-

Bara Ltd. is contemplating a bid for the share capital of Pwani Ltd. with an intention of buying the whole company. The following data for the two companies have been provided.

After acquisition, Bara Ltd. intends to sell a division of Pwani Ltd. which accounts for Sh.20 million

annually in equity earnings. The division does not form part of the core business of the intended group. The

division has a current market price of Sh. 50 million.

Bara Ltd.'s management believes that by introducing better management, earnings of Pwani Ltd. could

be permanently increased by 25% although the price/earnings multiple will remain the same. To avoid duplication,

some of Bara Ltd.'s own property could be disposed of at an estimated price of Sh. 130 million.

Rationalization costs are estimated at Sh. 100 million, these comprise retrenchment and legal costs

among others.

Required:

(a) Highlight the advantages of growth by acquisition.

(b) Calculate the effect on the current share price of each company, all other things being equal, of a two for

ten share offer by Bara Ltd., assuming that Bara Ltd.'s estimates are in line with those of the market.

(c) Assume that Bara Ltd. is proposing to offer Pwani Ltd.'s shareholders the choice of a two for ten

share exchange or a cash alternative. Giving reasons, advise Bara Ltd. whether the cash alternative

should be more or less that the current value of the share exchange.

After acquisition, Bara Ltd. intends to sell a division of Pwani Ltd. which accounts for Sh.20 million

annually in equity earnings. The division does not form part of the core business of the intended group. The

division has a current market price of Sh. 50 million.

Bara Ltd.'s management believes that by introducing better management, earnings of Pwani Ltd. could

be permanently increased by 25% although the price/earnings multiple will remain the same. To avoid duplication,

some of Bara Ltd.'s own property could be disposed of at an estimated price of Sh. 130 million.

Rationalization costs are estimated at Sh. 100 million, these comprise retrenchment and legal costs

among others.

Required:

(a) Highlight the advantages of growth by acquisition.

(b) Calculate the effect on the current share price of each company, all other things being equal, of a two for

ten share offer by Bara Ltd., assuming that Bara Ltd.'s estimates are in line with those of the market.

(c) Assume that Bara Ltd. is proposing to offer Pwani Ltd.'s shareholders the choice of a two for ten

share exchange or a cash alternative. Giving reasons, advise Bara Ltd. whether the cash alternative

should be more or less that the current value of the share exchange.

Date posted:

April 19, 2021

-

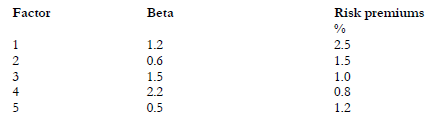

As a senior financial analyst of an investment bank, you are charged with the responsibility of

estimating the expected returns of various securities. One o the securities you want to estimate is

expected return in Alpha Steel works Ltd.

You have decided to use arbitrage pricing model and you have derived the following estimates

for the factor betas and risk premiums.

Required:

(i) Identify the risk factor for Alpha Steel Works Ltd.

(ii) If the risk free rate is 5%, estimate the expected return on Alpha Steel Works Ltd.

Required:

(i) Identify the risk factor for Alpha Steel Works Ltd.

(ii) If the risk free rate is 5%, estimate the expected return on Alpha Steel Works Ltd.

Date posted:

April 19, 2021

-

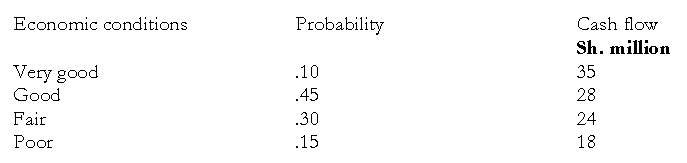

Goldstar Manufacturing Limited is evaluating an investment opportunity that would require an

outlay of sh.100 million. The annual net cash inflows are estimated to vary according to economic

conditions.

The firm's required rate of return is 14 percent. The project has an expected life of six years.

Required:

Compute the expected net present value (NPV) of the proposed investment.

The firm's required rate of return is 14 percent. The project has an expected life of six years.

Required:

Compute the expected net present value (NPV) of the proposed investment.

Date posted:

April 18, 2021

-

Juma Company Ltd. Which is effectively controlled by the Juma family although they own only a minority of shares, is to undertake a substantial new project which requires external finance of about Sh.400 million, leading to a 40% increase in gross assets. The project is to develop and market a new product and is fairly risky. About 70% of the funds required will be spent on land and buildings. The resale value of the land and buildings is expected to remain equal to or greater than, the initial purchase price. Expenditure during the development period of the first 4 to 7 years will be financed from other revenue of Juma Company Ltd. This

will have a consequent strain on the company's overall liquidity.

If, after the development stage, the project proves unsuccessful, then the project will be terminated and its assets sold. If, as is likely, the development is successful, the project's assets will be utilized in production and the company's profits will rise considerably. However, if the project proves to be very successful, then additional finance may be required to further expand the production facilities.

At present, Juma Company Ltd. Is all equity financed.

The financial manager is uncertain whether he should seek funds from a financial institution in the form of an equity interest, a loan (long or short term) r convertible debentures.

Required:

(a) Describe the major factors to be considered by Juma Company Ltd. In deciding on the method of

financing the proposed expansion project.

(b) Briefly discuss the suitability of equity, loans and convertible debentures for the purpose of

financing the project from the point of view of:

(i) Juma Company Ltd.

(ii) The provider of finance.

Clearly state and justify the type of finance recommended for Juma Company Ltd.

Date posted:

April 17, 2021

-

Discuss the importance and limitations of Executive Share Option Plans (ESOPs) in mitigating

management/shareholder agency conflicts.

Date posted:

April 17, 2021

-

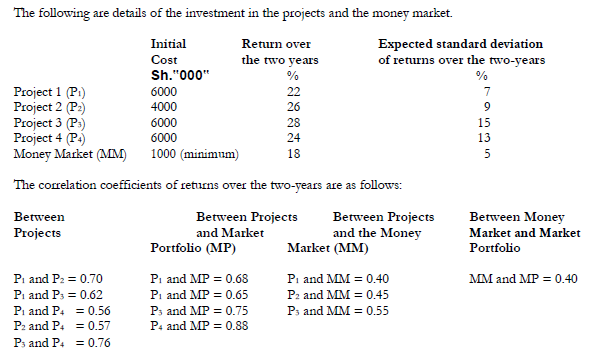

Tom Donji an investment specialist has been entrusted with Sh.10 million by a unit trust and instructed to invest the money optimally over a two-year period. Part of the instructions are that:

The funds be invested in one or more of four specified projects and in the money market

The four projects are not divisible and cannot be postponed.

The unit requires a return of 24% over the two years.

Over the two-year period, the risk free rate is estimated to be 16%, the market portfolio return, 27% and

the variance of the return on the market, 100%.

Required:

By analyzing the two-asset portfolios:

i ) Use the mean-variance dominance rule to evaluate how Tom Donji should invest the Sh.10 million.

ii) Determine the betas and required rates of return for the portfolios and then use the Capital Asset

Pricing Model (CAPM) to evaluate how Tom Donji should invest the Sh.10 million.

Over the two-year period, the risk free rate is estimated to be 16%, the market portfolio return, 27% and

the variance of the return on the market, 100%.

Required:

By analyzing the two-asset portfolios:

i ) Use the mean-variance dominance rule to evaluate how Tom Donji should invest the Sh.10 million.

ii) Determine the betas and required rates of return for the portfolios and then use the Capital Asset

Pricing Model (CAPM) to evaluate how Tom Donji should invest the Sh.10 million.

Date posted:

April 17, 2021

-

What are the limitations of the Capital Asset Pricing Model (CAPM) as an investment appraisal technique?

Date posted:

April 17, 2021

-

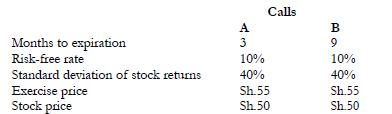

The following data relate to call options on two shares, A and B

Required:

Using the Black-Scholes Option Pricing Model (OPM).

Calculate the price of call option A. Of the two call options, which would you expect to have the higher price? Why? (Do not compute).

Required:

Using the Black-Scholes Option Pricing Model (OPM).

Calculate the price of call option A. Of the two call options, which would you expect to have the higher price? Why? (Do not compute).

Date posted:

April 17, 2021

-

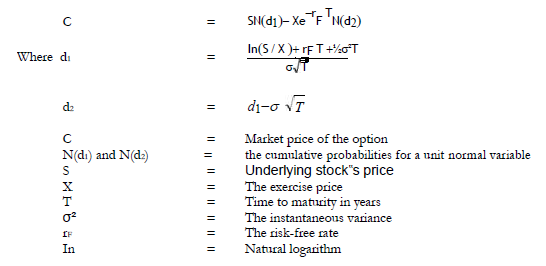

Given below is the Option Pricing Model (OPM) derived by Black and Scholes in 1973 for predicting the market price of call options.

Required:

State and briefly explain the relationship between a call option‟s price and the following determinants:

1) the underlying stock‟s price.

2) the exercise price

3) the time to maturity

4) the risk-free rate.

Required:

State and briefly explain the relationship between a call option‟s price and the following determinants:

1) the underlying stock‟s price.

2) the exercise price

3) the time to maturity

4) the risk-free rate.

Date posted:

April 17, 2021

-

City Graphics Limited is evaluating a new technology for its reproduction equipment. The technology will have a

three-year life and would cost Sh.800,000. Its impact on the company‟s cash flows is subject to risk.

In the first year, management estimates that there is an equal chance that the technology will either

succeed and save the company Sh.800,000 or fail saving it nothing at all.

If the technology fails in the first year, savings in the last two years will be zero. Even worse, there is a 40%

chance that additional Sh.240,000 may be required in the second year to convert back to the original process.

If the technology succeeds in the first year, the second year cash flows may be Sh.1,440,000, Sh.1,120,000 or

Sh.800,000 with probabilities of 0.20, 0.60 or 0.20 respectively. Third year cash flows are then expected to be

Sh.160,000 greater or Sh.160,000 less than cash flows in the second year, with equal chance of either

occurring.

All the cash flows above are after taxes.

Required:

a) A probability tree depicting the above cash flow possibilities.

b) Net present values for each possibility using a risk-free rate of 5%.

c) The expected net present value of the technology using a risk-free rate of 5%

Date posted:

April 17, 2021

-

Explain with the aid of a diagram a protective put buying strategy.

Date posted:

April 16, 2021

-

Explain and illustrate graphically the options concepts of being:

i) “at the money”

ii) “in the money”

iii) “out of the money”

for both a call and put option.

Date posted:

April 16, 2021

-

Using a numeric example, illustrate and explain the pay-offs of a futures option and a futures

contract.

Date posted:

April 16, 2021

-

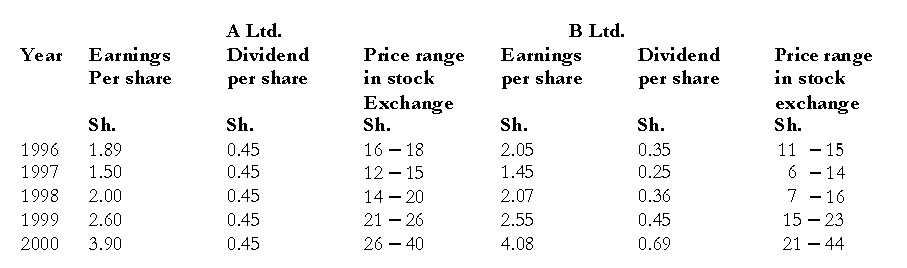

A comparative study of the records of two oil companies, A Ltd. and B Ltd., in terms of their asset composition, capital structure and profitability shows that they have been very similar for the past five years. The only significant difference between the two firms is their dividend policy. A Ltd. maintains a constant dividend per share while B Ltd. maintains a constant dividend pay-out ratio. Relevant data is as follows:

Required:

a) For each company, determine the dividend pay-out ratio and the price – earnings ratio for each of

the five years.

b) B Ltd‟s management is surprised that the shares of this company have not performed as well

as A Ltd‟s in the stock exchange. What explanation would you offer for this state of affairs?

c) Comment on the applicability of the Simple Price/Earnings (P/E) ratio to the typical technology

(IT) company with a high valuation and heavy losses.

Required:

a) For each company, determine the dividend pay-out ratio and the price – earnings ratio for each of

the five years.

b) B Ltd‟s management is surprised that the shares of this company have not performed as well

as A Ltd‟s in the stock exchange. What explanation would you offer for this state of affairs?

c) Comment on the applicability of the Simple Price/Earnings (P/E) ratio to the typical technology

(IT) company with a high valuation and heavy losses.

Date posted:

April 16, 2021

-

A Kenyan company has agreed to sell goods to an importer in Zedland at an invoiced price of

Z 150,000 (Zed (Z) is the currency of Zedland). Of this amount, Z 60,000 will be payable on

shipment, Z 45,000 one month after shipment and Z 45,000 three months after shipment.

The quoted foreign exchange rates (Z per KSh.) at the date of shipment as as follows:

Spot 1.690 - 1.692

One month 1.687 - 1.690

Three months 1.680 - 1.684

The company decides to enter into appropriate forward exchange contracts through a bank in

order to hedge these transactions.

Required:

i) State the advantages of hedging in this way.

ii) Calculate the amount in Kenya Shillings that the Kenyan Company would receive.

iii) Comment with hindsight on the wisdom of hedging in this instance, assuming that the spot rates at

the dates of receipt of the two instalments of Z 45,000 were as follows:

Fist instalment 1.69 - 1.69

Second instalment 1.700 - 1.704

Date posted:

April 16, 2021

-

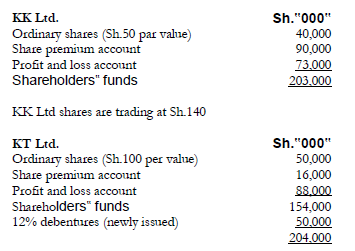

KK Ltd. and KT Ltd. are two companies in the printing industry. The companies have the same business

risk and are almost identical in all respects for their capital structures and total market values. The companies

capital structures are summarized below:

KT‟s ordinary shares are trading at Sh.170 and debentures at Sh.100. Annual earnings

before interest and tax for each company is Sh.50 million.

Corporate tax is at the rate of 30%.

Required:

a) If you owned 4% of the ordinary shares of KT Ltd. and you agreed with the arguments of

Modigliani and Miller, explain what action you would take to improve your financial position.

b) Estimate by how much your financial position is expected to improve. Personal taxes may be

ignored and assumptions made by Modigliani and Miller may be used.

c) If KK Ltd. was to borrow Sh.40 million, compute and explain the effect this would have on the

company‟s cost of capital according to Modigliani and Miller. What implications would this suggest

for the company‟s choice of capital structure?

KT‟s ordinary shares are trading at Sh.170 and debentures at Sh.100. Annual earnings

before interest and tax for each company is Sh.50 million.

Corporate tax is at the rate of 30%.

Required:

a) If you owned 4% of the ordinary shares of KT Ltd. and you agreed with the arguments of

Modigliani and Miller, explain what action you would take to improve your financial position.

b) Estimate by how much your financial position is expected to improve. Personal taxes may be

ignored and assumptions made by Modigliani and Miller may be used.

c) If KK Ltd. was to borrow Sh.40 million, compute and explain the effect this would have on the

company‟s cost of capital according to Modigliani and Miller. What implications would this suggest

for the company‟s choice of capital structure?

Date posted:

April 16, 2021

-

Jabali Ltd. is a quoted company which is financed by 10,000,000 ordinary shares and Sh.50,000,000 of

irredeemable 8% debentures. The market value of the shares is Sh.20 each ex-div and an annual dividend of

Sh.4 per share is expected to be paid in perpetuity. The debentures are considered to be risk-free and are

valued at par.

Mr. Jabali the managing director of the company is wondering whether to invest in a project which cost

Sh.20 million and yield Sh.3.8 million a year before tax in perpetuity. The project has an estimated beta value

of 1.25. The return from a well-diversified market portfolio is 16%.

Required:

a) The weighted average cost of capital of the company.

b) The beta of the company.

c) The beta of an equivalent ungeared company ignoring taxes.

d) Advise the company whether/or not the project should be accepted. In your explanation, highlight

the significance of your calculations in (a), (b) and (c) above.

Date posted:

April 16, 2021

-

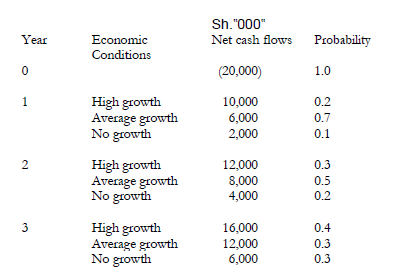

Company A is considering investing in a project which has a three year life. The project would involve an initial investment of Sh.20 million. The finance manager has come up with expected probabilities for various possible economic conditions as follows:

Required:

Assuming a discount rate of 15% should company A invest in the project?

Required:

Assuming a discount rate of 15% should company A invest in the project?

Date posted:

April 16, 2021

-

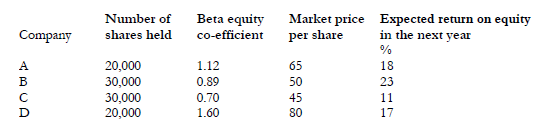

Mr. Mlachake is currently holding a portfolio consisting of shares of four companies quoted on the Bahati Stock Exchange as follows:

The current market return is 14% per annum and the treasury bills yield is 9% per annum.

Required:

(i) Calculate the risk of Mlachake‟s portfolio relative to that of the market.

(ii) Explain whether or not Mlachake should change the composition of his portfolio.

The current market return is 14% per annum and the treasury bills yield is 9% per annum.

Required:

(i) Calculate the risk of Mlachake‟s portfolio relative to that of the market.

(ii) Explain whether or not Mlachake should change the composition of his portfolio.

Date posted:

April 16, 2021

-

What part of the Companies Act relates to foreign companies?

Date posted:

April 15, 2021

-

Outline the examples of access controls.

Date posted:

April 15, 2021

-

State the similarities between debentures and shares.

Date posted:

April 15, 2021

-

State the advantages of a trust deed.

Date posted:

April 15, 2021

-

State the disadvantages of floating charges.

Date posted:

April 15, 2021

-

What chapter number of the laws of Kenya is the Cooperatives Societies Act?

Date posted:

April 15, 2021

-

What is the maximum number of persons in a sole trader?

Date posted:

April 15, 2021

-

What are the two fundamental principles of company law?

Date posted:

April 15, 2021

-

State and explain the types of euro-currency loans.

Date posted:

April 15, 2021

-

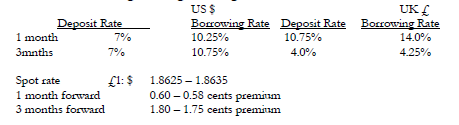

XYZ Ltd, a UK firm has bought goods from a US supplier and must pay USD 4 million in 3 months time.

The company finance director wishes to hedge against the foreign exchange risk and is considering 3

methods:

- Using the forward exchange contract

- Using the money market hedge

- Using a lead payments

Annual interest rate and foreign exchange rate are given below:

Required

Advise the company on the best method to use.

Required

Advise the company on the best method to use.

Date posted:

April 15, 2021

-

Assume that the foreign currency (F) has been quoted against the £ as follows :

Spot rate £1: F2156 – 2166

3 months forward rate £1: F2207 – 2222

Required:

1. Determine the amount required in sterling pound to buy 2 million foreign currencies

• At the spot

• In 3 months time under the forward exchange contract.

2. Compute the amount a customer would get if he were to sell 2 million foreign currency.

• At the spot rate

• In 3 months time under forward exchange contract

Date posted:

April 15, 2021