be considered in determining an entity's functional currency.

b) Ufanisi Ltd. is a Kenyan-based company that uses the Kenya Shilling (Ksh) as its presentation currency. On 1 January 2010, the company established a wholly owned

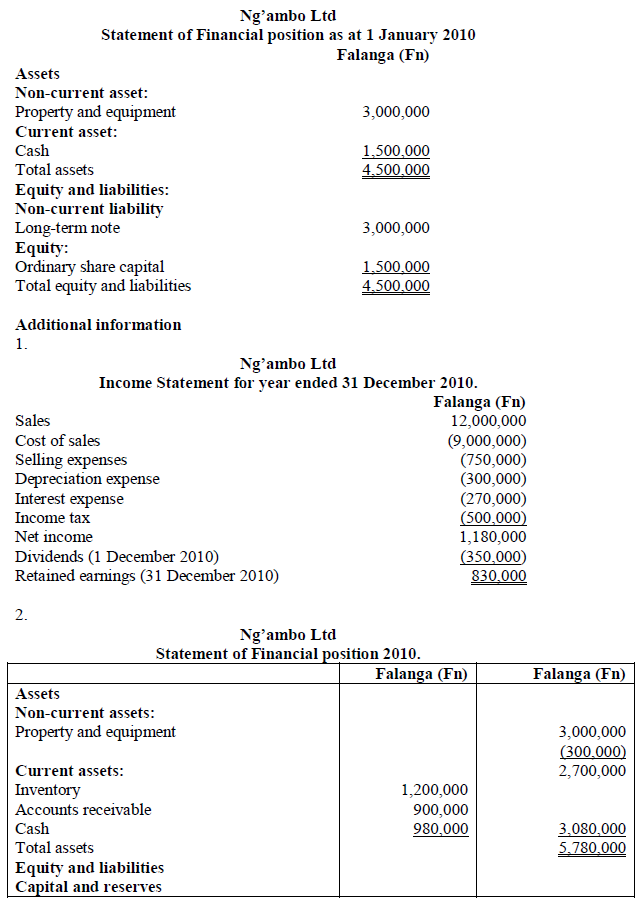

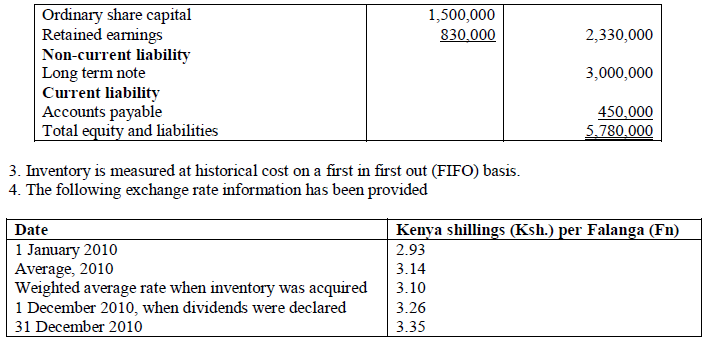

subsidiary, Ng'ambo Ltd., in a foreign country known as Ugenini, In addition to Ufanisi Ltd. making an equity investment in the subsidiary, a long term note payable to an Ugenini bank was negotiated to purchase property and equipment. The currency used in Ugenini is known as the Falanga (Fn). The subsidiary began operations with the following statement of financial position as at 1 January 2010:

Required:

Translate the following financial statements of Ng'ambo Ltd. using the temporal method:

i) Income statement for the year ended 31 December 2010.

ii) Statement of financial position as at 31 December 2010.

Required:

Translate the following financial statements of Ng'ambo Ltd. using the temporal method:

i) Income statement for the year ended 31 December 2010.

ii) Statement of financial position as at 31 December 2010.

Date posted:

February 13, 2019

-

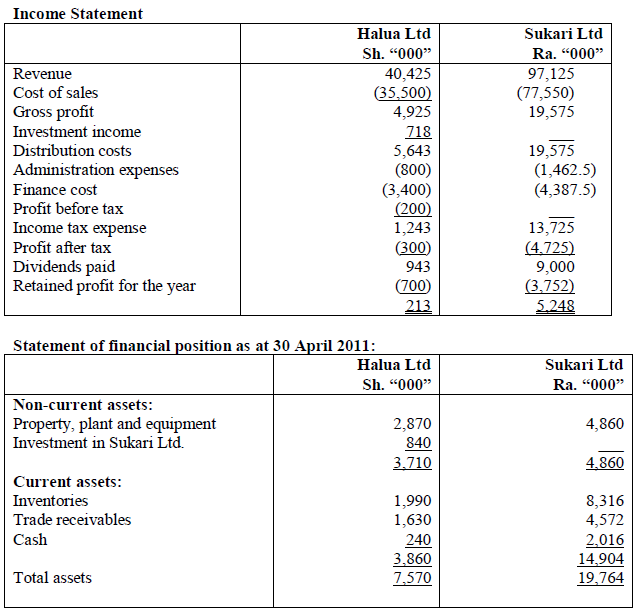

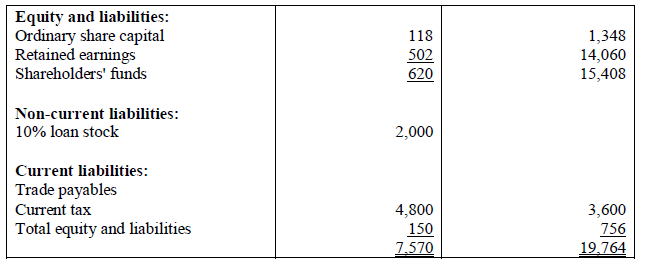

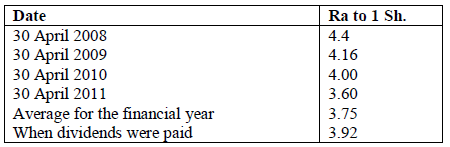

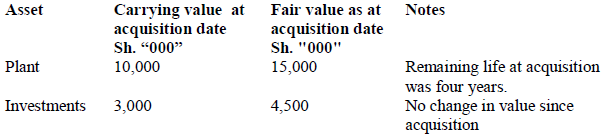

Halua Ltd., a local company, acquired 75% of the ordinary share capital of Sukari Ltd., a foreign company on 1 May 2008. Sukari Ltd.'s functional currency is the Rupia (Ra).

The following financial statements relate to the two companies for the year ended 30 April 2011:

Additional information:

1. Halua Ltd. acquired the shares in Sukari Ltd. when the retained earnings in Sukari Ltd. were Ra 2,876,000.

2. During the year, Halua Ltd. sold goods worth Sh.5 million to Sukari Ltd. and reported a gross profit margin of 20% on selling price. Half of these goods were still in the inventory of Sukari Ltd. as at the year end.

3. Included in the receivables of Halua Ltd. is Sh.500,000 due from Sukari Ltd.

4. The translation differences in the consolidated financial statements at 30 April 2010 relating to the translation of Sukari Ltd. (excluding goodwill) were Sh.208,000. Retained earnings on the same date in Sukari Ltd.'s financial statements in the post-acquisition period as at 30 April 2010 amounted to Sh. 1,372,000.

5. The group uses the partial goodwill method and no impairment loss has been reported so far.

6. The following exchange rates are relevant.

Additional information:

1. Halua Ltd. acquired the shares in Sukari Ltd. when the retained earnings in Sukari Ltd. were Ra 2,876,000.

2. During the year, Halua Ltd. sold goods worth Sh.5 million to Sukari Ltd. and reported a gross profit margin of 20% on selling price. Half of these goods were still in the inventory of Sukari Ltd. as at the year end.

3. Included in the receivables of Halua Ltd. is Sh.500,000 due from Sukari Ltd.

4. The translation differences in the consolidated financial statements at 30 April 2010 relating to the translation of Sukari Ltd. (excluding goodwill) were Sh.208,000. Retained earnings on the same date in Sukari Ltd.'s financial statements in the post-acquisition period as at 30 April 2010 amounted to Sh. 1,372,000.

5. The group uses the partial goodwill method and no impairment loss has been reported so far.

6. The following exchange rates are relevant.

Required:

a) Consolidated income statement for the year ended 30 April 2011.

b) Consolidated statement of changes in equity for the year ended 30 April 2011.

c) Consolidated statement of financial position as at 30 April 2011.

Required:

a) Consolidated income statement for the year ended 30 April 2011.

b) Consolidated statement of changes in equity for the year ended 30 April 2011.

c) Consolidated statement of financial position as at 30 April 2011.

Date posted:

February 13, 2019

-

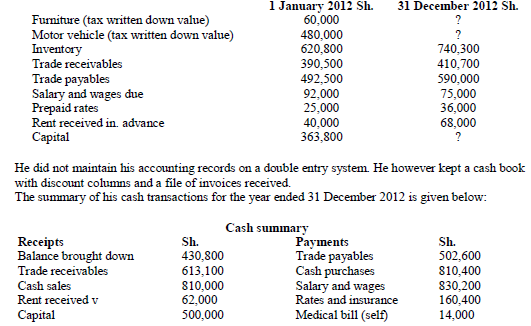

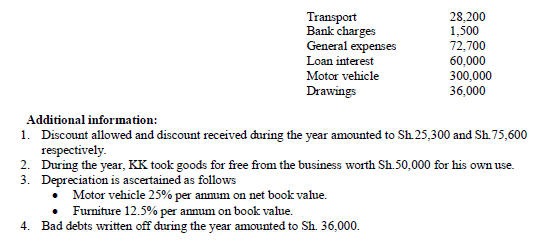

KK, a sole trader listed the following assets and liabilities as at 1 January 2012 and 31 December 2012:

Required:

i) The taxable income for KK for the year ended 31 December 2012.

ii) Tax payable by KK, if any.

Required:

i) The taxable income for KK for the year ended 31 December 2012.

ii) Tax payable by KK, if any.

Date posted:

February 13, 2019

-

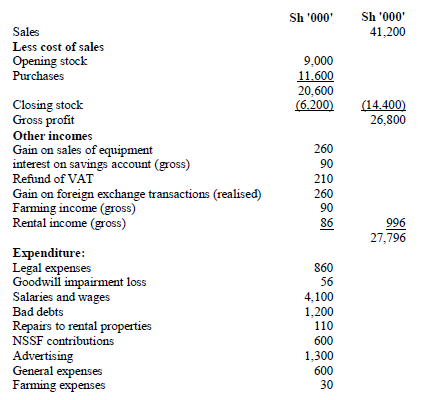

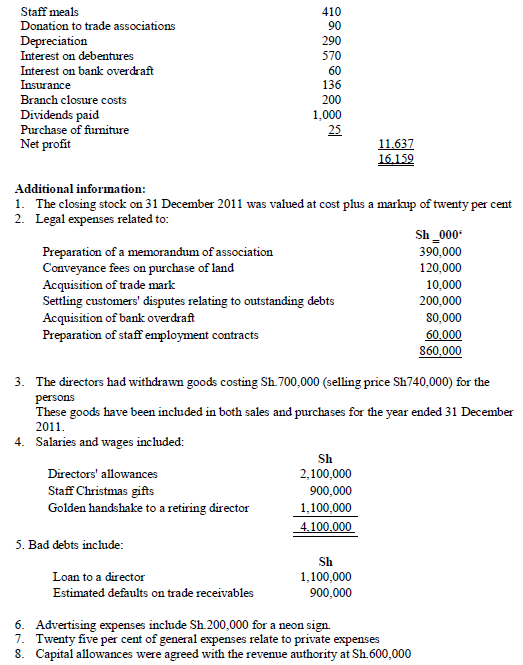

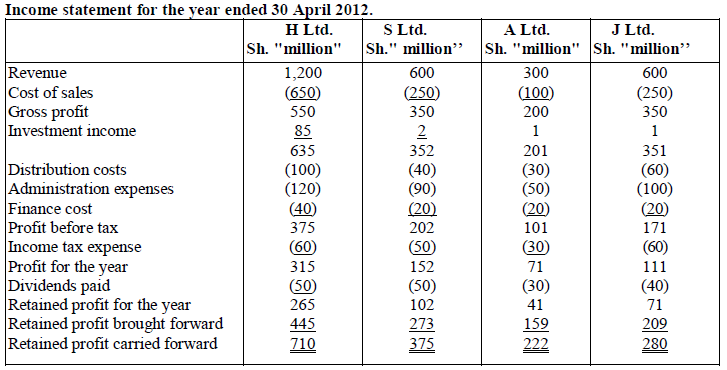

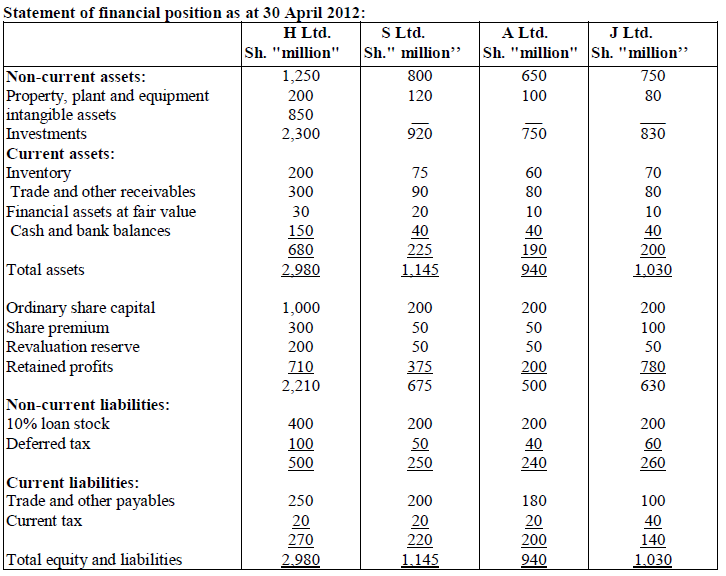

The following financial statements relate to H Ltd. and its investment companies S Ltd., A Ltd. and J Ltd. for the year ended 30 April 2012:

Additional information:

1. H Ltd, acquired the investments in the other companies as follows:

Additional information:

1. H Ltd, acquired the investments in the other companies as follows:

2. The fair value of the non-controlling interest in S Ltd. was Sh.75 million on 1 May 2008.

3. During the year ended 30 April 2012, II Ltd. sold goods lo S Ltd. and A Ltd. as follows:

2. The fair value of the non-controlling interest in S Ltd. was Sh.75 million on 1 May 2008.

3. During the year ended 30 April 2012, II Ltd. sold goods lo S Ltd. and A Ltd. as follows:

4. On 1 May 2010, H Ltd. sold S Ltd. an item of plant for Sli.200 million reporting a 25% profit on the initial cost plant. The group charges depreciation at 20% per annum on cost on plant.

5. All the goodwills of the three companies in which H Ltd. has invested are estimated to be impaired by 25% in the year ended 30 April 2012. No impairment losses have been reported in the past.

6. Included in trade and other receivables and trade and other payables arc the following outstanding balances:

- Due from S Ltd. to II Ltd. - Sh.50 million

- Due from A Ltd. to II Ltd. - Sh.10 million

- Due from H Ltd. to J Ltd. - Sh.40 million

In the books of S Ltd. the amount due to H Ltd. was shown at Sh.40 million because S Ltd. had sent a cheque Sh.10 million but H Ltd. had not recorded the cheque. All the other balances were in agreement.

7. The group uses the full goodwill method and proportionate consolidation as per IAS 31 (Joint Ventures).

8. All dividends and interest had been paid by the end of the year.

Required:

a) Consolidated income statement for the year ended 30 April 2012.

b) Consolidated statement of financial position as at 30 April 2012.

4. On 1 May 2010, H Ltd. sold S Ltd. an item of plant for Sli.200 million reporting a 25% profit on the initial cost plant. The group charges depreciation at 20% per annum on cost on plant.

5. All the goodwills of the three companies in which H Ltd. has invested are estimated to be impaired by 25% in the year ended 30 April 2012. No impairment losses have been reported in the past.

6. Included in trade and other receivables and trade and other payables arc the following outstanding balances:

- Due from S Ltd. to II Ltd. - Sh.50 million

- Due from A Ltd. to II Ltd. - Sh.10 million

- Due from H Ltd. to J Ltd. - Sh.40 million

In the books of S Ltd. the amount due to H Ltd. was shown at Sh.40 million because S Ltd. had sent a cheque Sh.10 million but H Ltd. had not recorded the cheque. All the other balances were in agreement.

7. The group uses the full goodwill method and proportionate consolidation as per IAS 31 (Joint Ventures).

8. All dividends and interest had been paid by the end of the year.

Required:

a) Consolidated income statement for the year ended 30 April 2012.

b) Consolidated statement of financial position as at 30 April 2012.

Date posted:

February 13, 2019

-

Discuss the relevance of the concept of ―residence‖ in the determination of tax liabilities for both an individual and a body corporate

Date posted:

February 13, 2019

-

Umeshi Osodo was employed by Metal Max Ltd. as a human resource manager with effect from 1 January 2012. He reported the following incomes for the year ended 31 December 2012

1. Basic salary Sh. 80,000 per month (PAYE Sh. 12,000 per month).

2. The employer paid his annual life insurance premiums at an amount equivalent to 5% of his annual basic salary.

3. He earned a net interest income of Sh. 150,000 during the year from his investments in housing development bonds.

4. The employer provided him with a house whose market rental value was Sh. 50,000 per month.

The employer deducted 5% of his basic salary per month as nominal rent.

5. Education fees for his two children amounting to Sh. 180,000 were paid by the employer during the year.

This amount was charged in the employer's income statement.

6. The employer reimbursed him for all out of pocket expenses incurred on the official use of his personal car.

In the year 2012, the amount reimbursed amounted to Sh. 180,000. He had purchased the car in the year 2010 at a cost of Sh. 900,000. The car had an engine capacity of 1600 cc.

7. He contributed Sh. 28,000 per month to a registered pension scheme. The employer contributed Sh. 18,000 per month for him to the same scheme.

8. He received entertainment allowance amounting to Sh. 40,000. He utilized the amount in celebrating his birthday together with his family.

9. He received a year-end bonus payable to executive staff of Sh. 80,000

10. The employer provided him with electricity, water, telephone and a cook at a cost of Sh. 15.000, Sh. 9,000, Sh.60,000 and Sh. 18,000 per month respectively.

11. During the year UmeshiOsodo was declared the best employee and the employer paid him a reward of Sh. 100,000.

12. He received medical benefits amounting to Sh. 420,000 from the employer. The company has a medical scheme for all staff members.

Compute the following for the year ended 31 December 2012:

i) Taxable income for Umeshi Osodo.

ii) Tax liability (if any) on the income in (i) above.

Date posted:

February 13, 2019

-

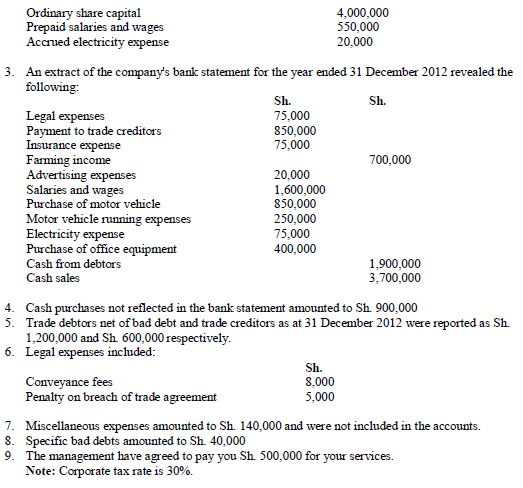

The management of Light Traders Ltd. has engaged you to ascertain the company's tax position as they have not been maintaining proper books of account. The following information has been availed to you for the year ended 31 December 2012:

1. Stock balances as at 1 January 20i2 and 31 December 2012 were Sh. 250,000 and Sh. 400,000 respectively.

2. The balance sheet extract as at 1 January 2012 revealed the following balances:

Required:

i) Adjusted taxable profit or loss for Light Traders Ltd. for the year ended 31 December 2012.

ii) Tax liability, if any.

Required:

i) Adjusted taxable profit or loss for Light Traders Ltd. for the year ended 31 December 2012.

ii) Tax liability, if any.

Date posted:

February 13, 2019

-

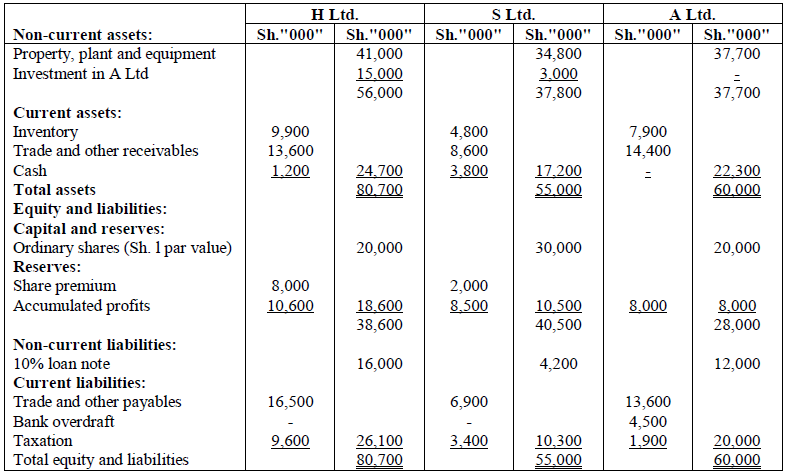

a) In the context of IAS 21 (The Effects of Changes in Foreign Exchange Rates), critically appraise the concepts on which the closing rate and the temporal methods are based indicating which factors should be taken into account when choosing between the two methods.

b) H Ltd., a publicly listed company, acquired the following investments:

- On 1 April 2012, the company purchased 24 million shares in S Ltd. This acquisition was made by way of an immediate share exchange of two shares in H Ltd. for every three shares in S Ltd. plus a cash payment of Sh. l per one share of S Ltd. This cash payment will be payable on 1 April 2015. The market price of H Ltd.'s shares on 1 April 2012 was Sh.2 each.

- On 1 October 2012, the company purchased 6 million shares in A Ltd. by paying an immediate Sh.2.50 in cash for each share.

The statements of financial position of H Ltd., S Ltd. and A Ltd. as at 31 March 2013 were as follows:

Additional information:

1. Below is a summary of the results of a fair value exercise S Ltd. carried out as at the date of acquisition:

Additional information:

1. Below is a summary of the results of a fair value exercise S Ltd. carried out as at the date of acquisition:

The book values of the net assets of A Ltd as at the date of acquisition were considered to be a reasonable approximation to their fair values.

2. The profits of S Ltd. and A Ltd. for the year to 3 1 March 2013 were Sh.4.5 million and Sh.6 million respectively. No dividends have been paid by any of the companies during the year. Profits are deemed to accrue evenly throughout the year.

3. In January 2013, A Ltd. sold goods to H Ltd. at a selling price of Sh.4 million. These goods had cost A Ltd. Sh.2.4 million. H Ltd. had Sh.2.5 million (at cost to H Ltd.) of these goods still in inventory as at 31 March 2013.

4. Depreciation is charged on a straight-line basis. A full year's depreciation is charged in the year of acquisition.

5. Based on H Ltd.'s cost of capital which is 10% per annum. Sh. l receivable in three years' time can be taken to have a present value of Sh.0.75.

6. H Ltd. has not yet accounted for the acquisition of S Ltd. but has recorded the investment in A Ltd.

Required:

Consolidated statement of financial position as at 31 March 2013 in accordance with international financial reporting standards (IFRSs)

The book values of the net assets of A Ltd as at the date of acquisition were considered to be a reasonable approximation to their fair values.

2. The profits of S Ltd. and A Ltd. for the year to 3 1 March 2013 were Sh.4.5 million and Sh.6 million respectively. No dividends have been paid by any of the companies during the year. Profits are deemed to accrue evenly throughout the year.

3. In January 2013, A Ltd. sold goods to H Ltd. at a selling price of Sh.4 million. These goods had cost A Ltd. Sh.2.4 million. H Ltd. had Sh.2.5 million (at cost to H Ltd.) of these goods still in inventory as at 31 March 2013.

4. Depreciation is charged on a straight-line basis. A full year's depreciation is charged in the year of acquisition.

5. Based on H Ltd.'s cost of capital which is 10% per annum. Sh. l receivable in three years' time can be taken to have a present value of Sh.0.75.

6. H Ltd. has not yet accounted for the acquisition of S Ltd. but has recorded the investment in A Ltd.

Required:

Consolidated statement of financial position as at 31 March 2013 in accordance with international financial reporting standards (IFRSs)

Date posted:

February 13, 2019

-

Explain the tax position in relation to irregularly paid employees

Date posted:

February 13, 2019

-

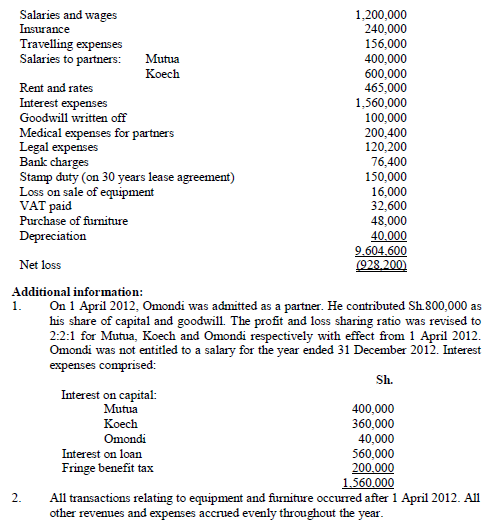

Mutua and Koech are in partnership trading as Mukoe Enterprises. They share profits and losses in the ratio of 2:3 for Mutua and Koech respectively. The partners presented the following income statement of the partnership for the year ended 31 December 2012:

Required:

i) The adjusted partnership profit or loss for the year ended 31 December 2012

ii) Distribution schedule of the profit or loss calculated in (b)(i) above

Required:

i) The adjusted partnership profit or loss for the year ended 31 December 2012

ii) Distribution schedule of the profit or loss calculated in (b)(i) above

Date posted:

February 13, 2019

-

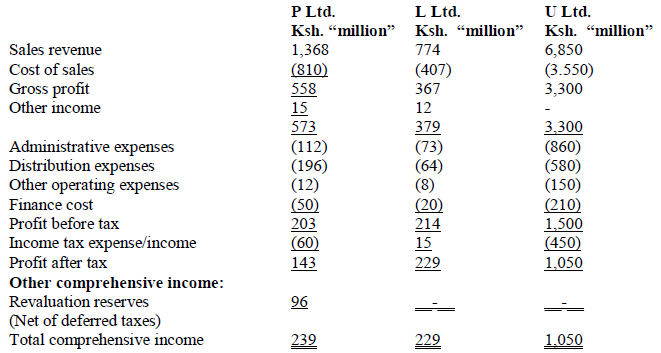

P Ltd., a company incorporated in Kenya is listed in all the East African securities exchanges. P Ltd. uses the Kenya shilling (Ksh.) as the reporting currency. On 1 April 2012, P Ltd. acquired a controlling interest in L Ltd.

On 1 October 2012, P Ltd. also acquired a controlling interest in U Ltd., a Ugandan. company that uses the Uganda shilling (Ush.) to report its financial results. The statements of comprehensive income for the three companies for the year ended 31 March 2013 are as set out below:

Additional information:

1. P Ltd. acquired 75% of L Ltd. through an exchange of 3.5 million equity shares of Ksh. 10 each.

The market value of the equity shares as at that date was Ksh.28 each. The fair value of the net assets of L Ltd, as at the date of acquisition was Ksh. 100 million.

2. P Ltd. acquired 60% of U Ltd. on 1 October 2012 for Ksh.47.5 million paid in cash. The fair value of the net assets of U Ltd. on that date amounted to Ush. 1,800 million. As at 31 March 2013, the exchange gain on retranslation of the net investment in U Ltd. was determined as Ksh.6.2 million.

3. During the year ended 31 March 2013, P Ltd. sold goods to L Ltd. for Ksh.28 million at cost plus 25%. 40% of these goods were still held within the group as at 31 March 2013.

4. P Ltd. operates some machines that pose an environmental hazard, for which they have an

irrevocable agreement to undertake decommissioning of the machines at the end of their useful life at a cost of Ksh. 18 million. The management estimates the remaining useful life of the machines to be 5 years and the relevant discount rate to be 12%. This item has not been accounted for.

5. The goodwill on acquisition of U Ltd. was considered to be impaired by 30% as at 31 March 2013.

6. On 1 January 2013, P Ltd. sold 1/3 (one third) of its investment in L Ltd. for a cash consideration of Ksh.62 million. The fair value of the net assets on that date was Ksh. 184 million. P Ltd. will account for the 50% interest in L Ltd. using the equity method in accordance with IFRS 11 (Joint Arrangements).

7. The following exchange rates are relevant:

Additional information:

1. P Ltd. acquired 75% of L Ltd. through an exchange of 3.5 million equity shares of Ksh. 10 each.

The market value of the equity shares as at that date was Ksh.28 each. The fair value of the net assets of L Ltd, as at the date of acquisition was Ksh. 100 million.

2. P Ltd. acquired 60% of U Ltd. on 1 October 2012 for Ksh.47.5 million paid in cash. The fair value of the net assets of U Ltd. on that date amounted to Ush. 1,800 million. As at 31 March 2013, the exchange gain on retranslation of the net investment in U Ltd. was determined as Ksh.6.2 million.

3. During the year ended 31 March 2013, P Ltd. sold goods to L Ltd. for Ksh.28 million at cost plus 25%. 40% of these goods were still held within the group as at 31 March 2013.

4. P Ltd. operates some machines that pose an environmental hazard, for which they have an

irrevocable agreement to undertake decommissioning of the machines at the end of their useful life at a cost of Ksh. 18 million. The management estimates the remaining useful life of the machines to be 5 years and the relevant discount rate to be 12%. This item has not been accounted for.

5. The goodwill on acquisition of U Ltd. was considered to be impaired by 30% as at 31 March 2013.

6. On 1 January 2013, P Ltd. sold 1/3 (one third) of its investment in L Ltd. for a cash consideration of Ksh.62 million. The fair value of the net assets on that date was Ksh. 184 million. P Ltd. will account for the 50% interest in L Ltd. using the equity method in accordance with IFRS 11 (Joint Arrangements).

7. The following exchange rates are relevant:

8. Incomes and expenses of all the three companies were deemed to accrue evenly throughout the year.

Required:

(a) Goodwill on acquisition of L Ltd. and U Ltd.

(b) Consolidated statement of comprehensive income for P Ltd. for the year ended 31 March 2013. (NB: Round off the Ush. to the nearest Kenya shilling)

8. Incomes and expenses of all the three companies were deemed to accrue evenly throughout the year.

Required:

(a) Goodwill on acquisition of L Ltd. and U Ltd.

(b) Consolidated statement of comprehensive income for P Ltd. for the year ended 31 March 2013. (NB: Round off the Ush. to the nearest Kenya shilling)

Date posted:

February 13, 2019

-

Outline four tax set-offs available to an individual tax payer

Date posted:

February 13, 2019

-

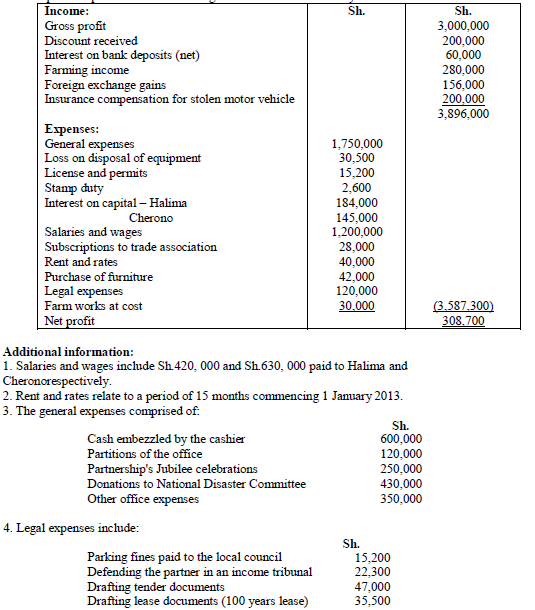

Halima and Cherono are partners trading as Hache Enterprises and sharing profits and losses in the ratio of 2: 1 respectively

The partners presented the Following income statement for the year ended 31 December 2013:

Required:

i. Adjusted partnership taxable profit or loss for the year ended 31 December 2013.

ii. Allocation of the taxable partnership profit or loss computed in (i) above.

Required:

i. Adjusted partnership taxable profit or loss for the year ended 31 December 2013.

ii. Allocation of the taxable partnership profit or loss computed in (i) above.

Date posted:

February 13, 2019

-

With reference to IAS 31 (Interests in Joint Ventures), explain the three types of joint ventures.

Date posted:

February 13, 2019

-

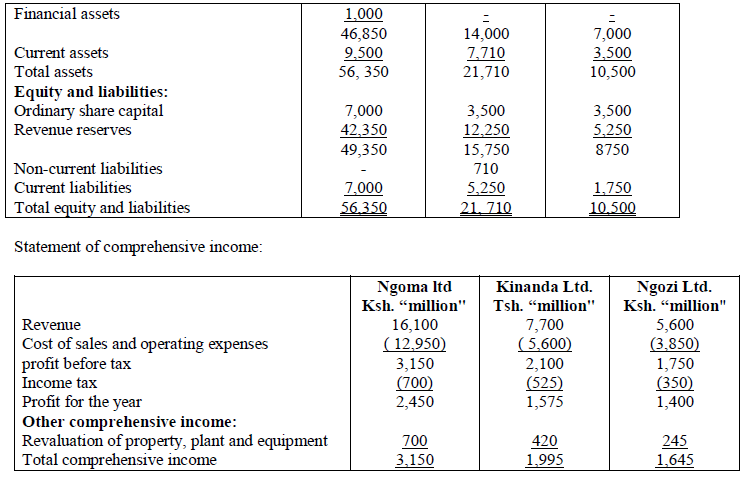

The following is an extract of the summarized financial statements of Ngoma Ltd, Kinanda Ltd. and Ngozi Ltd. for the year ended 30 September 2013:

Additional information:

1. The functional currency of both Ngoma Ltd. and Ngozi Ltd. is the Kenya shilling (Ksh.) while the functional currency of Kin and a Ltd. is the Tanzania shilling (Tsh.).

2. Ngoma Ltd. acquired 80% of Kinanda Ltd. on 1 October 2011 for Ksh.18, 200 million when the revenue reserves of Kinanda Ltd. were Tsh.6, 300 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

3. Ngoma Ltd. acquired 40% of Ngozi Ltd. on 1 October 2008 for Ksh.3, 150 million when the revenue reserves of Ngozi Ltd. were Ksh.2, 450 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

4. Ngoma Ltd. advanced a 5 year loan of Ksh.1, 000 million to Kinanda Ltd. on 30 September 2012. This loan is included in the financial assets and non-current liabilities of Ngoma Ltd. and Kinanda Ltd. respectively. Kinanda Ltd. had recorded the loan at the exchange rate prevailing as at 30 September 2012.

5. An impairment test conducted on 30 September 2013 revealed that cumulative impairment losses in respect of the investment in Ngozi Ltd. were Ksh.1 ,000 million, of which Ksh.250 million related to the current financial year. No impairment losses were necessary in respect of the investment in Kinanda Ltd.

6. The group's policy is to value the non-controlling interest at fair value at the date of acquisition. The fair value of the non-controlling interest of Kinanda Ltd. at 1 October 2011 was Tsh.2, 100 million.

7. Ngoma Ltd. has a building which is located in the same country as Kinanda Ltd. The building was acquired on 30 September 2012 and is carried at a cost of Tsh.2.500 million. The property is depreciated over 10 years on a straight line basis. As at 30 September 2013, the property was revalued to Tsh.3, 500 million. Depreciation has been charged for the year but the revaluation has not been taken into account in the preparation of financial statements as at 30 September 2013.

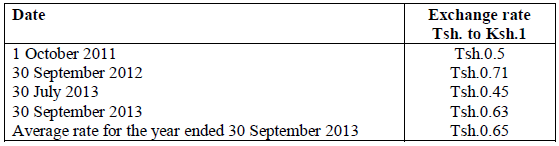

8. Relevant exchange rates are as follows:

Additional information:

1. The functional currency of both Ngoma Ltd. and Ngozi Ltd. is the Kenya shilling (Ksh.) while the functional currency of Kin and a Ltd. is the Tanzania shilling (Tsh.).

2. Ngoma Ltd. acquired 80% of Kinanda Ltd. on 1 October 2011 for Ksh.18, 200 million when the revenue reserves of Kinanda Ltd. were Tsh.6, 300 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

3. Ngoma Ltd. acquired 40% of Ngozi Ltd. on 1 October 2008 for Ksh.3, 150 million when the revenue reserves of Ngozi Ltd. were Ksh.2, 450 million. The investment is held at cost in the individual financial statements of Ngoma Ltd.

4. Ngoma Ltd. advanced a 5 year loan of Ksh.1, 000 million to Kinanda Ltd. on 30 September 2012. This loan is included in the financial assets and non-current liabilities of Ngoma Ltd. and Kinanda Ltd. respectively. Kinanda Ltd. had recorded the loan at the exchange rate prevailing as at 30 September 2012.

5. An impairment test conducted on 30 September 2013 revealed that cumulative impairment losses in respect of the investment in Ngozi Ltd. were Ksh.1 ,000 million, of which Ksh.250 million related to the current financial year. No impairment losses were necessary in respect of the investment in Kinanda Ltd.

6. The group's policy is to value the non-controlling interest at fair value at the date of acquisition. The fair value of the non-controlling interest of Kinanda Ltd. at 1 October 2011 was Tsh.2, 100 million.

7. Ngoma Ltd. has a building which is located in the same country as Kinanda Ltd. The building was acquired on 30 September 2012 and is carried at a cost of Tsh.2.500 million. The property is depreciated over 10 years on a straight line basis. As at 30 September 2013, the property was revalued to Tsh.3, 500 million. Depreciation has been charged for the year but the revaluation has not been taken into account in the preparation of financial statements as at 30 September 2013.

8. Relevant exchange rates are as follows:

Required:

a) Consolidated statement of comprehensive income for the year ended 30 September 2013.

b) Consolidated statement of financial position as at 30 September 2013.

Required:

a) Consolidated statement of comprehensive income for the year ended 30 September 2013.

b) Consolidated statement of financial position as at 30 September 2013.

Date posted:

February 13, 2019

-

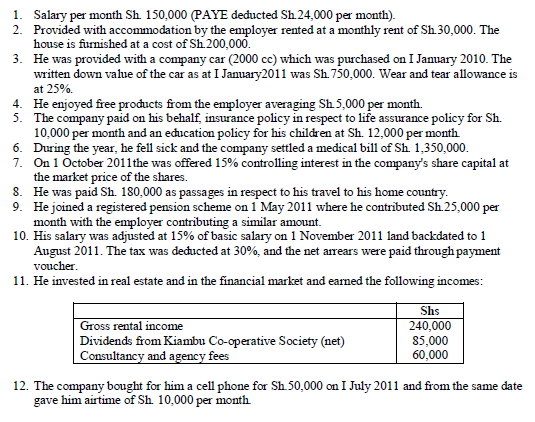

Mr. Herrad Makali is employed as a senior manager with Brook Enterprises Ltd. He holds 18% of the company's controlling interest.

The following details relate to Mr. Makali for the year ended 31 December 2013.

1. Basic salary Sh.82, 000 per month (PAYE Sh. 18,400 per month).

2. Benefits in kind for the year amounted to Sh.48, 000.

3. He was provided with a company car of 2000 cc whose cost was Sh.700, 000. The car was leased by the company at a monthly rent of Sh.24, 000. He also received a monthly fuel allowance of Sh.10, 000 for the car.

4. He was provided with a house by the employer. The house is rented from one of the company's directors at Sh40, 000 per month. The electricity is supplied from a generator installed by the company, the monthly expenses in relation to the generator amounted to Sh.30, 000.

5. On 1 May 2013, he moved to his own house which he had constructed through a 12% mortgage loan of Sh.2, 000,000. The loan had been obtained from National Housing Corporation on 1 October 2012.

6. He is a member of a registered pension scheme where he contributes Sh.18, 000 per month with the employer contributing an equal amount for him.

7. On 1October 2013, he secured an education insurance policy for his child at an annual premium of Sh.72, 000 payable by the company.

8. He reported a farming income of Sh. 98,000 after presumptive tax.

9. He was out of work station for 5 days for which he was paid per diem of Sh.4, 600 per day.

Required:

(i) Total taxable income of Mr Herrad Makali for the year ended 31 December 2013.

(ii) Tax due on the taxable income calculated in (i) above.

(iii) Comment on any information not used in your computations under (i) above.

Date posted:

February 13, 2019