-

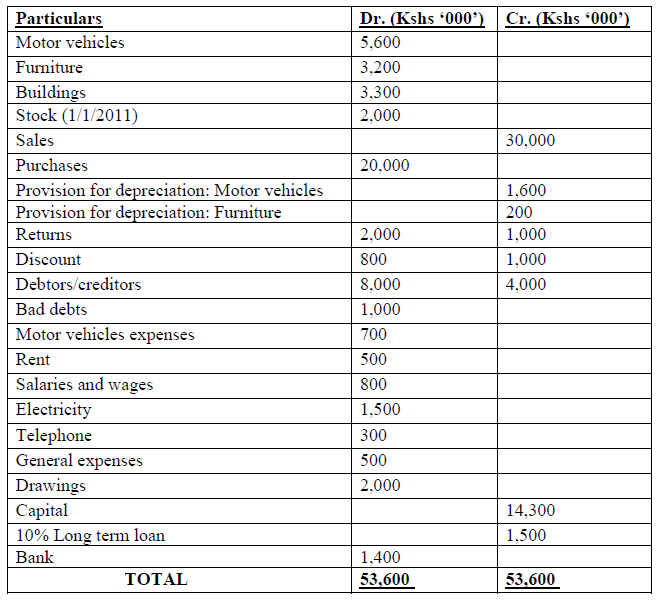

Maxwell is a sole proprietor operating business in Juja and the following trial balance relates to his business for the year ended 31st December, 2013.

Additional information

1. Stock at 31/12/2013 amount to Kshs 3,000,000

2. Motor vehicle expenses unpaid amount to Kshs 300,000.

3. A quarter of telephone bills relate to the year 2014.

4. Un paid electricity and water amount to Ksh 100,000

5. Depreciation on motor vehicles and fixtures is at 20% and 10% respectively on cost.

6. Salary and rent prepaid were Kshs 200,000 and Kshs 100,000 respectively.

7. Interest on loan was outstanding as at 31st December 2013.

Required

i. Income Statement for the year ended 31/12/2013.

ii. Balance sheet as at 31/12/2013.

Additional information

1. Stock at 31/12/2013 amount to Kshs 3,000,000

2. Motor vehicle expenses unpaid amount to Kshs 300,000.

3. A quarter of telephone bills relate to the year 2014.

4. Un paid electricity and water amount to Ksh 100,000

5. Depreciation on motor vehicles and fixtures is at 20% and 10% respectively on cost.

6. Salary and rent prepaid were Kshs 200,000 and Kshs 100,000 respectively.

7. Interest on loan was outstanding as at 31st December 2013.

Required

i. Income Statement for the year ended 31/12/2013.

ii. Balance sheet as at 31/12/2013.

Date posted:

August 17, 2021

-

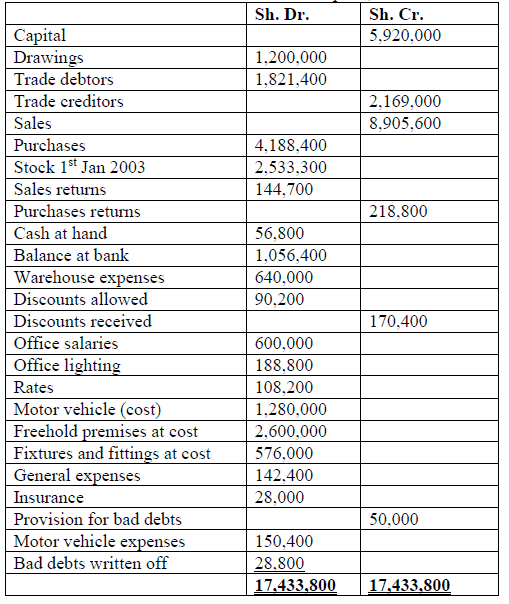

The following trial balance was extracted from books of Simpson, a sole trader as at 31st Dec 2013.

Additional information

1) Stock as at 31st Dec 2013 was valued at Sh. 1,760,000

2) Depreciation on fixtures and fittings and motor vehicle is provided at 5% and 10% p.a. on cost respectively.

3) Included in sales are goods for Sh. 13,000 ordered by Mr. Patel in the month of April. He has never communicated though the goods have been included in the closing stock.

4) Rates prepaid as at 31st Dec 2013 amounted to Sh. 25,600.

5) Unexpired insurance as at 31st Dec 2013 was Sh. 4,000.

6) Provision for bad debts as at 31st Dec 2013 is to be made at 2.5 % of net trade debtors.

Required

a) Trading and profit and loss account for year ended 31st Dec 2013

b) Balance sheet as at 31st Dec 2013.

Additional information

1) Stock as at 31st Dec 2013 was valued at Sh. 1,760,000

2) Depreciation on fixtures and fittings and motor vehicle is provided at 5% and 10% p.a. on cost respectively.

3) Included in sales are goods for Sh. 13,000 ordered by Mr. Patel in the month of April. He has never communicated though the goods have been included in the closing stock.

4) Rates prepaid as at 31st Dec 2013 amounted to Sh. 25,600.

5) Unexpired insurance as at 31st Dec 2013 was Sh. 4,000.

6) Provision for bad debts as at 31st Dec 2013 is to be made at 2.5 % of net trade debtors.

Required

a) Trading and profit and loss account for year ended 31st Dec 2013

b) Balance sheet as at 31st Dec 2013.

Date posted:

August 17, 2021

-

Describe an Income Statement.

Date posted:

August 17, 2021

-

A company depreciates its plant at the rate of 20% p.a. straight line method for each month of ownership.

On 1st January 1999 bought plant costing Sh. 9,000. On 1st October 1999 also bought plant costing Sh. 6,000. On 1st July 2001 bought plant costing Sh. 5,500.

On 30th September 2002, the plant that had been bought for Sh. 9,000 on 1st January 1999 was sold for Sh. 2,750.

Required:

(a) Plant A/c

(b) Provision for depreciation A/c

(c) Disposal A/c

Date posted:

August 17, 2021

-

XYZ Ltd has three machines in operation. Machine A was bought on 1st January 2013 at Ksh 250,000 and the other two machines; machine B and machine C were bought on 1st January 2014 at Ksh 350,000 and Ksh 300,000 respectively. The business has a policy to depreciate all non current assets at 15% using straight line basis of depreciation. On 1st July 2014, XYZ Ltd disposed off the machine bought on 1st January 2013 for Ksh 188,000. Assuming that the financial year of XYZ Ltd ends on 31st December.

Prepare the following accounts relating to financial year ending 31st December 2014 only.

i. Machine Account

ii. Provision for depreciation Account

iii. Disposal Account

Date posted:

August 17, 2021

-

A business firm started trading on 1st January in year 2013. On 1st April, it bought a new motor vehicle costing Ksh 400,000 and later on 1st July it bought another motor vehicle costing Ksh 550,000. The financial year for the business ends on 31st December and it has a policy of depreciating motor vehicles at 20% p.a. using straight line basis.

Required:

i. Motor vehicle account as at 31st December 2013

ii. Provision for depreciation account as at 31st December 2013

iii. Income statement extract for year ending 31st December 2013

iv. Cash/ bank account extract

Date posted:

August 17, 2021

-

A company purchased a machine at a cost of Sh. 450,000. The estimated life of this machine is 5 years. Using the sum of years digits determine its depreciation.

Date posted:

August 17, 2021

-

Calculate the reducing balance depreciation charged at 20% for the first 3 years on a machine bought for Sh. 10,000.

Date posted:

August 17, 2021

-

Define the Reducing Balance Method of calculating depreciation.

Date posted:

August 17, 2021

-

Describe the Straight Line Method of calculating depreciation.

Date posted:

August 17, 2021

-

A Machine was bought for Sh. 220,000 and it was estimated to be in operation for 4 years with a residue value of Sh. 20,000. Calculate the depreciation expense for each year.

Date posted:

August 17, 2021

-

A business firm that had previously written of bad debts amounting to Ksh 34,000 now recovers the same amount that was paid by cheque. In the same financial year the debtor account amount to Ksh 270,000 and out of this the firm will write off bad debts amounting Ksh 20,000.

Required:

i. Debtors Account

ii. Bad debts (written off) Account

iii. Bad debts recovered Account

iv. Bank Account

Date posted:

August 17, 2021

-

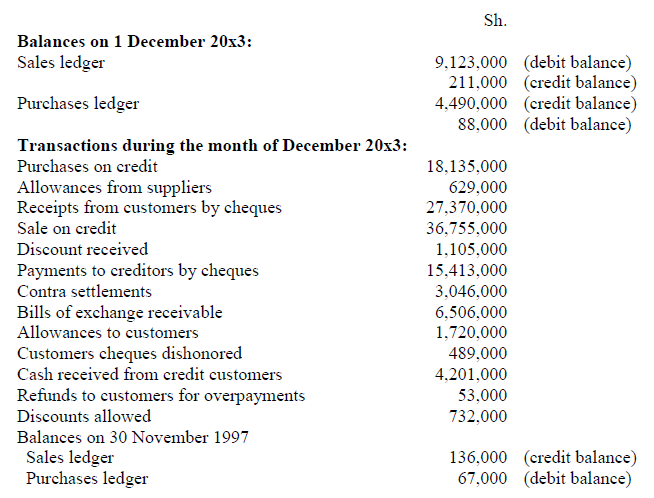

XYZ Ltd started trading on 1 January 2013. The following are some of the bad debts that were written off during two years that XYZ Ltd has been trading.

On 31 December 20x3 debtors balance was Ksh 4,050,000. Provision for bad debts was maintained at 3%.

On 31 December 20x4 debtors balance increased to Ksh 4,730,000. Provision for bad debts was maintained at 5%.

Required:

i. Debtors Account for the two years

ii. Bad debts Account for the two years

iii. Provision for bad debts Accounts for the two years

iv. Income statement Extract for the two years

v. Balance sheet Extract for the two years

On 31 December 20x3 debtors balance was Ksh 4,050,000. Provision for bad debts was maintained at 3%.

On 31 December 20x4 debtors balance increased to Ksh 4,730,000. Provision for bad debts was maintained at 5%.

Required:

i. Debtors Account for the two years

ii. Bad debts Account for the two years

iii. Provision for bad debts Accounts for the two years

iv. Income statement Extract for the two years

v. Balance sheet Extract for the two years

Date posted:

August 17, 2021

-

The debtors account for ABC Ltd was Ksh 500,000 by end of the year 2013. Bad debts amounting to Ksh 50,000 were written off from this balance. The specific provision stood at Ksh 10,000 while the general provision was maintained at 5% on the debtors balance.

Required:

i. Debtors Account

ii. Bad debts Account

iii. Provision for bad debts Accounts

iv. Income statement Extract

v. Balance sheet Extract

Date posted:

August 17, 2021

-

Define Accrued Expenses.

Date posted:

August 17, 2021

-

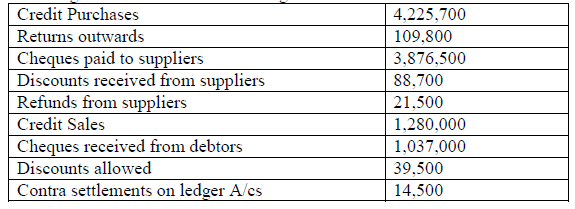

The following transactions relate to Jaime Ltd for the month of December 2013. Prepare sales ledger and purchases ledger control account for that month.

Date posted:

August 17, 2021

-

The following information relates to Zeta Ltd for the month of June, 2013.

Balances as at 1st June,2013

Sales Ledger Sh. 642,000 on Debit side

Purchases Ledger Sh. 103,700 on Credit side

The following were the transactions during the month

Compute the information to Purchases and Sales ledger accounts.

Compute the information to Purchases and Sales ledger accounts.

Date posted:

August 17, 2021

-

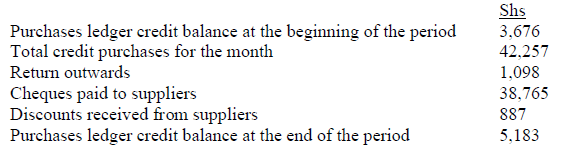

Prepare a Purchases Ledger Control A/c from the following details for the month of June 2008.

Date posted:

August 17, 2021

-

State the items that decrease creditor’s balance.

Date posted:

August 17, 2021

-

State the items that increase creditor’s balance.

Date posted:

August 17, 2021

-

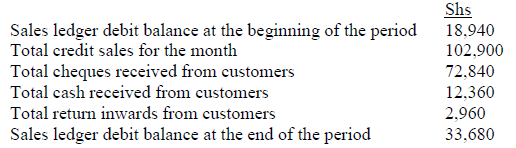

Draw a Sales Ledger control A/c to record the following details relating to a business.

Date posted:

August 17, 2021

-

State the items that decrease debtor’s balance.

Date posted:

August 17, 2021

-

State the items that increase debtor’s balance.

Date posted:

August 17, 2021

-

What are Control Accounts?

Date posted:

August 17, 2021

-

The following cash book relates to Jockey Ltd for the month of October, 2013. The bank statement had a debit balance of Sh 1,353,000.

On investigation the following was discovered;

1. Bank charges of Sh. 136,000 in the bank statement have not been reflected in the cash book.

2. Cheques drawn amounting to Sh. 267,000 had not been presented to the bank for payment.

3. Cheques received totaling to Sh. 726,000 had been entered in the cash book but credited by the bank by 3rd November.

4. A cheque for Sh. 22,000 for expenses had been entered in the cash book as a receipt instead of a payment

5. A cheque received from John for Sh. 80,000 had been returned by the bank and marked “No Funds Available”. No adjustment has been made in the cash book

6. A standing order for business rates of Ksh 150,000 on 30th October had not been entered in the cash book.

7. Dividends of Sh. 62,000 were received and credited directly to the bank account with no entries in the cash book.

8. A cheque drawn for Sh. 66,000 for stationery had been incorrectly entered in the cash book as Sh. 60,000.

9. The balance brought forward in the cash book should have been Sh. 711,000 not Sh. 761,000.

Required:

Prepare an adjusted cash book and a bank reconciliation statement as at 31 October, 20x3 to reconcile the difference in the cash book and bank statement balance.

On investigation the following was discovered;

1. Bank charges of Sh. 136,000 in the bank statement have not been reflected in the cash book.

2. Cheques drawn amounting to Sh. 267,000 had not been presented to the bank for payment.

3. Cheques received totaling to Sh. 726,000 had been entered in the cash book but credited by the bank by 3rd November.

4. A cheque for Sh. 22,000 for expenses had been entered in the cash book as a receipt instead of a payment

5. A cheque received from John for Sh. 80,000 had been returned by the bank and marked “No Funds Available”. No adjustment has been made in the cash book

6. A standing order for business rates of Ksh 150,000 on 30th October had not been entered in the cash book.

7. Dividends of Sh. 62,000 were received and credited directly to the bank account with no entries in the cash book.

8. A cheque drawn for Sh. 66,000 for stationery had been incorrectly entered in the cash book as Sh. 60,000.

9. The balance brought forward in the cash book should have been Sh. 711,000 not Sh. 761,000.

Required:

Prepare an adjusted cash book and a bank reconciliation statement as at 31 October, 20x3 to reconcile the difference in the cash book and bank statement balance.

Date posted:

August 17, 2021

-

Haze Ltd had a Credit balance of Ksh 351,300 in the bank statement and a debit balance of Ksh 389,600. Upon investigation the following transactions were missing in the books of accounts.

Date posted:

August 17, 2021

-

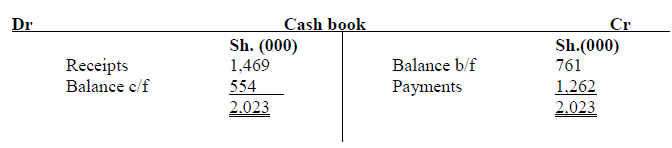

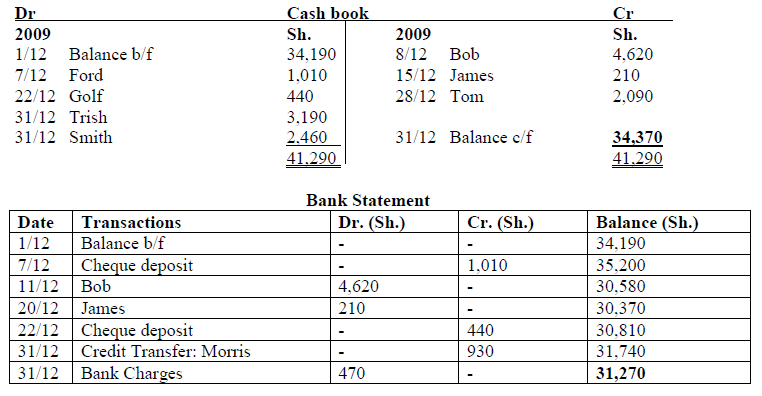

The following bank statement and cash book relates to Sunshine Enterprises. Prepare an updated cash book and a bank reconciliation statement to explain the difference in their balance as on 31st December 2013.

Date posted:

August 17, 2021

-

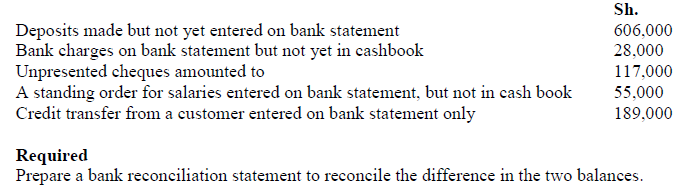

Outline the steps in preparing a bank reconciliation statement.

Date posted:

August 17, 2021

-

State and explain the items appearing in the bank statement and not reflected in the cashbook.

Date posted:

August 17, 2021

-

Explain the items that appear in The Cashbook and do not reflect in the Bank Statement.

Date posted:

August 17, 2021